Firm global container rates expected to continue

Strong rates expected well into second half of 2021

Expectations for void sailings to protect rates and rebalance schedules

Queue of vessels at Port of Los Angeles starting to fall

The global container market remains beset by the equipment shortages that emerged in the second half of 2020, caused by containers taking longer to turn around. The resultant shortage of empty containers to be taken on vessels around the world has resulted in higher freight rates.

Carriers have been shortening the number of free days that cargo owners have in an effort to return containers to the exporting ports faster, but despite this it looks likely to be some time before the logistical issues are resolved.

Expectations are now that it could be as far ahead as the start of 2022, much to the chagrin of shippers who have seen cargo rolled repeatedly, and are facing premium rates to secure shipments, often many times higher than their contracted rates.

Key regions where this has impacted include Europe, where logistical delays reported at the end of 2020 owing to front-loading ahead of Brexit and Christmas resulted in significant delays and thus carriers imposing congestion surcharges, and also in some instances refusing to take cargo back on an backhaul basis to Asia from Europe.

The other key region that is currently experiencing significant issues is the West Coast of North America, where many ships are still waiting in line off the coast of California for their slot in the ports of Los Angeles and Long Beach. As of March 16, there were 17 container vessels in the San Pedro Bay area, 10 of which were destined for the Port of Los Angeles. This was the lowest number of ships waiting to unload at the Port of Los Angeles since late December.

The delays are naturally pushing container freight rates higher and in the first quarter of the year they reached all-time highs on both the Asia westbound and transpacific trade lanes. Many in the freight market expected these rates would come down significantly following the Lunar New Year holidays in North Asia. However, this was not the case and as a result many are expecting rates to remain high well into the second half of 2021 and in some instances into the start of 2022.

"I expect carriers will manage capacity and rates could remain stable," another freight forwarder said. "The global economy is coming back, which should support demand."

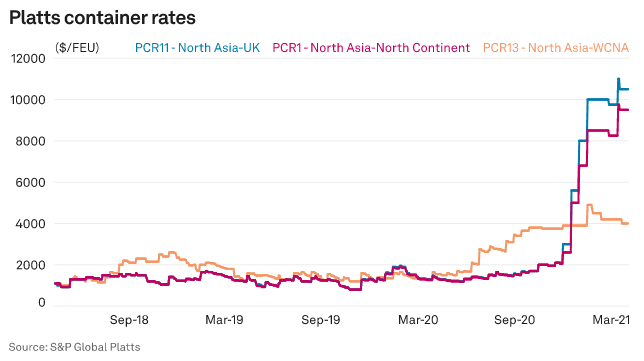

Platts Container Rate 1 — North Asia-to-North Continent — was assessed at $9,500/FEU on March 16, 645% higher than a year earlier when rates were at $1,275/FEU, while PCR11 — North Asia-to-UK — was assessed at $10,500/FEU, up 708% on the year.

These all-time high levels are expected to hold firm for some time to come. This is because carriers showed throughout the pandemic in 2020 when there was significant demand destruction that they were able to employ a raft of void sailings which kept freight rates at a relatively stable level despite lower demand levels. Many market participants are expecting the same to be seen throughout much of this year as, although demand will likely fall from present levels, carriers will employ similar techniques to keep them high.

"Carriers have shown they can keep rates firm even when nobody is moving cargo, it would be foolish to assume they wouldn't do the exact same thing going forward to keep rates steady," said a European freight forwarder.

While rates are likely to come down they are unlikely to reach the levels seen in 2019 and before. Many expect them to remain at what would previously have been all-time highs although relative to the significant increases seen at the start of 2021 they should appear affordable.

Despite the slightly rosier outlook from shippers that rates will come down, many importers, specifically those in Europe, are concerned that rates will only fall to a level that would still keep arbitrage opportunities closed for many commodities, such as agricultural and petrochemical products.

"I don't see rates coming down in the short to medium term to allow us to import anything in realistic volumes," said a UK-based importer. "I think to some degree this may mark the end of globalization that there will be not enough opportunities for people to ship around the world and therefore domestic production, or at least closer to home [production] will take precedence over these longer head haul routes."

The container shortage in Southeast Asia is starting to ease somewhat, hinting at better times to come for importers, although bottlenecks still persist across the world so it will take some time for these logistical issues to abate.

By George Griffiths