Global PE braces for supply glut, stiffer regional price competition

Demand levels by end-use vary in the wake of COVID-19

Uncertainty amid fears over economic growth

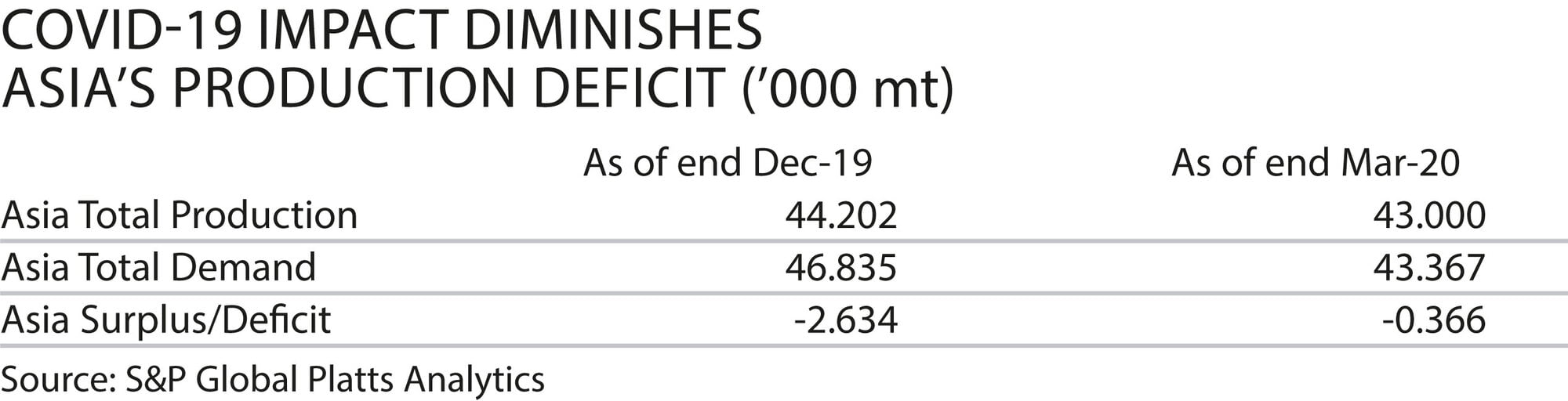

Uncertainty surrounds the global polyethylene market after the coronavirus pandemic idled suppliers, curbed demand and pressured prices, some to all-time lows, during the first half of 2020. PE supply conditions post COVID-19 were in question following potential delays to planned expansions in 2020 to 2021 from weaker demand, sources said. Some traders, meanwhile, were optimistic over the outlook on the back of rising demand in China and the likelihood of less cost-efficient producers reducing production rates.

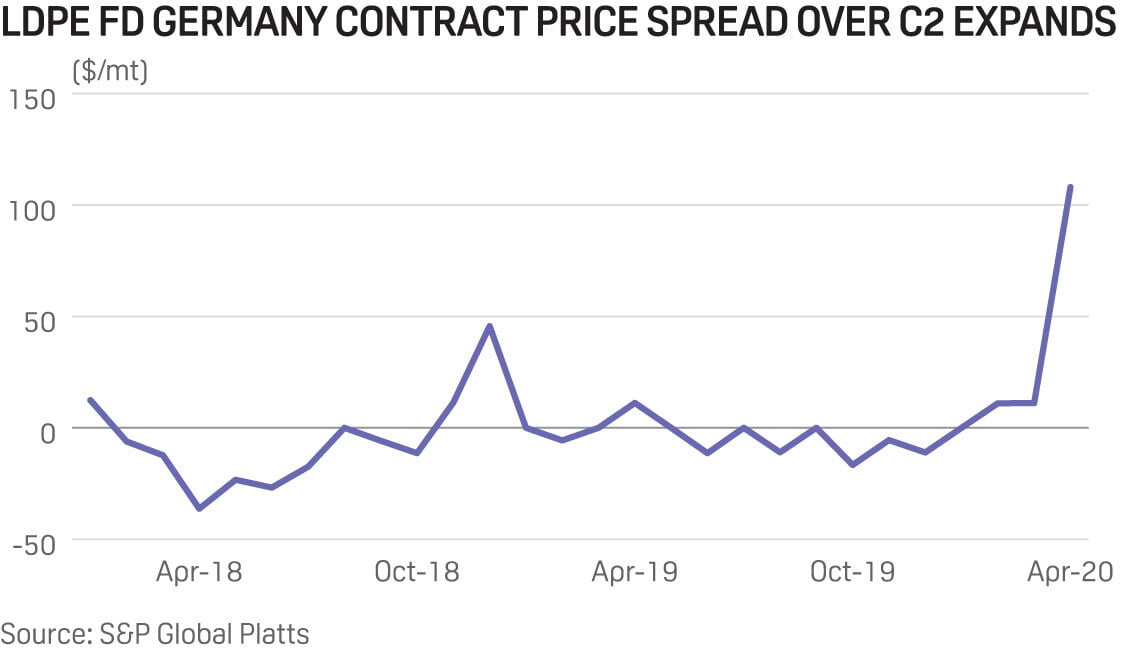

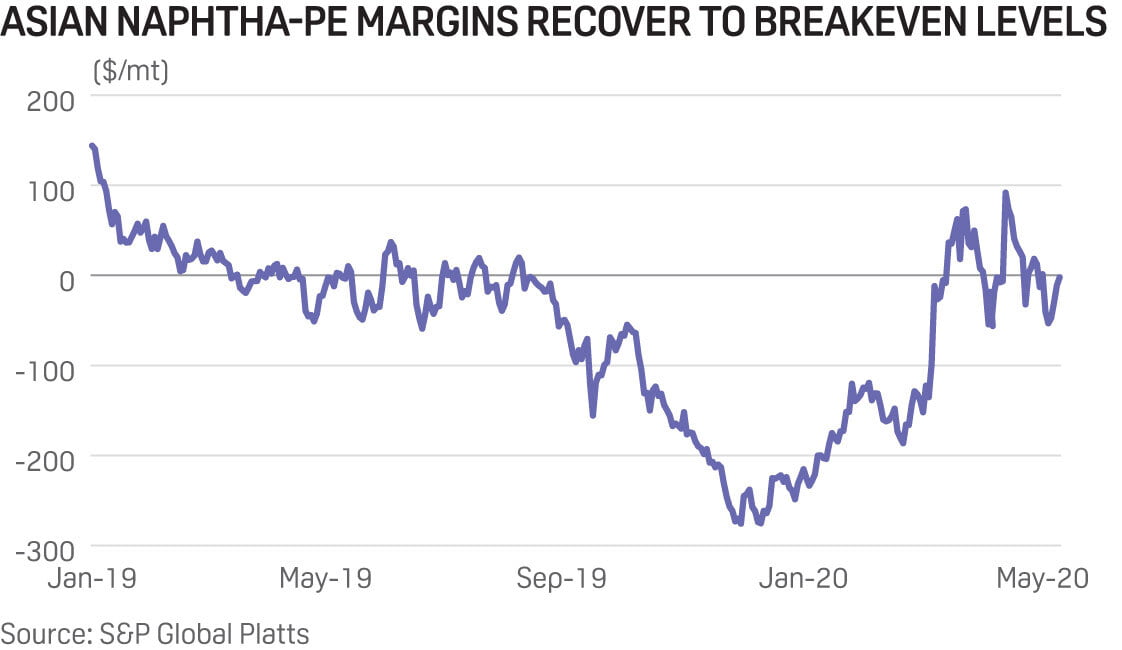

European, Asian PE margins improve Cost differences in differing PE production methods narrowed because of volatility in feedstock values recently, subsequently eroding cost advantages of ethane-based US producers and shifting cost advantages to naphtha-based producers instead, sources said.

Producer margins based on ethylene cost comparisons for Europe and naphtha for Asia turned around in H1 2020 as the pandemic took hold, and this is expected to continue heading into the second semester as the two regions gradually regain the cost competitiveness lost to US shale-based producers in recent years, sources said.

The monthly European ethylene contract price against the monthly low-density PE contract price showed that margins increased in February for the first time since April last year. However, real significant gains were made in April, as PE margins widened by Eur100/mt, according to S&P Global Platts data.

In Asia, naphtha-based PE margins rose to near breakeven levels in mid-April from negative $200s/mt around the start of the year, according to Platts data.

"Curious how the US producers can survive in this [low oil] environment.”

Asian PE prices have largely trended in line with crude oil’s general price movements, sources said. Some crude-oil based producers were more positive on the outlook for PE, citing it as one of the better performers among the suite of petrochemical products.

Uptick in demand for food, cleaning, healthcare packaging Some sources predict a return to normal demand in the third quarter of 2020 at the earliest. Lockdown measures, meanwhile, have spurred demand for flexible packaging for food, cleaning and pharmaceuticals, boosting producer margins, while lower feedstock costs and a slowdown in imports have reduced competition and kept supply-demand fundamentals balanced in the domestic markets, sellers said.

Packaging, consumer and healthcare markets will continue to fare better, while demand may remain weak for other sectors as a result of the "work from home” culture, lower exports of finished goods, and cash flow problems, sources said.

Some buyers said the next traditional peak demand season in Asia might be in late November, in preparation for Chinese New Year. Some traders, meanwhile, said prices may move lower during the year-end as more US material typically arrives at Asian shores before the fiscal year closes to reduce payable taxes.

Traders said the various economic stimulus by governments had had some effect in propping up the PE market, but said export demand for general finished plastic goods in Europe and the US would not be recovered for the full year. Sources also said the overall annual global growth rate was likely to be lower.

Low US prices had many Chinese traders scrambling to book materials for arrival in July, given that a number of companies were successful in applying for 27.5% tax exemptions, sources said.

The exemptions, which importers were able to apply for from March 2, will last for one year, starting from the date of approval, and will be granted on the basis of market value instead of volume, the Chinese ministry of finance said.

More supply expected in H2, albeit with delays Delays are expected in new steam cracker startups, given market uncertainty on top of efforts to protect their own financial health, producers said.

Additional capacities in Asia totaling 2 million mt/year might be delayed to 2021 as a result of the coronavirus pandemic.

In the US, Sasol was commissioning a new 420,000 mt/year LDPE plant at its Lake Charles, Louisiana, complex in January when a fire prompted a shutdown for lengthy repairs, and its startup was pushed to the second half of the year. The unit is expected to reach beneficial operation in the third quarter, spokeswoman Kim Cuismano said. Formosa also delayed the January startup of its new 400,000 mt/year LDPE plant in Texas to late July or early August, a spokesman told Platts in May.

— Hui Heng, Miguel Cambeiro, Jacquelyn Melinek, Eric Su

Uncertainty, slide in demand leads sentiment into H2 2020 for PP

Chinese PP capacity up 10%

Auto sector improvement expected

US proceeds cautiously

The impact of the coronavirus pandemic on the global polypropylene market is expected to last beyond the summer, with ongoing uncertainty on the demand outlook from automotive and healthier demand for hygiene applications.

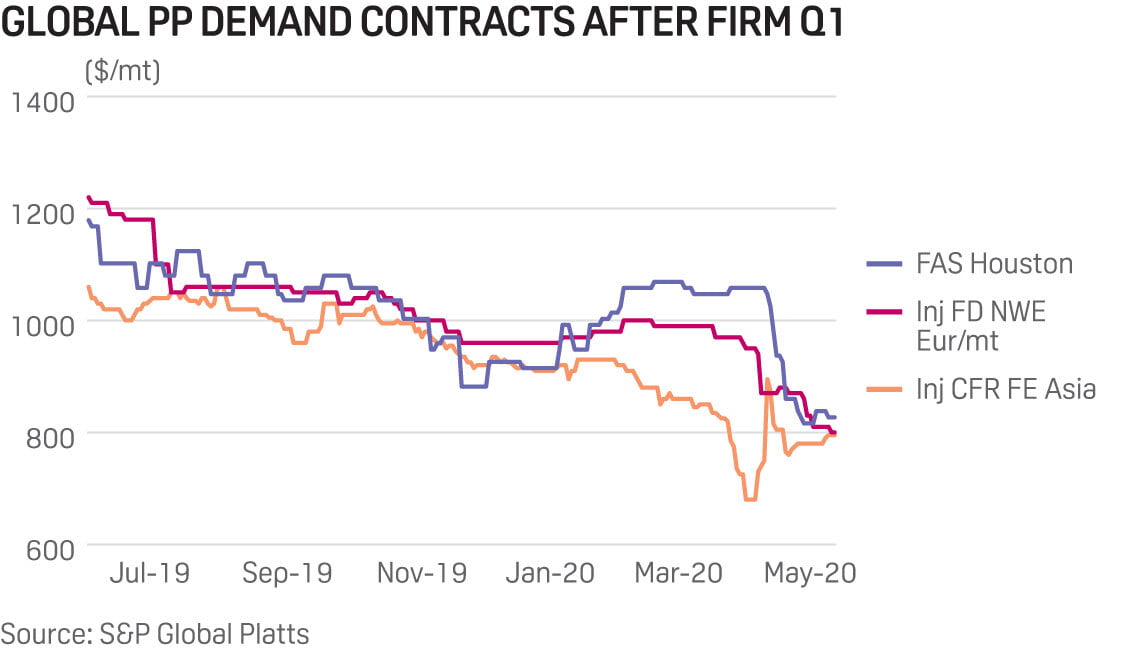

Asia supply to increase Asian polypropylene fundamentals are likely to remain bearish amid expected new startups, although overall demand should gradually improve with coronavirus concerns easing in the second half of 2020.

Total Chinese PP capacity is expected to increase by 2.7 million mt/year, or around 10%, in H2 2020, according to S&P Global Platts data and market sources. With the new capacities and demand destruction due to COVID-19, Asia is estimated to be net short of PP by 0.4 million mt in 2020, down from 2.3 million mt in 2019, Platts Analytics data showed.

Nevertheless, market sentiment is mixed, with some sources citing potential bullish upstream propylene and production losses from refinery cuts. As a result, the room for polypropylene prices to fall further is limited with prices already at record lows, a source said. Asian prices hit $680/mt CFR FE Asia for raffia grade in early April, a record low, before recovering to the high-$700s/mt and low-$800s/mt in May, according to Platts data.

In the automotive sector, China — the world’s largest auto market — will be supported by the gradual recovery of domestic demand in H2, as exports accounted for only a small percentage of the total automotive production — 4% in 2019, according to China Association of Automobile Manufacturers.

However, Japan and South Korea's automotive sectors will face greater uncertainties in the global environment, with tie-ups and consumer bases straddling both developed and developing countries.

S&P Global Ratings' credit team projected in a recent analytical report that global light vehicle sales will fall below 80 million units in 2020, a near 15% decline from the 90.3 million units produced in 2019.

Europe to benefit from easing lockdown Demand for European PP is likely to see an improvement heading into the second half of the year as government lockdown measures are eased and key sectors restart operations.

Demand from the automotive sector in particular will improve as car factories reopen alongside easing lockdown restrictions, with supply in the second half of 2020 likely to be fed by imports from Russia, where prices are expected to be competitive, participants said.

European demand for PP collapsed in the first half of the year as the coronavirus pandemic hammered the key automotive and construction industries and brought them to a near standstill across the continent.

As consumption slumped and propylene prices went south, European polypropylene was sent tumbling in the first half. European PP spot prices fell 15% from Eur960/mt at the start of 2020 to Eur810/mt in early May, according to Platts data. However, some participants said they thought prices were bottoming out in May, with some signs of recovery in upstream naphtha prices.

Some of the lost demand was offset by a surge in demand from the food packaging and hygiene sectors, driven by consumer panic buying of food and sanitizer products, partially mitigating the price drop. Converters were running at full capacity to meet the spike in demand, which continued into May.

Meanwhile, demand for hygiene and medical applications will remain strong in the second half of the year, with demand for food packaging expected to return to pre-pandemic levels as consumer panic buying diminished.

US market participants brace for rocky H2 US polypropylene for domestic and export use also face looming uncertainty as several stalled sectors including auto manufacturing threaten to further diminish demand amid ongoing coronavirus concerns, sources said.

The first half of the year grappled with an unprecedented crisis that pressured pricing to historic lows despite initial firm demand from the medical industry.

A heavier-than-usual turnaround season was also heard to be contributing to the tightness of material for medical supply, sources said.

US spot export pricing rose $143/mt or nearly 16% from January 2 to March 31, Platts data showed. Still, as coronavirus fears grew and manufacturing slowed, pricing trended to its lowest in over 11 years and was assessed at $816/mt on April 29, down 26% year on year. Weaker contract monomer was also attributed to the fall.

Market participants are taking a wait-and-see approach as the country continues to ease restrictions and states re-open for business. Traders and distributors said the challenge lies in balancing inventory amid an expected upcoming slowdown.

From an export standpoint, the sentiment is more bearish. Exports to key markets have been difficult, including to Latin America, which have been propped up by cheaper polypropylene from the Middle East and Asia.

There is talk that certain grades will remain strong, including grades for medical applications, as the world deals with the aftermath of the pandemic.

— Emmanuel Gallegos Miranda Zhang, Abdulaziz Ehtaiba

PVC demand facing slow climb to pre-pandemic levels in H2 2020

Pandemic crushed demand for construction materials in Q2

Eased shutdowns allowing for gradual rebound

Construction staple PVC faces an uncertain rebound in terms of prices and demand from a ruthless coronavirus pandemic-induced nosedive as global markets look ahead to the rest of 2020.

As regions work to overcome economic shocks and emerge from widespread lockdowns, buyers of the powder used to make pipes, window frames, vinyl siding and other construction products are trying to gauge when hammers and backhoes will be back in action.

PVC’s fortunes have always been closely tied with economic health and GDP growth, and the pandemic has brutalized both. The International Monetary Fund expects the global economy to shrink by 3% in 2020, with no growth in Asia as a region for the first time in 60 years. The IMF expects the US economy to shrink by 5.9%, and Europe's by 7.5%. In the US alone, 33 million people lost their jobs through April, federal data show. Such prospects leave PVC producers and traders worldwide cautious and hopeful that resumptions of economic activity proceed slowly to prevent a second wave of shutdowns and job losses.

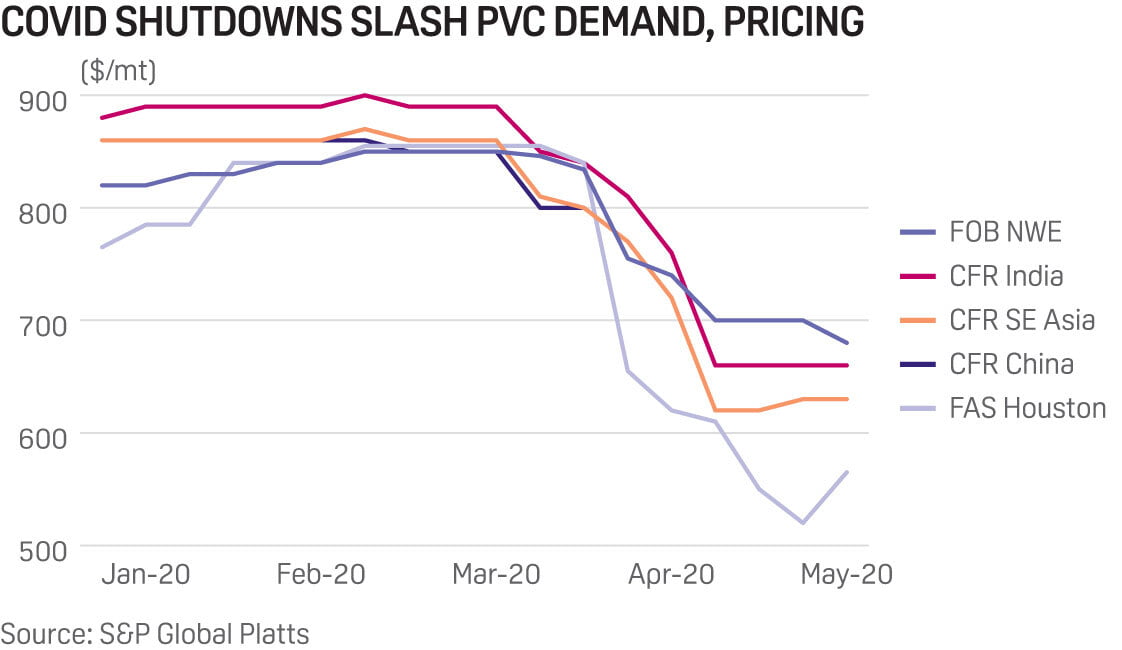

India lockdown showed global ripple effects India's lockdown, first imposed March 25 and repeatedly extended with eased restrictions through the end of May, threw international PVC markets into turmoil as countries that routinely supply the net PVC importer sought other destinations for their product. That intensified competition with US and European exporters as all chased the same shrinking pockets of demand.

CFR India PVC prices fell to a record low of $660/mt in early April, and CFR China prices plunged to an 11-year low of $620/mt, S&P Global Platts data showed. US export PVC prices fell 39% to $520/mt FAS Houston between the middle of March and the end of April. European prices plunged 29% to $600/mt FOB NWE between early March and mid-May, and CFR Turkey prices fell 33% to $620/mt between February and mid-May.

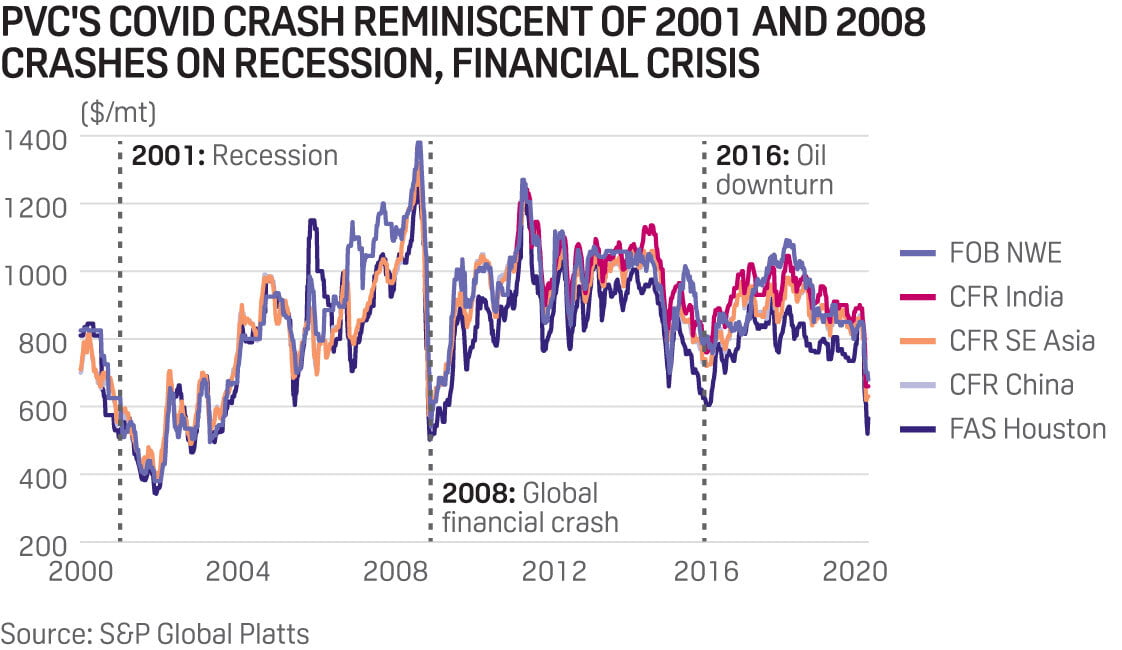

By June prices had rebounded almost as sharply. However, market sources saw those moves more as pre-buying ahead of higher prices than a real recovery, which was expected to be slow, much like that after the 2008-2009 global financial crash.

“Business will be less than expected this year. Nobody knows how this will play out in the coming months,” a European PVC converter said, adding that there was “uncertainty in prices also, and we hope for better demand, and the construction to start again, but its very difficult.”

Pandemic-related shutdowns that squashed construction activity came when many regions typically are stocking up on PVC to get products made in time for the peak summer construction season. Demand was seen as healthy until it suddenly was not.

Adding that the month of “Ramadan ... also is not helping. India is dead, the biggest import market, number two market Turkey – very bad. This will be a slow process, even when lockdowns open.”

India normally imports 2 million mt/year of PVC, but sources expect demand there to remain soft through 2020 as public project delays linger on top of the June-September monsoon season, sources said.

Podcast: PVC markets feeling the force of pandemic's global impact

China PVC makers push for new anti-dumping duties In China, PVC makers in April revived a push for the government to impose anti-dumping duties on US-origin PVC, which were lifted last year. Chinese manufacturers voiced concerns that the US would flood Asia with imports as the region first hit by coronavirus shutdowns was among the first to resume some normalcy. That process involves months- or years-long investigations.

US export data show China received 61,233 mt from the US in the first quarter of 2020, down 40% from the same period last year when those duties were in effect, reflecting its demand squeeze from widespread shutdowns during those months. China Customs data show the US flows were 45% of China’s total imports in Q1.

And in Latin America, where markets are heavily influenced by prices in Asia, the US and Europe, market participants expect to see the most bearish demand in years for the rest of 2020, sources said. PVC consumption in Latin America reached nearly zero with prices at historic lows, but domestic output gained favor as exchange rate volatility due to uncertainty induced by the pandemic saw currencies across the region depreciate.

Albert Chao, CEO of Westlake Chemical, said in early May that PVC demand could benefit if governments invest in infrastructure to stimulate economies in the short term, and longer term if more consumers seek single-family homes to gain distance from concentrations in multi-family dwellings. But blistering levels of job losses are expected to hamper big-ticket purchases like homes.

“Time will tell when that demand comes back, depending on economic recoveries.”

— Kristen Hays, Ora Lazic, Fumiko Dobashi

Global PET markets face bearish H2 2020 sentiment

Major event delays reduce, shift demand

Consumer stockpiling wanes, expected to shift to new normal

Polyethylene terephthalate demand saw a boost from bottle and food packaging sectors in the first half of 2020 from the coronavirus pandemic, but more bearish sentiment looms in H2 2020 for upstream feedstock markets and global supply-demand imbalances.

Postponing or shortening major events where millions of bottled beverages are typically sold, from the Summer Olympics to US Major League Baseball and European football championships, has left markets facing demand shifts and adjustments that are expected to linger through the rest of the year.

PET’s crude link may attract switching from PE, PP Asia’s bottle industry expects some demand recovery as countries come out of lockdown and consumer activity begins to return to normal.

However, the year-long delay of the 2020 Olympics in Tokyo and other large-scale events and gatherings has left some market sources not so optimistic.

There also may be some demand moving into the PET market from other polymers, a producer said. As packaging producers evaluate feedstock prices, some expect to switch from polyethylene and polypropylene to PET, as its close link to crude may benefit from sharply lower oil prices.

Another factor that producers must face in H2 2020 is a supply and demand imbalance. China is likely to remain a net exporter, and increased capacity is expected to prompt Asian producers to seek more export opportunities to the US, Africa, Europe and the Middle East.

Achievable prices for Asian PET remain uncertain, however, given volatility seen upstream in crude oil, paraxylene, purified terephthalic acid and monoethylene glycol markets. Non-integrated producers will feel the greatest pressure from those markets, while integrated producers can better weather the storm.

US PET import needs to remain strong with complex construction delay One key recipient of the Asian PET supply length in H2 may be the US, partly because of a further delay of the world’s largest PET/PTA complex under construction in Texas. The plant, co-owned by Thailand’s Indorama Ventures, Mexico’s Alpek and Taiwan’s Far Eastern New Century, has been delayed another two years to 2023 due to higher-than-expected labor costs.

The 1.1 million mt/year PET plant, originally slated to start up this year and initially delayed to mid-2021, will decrease US PET import needs, just later than planned.

The US imported nearly 3 million mt of PET in 2019, according to US International Trade Commission data, with Mexico the top source, having shipped 28% of the total.

So far in 2020, PET supply has not been a problem in the US, despite many large beverage companies reporting strong PET demand for plastic bottle production in the first quarter, particularly for water. PET imports in the first quarter fell 17% from Q1 2019, reflecting global production cuts and reduced overall demand amid the coronavirus pandemic.

What are US Recycled plastics PET price assessments?

Read more

What are European Recycled HDPE price assessments?

Offsetting the better demand in the beverage sector was, and is expected to be through to the end of the year, suppressed demand in the fiber market. This is especially seen in the carpet production industry. Weak consumer activity and widespread shutdowns in textile, pipe, and automotive industries was expected to hamper growth through H2 2020 as consumers back off from big-ticket purchases like vehicles or homes.

As in Asia, the postponement and cancellation of large events and gatherings over the summer is expected to trim PET bottle demand, with producers assuming the effects of which will be felt “for the remainder of the year,” according to Alpek CEO José de Jesús Valdez.

European producers focused on maintaining market share Following a stark drop in import PET volumes into Europe for H1 2020, domestic producers will be keen to maintain market share in H2, with memories of 2019 oversupply still fresh.

However, even with lower import volumes, buyers will still be afforded negotiating power, with PET prices just starting to feel the effect of a bearish feedstock market in May. At the beginning of the year, the PET margin over PX and MEG stood at Eur264/mt; by mid-May, it had risen to Eur434.50/mt.

Despite falling PET prices, strong demand emerged from the beverage and food packaging sector across Europe as consumers stockpiled groceries during the pandemic, giving PET prices strength over feedstocks. Market participants expect that margin to shrink in H2, in part because of reduced consumer demand as stockpiling eases and consumers adjust to a new normal.

Mostly, that demand decline will stem from major event cancellations over the summer, including the European football championships, which have been postponed.

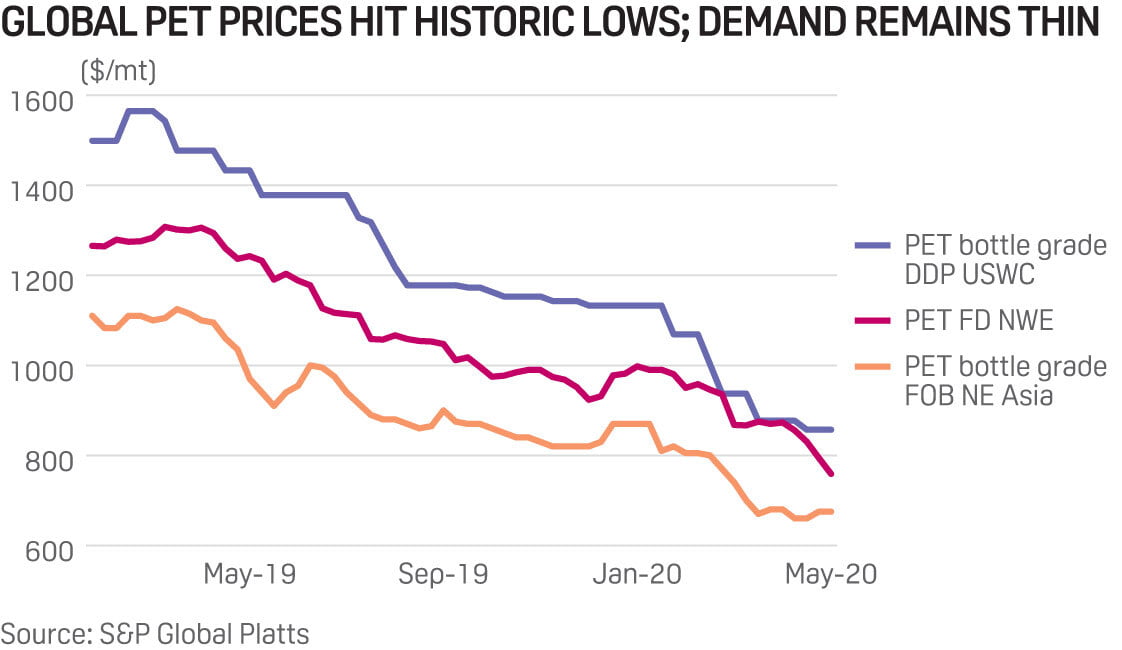

PET prices in Northwest Europe had already fallen below lows seen in the 2008-2009 global financial crash, pricing at a low of Eur700/mt FD NWE on May 13. With oil prices expected to remain low at least for the remainder of the year and the potential for competitively priced imports from Asia, buyers will be looking to revert the margin over PX and MEG to a more historically in-line price.

— Benjamin Brooks Sarah Schneider Chris Liu

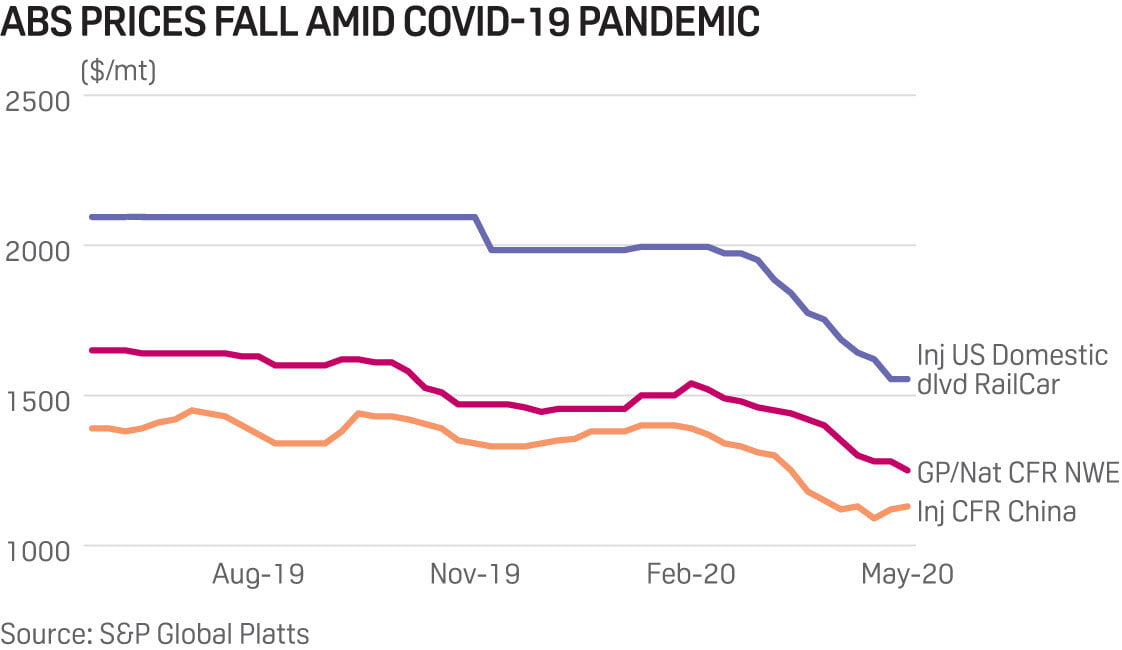

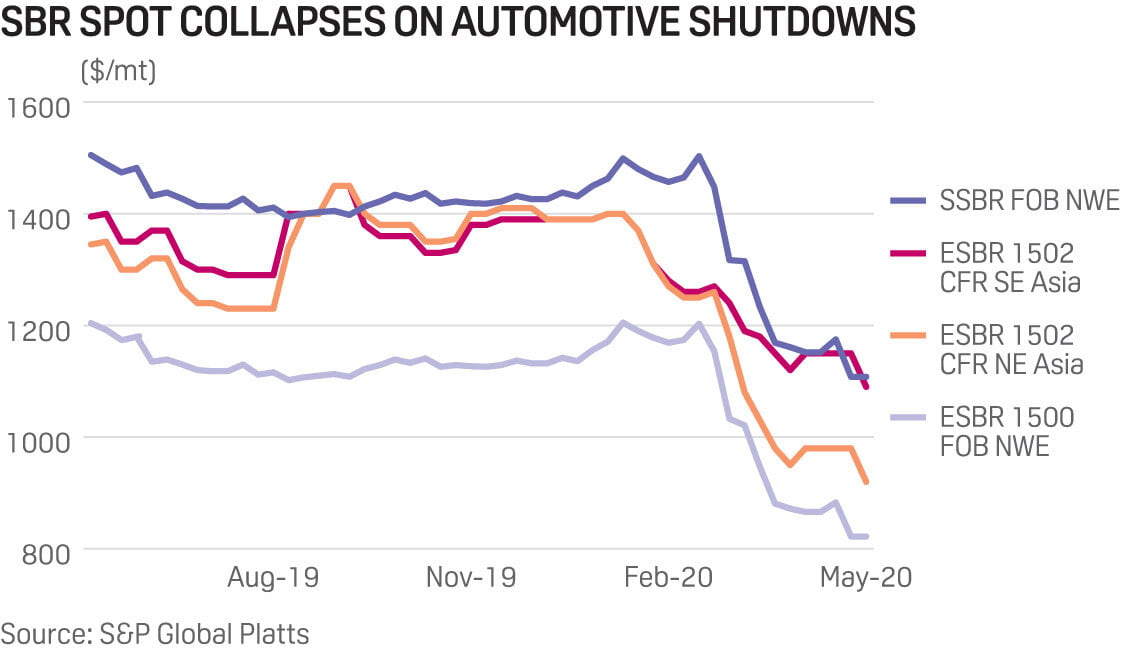

Global ABS and SBR markets to see continued pressure amid tepid demand in 2H 2020

Global ABS demand expected soft during the second half of 2020

Automotive sector demand key to SBR’s fortunes

Asian styrene-butadiene-rubber would likely remain under pressure for the second-half of this year as weak automobile sales would continue to slash tire demand.

For the first half of 2020, Asian SBR market dropped to a record-low, due largely to lower automobile production amid the coronavirus pandemic. Meanwhile, competition with natural rubber will continue in the second-half of this year.

Asian acrylonitrile-butadiene-styrene is expected to see market recovery in the second half of 2020, with demand from China continuing to support the market. It will also find cues from feedstock styrene market movement as the weakness in styrene has translated to improved ABS production margins.

Demand recovery in automobile and home appliances sector remains a top concern for the Asian ABS market, while China’s demand is regarded as the main contributor.

China’s automobile sector, a key downstream of SBR and ABS, was hit heavily on both the production and demand front due to the coronavirus outbreak in early 2020. In Q1 2020, auto production in China plunged 45.20% on the year, while auto sales suffered a plummet of 42.40% on the year, according to data from the China Association of Automobile Manufactures. However, following the eased restrictions in China, both auto sales and production surged on the month in March and market participants expected to see more macro-economic policies to spur the sector in the coming months.

Although the market is progressively returning to normal, uncertainties over the coronavirus and global trade tensions continue to loom the market and some sources were cautiously optimistic about the outlook amid market volatility.

Bearish outlook for European markets as automobile picture remains bleak In the European markets, sources were unsure on when ABS would stage a recovery noting any rebound was dependent largely on automobile production levels which looked set to remain significantly reduced for much of the remainder of 2020.

However, sources noted that the ABS market was unlikely to come under a great deal of pressure initially from feedstock, with butadiene expected to be similarly impacted by the automotive sector downturn.

Sources noted that the likelihood of a significant European recession was likely to provide little support to the white goods and home appliances sector, with buying activity expected to remain limited.

The European SBR markets were even further exposed to the state of the automotive sector, with some 70% of European SBR produced going into tire production. SBR sources remained pessimistic about the remainder of 2020, again noting the macroeconomic outlook and subsequent impact on buying patterns.

“The real concern now is that requirement for original or replacement tires won't be good for several years,” an SBR source described.

Market sources also described how substantial stocks had built up at tire producers prior to the lockdown, with the inventory situation being further amplified during the spring lockdown when, at one stage, every major European automobile manufacturer had halted production. The substantial tire stocks were heard likely to prove a further obstacle to SBR demand as tire manufacturers looked to clear backlogs of inventory.

US ABS market expects continued soft demand US ABS market participants anticipate continued soft demand for the second half of the year with a possible recovery as the automotive industry restarts in the fourth quarter.

Due to demand destruction from the coronavirus pandemic, prices fell to 11-year lows in the first quarter of 2020 as many automakers, which make up a large segment of ABS users, halted assembly lines in the first half of the year.

With a depressed automotive industry, there is little demand for upstream butadiene. Upstream styrene and ACN were also depressed on weak demand during the first quarter.

According to market sources, demand will improve when the automotive industry recovers. The automotive industry could come back strong, anticipating improvement in the second half for butadiene and styrene, translating to improved demand for ABS, one source said.

5Demand for styrene derivatives is expected to pick up in the second half, as some automakers announce plans to ramp back up, market participants said.

— Sophia Yao, Callum Colford, Fumiko Dobashi, Astrid Torres

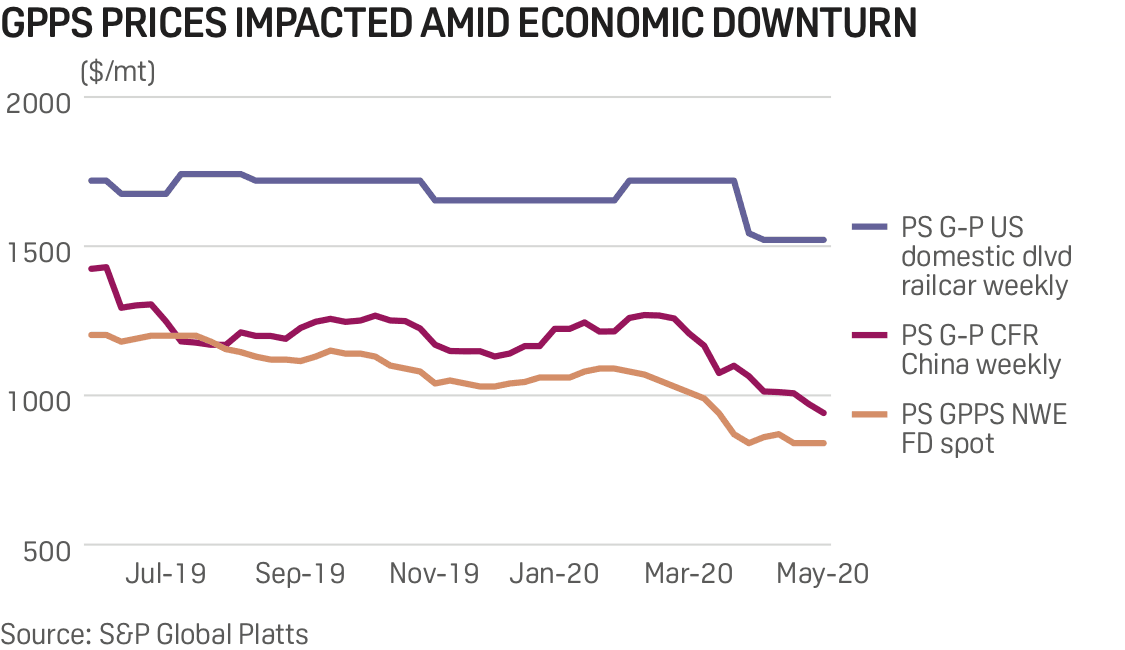

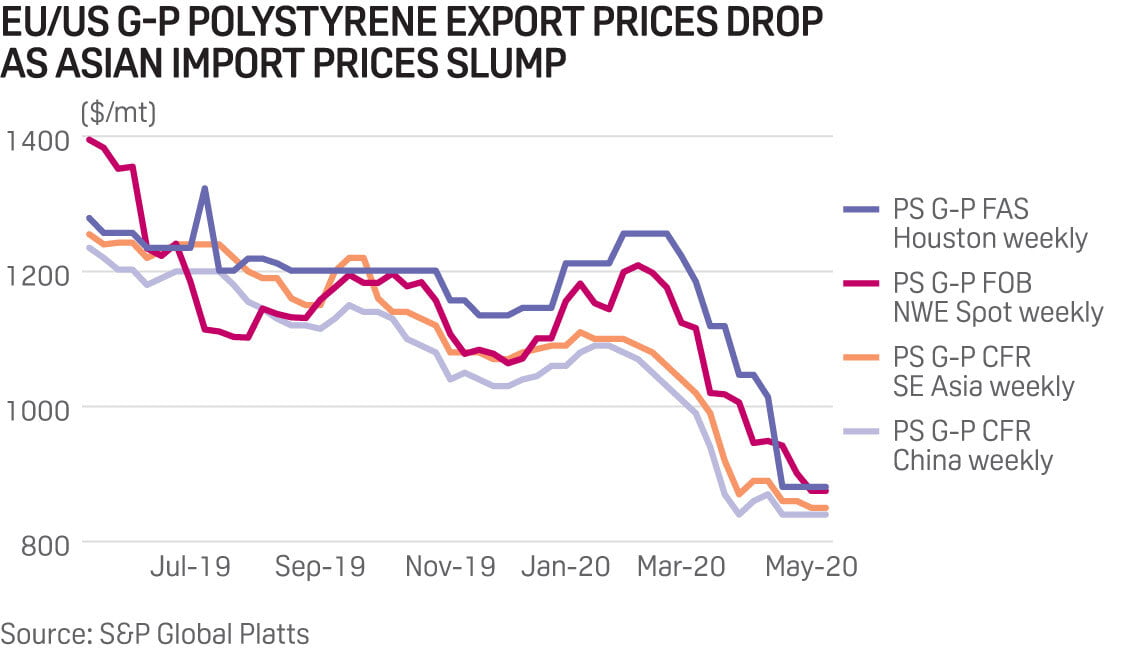

Construction, feedstock supply key drivers for global polystyrene recovery in H2

Feedstock supply glut in Asia supports production margins

Food packaging, medical applications to draw on polystyrene

Headed into the latter half of 2020, the Asian polystyrene market is expected to rebalance on the closure and commissioning of supplies, and PS will continue to mirror the price movement in feedstock styrene.

Meanwhile, the resumption of demand remains the key question in Europe, with the construction slowdown heavily hitting the expanded polystyrene market. Polystyrene prices have been exposed to extreme volatility in upstream markets in the first half of 2020, and this is likely to set the tone for the second half of the year.

US polystyrene demand is unlikely to see an improvement, though prices are set to gain following a slow rebound in upstream benzene and styrene markets.

Asian PS supplies to rebalance On the supply front, two major polystyrene producers in Asia will exit the market due to a bearish long-term outlook. Denka will terminate its 200,000 mt/year general purpose polystyrene line in Singapore in late 2020, and Chi Mei Corporate also ceased to produce general purpose polystyrene at its Tainan plant in May. However, such supply losses will be compensated by several new supplies to be brought online in China over 2020-2021.

PS production margins have improved since late 2019 and are expected to remain healthy, as a supply glut in styrene would pressure feedstock prices while demand seems to be recovering. However, positive spreads have led to higher run rates in China, which may persist to the second half of the year. It will also trigger a collapse in prices if supply outstrips demand amid the absence of end-users.

Demand for polystyrene should register a steady recovery, although this is largely dependent on the coronavirus situation. Market sentiment may remain weak given the great uncertainties, but sources expect a demand revival in China, a main PS consumer, to lift the market as many PS producers in Asia are China-centric.

Meanwhile, the market is closely monitoring the conditions in Europe and the US as they are the main consumers of PS end products, hoping the reopening of some economies will boost demand from the bottom up.

Construction demand key for Europe In Europe, construction demand will remain in focus for much of the second half of the year.

Expanded polystyrene is a major insulation material for many countries in Europe, and is in particular use within Germany and France for homes. Construction activity across the continent has shrunk, with many countries reporting expected economic contraction in the sector due to COVID-19.

No clear signposting has been discussed by European governments for an end to the lockdowns, with social distancing measures expected to remain in place until the third quarter at the earliest. This will continue to impact workforces, as even though essential construction works have continued, proximity restrictions will continue to cut activity drastically.

Steady demand will continue to be seen from food packaging and medical applications drawing on polystyrene grades, and producers will continue to push to maintain or widen margins on these products due to demand destruction for other styrenics markets.

Pricing volatility is likely to remain a key concern in Europe during the second half of the year, as changing restrictions on lockdown measures are likely to differ between countries.

Both styrene and benzene markets have high stock levels in Europe, and without a significant improvement in demand from the downstream, both markets will look to export for support. Further quick swings in pricing may result from length clearing, but without a sympathetic increase in downstream demand from domestic Europe, this will place pressure on polystyrene producers.

Weak US H2 demand During the second half of the year, both benzene and styrene are poised to rebound slowly and this should provide a boost to US polystyrene pricing. US polystyrene prices saw significant declines during the first half of the year, with prices pressured by sharp decline in the US benzene contract. The US benzene contract fell 161 cents/gal between March and May, dragging polystyrene prices lower.

Sources noted that US styrene producers were running at reduced rates, and expectations were that run rates were close to 70% industry-wide to end the year. This was expected to result in an uptick in pricing and ultimately could keep margins soft.

Demand growth, which was poor prior to COVID-19, is likely to be muted for the remainder of the year, with strength seen in food packaging and medical applications. However, demand from larger segments, such as appliances, automotive and construction, are not expected to show significant improvement in 2020 as high unemployment rates and uncertainty surrounding economic growth curtail buying interest for durable goods. This will negatively impact initial expectations that put annualized polystyrene growth at between 1.8%-2%, said sources.

— Sophia Yao Simon Price Kevin Allen

Latin America sees coronavirus fallout on polymers lasting through 2020

Latin American economies took the same punches the coronavirus pandemic hurled at the rest of the world, and the region expects to feel that fallout through the rest of 2020 with lower output and wary spending.

“Coronavirus pandemic took everyone by surprise,” said Luiz Francisco Cunha, director at Schutz Vasitex and head of Brazil’s Blown Industrial Packaging Manufacturers Chamber (COFEIS).

The pandemic prompted governments to adopt quarantine measures and restrict nonessential services. Shopping malls, car dealerships, and movie theaters were closed in most Latin American capitals, and countries were expected to continue at least minimum quarantines into the second half of 2020.

The restrictions slammed polymer demand for automotive and construction sectors, known for heavy usage of polypropylene and polyvinyl chloride. At the same time, PP demand for N-95 masks, gowns and other medical products used to combat the pandemic was not enough to offset impact on the auto sector. All auto makers in Brazil and Argentina shut down operations in the second quarter 2020, sharply siphoning regional PP consumption, while resuming slightly some plants in June or the third quarter.

As for polyethylene grades, demand veered to food packaging, bottles for cleaning products or hand sanitizers, and flexible general packaging or plastic bags. Even so, some distributors reportedly halted buying. “We are not having enough consumption to justify new purchases,” a Brazilian distributor said.

In Argentina, Ecuador and Colombia, lockdowns were more intense than in Peru, Chile and the Mercosur region. For the coming months, however, activity is expected to come online in all countries.

“Industries are working with much reduced rates, but at least resuming some operations,” a regional distributor said, adding that by June or July, expectations are for higher consumption in general.

Polymer prices hit historic lows Lower demand pushed imported polymer prices to historic lows in America during the first half of the year. Global prices regained upwards momentum in June and this was reflected in Latin America, but prices continue to face headwinds. Compared to January levels, most polymers fell about $100/mt or more in Brazil and in the West Coast of South America. Latin American PE import markets are highly influenced by the US, while PP markets see more impact from the Middle East and Asia.

Brazil’s domestic market was more resilient, as the country’s naphtha-based producer Braskem benefited from low feedstock prices amid the global oil price crash. Braskem increased naphtha consumption from the state-owned oil company Petrobras in Q1 and again in April.

Domestic prices also reached historical lows in Argentina, Colombia and Mexico, but recovered during June.

Sources were divided on price movement in the near future, given pandemic-driven volatility. Some believe prices hit bottom in the second quarter, while others say values could reach new lows in the coming months, depending on activity and consumption resumption levels.

In Brazil, plastics-related companies were said to rely on short-term expectations, with longer term forecasts unavailable. According to plastics association Abiplast, more than 50% of the companies have frozen investments completely. Abiplast also expects a 5% decline in 2020 plastics manufacturing output.

GDP declines looming In general, expectations for the Brazilian economy have become gloomier so far in 2020. A weekly report published by Brazil’s Central Bank initially projected 2.34% GDP growth, but had evolved to a contraction of more than 4% by the second quarter. The International Monetary Fund (IMF) expects Brazil’s GDP to decline by up to 5.3% in 2020.

Argentina, the second largest South American economy, expects to see its GDP decline by 6.5%, the largest drop since 2002, according to its Ministry of Economy. IMF projects a smaller decline of 5.7%, however. Mexico’s economy, according to IMF, is expected to fall 6.6%.

For the recovery, plastic players expect a U-curve rather than a V-curve because of those anticipated GDP declines.

Additional stress stemmed from the devaluation of Latin American countries’ currencies towards the dollar. In Brazil, the exchange rate entered 2020 with a high value, at Real4.01/$1, but it hit new levels in the first half of the year, surpassing Real5.90/$1 toward Real6.0/$1, the most depreciated currency in the region. The Real appreciated during June, but it’s still ahead the Real5/$1 mark.

Another issue for converters was limited availability of credit lines in the region, where financing became 40% to 50% more expensive.

“Nothing is certain because we do not know what can be determined by public authorities, since there is a possibility of lockdown, and a drastic closure in this way would prevent trade and business from evolving,” said Edson Begnami, sales director at Plasutil and head of the Brazil’s Houseware Manufacturers Chamber (COFAUD).

— Guilherme Baida , Flavia Alemi

Tough times ahead as recycled plastics struggle with sustainability shifts

US, Europe coronavirus supply impact to be felt through H2 2020

Planned Asia recycling plants delayed amid economic uncertainty

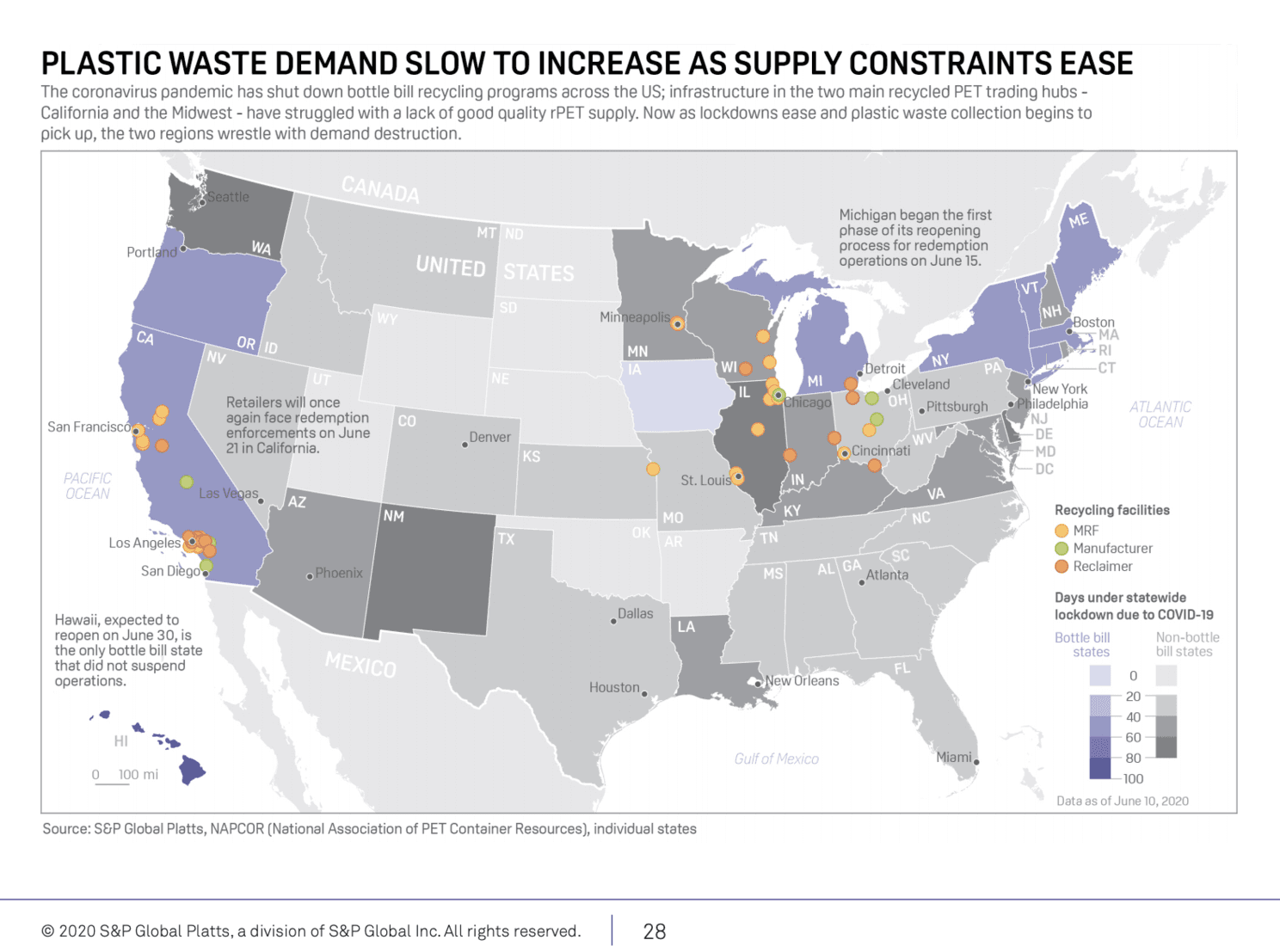

The repercussions of the coronavirus pandemic look set to test recycled plastics markets across the globe in the second half of the year, with tight supply and poor economics the key hurdles for both sellers and buyers.

Sustainability commitments tested as US R-PET economics pose challenges Prior to the coronavirus outbreak, the US recycled plastics industry had already been plagued by extremely cheap virgin PET, high fixed-processing costs and export restrictions, leading to calls for systemic and policy reform initiatives across the supply chain. In 2019, Congress saw an historic influx of recycling-related legislation. However, in the first half of the year, most sustainability legislation took a back seat as the US focused on containing the coronavirus.

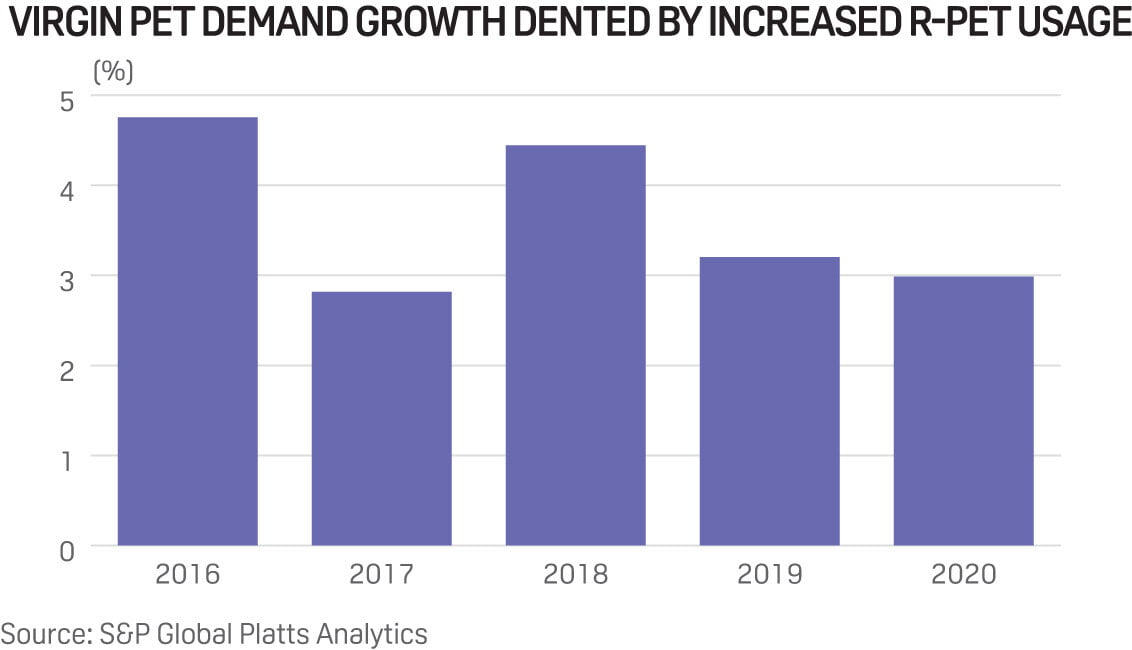

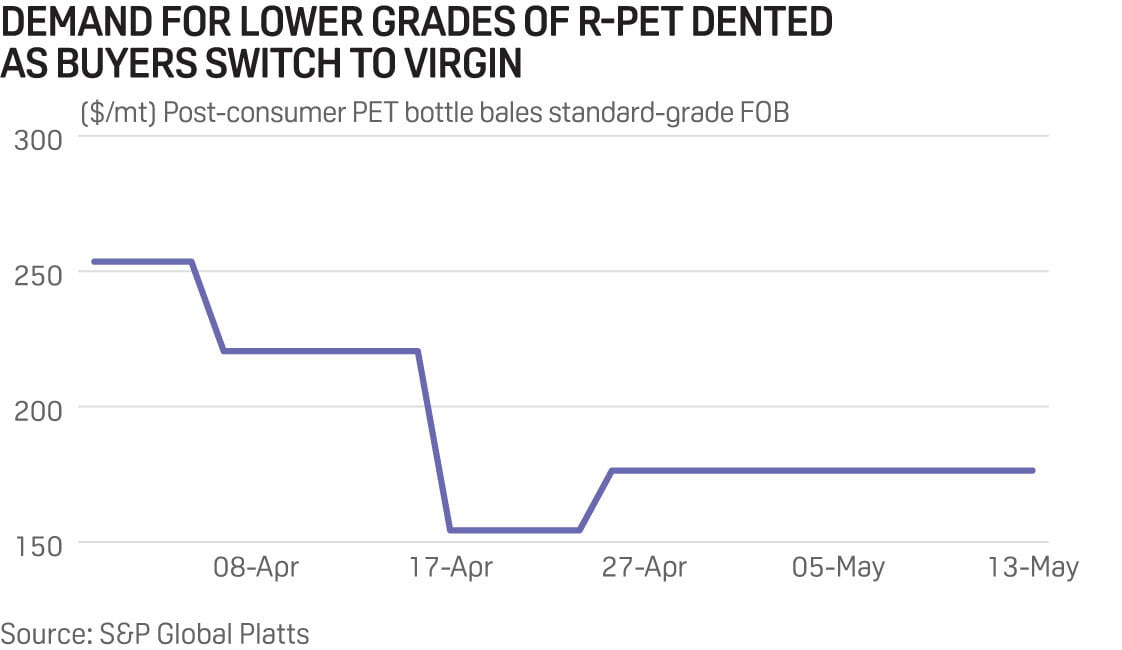

Without government mandates, R-PET demand is expected to remain weak as cost-sensitive bottle manufacturers increasingly reject recycled material for low-cost virgin resin, which saw historic lows in April.

Supply of post-consumer bottle bales has been severely limited during the pandemic due to labor shortages, collection cuts and bottle bill suspensions, prompting PET bale prices to surge and recycled flake/pellet output to decline.

Therefore, given low-cost virgin PET prices and R-PET supply constraints, many end users in the flake to packaging sector struck 6-12 month contractual agreements with resin producers to secure reliable PET supply.

The recycled PET fiber market will likely bear more of the brunt of the imbalance between virgin and recycled PET. Demand will remain weak in the near term as the textile, carpeting and automotive industries continue to face global manufacturing slowdowns and are forced to curtail operations amid financial constraints. Even if supply volumes and demand levels begin to normalize in H2 2020, some market participants fear the full PET reclamation chain will be unable to survive. Overall, market sources expect R-PET buying and selling to shift away from contracts towards the spot market this year as the future relationship between virgin and recycled PET remains uncertain.

European sustainability commitments endure downturn; supply still key concern The European virgin and recycled PET markets have been decoupling since mid-2019, but H2 2020 will bring fresh concerns for participants looking to secure supply.

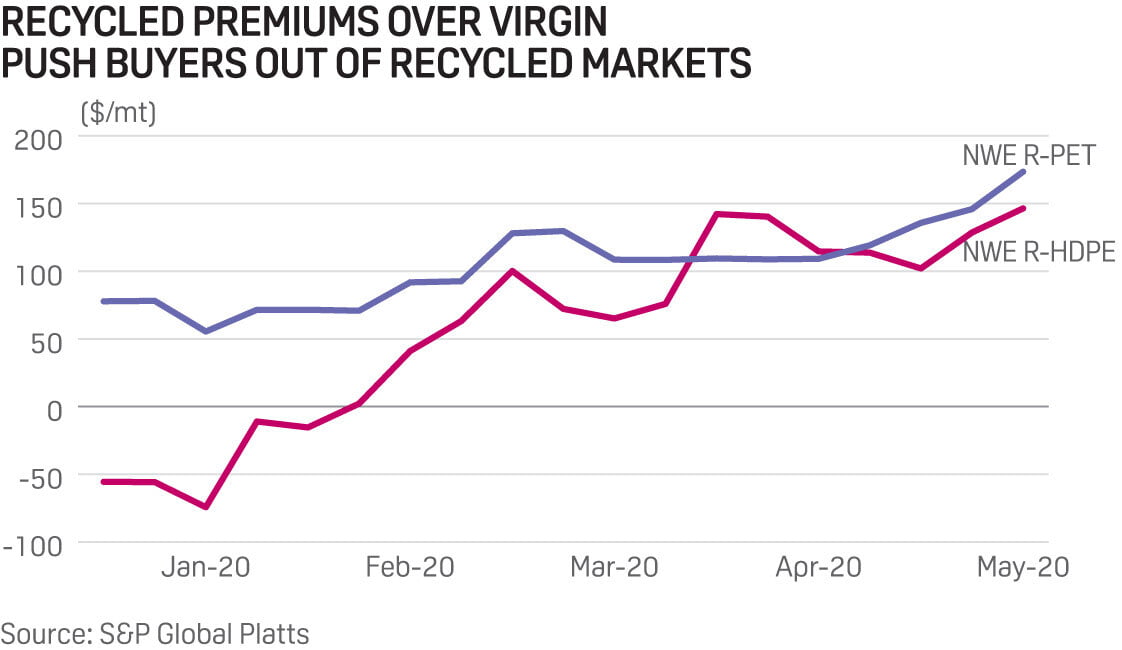

Recycled HDPE and PET premiums over virgin equivalents have increased during the coronavirus pandemic, partly due to more stable demand than virgin but also to high-cost bales and squeezed margins for recyclers. This primarily caused fragmentation in the recycled markets, with demand for higher grade material robust and lower-grade suffering the full effects of the economic slowdown.

As in the US, more economically sensitive buyers — such as those purchasing construction and automotive grades of R-HDPE or tray and sheet participants in the R-PET market — switched further volumes to the virgin market. By mid-May pricing was lower than during the 2008-09 global financial crisis.

At the top end of the market, however, dwindling supply is being consolidated by a small proportion of larger buyers, who remain committed to publicly announced sustainability initiatives.

Across the board, supply was, and will remain, hampered by the coronavirus. Cancellation of large sporting events and mass gatherings over the summer will dampen demand, with far less post-consumer material entering the recycling supply chain moving into the third quarter.

Recyclers may remain reluctant to purchase post-consumer material if margins do not recover.

With pressure from the low-priced virgin market on recycled PET flakes, margins are under pressure; this will lead to lower volumes and even the halting of production of lower grades of R-PET and R-HDPE.

Instead, recyclers will try to offset lower volumes by producing higher quality grades such as R-PET food-grade pellets and R-HDPE natural pellets, where ready buyers remain.

Asian recycling business growth slows Asian recycling businesses are expected to continue expanding, though at a slower rate due to the coronavirus.

Major projects to increase recycling capacity remain in the pipeline, expected to be brought online in the coming six to 18 months, including but not limited to new capacity of 50,000 mt/year of R-PET and R-HDPE from PTT Global Chemical and Alpha Packaging in Thailand, 25,000 mt/year of R-PET from Veolia Services Indonesia, 16,000 mt/year of R-PET from PETValue in the Philippines and 30,000 mt/year of R-PE film from Suez in Thailand.

Nevertheless, the current economy is particularly challenging for small and medium-sized enterprises. Countries lacking infrastructure for both waste collection and reprocessing will see scant government support, with other sectors of their economies the more immediate priority, observers said. Some recyclers are likely to remain closed even after lockdowns due to scant waste and sorting collection supply, and concerns of virus exposure from handling materials, sources said.

The pandemic has also delayed the transition to higher-end applications by at least six to 18 months, a source said.

— Benjamin Brooks, Sarah Schneider, Miranda Zhang

Listen to the webinar

Click here