Supramaxes and Panamaxes

Atlantic Supramaxes face dead calm as global demand evaporates

Coronavirus is set to hit the Atlantic dry bulk market in its weakest spot — demand. After a weak first quarter, Q2 may see historic price falls in dry freight as the perpetually overtonnaged Atlantic basin collides with a pandemicinduced collapse in demand for dry bulk commodities.

As ports and factories shutter around the basin, unsure of when — or if — they will reopen, there was little optimism among owners of the Handysize and Supramax workhorses of the dry bulk market.

Slow Q1 but healthy

The Atlantic Supramax and Handysize dry bulk markets began the second quarter quietly, but with widespread weak sentiment across the basin.

In the bellwether US Gulf Coast markets, scarce inquiry across various cargo types has seen trans-Atlantic business fall to January 2019 levels.

Typically, the key commodities of grains, coal, and petcoke underpin demand for Supramax and Ultramax ships, but each has suffered its own crisis of demand as geopolitical and macroeconomic factors wreaked havoc on their respective markets.

The twin bearish factors of the China-US trade tensions and African swine fever gutted demand for US-sourced soybeans, while an unusually warm winter and Indian port/factory closures stymied demand for coal and petcoke, respectively.

Poor returns for ships redelivered in the Pacific basin — along with shipowner concerns about coronavirus contamination — propped up front-haul rates throughout most of Q1. However, as the virus increasingly spread west into the Atlantic, those foundations have been collapsing.

COVID-19 hit

As industry closes its doors around Europe and North America, the hammer has fallen on Atlantic freight.

February-March trans-Atlantic time charter rates had wavered in the $13,000/d-$16,000/d before early April fixtures saw deals done at below half that rate.

In one example, the shipowner Oldendorff was heard in the market having fixed an Ultramax from Mobile, Alabama to Ploce, Croatia, at $7,000/d APS basis -— lower even than a comparable recent fixture by Ultrabulk at $8,000/d.

Market participants wondered aloud how low trans-Atlantic rates could fall before shipowners refused the business.

“I think the worst is yet to come,” one senior shipbroker source said. “Maybe half the Oldendorff rate, something like that. I cannot see any way in which shutting down the world economy for an extended period does not end up with numbers like that.”

Comparable drops in time charter rates were reported in the UK Continent and Baltic ferrous scrap markets, as charterers withdrew cargoes due to inactive Turkish buyers.

However, market participants expected to see rates fall even further as Q2 progresses.

“I think the only reason owners are still getting decent levels is due to cheap bunkers,” said a shipbroker specializing in Baltic scrap freight. “If bunkers will move up, the time charter levels will drop much faster. Operators are evaluating voyage business forward at around $8,000/d passing Skaw.”

Light in the darkness

“Although, in these uncertain times, it is admittedly hard for one to confidently predict the market’s direction moving forward, basic fundamentals point to a certain recovery,” Athens-based Panamax shipbroker Eastgate Shipping said in its recent quarterly note.

With China slowly returning to work, the South Atlantic grains export trade flow was one area that might show some promise.

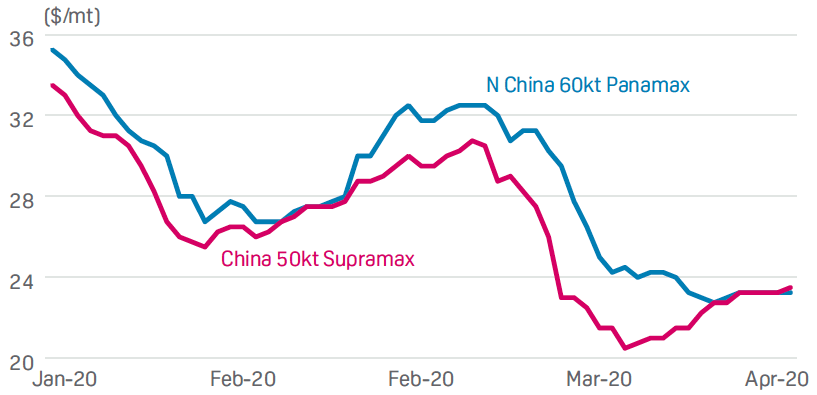

Source: S&P Global Platts

While 60,000 mt soybean cargoes to China from Argentina and Brazil most commonly travel on Kamsarmax/Panamax ships, smaller Supramaxes and Ultramaxes can be used where Panamax rates become uneconomical.

On April 1, the S&P Global Platts Santos-to-Qingdao, 50,000 mt Supramax and 60,000 mt Panamax $/mt assessments were at parity at $22.75/mt, suggesting charterers could find bargains — and Supramax shipowners could find cargoes — by undercutting an oversupplied Panamax sector.

— Samuel Eckett, Managing Editor, Dry Bulk and Tankers

A roller coaster ride greets Atlantic Panamaxes in 2020

With the turn of the decade, the global commodities sector experienced a remarkable roller coaster ride on prices in the first quarter of 2020, and the Atlantic dry bulk Panamaxes segment was no exception.

Where the market stands today: A gloomy outlook for Q2

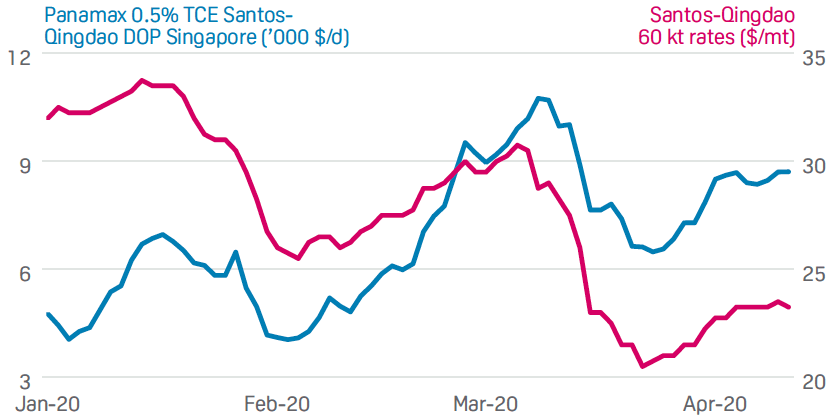

With China having achieved relative success in controlling the coronavirus and its industrial output gradually returning to normalcy, the last week of March saw some revival of demand for Panamaxes in Asia. Time Charter Equivalent rates on the key Santos-to-Qingdao grains route were also helped by this development as the tonnage oversupply eased. However, the picture remained murky as the pandemic’s march was yet to be controlled elsewhere.

At the end of March, other major demand centres such as India, the Middle East and Europe remained under complete lockdown, expected to last at least until the third week of April. With no certain end in sight and an extension of the lockdown in most countries highly likely, prospects appeared bleak for the global economy and with the likelihood of industrial demand remaining depressed.

This is set to have a knock-on effect for dry bulk Panamaxes, and while grains exports out of East Coast South America gain momentum in the coming weeks, unless a vaccine for the coronavirus is found in the near future, the upside on Santos-to-Qingdao TCE rates would likely be capped by a substantial proportion this time around in the “high season” second quarter.

Q1 seasonality: The double-dip start to 2020

Typically, the first quarter and specifically the first six weeks of the year have been “low season” for the Atlantic Panamax market. This has historically been attributable to the grains export cycles in the ECSA region, as well as the Chinese Lunar New Year holidays. In the latter half of a given year’s first quarter, demand for shipping soybean cargoes out of ECSA revives and typically leads to a rebound in rates, usually towards the end of March.

In the first quarter of 2020, however, rates did not exactly replicate the trend historically observed on the key Santos-to-Qingdao route, although having experienced slight declines during the first week of January. With the implementation of IMO 2020 regulations on marine fuel sulfur content, charterers were faced with significantly increased bunker fuel prices for their timecharter hires, which had dominated marketplace discussions in the previous quarter and kept sentiment slightly nervous.

Nevertheless, on the back of strong growth in soybean exports out of ECSA, the Santos-to-Qingdao freight rates experienced an unusual rebound as early as the second week of January. This upside turned out to be rather short-lived and was followed by a double-dip effect, with the trajectory turning negative in H2 January as demand faded as the Chinese Lunar New Year holidays began.

Consequentially, TCE rates for Panamaxes on the Santos-to-Qingdao route hit a multi-year low of $4,046/day DOP Singapore on February 4, with high bunker fuel prices adding salt into the wounds of shipowners.

As Chinese buyers returned to the marketplace in the first week of February, the Santos-to-Qingdao rate was yet again quick to rebound on healthy demand fundamentals. The overall trajectory remained strongly positive throughout February and the market entered March on a rather firm note.

With a feeling of spring having come earlier this time around in the market, shipowners were delighted as the route’s TCE rates for Panamaxes hit $10,751/d DOP Singapore on March 9, a multi-year high within the Q1 cycle. However, while prospects for grains demand remained strong, there was a storm brewing in parallel that would wreak havoc on rates in a matter of days.

Enter: Coronavirus pandemic and the grains of hope

With the coronavirus outbreak declared a pandemic by the World Health Organisation on March 11, the global economy was quick to take a hit as many countries rolled out a series of lockdowns, which remain in effect.

This brought about a severe dampening effect on the demand side of most industrial commodities, with the manufacturing segment largely grinding to a halt across the globe.

While the demand for shipping grains was largely unaffected by this global development, the dry bulk Panamax segment was not as fortunate. With coal and iron ore shipments taking a hit and cargoes of these commodities turning scarce, overall spot demand for Panamaxes succumbed. With vessels open in Asia facing a dearth of enquiries for round voyages in the Pacific and Indian Ocean basins, shipowners only saw one ray of hope: grains cargoes.

Panamax shipowners in Asia actively began ballasting westwards to seek employment for their vessels, as spot liquidity increasingly became centred around grains cargoes loading out of ECSA.

Consequentially, with the segment faced with a substantial tonnage oversupply, rates were quick to plummet.

In a matter of a fortnight, the Santos-to-Qingdao TCE rate for Panamaxes fell to $6,484/day DOP Singapore on March 24, down nearly 40% from the March 9 peak.

Voyage rates on the route also plummeted and hit a more than three-year low of $20.50/mt on March 23. This was as a full-scale price war broke out in the global crude oil market, with the spot market flooded with oil, pushing the Dated Brent crude benchmark price to a record low.

In contrast to the nervousness among market participants in Q4 2019 on the prospects of significantly higher fuel prices, the impact of IMO 2020 regulations were put onto the backburner in March as bunker fuel oil prices plummeted across the globe. Instead, the prospects of depressed earnings now loomed on the the dry bulk segment amid the economic collapse brought about by the coronavirus pandemic.

The impact of IMO 2020 regulations were put onto the backburner in March as bunker fuel oil prices plummeted across the globe

Nevertheless, a healthy appetite from buyers in Asia for ECSA-loading grains cargoes has helped a recovery in Panamax rates in the first decade of April, with the Santos-to-Qingdao Panamax TCE rate edging up to the mid- $8,000s/d DOP Singapore at the start of the Q2 soybean export “high season.”

With some uncertainty surrounding the marginal demand for balance-April loading cargoes, one thing appears to be near certain for Panamax shipowners: the worst is behind them.

— Sam Hashmi, Associate Editor, Dry Bulk