Freight jumps on floating storage rush, uncertainty reigns amid coronavirus-related demand slump

Freight jumps on floating storage rush, uncertainty reigns amid coronavirus-related demand slump

Oil tankers have found a second life as floating storage engines to stock cheap crude until markets pick up, after March saw near record low oil prices and sinking demand.

Source: S&P Global Platts

As ships were chartered out for storage, spot lists shortened and freight spiked in March. The contango in the crude oil market has since narrowed amid the OPEC+ meeting announcement, to then widen again amid wanting storage availability.

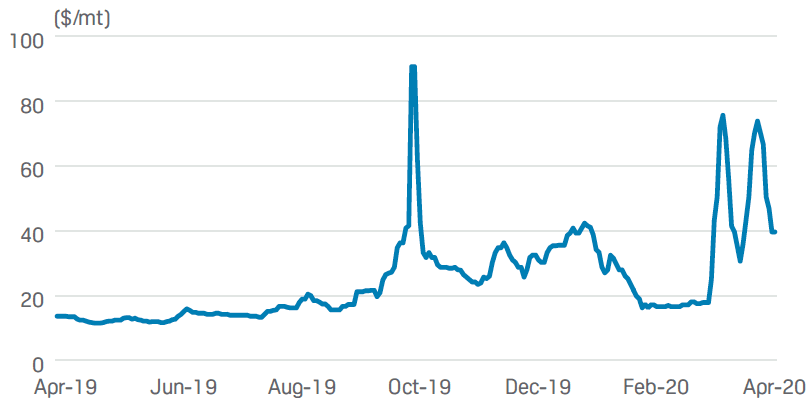

VLCC and Suezmax freight rates jumped in the first quarter of 2020, largely due to the oil price war and crude prices tumbling to levels not seen in 20 years.

On April 1 Dated Brent was assessed at $15.135/b. It was last assessed lower on April 9, 1999. As of Tuesday April 7, oil prices had rallied ahead of Thursday’s OPEC+ meeting and predictions of a production cuts.

A steep contango structure in the crude market has supported the economics of storage, with market participants turning to oil tankers as a solution given the limited land-based storage available.

Traders would hence buy cheap oil on the spot market, and instantly sell the cargo forward in the futures market, and locking in the difference.

However, recent developments in oil prices have already challenged these fundamentals as ICE Brent futures have found support from the potential production cuts. While the flat price component of the Dated Brent benchmark – Cash BFOE – has also found some support as a result of the upcoming OPEC+ meeting, Brent Contracts for Difference remain in a steep contango as the current oversupply combined with the demand destruction keeps pressure on prompt physical differentials.

Limited buying interested from China as a result of competitive local grades and higher freight rates has caused a number of fixtures to fail as the contango was not wide enough to incentivise interest from Chinese buyers.

This has caused the freight market to weaken considerably, and has pushed charterers to renegotiate freight rates, shipping market participants said.

Two competing trends are also set to affect the freight market in the coming months. On the one hand, production cuts by OPEC+ members will reduce oversupply and sustain oil prices up, hence reducing the profitability of storage. On the other hand, April is already looking bearish on the demand side amid reduced refinery demand due to coronavirus-related lockdowns. Ultimately, it is unclear when the market will return to normal, which will also depend on how many ships remain on the spot market after so many have been charterer out on long-term contracts for storage.

Uncertainty over future demand

Traders in all West of Suez regions remain concerned about the oversupplied markets. Traders estimated global oversupply to reach 6 million b/d in April and 7 million b/d in May before the OPEC+ cuts, and with land storage options filling quickly, more oil is set to go on tankers.

“There are still some ships, but they are asking for a lot of money, so charterers are holding off with the expectation that the market will soften if there is less activity,” a broker said. Since April 2, freight rates have softened as low demand and high rates of ships failing subjects could not sustain the freight bubble for long. Charterers were reported to be holding off ahead of the OPEC+ meeting, with the prospect of higher crude prices.

“There are still some ships, but they are asking for a lot of money, so charterers are holding off with the expectation that the market will soften if there is less activity” – Shipbroker

The OPEC+ deal failed to impress in the freight market, sources said. On the one hand, it is helping removing some excess supply and push prices up. On the other hand, current supply cut seem unable to match the limited demand that is likely to roll over into the second quarter as the world tries to combat the spread of the coronavirus. The International Energy Agency estimated Wednesday April 15 current global storage capacity to near 6.7 billion bbls of crude oil. Out of the total capacity, 63% was reported already filled as of January 2020, or an equivalent of 4.2 billion bbls. Maximum operational capacity for mainland storage facilities is, however, estimated to be around 80% of capacity, or an equivalent of 5.0-5.7 billion bbls. The top end of the range was estimated to be reached in June 2020, or an equivalent of 1.5 billion bbls of crude oil going directly on storage.

While this meant that shipowners are more bullish and believe freight will pick up in Q2, the uptick in rates is being delayed by the lack of cargoes getting fixed.

Freight rates peak again in Q1

After spiking in the fourth quarter as the impending IMO 2020 regulation on sulfur limits loomed amid trade tensions between the US and China and sanctions against Cosco Shipping, rates jumped again in March as OPEC+ failed to reach a deal on further production cuts.

This led Saudi Arabia to discount its crude and flood the market. Hence, market participants started to load crude on tankers as land-based storage quickly filled.

Larger vessels such as VLCCs and Suezmaxes were first targeted for storage, which caused spot rates to spike as lists shortened. The West Africa to UK Continent and Mediterranean route, basis 130,000 mt, was assessed at $43.95/mt on March 17, the highest since July 28, 2008.

Earnings for owners putting VLCCs on storage were reported at $120,000/d over a six-month period, $85,000/d for 12 months and $48,000/d for three years.

Insufficient Chinese demand

Throughout January and February, freight rates tumbled to pre-IMO 2020 levels given reduced demand from China, the single largest importer of crude. As of early February, Chinese oil demand was estimated to have plunged by about 1.1 million b/d since the start of the year as it went into lockdown, according to the IEA.

This is equivalent to a reduction of three VLCCs per week going to China.

While China has begun to slowly emerge from coronavirus, the rest of the world has started to tackle it and has entered into lockdown, hammering crude demand in the process. Most vessels from the North Sea, Mediterranean and West Africa were in fact reported going East, or at least having included an option for doing so.

Consequently, market participants turned to floating storage as a solution for any crude not finding interest from China. While demand from China is expected to pick up in the coming months, countries remain cautious over a possible second wave of coronavirus.

Earlier this month, officials in South Korea, Taiwan and China tightened measures on foreign travel to Asia, highlighting anxieties about new cases coming from abroad.

A short-term full recovery in demand in China is unlikely given low end-demand for goods from the world’s largest exporter, with the second quarter set to be beset by the demand collapse. All countries will take their time to recover, and as refinery demand improves, mainland storage is likely to be used first, followed by chartered vessels with the shortest storage maturities.

Both traders and shipowners have benefitted from the steep contango in the oil market and lifted freight rates, allowing shipowners to recoup margins after a weak start to the year.

— Charlotte Bucchioni, Associate Editor, Dirty Tankers