As steelmakers transition to a less emission-intensive and ‘greener’ steelmaking process, the proportion of steel produced via electric arc furnaces is expected to grow substantially and subsequently the demand for ferrous scrap with it. The Turkish scrap assessment, representing the largest national importer of scrap globally, has become the global benchmark and widely used by scrap market participants across the world.

In 2019, 27.7% of global crude steel was produced via electric arc furnaces (EAF). This share is expected to considerably increase as steelmakers look to transition to a less emission-intensive and ‘greener’ steelmaking processes, amid the growing influence of environmental, social and governance (ESG) criteria among market participants. As it stands, Turkey is the largest national importer of ferrous scrap globally, importing over 20 million mt in 2020.

As such, Platts’ daily index assessment of imports of premium heavy melting scrap 1/2 (80:20) CFR Turkey has grown in importance and become the global benchmark, widely used by scrap market participants across the world.

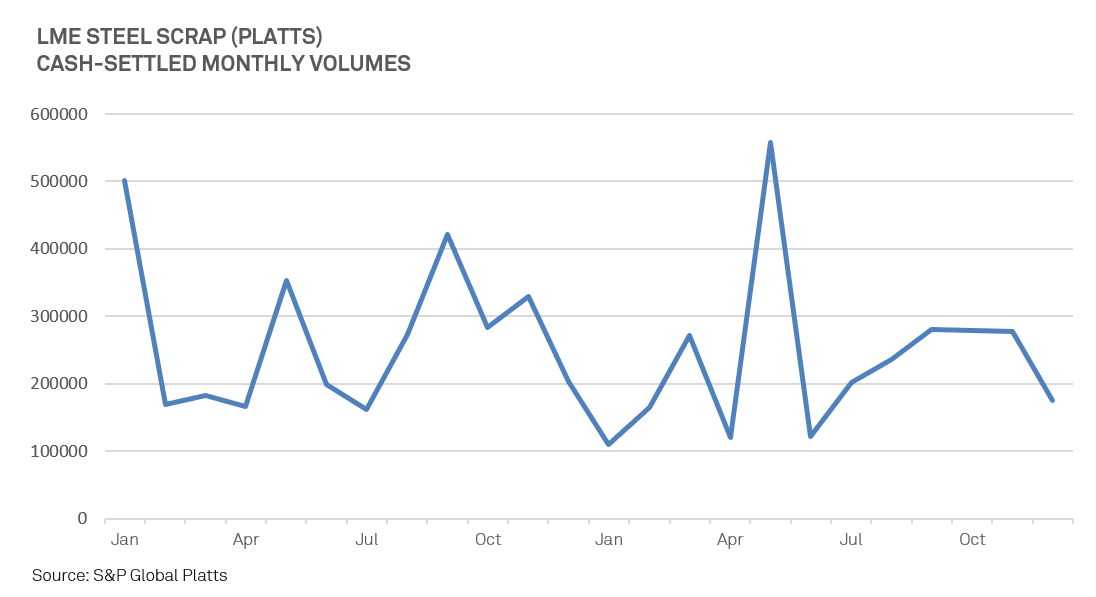

The LME Steel Scrap (Platts) contract was the first cash-settled contract in the exchange’s history. It has traded over 14.5 million MT over the 5 years since it started.

Several contracts for bulk scrap cargoes have been agreed against the Platts Turkish import scrap index. This enables counterparties to buy/sell a scrap cargo against the Platts index assessment, which reflects the daily tradable value of the physical spot market. Index-linked contracts can be flexible e.g. they can be based on a month-average to help smooth out any short-term price volatility; in early spring 2020, Turkish import prices sharply fell to a four-year low on demand concerns surrounding the coronavirus pandemic, before sharply rebounding. The index then rose to a near 10-year high in late 2020, amid supply concerns and a positive demand steel outlook amid news of viable vaccine candidates. Index-linked contracts have also been based on a price differential above/below the premium HMS 1/2 (80:20) assessment, depending on quality/grade differentials of the cargo in question. Some market participants opted not to lock in a whole cargo on the index – preferring to start with smaller volumes. Furthermore, using the Platts Turkish import scrap index, has the added benefit of removing the basis risk for those hedging through steel scrap futures contracts settled on the Platts index month-average.

Learn more about our pricing Methodology for Ferrous Scrap

Iron ore, another key steelmaking raw material, has already undergone indexation - with the prevailing physical and derivative benchmark being Platts’ IODEX spot price assessment, whereas previously iron ore contracts were based on fixed-price long-term contracts. China's economic growth coupled with the dramatic impact of the Global Financial Crisis forced iron ore demand and supply out of a comparatively stable relationship. Price negotiations had been determined by closed-door meetings between Australian and Brazilian producers and Japanese steel mills (JSMs) and later with Chinese steelmakers. But in 2009, negotiations broke down, as volatile prices in the spot market undermined efforts to agree on a fixed price for long-term contracts. This situation gradually led to the adoption of spot price assessments as the new pricing mechanism, in a sequence of steps. The first move was toward a quarterly lagged system — steel producers would purchase iron ore in the second quarter at the average of prices in the first quarter of any given year and sometimes lagged by a further month (i.e. four-months lagged from the start of the quarter). There were also quarterly-actual prices, whereby second-quarter prices were determined based on second-quarter averages — these provisional prices would then be balanced at the end of the quarter. The market then gradually began to seek better alignment between the delivery timing of cargoes and the relevant assessment timing. Quarterly lagged mechanisms were useful in smoothing volatility, but were also risky. In 2012, price falls led spot prices below quarterly lagged contract prices. This volatility led to widespread default on contractual obligations by Chinese steel producers who could purchase the same cargo on the spot market at a lesser price. Term contracts taking better consideration of time misalignments had less inherent lagged pricing risk.

The Platts premium HMS 1/2 80:20 (TS01011) price assessment reflects the tradeable value of bulk imports into Turkey of premium HMS 1/2 material, blended in an 80:20 mix. This covers ISRI codes 200-206 inclusive. The key supply regions for Turkish import scrap are the US, UK, Benelux, and the Baltics.

Platts captures trades, bids and offers from active market participants across the supply chain, with the data normalized to reflect premium HMS 1/2 80:20. All other grades (such as shredded, plate and structural, HMS1, HMS 1/2 75:25, and bonus) are normalized back to this grade based on prevailing market differentials. Platts assesses the market on a CFR Turkey basis, rather than normalizing to any single terminal or port within Turkey, due to the consistency in demand between the three major steelmaking clusters in Turkey. The assessment is published in US dollars on a per metric ton basis, and is timestamped to 4.30 pm UK time.

Platts’ pricing is compliant to International Organization of Securities Commissions’ (IOSCO) principles and undergoes an external annual review conducted by a Big Four auditor.

The word ‘benchmark’ is a term employed fairly loosely by market commentators in both the financial and physical markets. In recent years, the word has commonly come to refer to a published value used for the financial settlement of derivative contracts, typically over a defined calendar period, though also for shorter tenors. This is the spirit of the internationally-agreed IOSCO principles, which created a framework for considering the health of such benchmarks, with particular reference to transparency and process, and notably little focus on fundamental physical structure. A successful financial benchmark functions both as a hedging tool and as a financial trading instrument in its own right. It is measured by its success for price risk management, as well as its liquidity and depth derived from a wide user base and application. A benchmark with more heritage in the physical commodity markets is defined as a value used for the price settlement of a bilateral contract, particularly physical supply contracts. A physical benchmark exists primarily not to provide a hedge against a price movement, but to ensure the market price is directly and appropriately reflected in a physical supply or offtake contract. Buyers and sellers agree to use such a published value to reduce procurement and marketing costs by having a consistent link between the commodity exchanged and its current value. A physical benchmark therefore needs to be measured by its success in representing physical market economics – the broad-based value of the physical commodity bought and sold. This offers more complex considerations than a standard rational choice approach to a one-off exchange. Under a simple model, a seller should always prefer a higher price, a buyer a lower one, and the market clears where their utility curves meet. In the current focus, transactions take place repeatedly over time, and therefore total utility over time is preferred. A seller recognizes that a higher price at a particular point in time might reduce their overall sales over time through a reduction in market share, and therefore ultimately reduce total income. A buyer seeks access to the most competitive scrap price, but also those that provide the most savings over time, and hence has a concern for reliability and consistency. Long-term stability trumps short-term gain for both sides.

A market report providing expert analysis on the iron ore, coking coal and ferrous scrap markets. Find out more