Platts SEAT, or Platts Southeast Asia Thermal coal assessment, is a daily 15-60 day forward price assessment for seaborne thermal coal exported out of various origins typically shipped to the Gulf of Thailand region.

Platts SEAT reflects the value of 4,200 kcal/kg GAR coal, delivered on a standard Supramax vessel to the basis port of Ko Sichang in Thailand in the forward 15-60 days.

This new price provides thermal coal producers, power producers, end user power plants, coal traders and ship brokers with an independent, transparent source of open-marker spot prices for low cv-grade thermal coal shipped to Thailand, Vietnam, Philippines, Malaysia and other consuming regions in Southeast Asia.

Platts SEAT is available in these Platts services: Platts Coal Trader International and fixed pages GC0410, GC0425 and EP0910.

Platts SEAT captures the rising demand for seaborne coal in Southeast Asia due to higher power and energy consumption, with 115 million mt of thermal coal imported by Southeast Asia in 2019, and the assessment aims to reflect this growing market.

The 4,200 kcal/kg GAR grade of coal is the most liquid and active grade traded in Asia, with its low sulfur and ash content, serving as both a direct fuel and for blending in the foreseeable years to come.

Southeast Asian countries do not have significant production of its own and these developing economies require power at the cheapest cost, where thermal coal will be the most optimal choice.

Source: S&P Global Platts

Evolution of Platts SEAT – a brief history

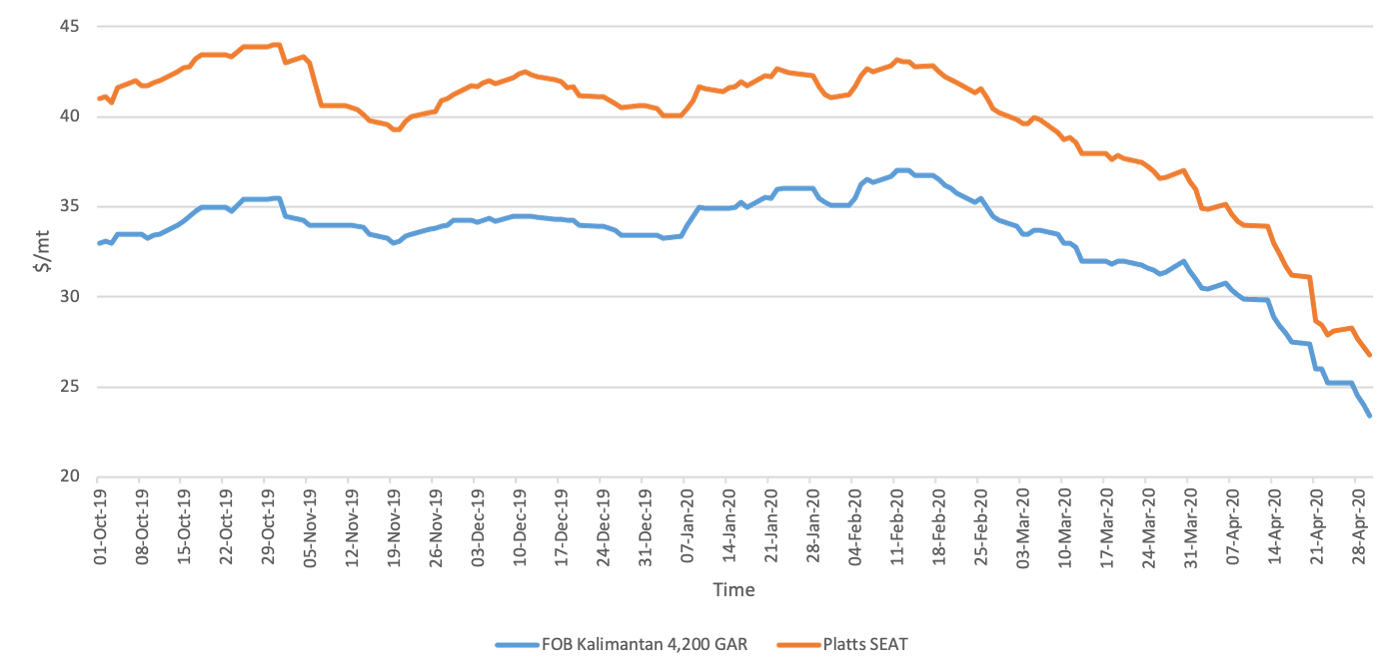

We began assessing the Platts SEAT on October 1, 2019, to reflect the delivered price of coal anticipating changes in supply and trade-flows.

In line with Platts focus of keeping up with evolution of markets and the move to a delivered price in coal, the SEAT assessment will accompany our existing Platts NEAT to give Platts further redirection of global coal assessments.

Platts SEAT also addresses a market need for a reliable delivered Southeast Asia price assessment to reflect the growing coal requirement in this region, where seaborne demand from the region has surpassed 115 million mt in 2019.

The 4,200 kcal/kg GAR coal continued to be the most sought after grade in Southeast Asia because of the proximity of its main supplier- Indonesia to all the consuming regions.

This grade of coal with low sulfur and ash content is widely used by Southeast Asian power plants for electricity generation. Given its nature as both a direct fuel and blending tool, demand for this grade of coal is not expected to fade in the foreseeable future.

In choosing the Gulf of Thailand as the delivered region of assessment, with Ko Sichang as the basis port, thermal coal buyers will now be able to purchase on basis Platts SEAT, at a premium or discount to the CFR delivered price.

Platts SEAT offers users the scope to normalize a CFR price to various consuming regions across Southeast Asia.

Sources have also supported a 15-60 days window as the laycan period, where the assessment considers cargoes across all origins and tracks shifting trade flows regularly to keep CFR prices up to date.

How do we assess Platts SEAT?

Our team of experienced coal market reporters surveys a broad pool of active market participants including but not limited to producers, consumers, traders and brokers on a daily basis.

Platts places great value on its ability to discover settled physical tonnage deals, as well as bids and offers for spot cargoes, which constitute the best indication of the true market value for a given coal.

In the absence of confirmed trades, bids, or offers, assessments take into account buying, selling, tradable indications that meet Platts methodology guidelines. Bids and offers must increase or decrease in reasonable increments to ensure that every price level has been tested, and yield an assessment that reflects transactable value.

We publish bids, offers, expressions of interest to trade, and confirmed trades during our Market on Close process every day. The information is summarized in daily market commentary in Platts Coal Trader International.

Our CFR Gulf of Thailand 4,200 kcal/kg GAR coal assessment reflects the daily tradable, repeatable spot market price of this increasingly important grade of coal at 1730 Singapore Time precisely.

SPECIFICATION: The assessment reflects thermal coal cargoes with a calorific value of 4,200 kcal/kg GAR with 0.6% sulfur, 7% ash and 35% moisture. Other grades may be normalized to this basis. LOCATION: The assessment reflects deliveries to SE Asia ports on a CFR basis, with Ko Sichang in Thailand as the basis port. Deliveries to other regions in SE Asia may be normalized to this basis for assessment purposes. ASSESSMENT PERIOD: Platts assesses cargoes delivering 15-60 days forward from the date of publication. For example, on October 1st, the assessment would reflect cargoes delivered from October 16th to November 30th. VOLUME: The assessment reflects cargoes delivered on a standard Supramax vessel.

Discover more in the specifications guide

Why is Platts SEAT important?

Southeast Asia is one of the fastest growing market in Asia-Pacific with nearly 1 billion mt produced by the largest export nations in Indonesia and Australia. That growing production is expected to feed into an astounding 128 million mt of coal demand from SE Asian power plants in 2020 alone. Southeast Asia’s demand for thermal coal shall continue to grow and is expected to be around 140 million mt by the year 2021. As the cheapest form of fossil fuel which is easily and widely available in the market, developing nations which require energy fuel at the lowest cost will rely on thermal coal for power generation. Platts SEAT here plays a critical role as Southeast Asian thermal coal buyers yearn for a CFR delivered price as an independent, transparent source of open-marker spot price assessment for low cv-grade thermal coal. This is also part of Platts’ overarching global strategy of moving from FOB focused assessments to delivered price markers.

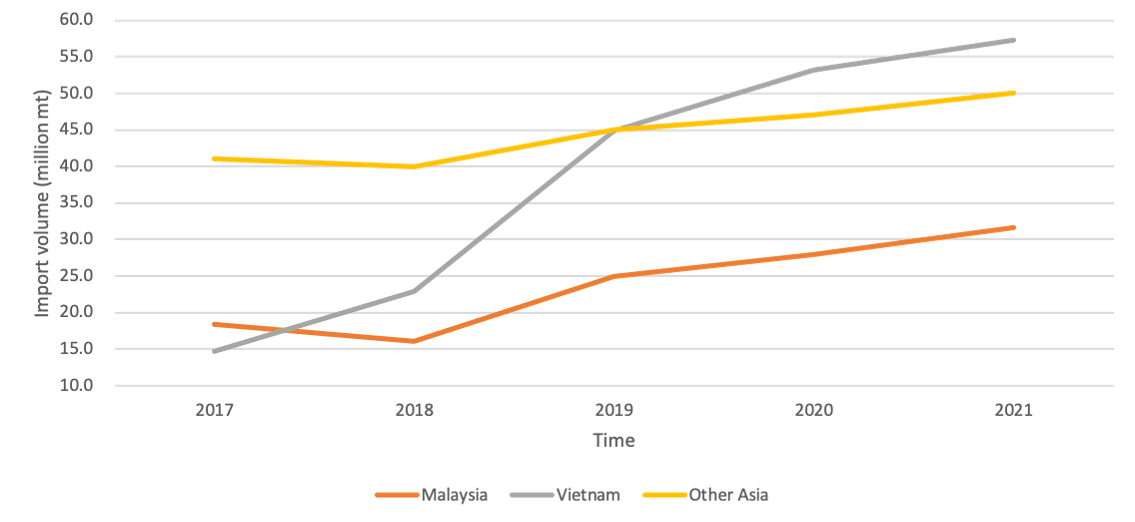

Platts SEAT caters to market participants including but not limited to Malaysia, Thailand, Philippines, and Vietnam as well as other consuming regions in Southeast Asia.

In Malaysia, based on Platts’ Analytics forecast, we are seeing 28 million mt of thermal coal imports in 2020 and another 4 million mt increased by 2021. Coal plays a large role in Malaysia’s energy scheme and is fully imported. Some 63%, is imported from Indonesia, with another 24% coming from Australia and the remainder from nations as far away as Russia (11%) and South Africa (2%). Malaysia’s power generation is highly dependent on fossil fuel with 53% coal, 42% natural gas and 5% hydropower.

Malaysia’s first of two 1000 MW ultra-supercritical coal-fired power plants in Port Dickson have started commercial operations, bringing the total power generation capacity in Malaysia to almost 23,000 MW. According to the Malaysia’s national utility Tenaga Nasional Bhd (TNB), the second 1,000 MW plant is a joint venture involving TNB, Mitsui & Co and Chugoku Electric Power Co.

In Thailand, thermal coal import in 2019 was 21 million mt, down about 14% on year. Indonesia, Australia and Russia were the major suppliers over the year.

Thailand’s buying behavior is an amalgamation of long term contracts and spot purchases, where the country imports coal for its power plants to generate electricity for its industrial use.

The proportion of coal in the energy mix in Southeast Asia is more than 20%, and Thailand has about 1 million kilo tonne of oil equivalent of coal consumption on an annual basis.

Thailand does not have a significant production of its own and these developing economies require power at the cheapest cost, where imported thermal coal will be the most optimal choice.

In the Philippines, the country has been a net importer of coal since 2005, in which its import volume is expected to be around 27 million mt in 2020, with Indonesia being its predominant supplier, according to Platts Analytics forecast.

The total power demand in the Philippines was more than 100 TWh in 2019 and the demand has grown by an average of 6.3% per year since 2016. The Luzon grid is the home to the capital, Manila, and is the largest of all three grids with about 74% of total power demand.

According to Platts Analytics, the Philippines is bringing online 3.2 GW of new power plant capacity by the end of 2020, with another 7.2 GW planned by 2023; according to the S&P Global World Electricity Power Plant Database. The country is leaning increasingly towards coal, and 93% (3 GW) of the power plants under construction are coal-fueled plants. Luzon, being the largest grid in Phillippines and experiencing the fastest growth in demand, is bringing online the majority of these new plants. The Luzon grid region has 1.8 GW of coal-fired plants under construction with another 3.6 GW of coal-fired plants are planned in Luzon by 2023. The annual power demand in Luzon could reach 85 TWh by 2023, an increase from 71 TWh in 2018. However, the new coal capacity already under construction should be enough to meet new demand by 2023.

In Vietnam, coal demand has doubled in 2019 compared to the year ago and its import volume is looking to exceed 50 million mt in 2020, and close to 60 million mt in 2021.

Vietnam’s reliance on coal-fired power plants is expected to last for the next few decades. During the funding stage, although Vietnam did not have the financial capability to build coal power plants all by themselves, many Chinese, Japanese and South Korean investors are looking to involve themselves in such projects when banks back away.

As markets develop and we continue to track trade flows in Southeast Asia, Platts Analytics import forecasts for 2020-2021 are subjected to changes.