Clean tanker market bracing for COVID-19 hit to oil product demand

Shipowners could find themselves in a perilous position as the second quarter develops, should the coronavirus pandemic continue to instill a worldwide slowdown in demand for oil products, despite continued efforts to place material on floating storage for the months ahead.

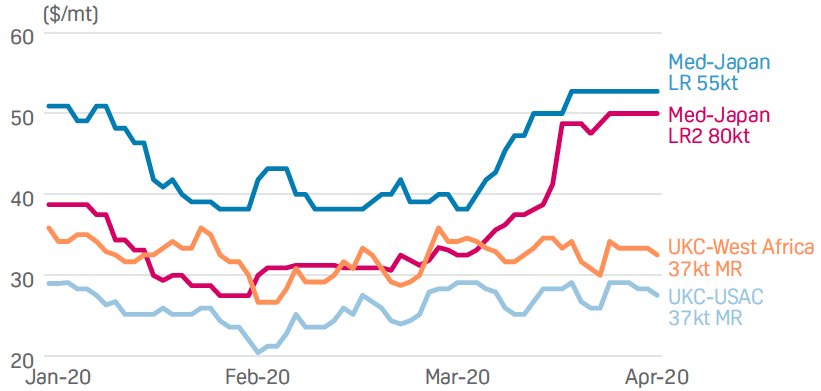

Having held at healthy levels for almost all vessel classes for large parts of the traditionally strong first quarter, the clean tanker market faces looming uncertainty on how rates will be reciprocated with the wider spectrum of oil products in the west of Suez market.

That is primarily tied with the expected levels and methods of stockpiling for each oil product which, in turn, will call for potential floating storage options for clean tankers in the quarter ahead.

Otherwise, wider recognition of a lack of product to be moved in light of a huge fall in prompt demand due to lockdown measures in European countries has instilled bearish sentiment in the market.

MRs to seek gasoline floating storage options

At present, all oil product traders are exploring storage options in light of price curves being in steep contango.

Storage for products such as ultra low sulfur diesel storage is being concentrated in storage in the Baltic region as opposed to floating storage, while naphtha shipments eastbound have been predominant for Medium Range and Long Range tankers to explore in recent weeks due to the sharp collapse in European prices against the Asian CFR price.

Instead, shipowners have been observing the contango for the months ahead in the gasoline market, which is enticing traders to push for storage options on clean tankers as a way of hedging for the future price increase.

The conversation surrounding floating storage has grown louder in the MR market, with shipowners concerned that sector was the most exposed to closed arbitrage opportunities for both trans-Atlantic and West Africa shipments.

Owners had been aiming to tie vessels for long-haul shipments in March due to more attractive time charter earnings, but have now been more willing to seek floating storage options because of recent softness in the tail end of the first quarter.

LRs to resist falls or follow suit?

More charterers have been exploring floating storage options with MRs, despite the less attractive rates in accordance with economies of scale, because the LR market showed sustained tightness of availability throughout March, fueled by a high volume of output from refineries in the Persian Gulf and Red Sea.

Record-breaking rates for Yanbu-UKC shipments, basis 80,000 mt, have spurred some LR owners to ballast all the way east of Suez, missing out on a long-haul shipment from Europe to secure a highly attractive back-haul shipment rate.

Source: S&P Global Platts

Coupled with that was the expectation charterers will target more LRs for floating storage once long-haul shipments are concluded, particularly if contango curves steepen in product markets. That would take more tonnage out of the market and preserve tight supply.

However, downside potential looms for LRs should expected refinery runs cut output volumes in the months ahead, hampering floating storage inquiries as a result.

Signs of a cooling off in rising freight rates in the Middle East would spell the end of the support for LRs, and pave the way for a full market correction to come for clean tankers.

— Chris To, Associate Editor, Clean Tankers