Improving COVID-19 prospects boost ton mile demand for Aframaxes, Handysizes

VLCCs, Suezmaxes pick-up delayed until H2 2021

Rising bunker costs push earnings into negative territory

Lackluster demand for oil and rising bunker fuel expenses continued to squeeze tanker owners’ earnings in Q1 2021, but with the rollout of vaccines now well underway, ton mile demand could start drawing support from greater mobility in Q2 as countries reduce lockdown measures, with smaller ship sizes benefitting first from the increase in demand.

Daily earnings in the quarter hovered around breakeven levels for VLCCs on the back of subdued oil demand, crude oil stock drawdowns and supply kept low by voluntary production cuts.

Freight rates reached a four-year low of $5.25/mt on the Persian Gulf-to-China VLCC run on March 11, its lowest assessment since August 2017. Low Worldscale rates combined with higher bunker prices caused earnings to turn negative from early February, according to data from S&P Global Analytics.

“The VLCC and Suezmax markets will remain steady with little volatility in freight rates in the coming months,” a broker said “Production is not expected to pick up substantially and these tankers really depend on end-user demand, particularly Indian and Chinese ones, which is currently subdued given refinery maintenance and high stocks that have yet to unwind.”

However, Aframaxes and Handysizes are likely to see more volatility in rates as refineries favor smaller tankers to retain flexibility over output.

“Aframaxes will see more volatility as we have seen in late February, especially if bad weather factors and refinery last minute needs combine,” the broker added.

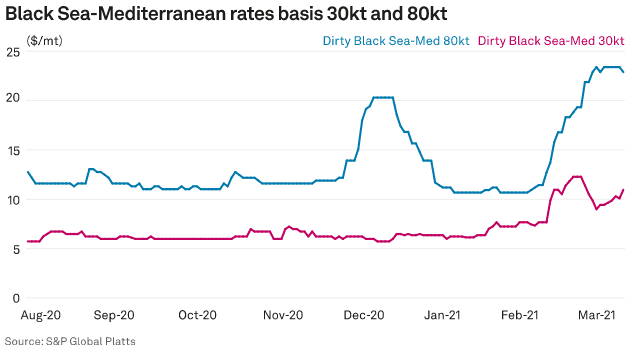

Aframax and Handysize price volatility was already visible throughout Q1 as vessels were caught out of position, causing supply tightness and price hikes. Mediterranean Handysize freight rates reached a 10-month high amid bad weather and tonnage unavailability starting mid-February. Freight rates on the Black Sea-to-Mediterranean run basis 30,000 mt reached $23.39/mt on March 5, its highest assessment since May 12, 2020.

Rebalancing

While more volatility is expected for intra-regional runs on smaller ships, utilization of VLCCs and Suezmaxes will likely remain subdued as global crude oil markets continue to rebalance.

Supply is currently being kept low by Saudi crude production cuts, with the country announcing it would roll over February and March quotas to April on the back of subdued Chinese demand. In addition, the recent polar vortex in the US Gulf Coast also caused a reduction in demand from the region as well as crude output.

Looking at demand, market participants expect this to continue growing at steady rates, with a stronger pull starting in H2 2021. S&P Global Platts Analytics sees global oil demand rising 250,000 b/d in April from March, before surging another 1.9 million b/d in May and a further 3.3 million b/d in June. However, 2019 levels are not expected until 2023 at the earliest with the likelihood of further delays, Platts Analytics said in a research note.

On tanker supply, prolonged pressure on earnings may lead to the long-awaited rebound in scrapping rates, which surged at the start of year but have since slowed. Average demolition prices have dipped since January, reaching a low of $410/ldt in Pakistan in mid-February, down from $450/ldt in the first week of January, according to Go Shipping. However, levels had now improved, shipping sources said, with a better demolition outlook for the rest of the year.

According to Platts Analytics, there are currently 177 VLCCs older than 16 years of age that could be candidates for scrapping. However, upcoming regulatory announcements from the International Maritime Organization and from the European Parliament risk delaying further scrapping decisions as owners wait for regulatory and technological improvements before phasing out older units and ordering new ships.

High bunker costs

Despite a slow demand recovery, the tighter oil supply picture during Q1 combined with a bullish paper market, caused the oil price to rise to a 14-month high of $71.38/b for ICE Brent futures March 8. Prices have fallen slightly since then and settled at $68.63/b on March 15 for May settlement.

The strong oil picture caused marine bunker prices to move up in line, despite continued subdued demand from tanker owners.

Rotterdam 0.5% sulfur marine bunker fuel was assessed at an 11-month high of $508/mt Feb. 25. It hit a low of $154/mt on April 24 last year as the initial wave of COVID-19 pulverized demand.

Despite low bunker demand from shipping markets, bunker costs are set to remain bolstered by the bullish crude complex, squeezing earnings for owners.

The wider Hi-5 differential, however, was a good development for owners who retrofitted scrubbers, or exhaust cleaning systems, in their tankers.

A wider Hi5 — the differential between low and high sulfur fuel oil — benefits owners who have installed scrubbers as they can use the cheaper high sulfur fuel.

The differential between lower sulfur 0.5% and high sulfur 3.5% marine fuel in Rotterdam was assessed at $104/mt March 15, up from a low of $27/mt reached on Aug. 21.

By Charlotte Bucchioni