S&P Global Commodity Insights’ European Electricity Long-Term Forecast report, published on March 29, 2022, offers an in-depth outlook for the power fundamentals across Western Europe through 2050, with annual and monthly forecasts for both baseload and wind and solar generator capture prices. Given the current market and geopolitical turmoil, in addition to our updated Reference Case, we have created an additional case called “New World” which explores how the current impetus to reduce dependence on gas, and in particular Russian gas, at an accelerated pace might impact European power demand, supply, and prices over the long-term.

The following represent the major takeaways through 2050 for the ten European countries analyzed (including Austria, Belgium, France, Germany, Great Britain, Italy, Netherlands, Portugal, Spain and Switzerland):

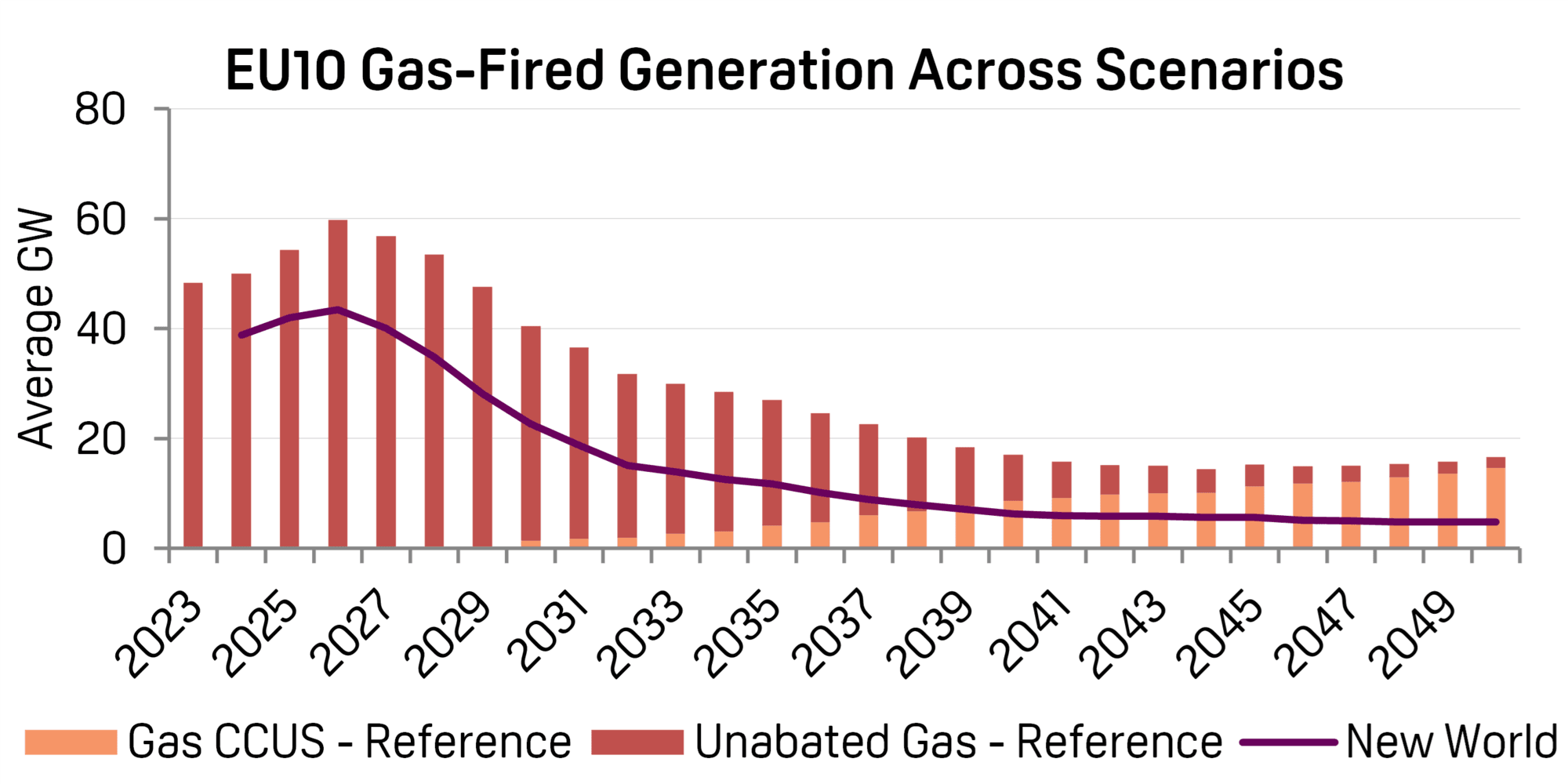

1. Gas: The bridge is collapsing.

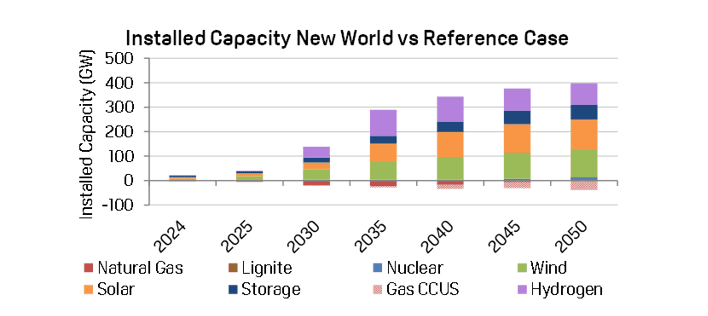

The current impetus to reduce the dependence on Russian gas is further weakening the role of gas as a bridge fuel in Europe. The “New World Case” assumes gas prices remain at elevated levels through at least this decade. Relative to our Reference Case, this leads to a larger decline in unabated gas capacity by over 25% by 2030 and around 50% by 2035, while gas-fired generation falls by, 60% and 80% vs 2021 levels, respectively. An accelerated gas phase out poses additional risks of a capacity crunch in the medium term across Western Europe. We see Germany capacity balances tightening considerably in this decade relative to the rest of the Continent, given that declining gas capacity coincides with the phase out of coal and nuclear. Italian wholesale power prices are also set to be supported, given that this market has a larger reliance on (Russian) gas.

Not only are the prospects for new unabated gas units drastically reduced, but the appetite to scale up gas with carbon capture, utilization and storage (CCUS) is likely to be tepid, reducing a key source of power sector flexibility post-2030.

2. Renewables and power storage win. Capture prices benefit from current market dynamics, but cannibalization risks remain a concern post 2030.

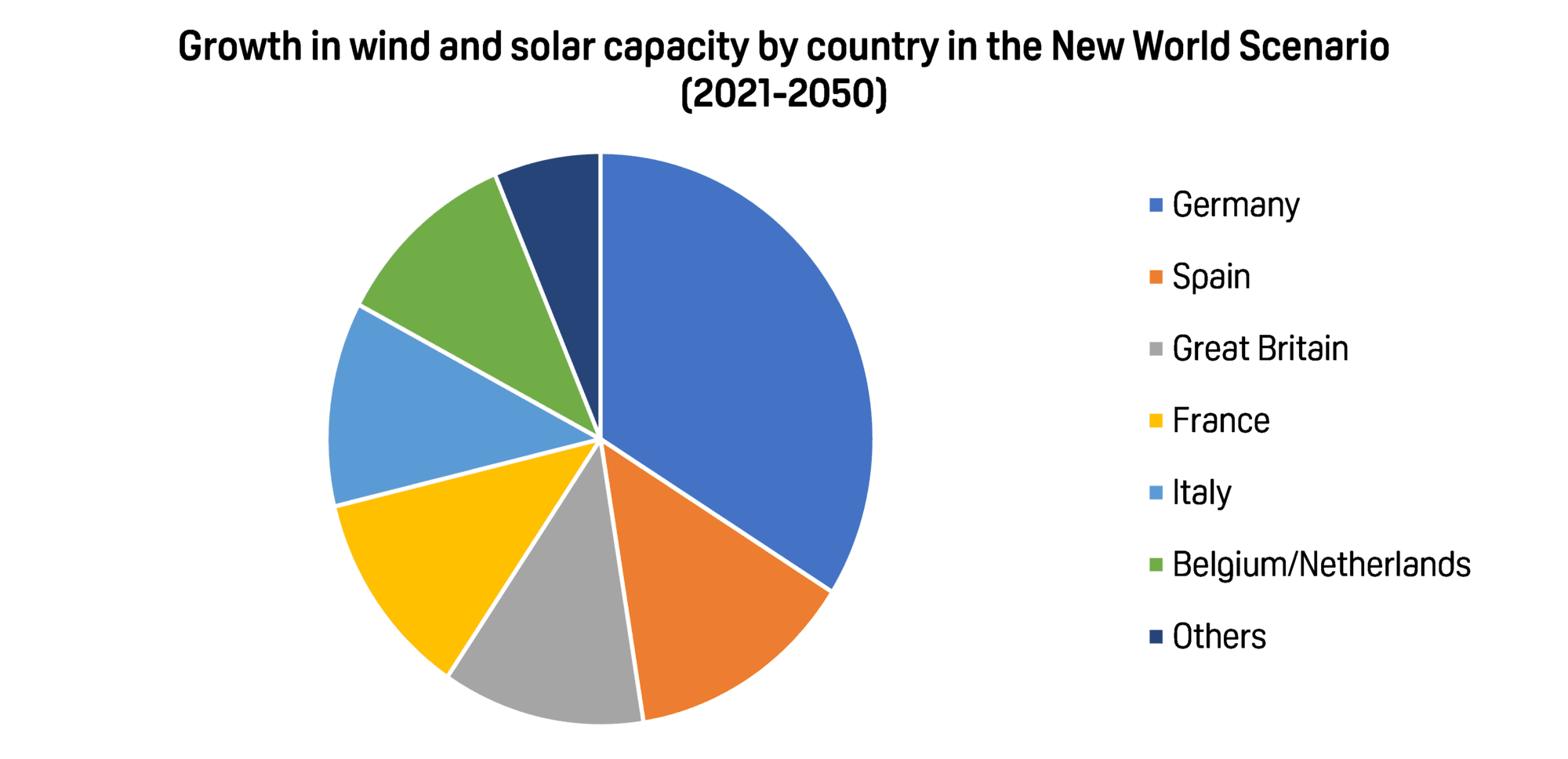

Recent events and policy developments from the European Commission and governments signal a steeper growth trajectory for renewables. Solar capacity will be the technology of choice in terms of total capacity additions across the EU 10, with up to 27 GW/year of additions, versus around 18 GW/year of wind (equally split between onshore and offshore), more than twice the installation trends seen in the past decade. Thanks to its higher capacity utilization, wind generation accounts for almost 50% of the mix by 2050 and becomes more influential in setting power prices. The additional wind and solar capacity accounts for more than 70% of the incremental investments in power generation needed in the “New World” Scenario, which could be quantified in about euro 20bn/year (2020 real) through 2035 (excluding investments in transmission). Although rising raw materials prices are underpinning renewables CAPEX, a higher gas price environment, together with faster electrification of heating, offer greater upsides for renewables capture prices in this decade. However, higher renewables penetration still leads to cannibalization risks for plant revenues, with solar PV the most exposed technology, even with substantial additions of co-located storage/batteries. Offshore wind projects also face these risks post 2030. In the GB market, wind projects will capture a higher percentage of baseload prices, however the capture price achieved sits at a discount to the other major markets by 2050.

3. Resource nationalism and promotion of energy independence a reality.

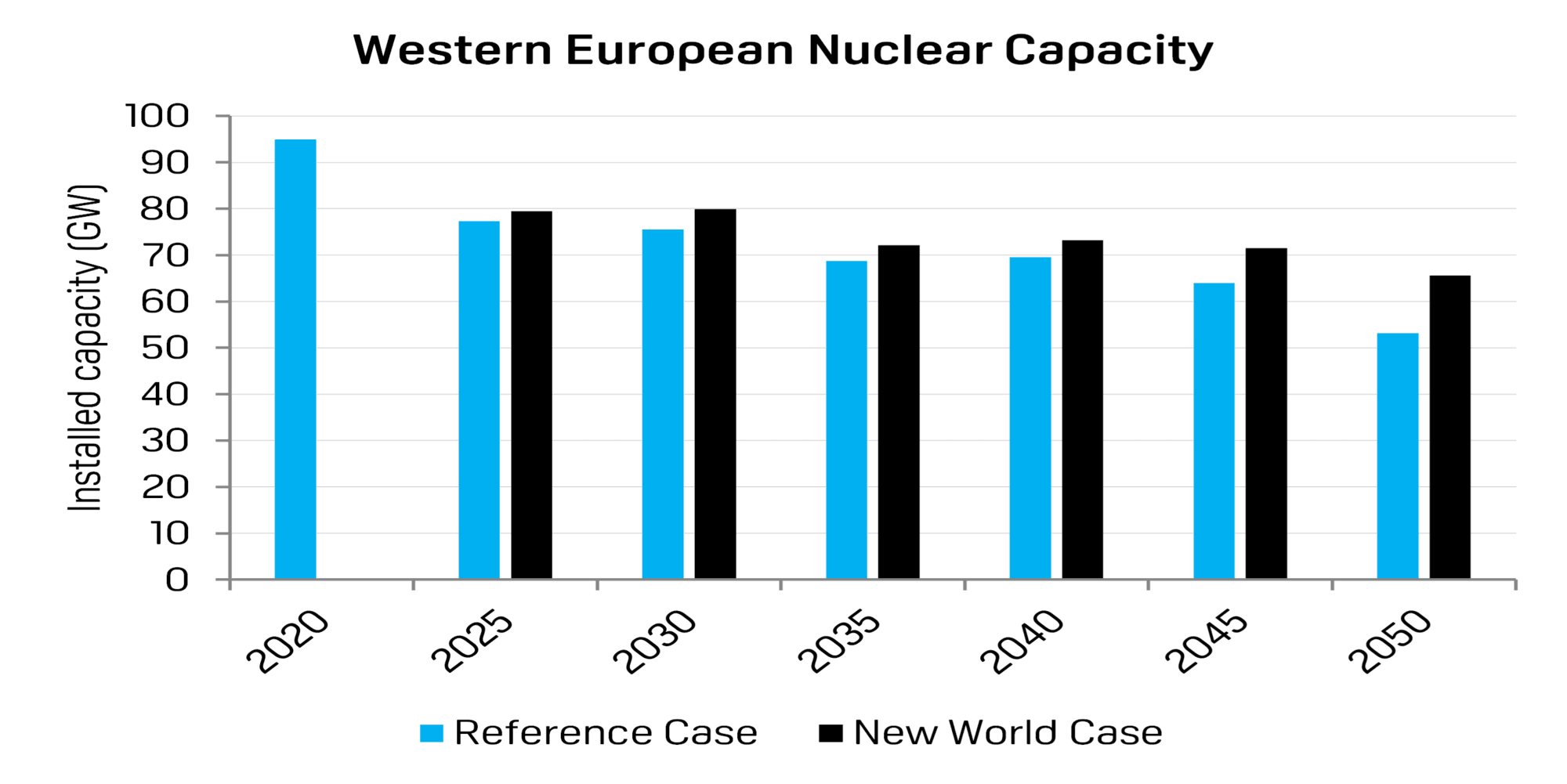

The Russian-Ukrainian conflict is raising the emphasis on greater reliance on domestic resources and a broader diversification of sources, which includes a potential lifeline for nuclear. After renewables, nuclear increases in our “New World Case”, with the growth most pronounced in the 2040-2050 timeframe. We see some upside to the investment appetite for new nuclear build in markets such as France and the UK and life extensions in markets like Belgium and Spain (with Germany seemingly still steadfast against extensions to its fleet). However, even with further investment, we still expect closures to significantly outweigh new build, and by 2050 nuclear capacity falls by 30% vs. current levels in the “New World Case” (vs a 40% fall in the Reference Case).

4. Electrification of heating will accelerate.

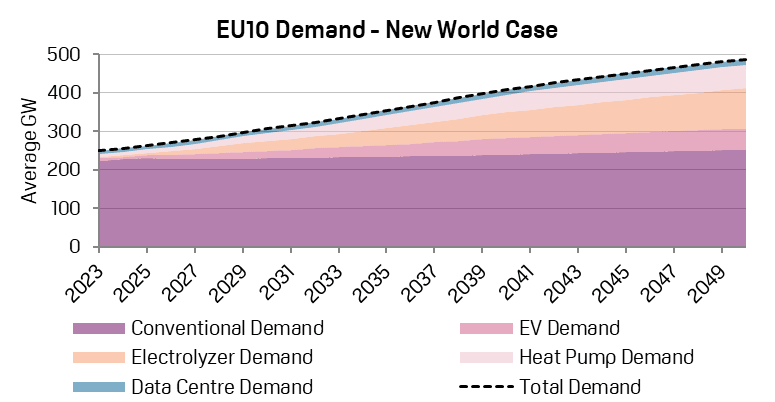

The current gas crisis has put more emphasis on the electrification of the heating sector, which so far has been lagging behind the electrification of transport. Our “New World” scenario assumes total power demand from heat pumps to average 20 GW by 2030 and over 60 GW by 2050 across EU 10, adding roughly 0.9% p.a. to annual average power demand growth over the next 30 years. A higher electrification of heating more than offsets risks of power demand destruction and is a key driver of further tightening in the winter balances across NWE. Additional growth in power demand from space heating (along with green hydrogen production) exacerbates the tightness in most electricity markets.

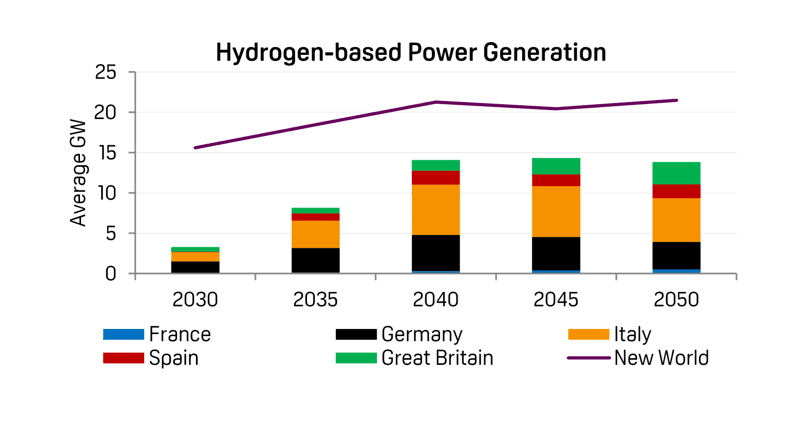

5. Green hydrogen and hydrogen-fueled generators driven to the fore.

Higher reliance on green hydrogen will be needed, especially to replace gas for ammonia and industrial applications and as a form of power system flexibility (given lower reliance on CCS/unabated gas). Electrolyzers account for over 40% of power demand growth in our “New World Case”, while also becoming the largest provider of flexibility in the power sector. While we see significant ramp up in renewables rich regions such as GB, Spain, and Portugal, we see the growing need for hydrogen to be partly met by imports from outside Europe.