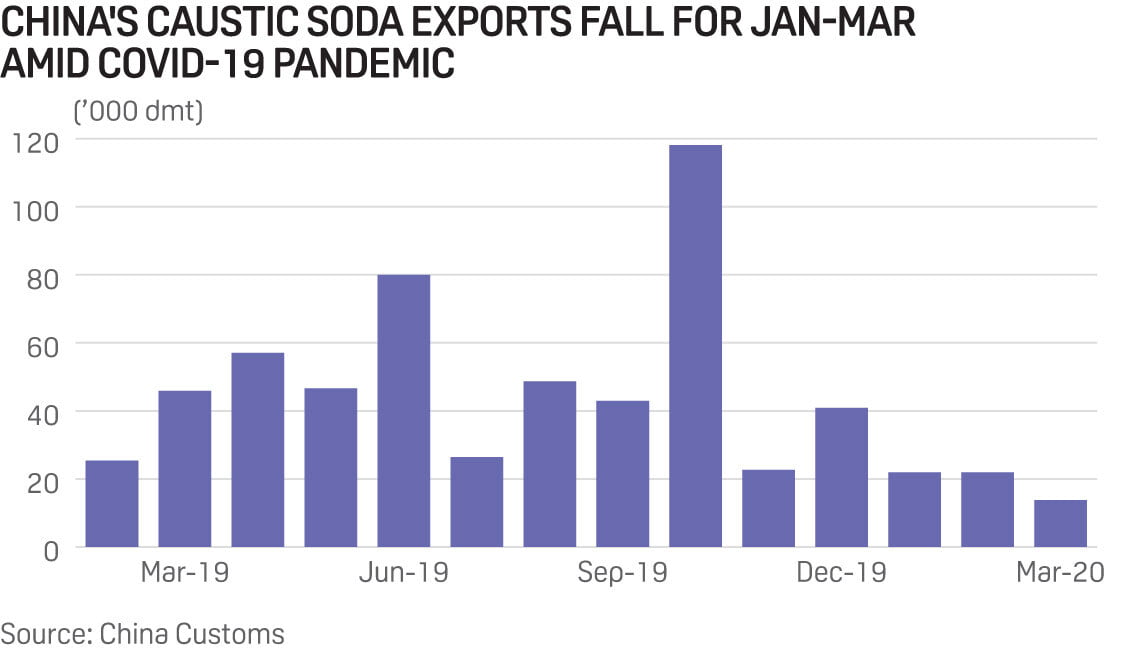

Caustic soda could see downturn in H2 after COVID-19 price boost

Low chlorine demand prompts chlor-alkali rate cuts

Caustic gains could soften if industrial demand remains weak

The global caustic soda market will likely see a downturn for the second half of 2020 as a supply-driven price boost from reduced chlor-alkali rates deflates, market sources said.

Lockdowns amid the global COVID-19 pandemic eased in May and June, but demand, which was already soft through 2019, remained uncertain

India’s lockdown, which started in late March and softened in May, could last at least for few months and the country may even return to full restrictions, depending on the spread of COVID-19.

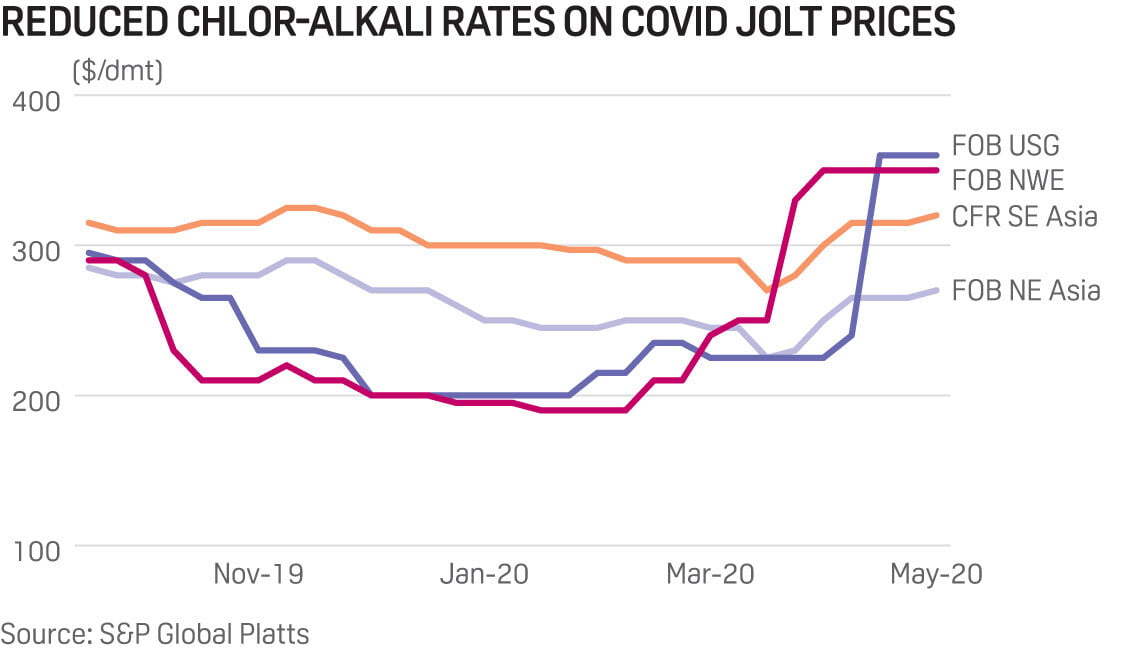

Caustic firms on limited supply Through the second quarter of 2020, global caustic soda prices firmed as producers reduced chlor-alkali rates, triggered by weak demand for chlorine and products throughout the downstream PVC chain.

Before the COVID-19 outbreak, prices had been relatively soft on weak demand in alumina and pulp and paper industries, for which caustic is a key feedstock. The FOB Northeast Asia caustic soda price rebounded by 20% to $270/mt in mid-May from $225/mt at the end of March, S&P Global Platts data showed.

US export caustic prices shot up by more than 75% between the end of March and June to reach $395/dmt FOB USG, with US producers having announced a third round of price increases so far this year for domestic material, seeking to capture that supply-driven opportunity.

The FOB Northeast Asia caustic soda price rebounded by 20% to $270/dmt in mid-May from $225/dmt at the end of March, then fell back to $250/dmt by early June, S&P Global Platts data showed.

However, demand may not support the stronger pricing levels — at around $650-750/mt — seen in Europe during the 2008-09 financial crisis and 2018 mercury cell upgrades.

Market sources said Asian caustic soda demand remained healthy in the first half of 2020 despite the COVID-19 pandemic, amid high alumina refinery operations. India continued to import caustic soda despite its lockdown as well. China is the world’s largest alumina producer, with half of global output.

“It takes months to adjust operations at an alumina refinery. For the first half of this year, a demand-and-supply condition was imbalanced as caustic soda demand remained healthy due to high alumina operations, while caustic supplies were limited on lower chlor-alkali operations,” a Japanese producer said.

The producer added that caustic soda demand in Asia would likely soften in the second half of the year in line with falling alumina refinery operations, likely pressuring caustic soda prices.

In the US, Olin might fast-track its closure of a 230,000 mt/year chlor-alkali facility in Texas by year-end, Chief Operating Officer James Varilek said in May, leaving the issue open-ended.

"What we're going to do is to take a look to see how demand materializes," Varilek said. "We'll assess what we need to do over the next several months."

Price strength could be short-lived US market sources also said that, if industrial demand remains soft as was the case pre-COVID-19, caustic soda’s pricing spike would likely be short-lived. Export prices reached $400/mt FOB in late May, but appeared prevented from rising further, particularly as chlor-alkali rates slowly ramped back up, increasing caustic supply.

That said, with domestic price increases pending and caustic supply on allocation through May, Olin CEO John Fischer said that the company in the short term at least was “bullish on caustic pricing.”

In Europe, caustic availability through the rest of the year is expected to remain limited, with demand somewhat flat.

“The market is short in caustic but the demand is still weak,” a European producer said.

Market sources said that, even with the lockdowns eased, it would take some time for the economy to recover, as end-user demand difficulty will continue for months, possibly into 2021. A European source noted that economic indicators pre-COVID were “not rosy,” and activity was not expected to bounce back to what it was before the outbreak.

“No one is going to buy a car, or a house and start renovation,” the source said.

European chlor-alkali plant capacity utilization stood at 80.9% in March, down 6.9% from February, while caustic soda stocks stood at 209,701 mt, 13% below February levels (241,996 mt) and 28% down year on year, according to Eurochlor.

Market sources said that April data will be also fully affected by the COVID-19 effects, with European plant rates expected at much lower than 80%. US market sources expect April rates to be 75% or lower, down from 90% in March.

In addition, some chlor-alkali plant turnarounds in the US and Europe, typically planned for spring, have been delayed as COVID-19 stay-at-home orders reduced subcontractor availability or companies sought to limit the numbers of people at plants to prevent COVID-19 spread. Delayed turnarounds could limit rates in the latter half of 2020 as well, potentially giving prices another supply-driven boost.

— Kristen Hays Fumiko Dobashi Ora Lazic