Examining the Platts IODEX basket and what makes each iron ore brand 'tick'

While hundreds of different iron ore products coexist and compete in the market every day, the five leading brands in the medium fines category stand out.

The intensity of their daily trading activity, their relatively high degree of substitutability and their inclusion in medium grade price benchmarks make them the beating heart of the iron ore market.

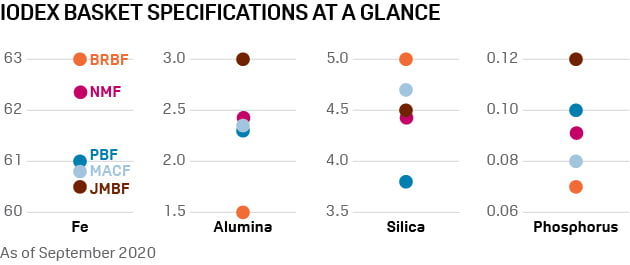

Until 2015, this core group used to include just three brands -- BHP’s Mining Area C Fines (MACF) and Newman Fines (NMF), together with Rio Tinto’s Pilbara Blend Fines (PBF) -- the so-called MNP trio. After Vale’s Brazilian Blend fines (BRBF) and BHP’s Jimblebar Fines (JMBF) were launched and their presence in the spot market firmly established, they were added to the group. Collectively, these five products form the “IODEX basket,” the selection of brands that directly drive the daily movement of IODEX, the industry benchmark.

While close cousins, these brands have differing

characteristics not only in terms of their chemical and metallurgical properties, but also in terms of the way they are traded and shipped, which means that their prices move dynamically on a

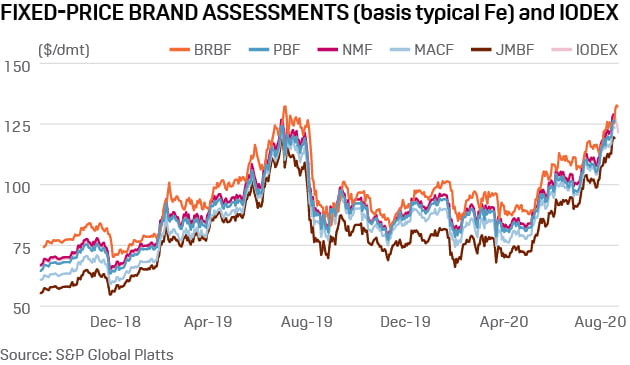

day to day basis. The total price delta between these five core brands is typically $11-$17/mt, and most of the time it is over 10% of the price of a ton of iron ore.

Close to a decade after relinquishing annual fixed price contracts in favor of spot indices, the iron ore market has, in the last couple of years, taken a greater interest in the pricing of these individual brands.

While indices, such as the benchmark IODEX assessment, do a great job of reflecting the price of iron ore as a whole, market participants have been looking for ways to adequately reflect the price difference that naturally exists between iron ore brands and benchmarks.

In September 2018, S&P Global Platts launched individual assessments for these key brands. These assessments reflect the actual value of these brands in the spot market and have been increasingly referred to by market participants in their contractual negotiations.

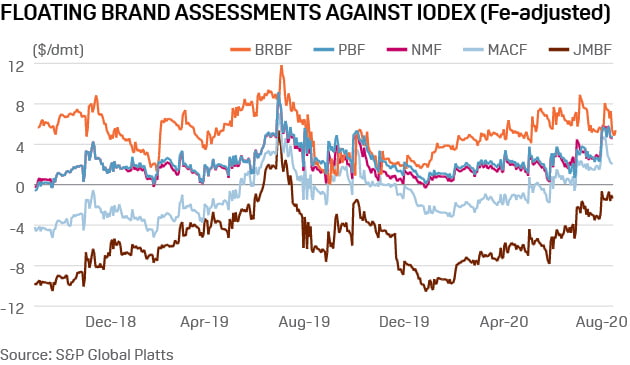

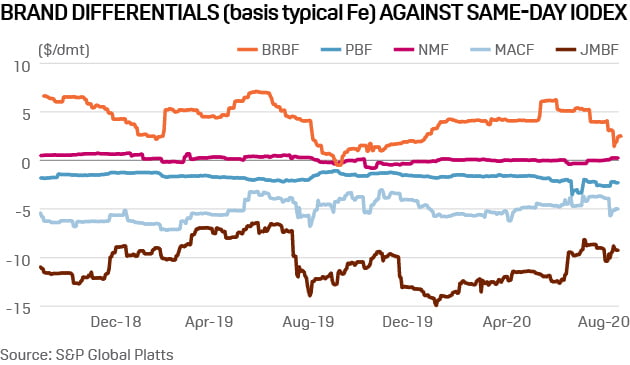

For comprehensiveness and ease of understanding, the same Platts brand assessments are expressed and published in three different ways -- as outright values, as Fe-adjusted premiums to front-month derivatives and as differentials to IODEX.

Firstly, fixed values based on each brand’s typical Fe, or iron, content. These very simply represent the daily outright market value, in dollars per dry metric ton, for each brand at 5.30 pm Singapore time.

Secondly, floating brand assessments are adjusted to 62%-Fe basis and are expressed as premiums to front month 62%-Fe derivatives daily at 5.30 pm in Singapore. Naturally, these premiums will be close to levels observed in the spot market, where index-linked transactions are often concluded in a similar manner.

Finally, brand differentials to IODEX are perhaps the purest expression of a brand’s premium or discount against the IODEX benchmark.

They are not adjusted for Fe, and simply reflect the premium or discount of each brand over that day’s IODEX achievable in outright fixed price transactions.

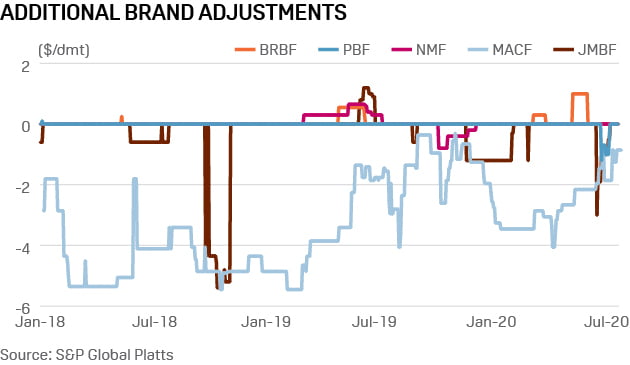

These brand assessments are made up of two components. Firstly, they include calculated penalties and premia reflecting differences in Fe, silica, alumina and phosphorus levels. These penalties and premia are actively assessed and published by Platts, and therefore transparent to the broader market. Secondly, these assessments may also include ‘additional brand adjustments’. These adjustments account for anything else, and typically reflect the spread between the aggregate Fe, silica, alumina and phosphorus penalties, or premia, for a brand and the actual observed spot market value of that brand.

Most commonly, these adjustments will reflect differences in the physical size of the ore and other metallurgical qualities, but can also include commercial or ‘market’ factors.

For one, brands that are produced in smaller quantities are not as widely used in the steelmakers’ sinter blends and therefore

provide fewer re-selling options to traders, giving rise to a “liquidity discount” of sorts.

Another example is the impact of potential short-term supply and demand dynamics.

Any iron ore brand, including those in the IODEX basket, can be subject to temporary oversupply or tightness in the spot market, leading to an extra discount or premium over and above their implied chemical value.

These short-term fluctuations in supply or demand can at times affect a single brand of ore, resulting in a price divergence with the rest of the basket.

Understanding the price drivers of each brand is critical in establishing a robust benchmark, as index compilers should seek to exclude such short-term, single-brand price divergences, which are not representative of the broader market. A good example of this occurred in early July with Rio Tinto’s PB Fines product.

To help contribute towards furthering the understanding of brand price drivers, here is a short analysis of the IODEX basket and what makes each brand “tick.”

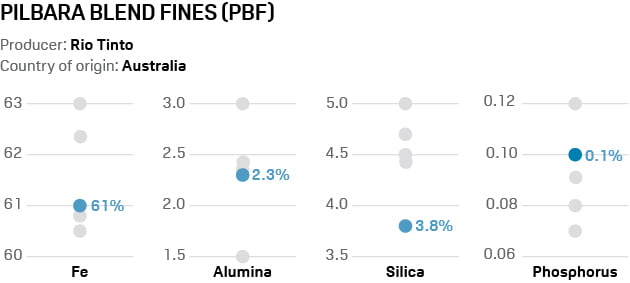

Produced by Australian miner Rio Tinto, PBF is by far the most liquid product in the market given its sheer volume and that it makes up a significant portion of the sintering feed of most Chinese end-users.

Due to its liquidity, PBF is often the choice iron ore brand for speculative buying activity.

Its supply dynamics frequently run parallel with that of the iron ore market, while its specifications are most similar to that of benchmark Platts 62% IODEX. As such, many participants consider PBF trading to be a VIU-neutral play, unlike that of Brazilian fines, as it provides a more generic position on iron ore demand and supply dynamics.

Given its specifications’ close similarities to Platts 62% IODEX, it is largely unaffected by alumina and silica, while its phosphorus levels can subject it to a higher penalty for normalization when end-users are chasing productivity.

It is a common misconception that the IODEX is a PBF, as it is the brand most commonly used in the assessment.

In late June 2020, oversaturation of PBF cargoes in the secondary market following a period of intense selling by Rio Tinto in the first half of June, with 10 cargoes sold on a spot basis and two strip tenders concluded for multi-month shipments.

This led to a steep drop in premiums for the brand from around $2.50/dmt over the arrival month IODEX to around $1/dmt towards the end of the month.

At the same time, prices of Newman, Jimblebar and MAC fines continued to be supported, highlighting PBF as an outlier.

Due perhaps to this oversupply, between June 23 and July 6, PBF was temporarily trading at a discount of 30 cents/dmt to $1.20/dmt beyond the Fe, silica, alumina and phosphorus suggested discounts, which were reflected in the additional brand adjustment.

The large volume of seaborne PBF cargoes and specifically the abundance of cargoes with different laycans means that the brand is often used by Platts to help assess the physical structure -- whether the market is in backwardation or contango -- of the iron ore market.

A market in tight supply tends to steepen the backwardation and it is usual to see early-month loading PBF valued at a significant premium to those loading in the middle or later in the month.

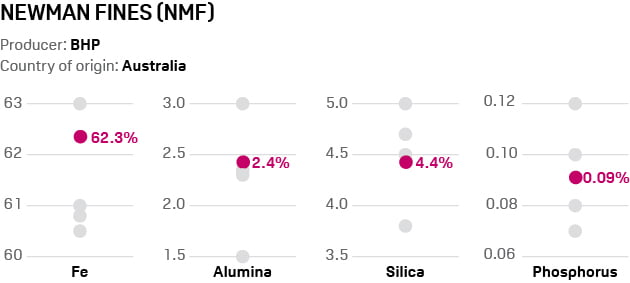

Produced by Australian miner BHP, Newman Fines have similar contaminant values to PBF, but is usually valued at a higher fixed price due to its higher Fe content as compared with PBF.

However, on a Fe-adjusted basis, the higher silica levels for NMF results in a silica penalty as opposed to that of PBF, leading to a larger VIU adjustment and impacting the premium it commands in index-linked transactions.

While end-users generally view both PBF and NMF as ‘silica-neutral’, in relation to their blast furnace sinter feed, the usage of higher silica Brazilian fines from junior Brazilian miners in first-half 2020 has affected end-users’ procurement decisions for Australian fines. They seek to lower the overall sinter feed silica levels to accommodate these high silica Brazilian fines.

Unlike PBF, NMF is usually sold in the spot market on a half-Capesize basis at a price which may include a port optionality for the buyer.

While this may inflate its apparent CFR value, depending on river port market dynamics, it is a factor that is taken into consideration when such transactions are used for assessment purposes.

Like other BHP medium grade products, being sold on a half-Capesize basis also leads to trades of combo-cargoes, or a combination of co-loaded brands, where its market valuation may also be influenced by that of the co-loaded product.

While the dynamics for NMF largely mirror that of PBF given their similar specifications, seemingly minor differences between the brands can be magnified in certain market conditions.

In a bearish market with limited buying interest, the valuation for NMF may decline in a higher proportion as compared with PBF due to its lower volume and use in blends, and therefore its resale potential.

On the flip side, tight inventory levels for NMF at Chinese ports can spark strong buying activity for seaborne cargoes from end-users, who will often prefer to pay an extra premium for NMF cargoes than have to make the necessary adjustments to the blast furnace such that it can process other Australian ores.

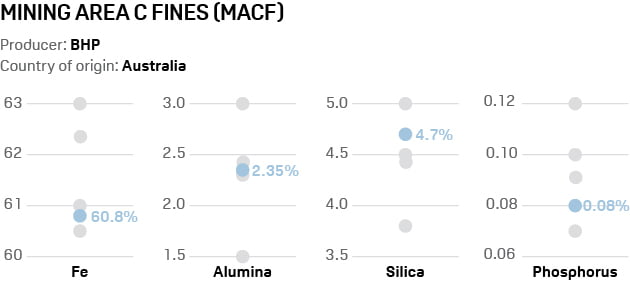

The last of the ‘MNP trio’, MAC Fines, has long been valued by the market at an additional discount in comparison with PBF and NMF due to perceived inferior metallurgical qualities and lower Fe levels.

As a result, MACF is the only one of the five brands in the IODEX basket to have a near-permanent additional brand adjustment to account for these factors.

While its differences are rooted in its physical and chemical nature, its market valuation can be affected by portside dynamics and end-user production rates.

Its finer sizing translates to a higher loss rate during the sintering process as compared with PBF and NMF and a higher loss on ignition (LOI) results in lesser mass remaining in the blast furnace during the initial production stage, which becomes increasingly significant when end-users are looking to maximize pig iron production.

With many end-users using MACF as a ‘replacement’ feed for PBF or NMF, given their similar specifications, its valuation tends to correlate with the market values of PBF and NMF, although not necessarily in a linear fashion.

Another significant difference for MACF, against PBF and NMF, is that its spot market pricing can seemingly be influenced by the monthly and quarterly term contract discounts set by BHP.

These discounts to the 62%-Fe index are offered by BHP to its term customers for MACF, JMBF and Yandi. These term price discounts are closely watched by traders.

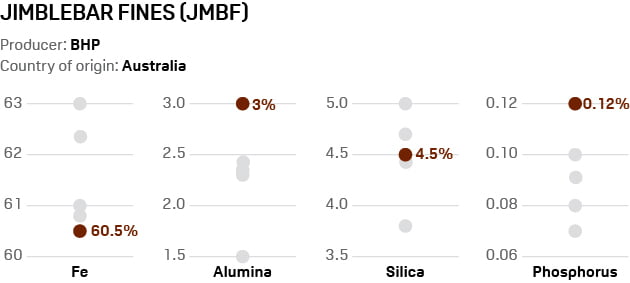

Jimblebar fines are characterized by their high phosphorus content, while its chemical differential to the IODEX are the highest compared with the other four brands.

As a result, it tends to be priced lowest on both a floating-price and outright basis.

While alumina and silica impacts the coking costs and production rates of the end-product, phosphorus, at higher levels, tends to impact the quality of the steel produced by making it more porous and brittle, and by lowering tensile elongation.

This is especially problematic for hot-rolled coil producers where ductility is important.

The nature of hot metal pre-treatment is that tolerance for phosphorus is more significant on an absolute rather than a relative basis, leading to a correlation with production rates.

As such, when end-users are increasing their production rates, the tolerance for phosphorus declines, which usually translates to a weaker buying appetite for JMBF.

It is worth noting that major adjustments to JMBF’s typical specification by producer BHP have had an important impact on its value relative to IODEX and other medium-grade fines.

This was clearly visible during the miner’sspecification adjustment in July 2019, when its Jimblebar’s Fe level was lowered to 59.5%, below the psychologically-important 60% mark, resulting in a decline of about $3-$4/dmt. And when its Fe level was restored in July 2020 to 60.5%, a $2-$3/dmt rise followed.

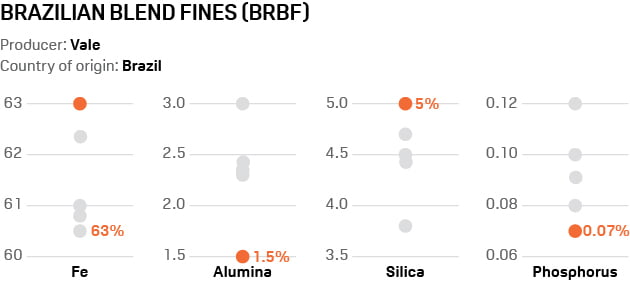

Produced by Vale, BRBF stands as the only Brazilian and non-Australian product in the IODEX basket.

The product is made up of a blend of Vale’s high grade Carajas fines with its Southern System feed, which are blended at its Teluk Rubiah blending facility in Malaysia, or at Vale’s numerous other blending facilities across various Chinese ports.

Thanks to its comparatively low alumina content of 1.5%, BRBF is usually valued at a premium to its Australian counterparts.

While its market value runs largely parallel with alumina differentials, additional brand adjustments have been applied at times to account for the effect of significant supply-side disruptions.

It is another common misconception that BRBF alone dictates the pricing evaluation for alumina differentials, being the only low-alumina brand in the IODEX basket. In reality, alumina differentials can also be assessed by observing non-mainstream low-alumina iron ore brands such as CSN’S IOC 6, Trafigura’s Sudeste and SNIM’s TZFC fines.

BRBF’s vastly different characteristics, origin and customer base can lead to price divergences with the MNP products.

During the period after the collapse of the Brumadinho dam in 2019, BRBF premiums surged significantly more than its Australian counterparts, reflecting a lack of substitutability between them.

Inversely in August 2020, a centralized market demand for MNP due to limited portside inventories led to a weakening in BRBF premiums due to its sufficient volumes at the port and a speculative preference for liquid products.

Increased transparency has gone a long way in helping market participants facilitate a deeper, more rational and communal understanding of each iron ore brand across the value chain. As a direct consequence, and thanks also to refinements in evaluating chemical penalties and premia, iron ore transactions occurring at a given time of day for different brands now routinely normalize to just a few cents of each other.

This should be seen as a welcome and significant achievement for the market as a whole, as it removes complexity and inefficiency, and enables a more robust measurement of benchmark price assessments.

There is no doubt that individual iron ore brands will continue to surprise market observers, but market participants can take comfort in knowing that there are effective new ways to keep track of price movements.

>> Download our Global Iron Ore Specifications Guide

Writer Jun Kai Heng and Julien Hall Editor Norazlina Juma'at Design & Production Lead Martina Klancisar Digital Editor Barbara Lorenzo Caluag Metals Content Director (Asia) Julien Hall

Contact us iodex@spglobal.com

spglobal.com/platts