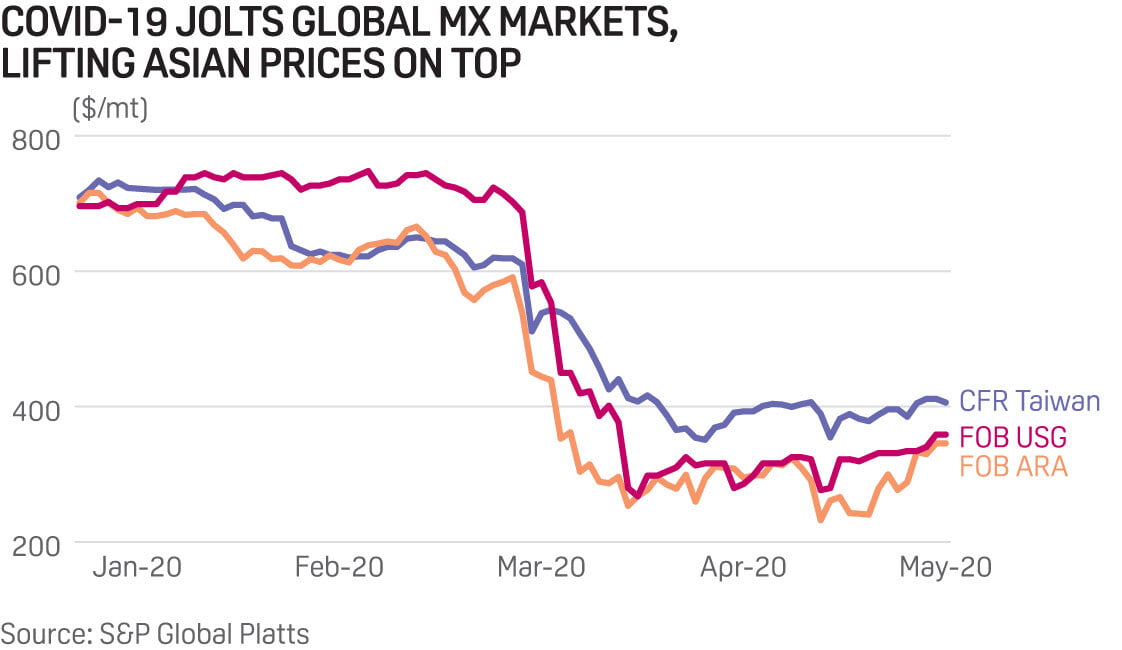

China domestic benzene values to be buffeted by global trader moves in H2

Established trade flows shift

China oversupply to continue without US demand recovery

Prices in the Chinese domestic benzene market are likely to be driven by short-term and opportunistic global plays during the second half of 2020, as the COVID-19 pandemic evolves and countries around the world gradually re-open their economies, according to market sources.

The revival of the global economy is very important for the widely used petrochemical, which relies heavily on inter-regional trading, with North Asian and European supply relying heavily on demand from China and the US Gulf Coast.

As different regions recover at different rates, traders are likely to buy and sell in a more opportunistic fashion, with previously established trade flows no longer viable.

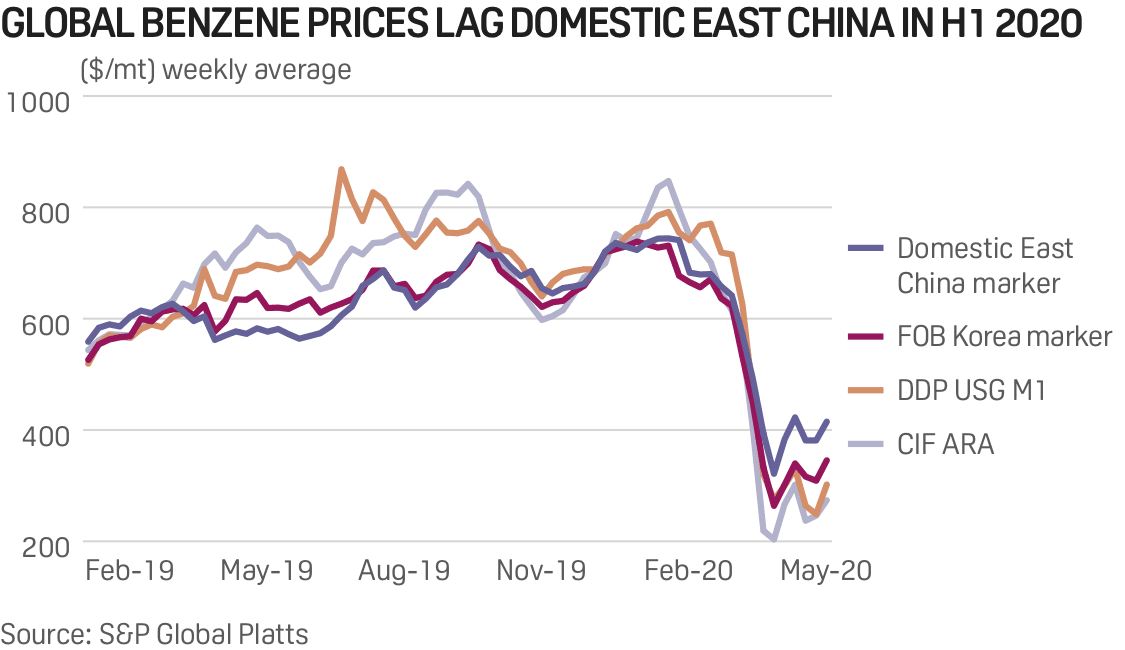

China's intercity borders re-opened in the first week of April, after which prices of domestically traded benzene soared in anticipation of a demand recovery, as traders sought to deliver benzene into the country’s limited commercial tanks.

European cargoes and displaced Asian supply, which would otherwise have been US-bound, began to flood the CFR China market, resulting in an open arbitrage between CFR China and domestic East China prices. The difficult storage situation was further exacerbated since available East China storage space is concentrated in the hands of just a few players, as trading houses tighten counterparty credit requirements in a volatile landscape.

Market sentiment is split over whether the domestic-import arbitrage is sustainable going into H2 2020. While an increase in operating rates and an improvement in downstream margins looks promising, an inability to export end-products could eventually result in a price plateau once domestic demand is satisfied.

If US demand does not recover, supply will continue to flood the CFR China market, keeping CFR China prices depressed compared to domestic cargoes.

Excess European supply With the prompt end of the benzene market in Europe straining under heavy supply during April and May, exports will play a key role in rebalancing benzene stocks against demand.

Uncertainty around easing lockdowns across Europe has left demand recovery in question. Benzene demand has been hit by sluggish automotive and construction sectors in the wake of the pandemic which has in turn led to heavily reduced demand for downstream styrenics. Estimates of styrene production run rates had been heard as low as 60% during May, sources said.

At the beginning of May, European benzene prices were lower than US and Asian values, creating the potential for the arbitrage of European product to other areas and prompting Middle Eastern exporters to turn away from Europe due to the low prices.

Flow toward Europe had been limited to contractual volumes only, he added. Demand would need to recover first to attract more material, and for the moment spot cargoes would be focused on the improving Chinese market.

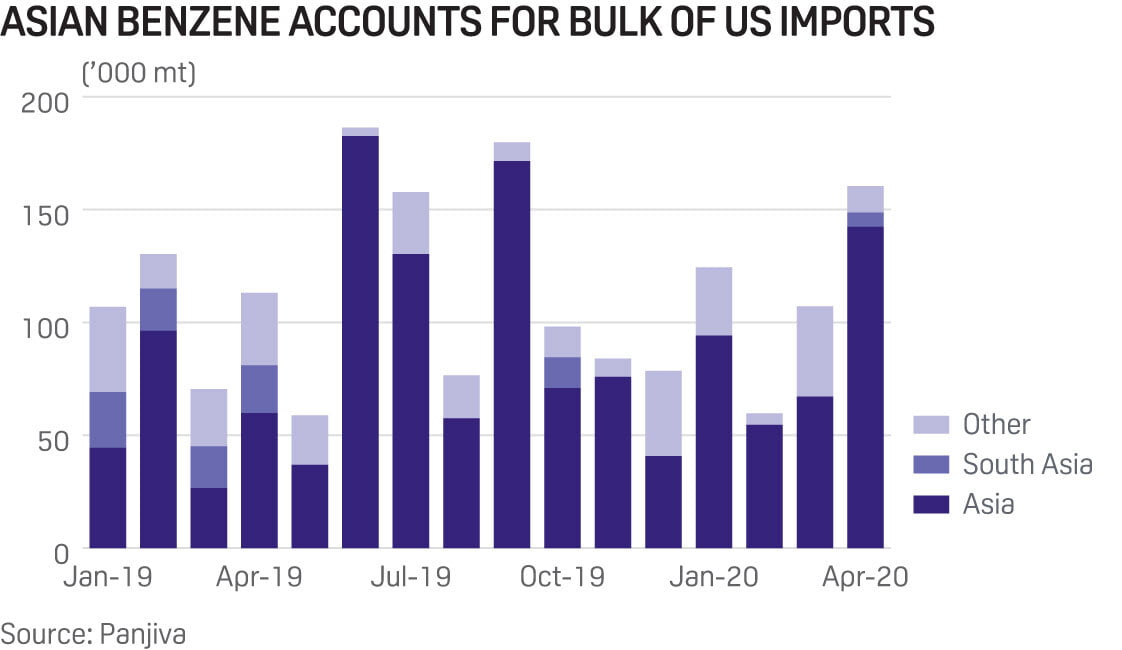

US demand Benzene imports were expected to pick up this year, with one producer pegging US import demand at 150,000 mt/month. Imports surpassed that number in April, when nearly 200,000 mt of benzene landed in the US — the delayed impact from China’s initial coronavirus shutdown in early February, which led South Korean and Japanese producers to divert cargoes westward.

Whether imports continue at such a rate in H2 is unlikely if the FOB Korea benchmark remains priced above DDP USG benzene, as was the case in spring. Imports are expected to decline in July and August because major exporting regions diverted cargoes elsewhere with US benzene the cheapest globally.

In July alone, demand for benzene in the US is expected to rise about 40,000 mt to 750,000 mt, according to S&P Global Platts Analytics. The operating rates of styrene producers should determine whether that trend holds. Participants expect demand for styrene to be healthier in H2 as automakers and construction work resumes.

Upstream volatility Supply length in Asia will be a key factor determining the fate of the FOB Korea benchmark, with producers potentially adjusting rates in reaction to key aromatics spreads, including benzene-naphtha and paraxylene-naphtha. While key exporting countries in North Asia have successfully completed annual maintenance in H1, several turnarounds in Southeast Asia earlier scheduled in H1 2020 have been postponed to H2 amid lockdowns.

Furthermore, new capacity slated to start up in H2 in Asia includes Saudi Aramco’s Jazan refinery and Sinochem’s Quanzhou unit among others, totaling just over 1 million mt/year of capacity.

Over in the US supply of benzene in H2 2020 will depend on a number of factors, including gasoline demand, the economics of STDP and TDP units, cracker operating rates and feedstock pricing. Lower spot prices of one benzene feedstock could create an opposite effect on others, leading to a complicated balance of supply.

— Tess Tseng, Simon Price, Emily Burleson

Styrene outlook for US, Europe in H2 hinges on China

Demand recovers in China as COVID-19 restrictions ease

But demand in Europe, US expected to remain weak in H2

China's increasing demand for styrene as COVID-19 restrictions ease at a time when fundamentals remain weak in Europe and the US is likely to continue driving cargoes east in the second half of the year, but challenges loom as a slate of new domestic capacity is due to come online in China in H2.

Demand in Europe and the US is expected to remain weak in H2 as downturns in the automobile and construction sectors have been only partially offset by enhanced demand from single-use plastics, and styrene producers in both markets are now actively looking to China for buyers.

However, while the revival in demand from Chinese importers supplying domestic downstream industries is likely to boost liquidity amid an open arbitrage between CFR China and domestic cargoes, it is clear the Asian styrene market is already grappling with high inventory and ample supply.

In addition, new Chinese integrated producers that started operating in the first quarter should stabilize production by H2 and even run at full capacity, adding further length to the styrene market.

Despite the delay in the startup of CNOOC-Shell’s 700,000 mt/year styrene plant in Huizhou to the first half of 2021 from the fourth quarter of 2020, oversupply remains a key concern in Asia, with Tangshan Xuyang Chemical’s 500,000 mt/year unit, Baolai Chemical’s 350,000 mt/year unit and Anhui Jiaxi’s 350,000 mt/year unit all starting up in China in H2.

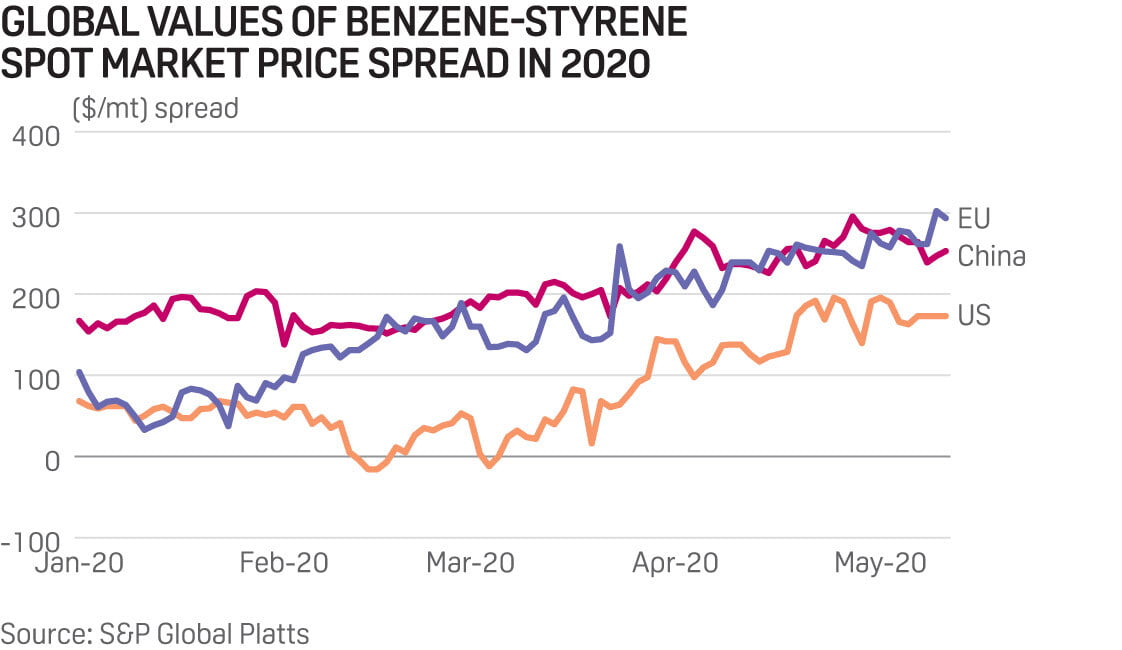

The heavy Asian plant maintenance season in early 2020 has also largely ended, which will add additional length. Arbitrage windows from Europe and the US to Asia re-opened in the second quarter due to the collapse of FOB USG and FOB ARA prices, even after the concurrent rise in freight rates was factored in. “As long as CFR China prices are lower than import parity prices, China’s styrene intake won’t decrease a lot, even as domestic supplies are increasing,” a trader said.

The open arbitrage is set to fuel a flurry of deepsea cargo arrivals in east China in June and July and result in a further inventory buildup in shore tanks. East China inventory levels hit a record high of 324,000 mt in the second week of March and remained above 270,000 mt in May as the global COVID-19 pandemic slashed demand. Market participants expect inventory levels to remain high for some time, keeping CFR China prices under sustained pressure.

US margins widen In the US, the gradual easing of COVID-19 lockdown restrictions should support domestic styrene demand and lead to a recovery in pricing in H2, market sources said. US styrene monomer prices plunged below even the weakest expectations of many market participants in Q1 to record multiple new lows before bottoming at $375/mt FOB USG on March 23.

Styrene production at US plants was estimated at around 75% of nameplate capacity in early May and was expected to increase in line with the recovery in global demand.

Volatile benzene and styrene prices created wide swings in US styrene production margins in Q2. Weak margins that hovered in the low $60s/mt in December turned negative in mid-February for plants utilizing spot benzene, according to S&P Global Platts data. By April however, Asian demand had lifted spot styrene prices and divorced them somewhat from benzene values, widening the margin to $195/mt. The spread stood at $201/mt on May 22, Platts data showed.

US demand for styrene derivatives is also expected to pick up in H2, market participants said. While polystyrene demand has risen in H1 on the increased use of styrofoam take-away food containers, demand for expanded polystyrene fell as construction projects slowed, and for acrylonitrile-butadiene-styrene tumbled as automakers halted assembly lines, due to COVID-19 lockdowns.

If the domestic car manufacturing and construction sectors were to recover in H2, styrene demand should follow, market participants said. However, the 1.2 million mt Chinese styrene production capacity that is expected to come online in 2020 may still have the knock-on effect of causing a styrene supply glut in the US, sources said.

Pressure in Europe The primary driver of European styrene prices in H2 will be the rate at which COVID-19 lockdown measures are eased, after prices hit historic lows in March at the peak of the demand destruction. Lower prices propelled a return to positive margins for styrene over feedstock benzene to just below the $250/mt mark, which the market considers a healthy spread.

However the slowdown of the automotive and construction sectors has had an immense impact on demand, with styrene butadiene rubber used in tire manufacturing and expanded polystyrene for home insulation, especially Germany and France.

Although several European governments are tentatively easing social distancing measures as summer approaches, some measures are expected to continue into Q3 and even Q4, maintaining pressure on demand. The market will continue to operate on a hand-to-mouth basis until the coronavirus pandemic passes, a European trader said.

Styrene consumers shifted to more spot buying and reduced reliance on contractual volumes in 2019, reducing demand and leaving the European market in an overly long position, and struggling to find outlets for its surplus, even before COVID-19 emerged. Without an arbitrage to Asia, European supply promises to remain long throughout 2020, market sources said.

— Sophia Yao, Simon Price, Emily Burleson

Toluene road to recovery far from clear in H2 2020

Operating rates to remain low amid ongoing coronavirus

Summer driving season could support toluene blending values

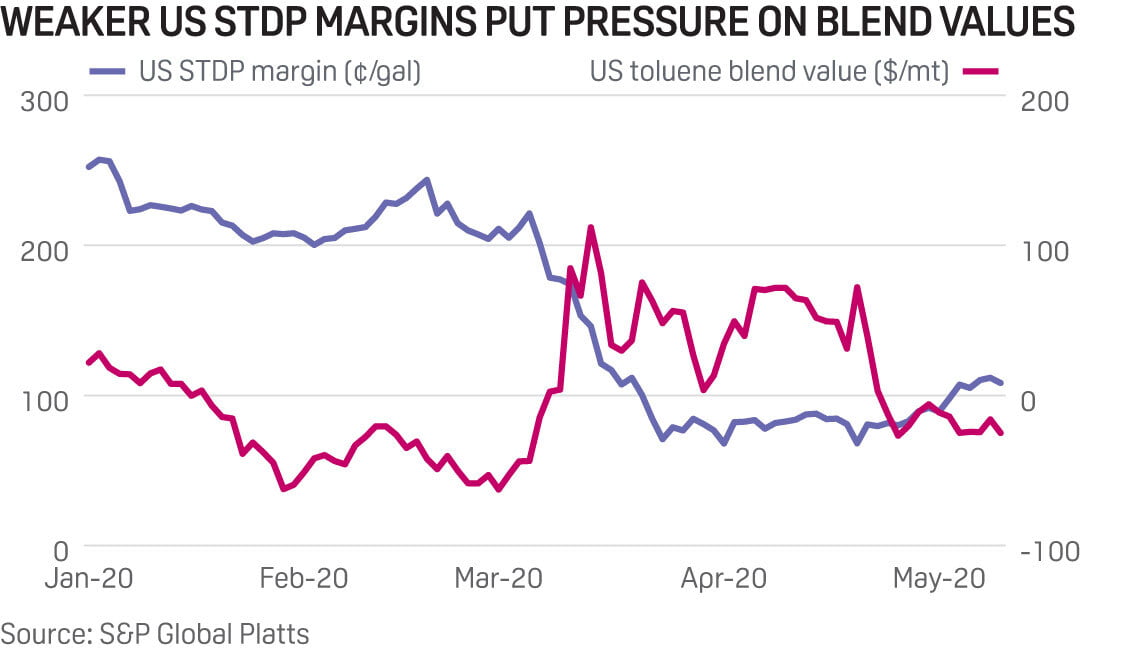

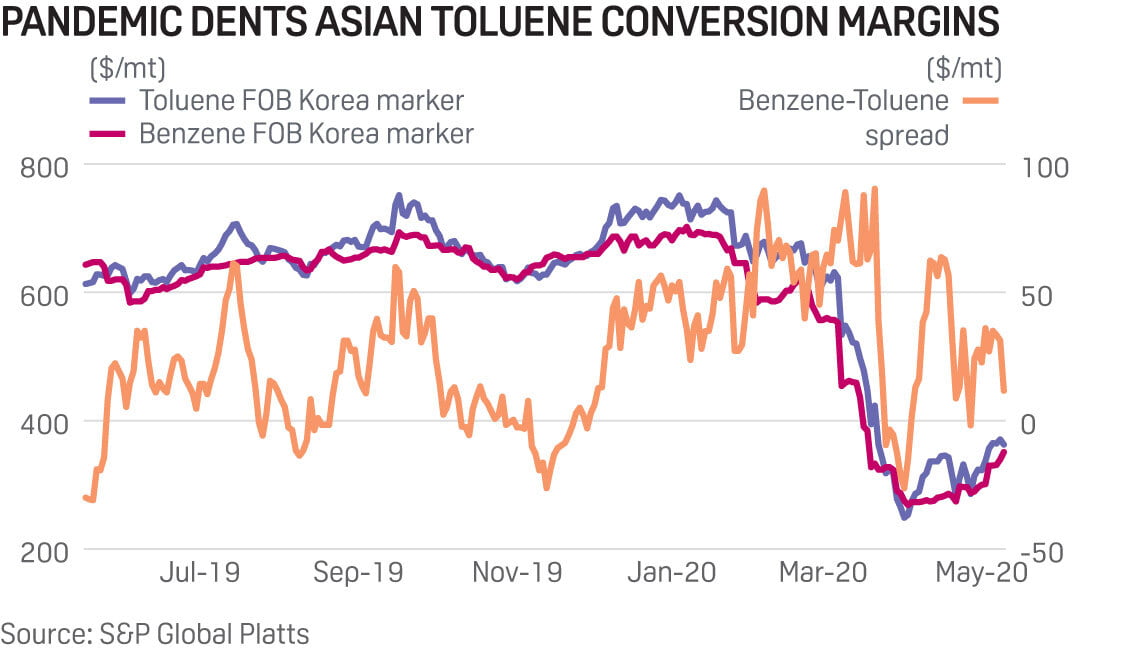

Global toluene supply and demand balances are expected to remain under pressure during the latter half of 2020 due to lower operating rates and reduced demand amid the ongoing coronavirus pandemic.

Weaker pricing in benzene and derivative styrene markets, as well as soft paraxylene prices, dented chemical demand for toluene during much of the first half of the year. However, while weaker aromatics pricing is expected to persist in the second half, demand for higher-octane toluene in summer and lower product availability due to refinery run cuts may give some upside to the market.

Blending economics to drive balances In the US market, Selective Toluene Disproportionation unit margins, have been in negative territory more often than not over the past 12 months. With little demand from toluene conversion units, octane demand will drive pricing despite weaker blend values to finish the first half of the year.

According to sources, demand from the blending segment will be contingent upon the length of time required to burn through higher gasoline inventories and an overall economic recovery. Sources in the US have forecast steady improvement throughout the second half of the year.

With COVID-19 having spread to the US, however, market participants in Asia have mostly written off the summer-driving season and are said to be scouring for other demand centers, notably China.

Gasoline blending activities within Asia, ex-China, are still thinly slated as government lockdowns enforced to curb the spread of COVID-19 has placed barricades to road fuel needs. Previously, market participants ballparked the US summer driving season, which typically starts in May, to be the driving factor that would spur interest in gasoline blending.

Operating rate drops present opportunityIn Europe, expectations surrounding the post-lockdown market response are more optimistic, with some participants hoping to see "an ideal market situation" as renewed demand meets limited production capacity availability.

"Most likely when we all come out of lockdown, the demand will come into the market with the limited production capacity availability," said a trader on May 1, adding:

Some European refineries that were unable to postpone necessary shutdowns until later this year are in the middle of the turnarounds, and will not be able to react to booming post-lockdown demand, said market sources.

US toluene prices will also see some support from lower refinery run rates, sources have said. Refinery utilization rates have fallen and reformer rates have been impacted accordingly. Extrapolating lower refinery utilization rates down to the reformer and assuming a total toluene capacity of roughly 4.8 million mt from reformate, a 10% reduction in run rates equates to roughly 40,000 mt/month.

This, coupled with expected strong reformate pricing, is expected to bolster toluene prices during the latter half of the year. Sources noted that this could stifle chemical demand if gains in benzene and paraxylene pricing fail to outpace toluene.

Renewed demand or temporary spike? Although the European aromatics market witnessed a rally in prices on the back of stronger crude oil prices in May, consensus among market sources remains mixed on how long-lived any additional spike in prices will be.

Adding that there is some expectation of increased demand in H2 2020 from consumers after the prolonged stay-at-home period.

Signs of renewed strength have been visible in China, with the market soaking up surplus barrels within and beyond Asia. However, despite the recent strength, questions remain on how sustainable the uptick in China’s demand could be while the rest of Asia and the world at large continue to grapple with COVID-19.

Meanwhile in India, the other strong foothold for Asian demand, the government has rolled out zoning plans to bring businesses in COVID-19 free areas back to life.

Some importers have already secured toluene cargoes to be brought into the country for early July in expectation that India's demand could progressively recover as the economy reopens.

With the two major Asian import hubs broadly offsetting each other in demand, the global market faces mixed fundamentals for the third and fourth quarters. Add to it the possibility of a global economic recession ahead, and the road to recovery seems far from clear.

— Kevin Allen, Alexander Borulev, Sue Koh

Mixed xylenes fate tied to gasoline demand recovery in H2

Paraxylene in abundant supply amid new global capacity additions

Asia gasoline demand contingent on low crude oil, lifting of lockdowns

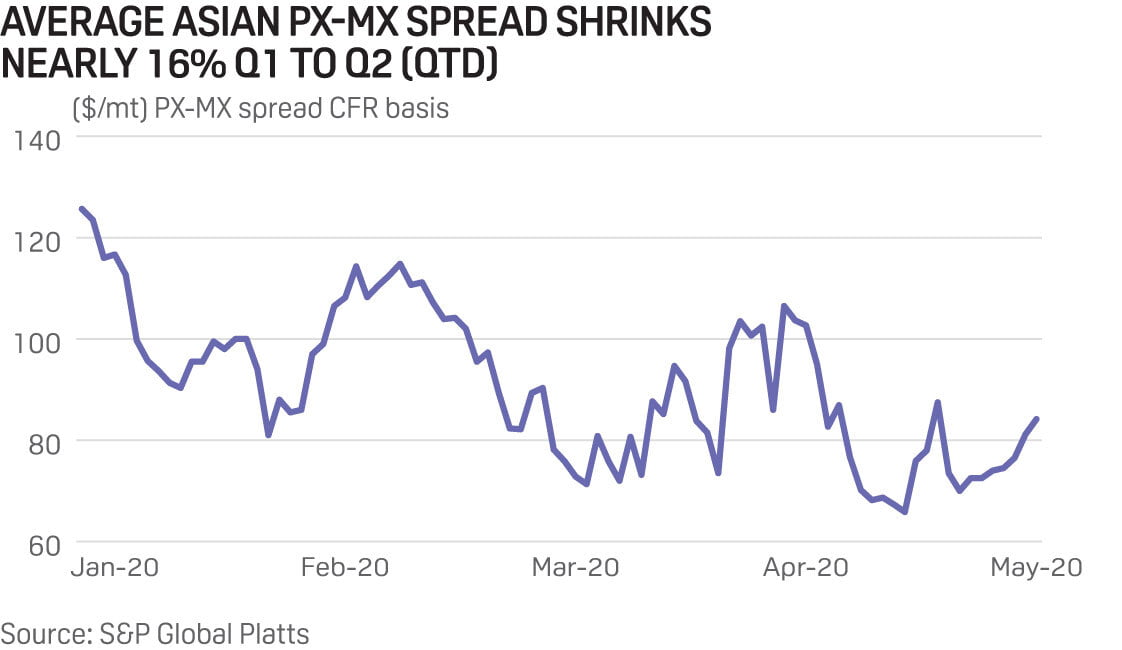

Global mixed xylene prices are expected to see continued pressure in the second half of 2020 amid expected weakness in the downstream paraxylene segment.

The xylenes chain has struggled amid protracted supply length in the US and Asia, and this has been further exacerbated by demand loss caused by the coronavirus pandemic.

Support for the mixed xylenes segment in H2 2020 is expected to come from supply constraints associated with lower refinery utilization rates and as countries move away from lockdown measures leading to increased aromatics demand as gasoline blending component.

PX glut threatens MX demand In China, new PX capacity of at least 1.8 million mt/year is expected to start up this year. These new units, Sinochem Quanzhou and shandong Dongying, are likely to consume their MX captively going forward, instead of selling it in the domestic market. However, additional PX capacity may exacerbate the glut in the PX market and further deteriorate production margins.

It remains to be seen if new purified terephthalic acid plants slated to start up in the second half of the year in China can lend some support to paraxylene prices and margins.

A 1.8 million mt/year reforming unit at Sinopec’s Zhongke refinery in Guangdong, is expected to start up in the third quarter, adding around 400,000-500,000 mt/year of new MX capacity in China.

In the US, demand from paraxylene is also expected to remain subdued for much of the year on the back of global length, as well as on imports. However in Europe, lower output rates in refineries has instead kept the mixed xylene market balanced to tight despite the coronavirus-led reduction in demand.

Overall, the factors that drive the xylenes market will likely be tied heavily to the recovery of the global economy. Demand from the downstream PET segment, but also gasoline octane demand, will be heavily influenced by the economic security and spending habits of individuals.

While reduced production rates have provided some support to European mixed xylenes prices after initial gasoline-led losses, market sources see the demand side as key to any potential uplift in the balance of the year.

Sources expect an upturn in Europe only if strong demand drivers emerge. With blending values being viewed as a price floor, these demand drivers should come from the chemical sector.

Increased aromatics into gasoline blending after lifting of lockdowns The fate of European mixed xylenes will also be reliant on the transition of countries away from lockdown measures and subsequent pick up in gasoline blending activity. Weak conversion margins since the start of the year, has already shifted the dependence of the MX market to the gasoline blending segment, with market participants now looking to inventories in the region for sign of additional demand.

With the growing levels of gasoline inventories in the Amsterdam-Rotterdam-Antwerp hub in May, it will likely take time to deplete the exciting gasoline before the demand for blending components will kick in at the full extent.

Mixed xylenes traders in the US will also be looking to gasoline for pricing support. Refiners began to cut rates in Q1 as gasoline inventories swollen to near record-levels and rates fell to as low as 67.7% in mid-April.

Those rate reductions helped to lend support to mixed xylenes prices and that trend is expected to continue into the second half of the year. While such a move would bolster pricing, it could also keep the PX-MX spread low and result in poor economics for paraxylene producers running crystallization units.

Another drawback to potential higher pricing due to refinery cuts is a negative impact on arbitrage economics. Though mixed xylenes exports out of the US are not as significant as some other petrochemicals, their importance increases once demand becomes confined sole to the gasoline blending segment.

Finally, low crude oil prices may support China's appetite for isomer-MX imports into gasoline blending, similar to the trend seen in the first half of the year when China saw strong demand for MX imports, market sources said in early May.

"If this low crude oil price continues until end of this year, MX demand from China will keep strong as gasoline blending value will be high," a Northeast Asian end-user predicted. "But if crude price returns to over $40-$50/b, the supply of MX will be more than demand and MX will be weak."

— Gustav Inge Holmvik, Alexander Borulev, Kevin Allen

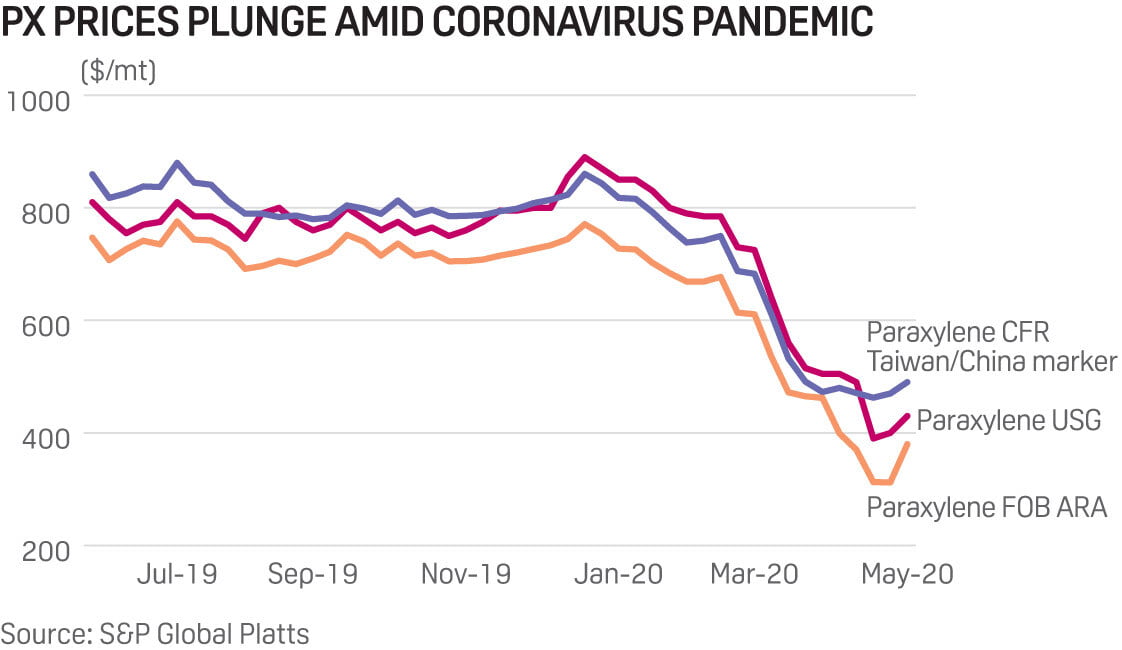

Global paraxylene looks to China for direction in H2

New Asian capacities expected in H2

Uncertain demand in the wake of the pandemic

The second half of 2020 holds many questions for the global paraxylene market as participants juggle with uncertain demand in the wake of the coronavirus pandemic, high levels of inventories and oversupply from new Asian capacities.

The world is looking to China, the world's biggest paraxylene buyer, to chart the course for the next half of 2020.

New normal in Asian prices Asian paraxylene players are uncertain of what the second half of 2020 will hold, but hope for a rebound in buying appetites after prices slumped to fresh lows in April. The COVID-19 pandemic had caused the CFR Taiwan/China paraxylene marker to collapse to a record low $432.50/mt on April 22, plunging 48% since the start of the year.

But the situation is fast evolving with negative changes in the paraxylene-naphtha spread causing Asian producers to question their operating rates. On May 27, the paraxylene-naphtha spread narrowed to a new low of $173.795/mt, not seen for at least 10 years, market sources said.

Its recovery is no longer solely [dependent] on the polyester chain following the demand disruption," an Asian PX source said.

With margins at unprecedented lows, the risk of run cuts or even the shutdown of PX plants loom on the horizon. This could mean that the stage is set for a gradual recovery in H2.

The heightened volatility in energy markets drove paraxylene players to hedge their risk exposures, with the volume of paraxylene derivatives traded on the Singapore Exchange over January-April, surging 62% on the year to over 2 million mt, the SGX data showed. The paraxylene derivatives market is likely to remain robust in H2, should volatility in both the oil and petrochemical markets persist.

Inventories may return to normal after a while, especially with purified terephthalic acid units operating at relatively stable rates amid decent production margins, market sources said. The pace of demand recovery matters as downstream consumers' buying patterns may change following the COVID-19 pandemic, a Southeast Asian source, who has a bearish market outlook till Q3, said.

However, additional paraxylene capacity slated to start in H2 will increase supply and possibly worsen the already fragile supply-demand dynamics. New capacity slated to come online include Shandong Dongying Petrochemical's 1 million mt/year plant, Sinochem Quanzhou's 800,000 mt/year unit and Aramco Jazan's 850,000 mt/year plant, whose start had been delayed since early 2020.

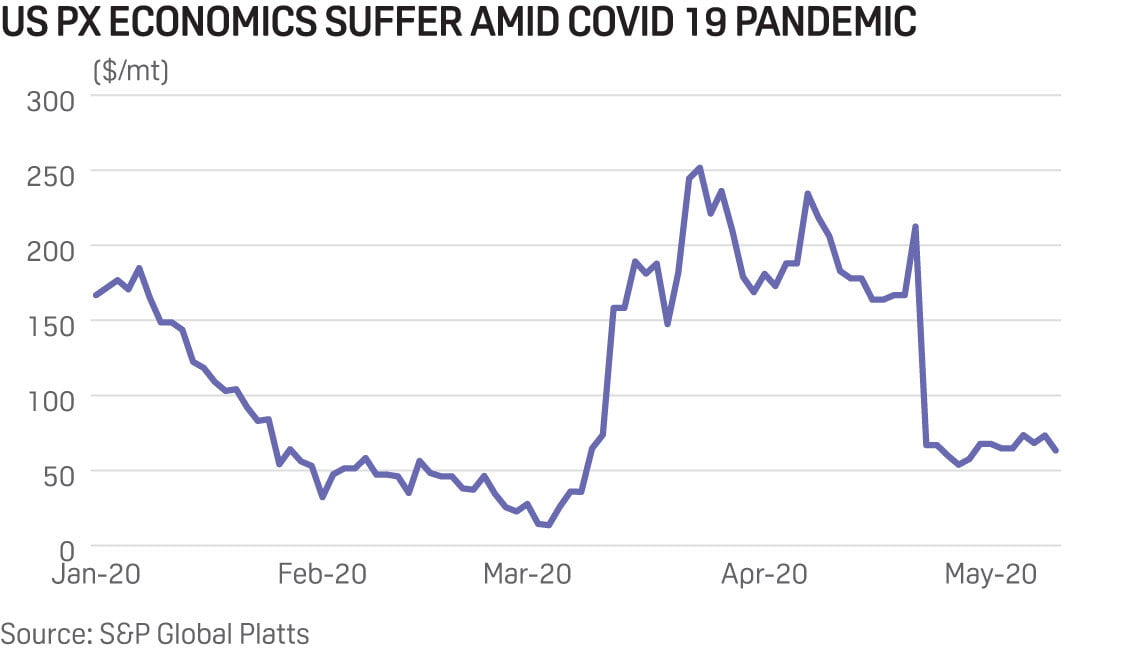

Asian market pressures impact US US paraxylene production has been hit by weak demand and high domestic prices. Weaker gasoline demand in the US has led to lower refinery run rates, which could lower reformer run rates and increase feedstock prices. This would support domestic US paraxylene prices, a trend which could persist into the second half of 2020.

Due to higher domestic US PX prices, there has been an increase in imports, which could also hamper the recovery of the paraxylene market, should volumes continue to flow into the US Atlantic Coast. Paraxylene import volumes into the US averaged just over 35,000 mt in 2019, but this has spiked in 2020 with the average for the first four months at just under 79,500 mt, data from Panjiva, the trade analysis unit of S&P Global Market Intelligence, showed.

But all may not be lost for the US PX market. Several PTA units are expected to come online in H2 and into 2021, with China's Hengli Petrochemical expected to start its 2.5 million mt/year No 5 PTA line in June-July. The paraxylene requirement for this line alone is estimated at over 1.6 million mt. This will likely push Chinese paraxylene prices higher and level the playing field for US paraxylene by easing the global oversupply.

However, after Chinese PTA inventories hit record highs in Q2, managing these inventories, combined with PET demand, will have the greatest impact on global and US paraxylene balances going forward.

Covid-19 rules European demand Social distancing measures in the wake of the COVID-19 pandemic will continue to depress European paraxylene demand in H2, market participants said. "Buyers are trying to be careful and see how it will go after the release of the lockdown, so we don't see recovery of demand for the moment," a market source said.

The destruction in demand for paraxylene and orthoxylene, driven by lockdowns, has caused European inventories to rise and this trend is unlikely to reverse in the short term, market sources said.

While European paraxylene joined the crude oil price rally over the first full week of May, with FOB ARA prices rising by slightly more than 21% month on month, the demand-supply fundamentals remain unchanged.

European market players see two major drivers for paraxylene over the next couple of months: Asian market fundamentals, led mainly by China, and warmer weather.

Warmer weather during summer, along with the potential easing of lockdown restrictions, could be good news for downstream packaging and bottle industries, and the polyester chain.

— Samar Niazi, Regina Sher, Kevin Allen, Simon Price, Alexander Borulev

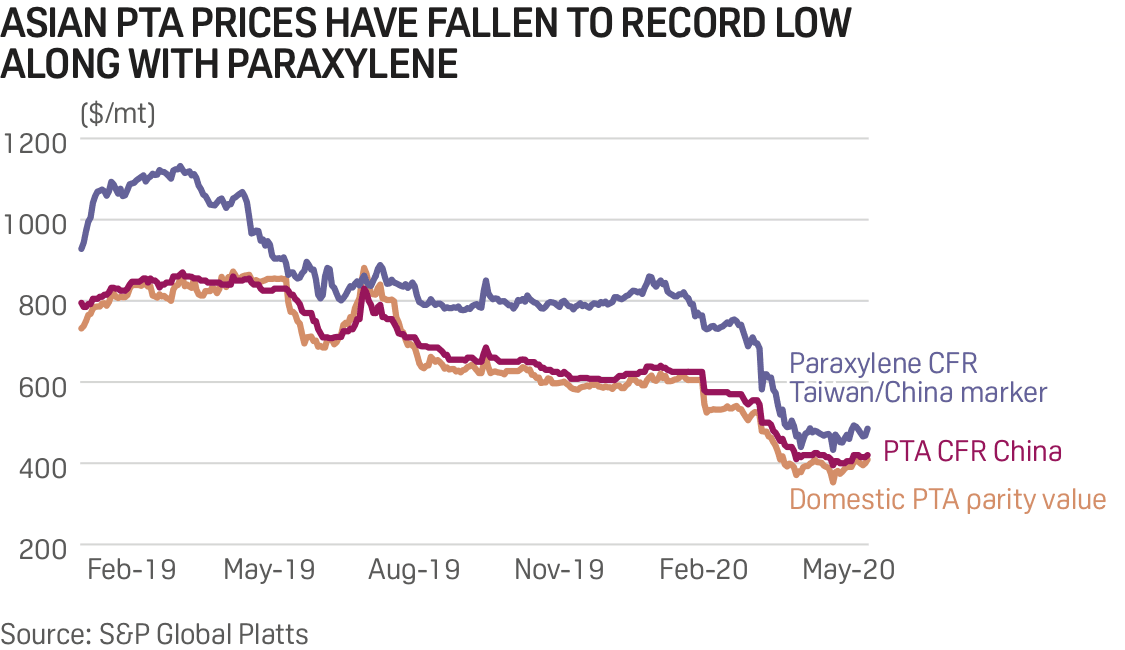

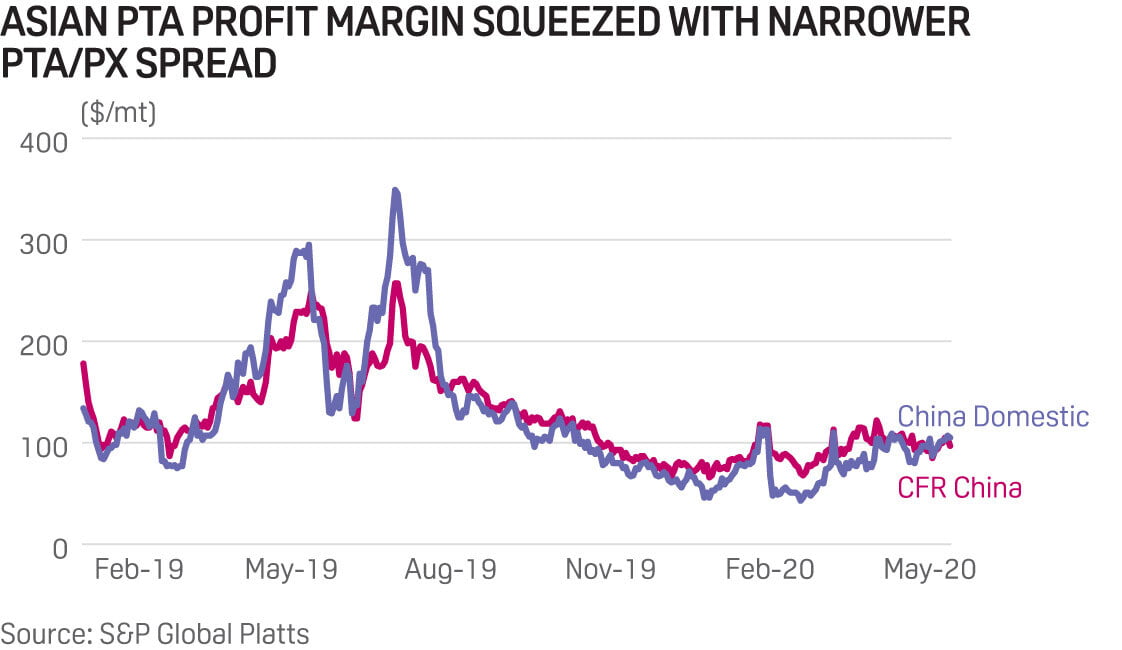

Asian PTA faces supply glut in H2; upstream markets to drive direction

High stock levels, new capacities to lengthen supply

Market participants turn to PX for direction amid uncertainty

Most Asian market participants are taking a bearish view on purified terephthalic acid for the second half of the year, in view of high stock levels, impending new startups and muted expectations over demand recovery after the coronavirus pandemic.

Some market participants, nevertheless, have been wondering if there is still room left for further price declines, given that PTA prices have already hit unprecedented lows.

Asian PTA prices tumbled to a record low of $395/mt CFR China on April 22, and have been hovering around the low-$400s/mt in May.

Prior to March, the PTA CFR China marker had never fallen below $538/mt since S&P Global Platts launched the assessment in April 2008.

High China stock levels to persist, impending startups Supply-wise, China PTA inventories hit record highs of 3.5 million-3.7 million mt in May, well above the typical level of 1 million-1.5 million mt seen in the past two years.

Such levels are sufficient to cover a month of polyester demand in China and it will take at least a few months to bring stock levels back to normal, on the conditions that polyester demand improves and PTA operating rates decline, sources said.

China-based PTA producers, however, have been maintaining high operating rates of 85-95% since April despite record high inventory levels because of decent PTA margins.

This caused concerns among some producers in Northeast and Southeast Asia as they were forced to cut production in the second quarter due to lackluster demand and less competitive production costs, with the exception of South Korea producers, which mainly targeted European markets for exports.

Cash flow could turn into a major problem for market participants within the polyester value chain if high stock levels for PTA and other commodities along the chain persist, two PTA producers said, adding that it is just a matter of time that rationalizing of production would be required for the industry.

A total of around 7.2 million mt/year of new PTA capacity is also expected to be brought online in China in H2 2020, including 2.5 million mt/year from Hengli Petrochemical in June-July, 2.2 million mt/year from Xinfengming Group Co Ltd in September, and 2.5 million mt/year from Fujian Baihong Group in October, according to market sources.

This will bring the total effective PTA capacity to 59.8 million mt/year in China and 79.8 million mt/year for the whole of Asia by year-end, Platts data shows.

Upstream PX to drive PTA Despite expectations of weak PTA demand-supply fundamentals extending into H2 2020, several trade participants said the recent key driver of PTA prices has been the price direction of upstream paraxylene and the direction of crude oil, and they are predicting a continuation of this scenario.

Subsequently, most US -dollar denominated spot PTA transactions have been discussed on a PX -linked floating formula basis, instead of fixed prices, to minimize risks amid sharp price volatility in upstream markets.

The PTA to PX spread averaged $93.7/mt over January to mid-May, according to Platts data.

— Miranda Zhang, Eric Su

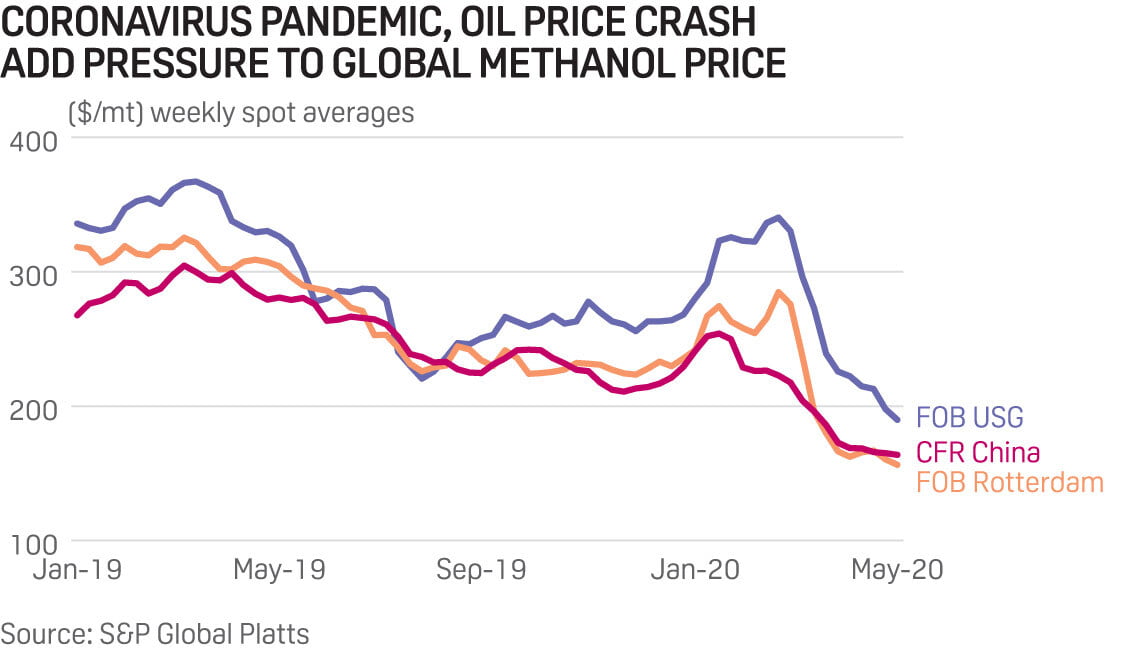

Global methanol supply to remain long amid slow recovery

Global demand still under pressure

China to see more Iranian supply

Europe and the US eye run rates

The global methanol market’s struggle with long supply levels, exacerbated by weaker demand due to the coronavirus pandemic and the recent oil price crash, is expected to continue in the second half of 2020, with only a moderate recovery in demand likely.

With methanol markets worldwide influenced by the price movements of oil, global methanol spot prices reached multi-year lows in the first half of 2020, following significant losses in crude oil values, and any recovery is expected to be slow paced. Fundamentally, little changed during the first half in the key global demand center market, China.

But although the Chinese market remained oversupplied, shortages of tank storage space in the east of the country this year were more acute than previously, with the global COVID-19 containment measures having weakened downstream demand.

As a result, Chinese methanol prices hit 11-year lows in Q2 and, while this should make methanol-to-olefin plants profitable, downstream demand for methylene diphenyl diisocyanate, superplaticizer and formaldehyde have been recovering at a glacial pace, trade sources said.

Only demand for polypropylene to make medical masks has been providing methanol-to-olefins positive margins, hitting a two-year high in Q2, according to S&P Global Platts calculations.

In addition, Chinese methanol prices could come under further pressure in H2 2020 with the start-up of two new methanol plants in Iran.

Middle East Kimiaye Pars Company's 1.65 million mt/year plant commenced operations in May, following on from Bushehr Petrochemical Company's 1.65 million mt/year plant in February, thereby increasing Iranian methanol nameplate capacity to 12.2 million mt/year. Both Kimiaye and Bushehr plan to target China as their main export market, as stricter banking controls in India have made payment to Iranian producers difficult.

India typically imports about 140,000-160,000 mt/month of methanol, with Iranian methanol constituting about 75% of that. But Iranian shipments to India have dropped significantly since February.

Saudi Arabian, Qatari and Omani methanol producers, which were previously priced out of the Indian market, will likely ramp up production to meet that demand, trade sources said.

Run rates under pressure In the European market, the demand outlook is set to be gloomy at least until the summer as underlying consumption will continue to be affected by the pandemic.

The automotive and construction industries were hit hard in Q2, with the market anticipating a drop in demand from formaldehyde — the largest single outlet for methanol — of some 10-20% below Q2 2019.

Total European methanol demand loss in 2020 is expected to be up to 20% this year, although estimates can vary to a drop of 8-9%, in line with the eurozone’s GDP fall.

Several methanol consumers said they had to reduce consumption, adjusting facilities’ run rates to reflect the drop in demand.

"Demand is on the low side, we are committed to contractual volumes, there is no room to buy from the spot market," a methanol buyer said, adding that spot prices were attractive.

The FOB Rotterdam spot level has been hovering around 40-45% discount to the Q2 contract price at Eur255/mt, significantly above the commercial discounts for 2020, which are around 25-26%.

With signs of recovery to pre-pandemic levels potentially to be seen only towards the end of the third quarter, the market will keep an eye on margins, expecting a drop in methanol production from marginal cost producers operating below cash costs.

The US is unlikely to see any facilities come offline entirely as a result of global markets trying to balance out supply with lagging global demand. The low cost and ready supply of domestic natural gas available as a feedstock have translated into a relatively low cost of production for North American producers.

However, with weaker demand from domestic production of formaldehyde, MTBE and acetic acid, some small declines in US methanol production rates could be seen moving into the second half of the year.

As the US works its way through methanol supply inventories in the face of low demand, the timelines for starting up several new planned production facilities could be extended. Methanex has placed development plans for its Geismar 3 methanol production facility on temporary hold for up to 18 months, and has temporarily idled its Titan plant in Trinidad and its Chile IV plant in Cabo Negro until market conditions and demand improve. A similar decision was taken by Proman in Q2, which idled two units at the Point Lisas Industrial Estate in Trinidad and Tobago. The units affected are M2 and M3, with an annual capacity of 525,000 mt and 575,000 mt, respectively.

— Esther Ng, Mary Hogan, Lara Berton

Supply length and marginal demand increase point to weak H2 for MTBE

Demand set to rebound in Q4

Stocks likely to remain high

Blending margins squeezed

With businesses reopening and car usage increasing, MTBE sellers have been pointing to a likely uptick in demand in the second half of 2020.

However, there are growing signs that the pandemic could lead to changes well beyond the easing of lockdowns. High stock inventories and weak blending demand are expected to remain a mainstay of MTBE in H2 2020.

Sluggish gasoline demand keeps Europe under pressure European MTBE faces a bleak second half of the year, with high levels of supply carried over after the low call for gasoline resulted in a large drop in blending activity.

The FOB Amsterdam-Rotterdam-Antwerp MTBE benchmark was heavily hit by the coronavirus pandemic and dropped below $180/mt in late April for the first time since March 1999, a sharp fall compared with the $779.075/mt averaged in April 2019, hitting production margins.

With the lifting of lockdown measures, demand is only expected to improve in H2.

“We have seen the bottom of the demand level,” another producer said.

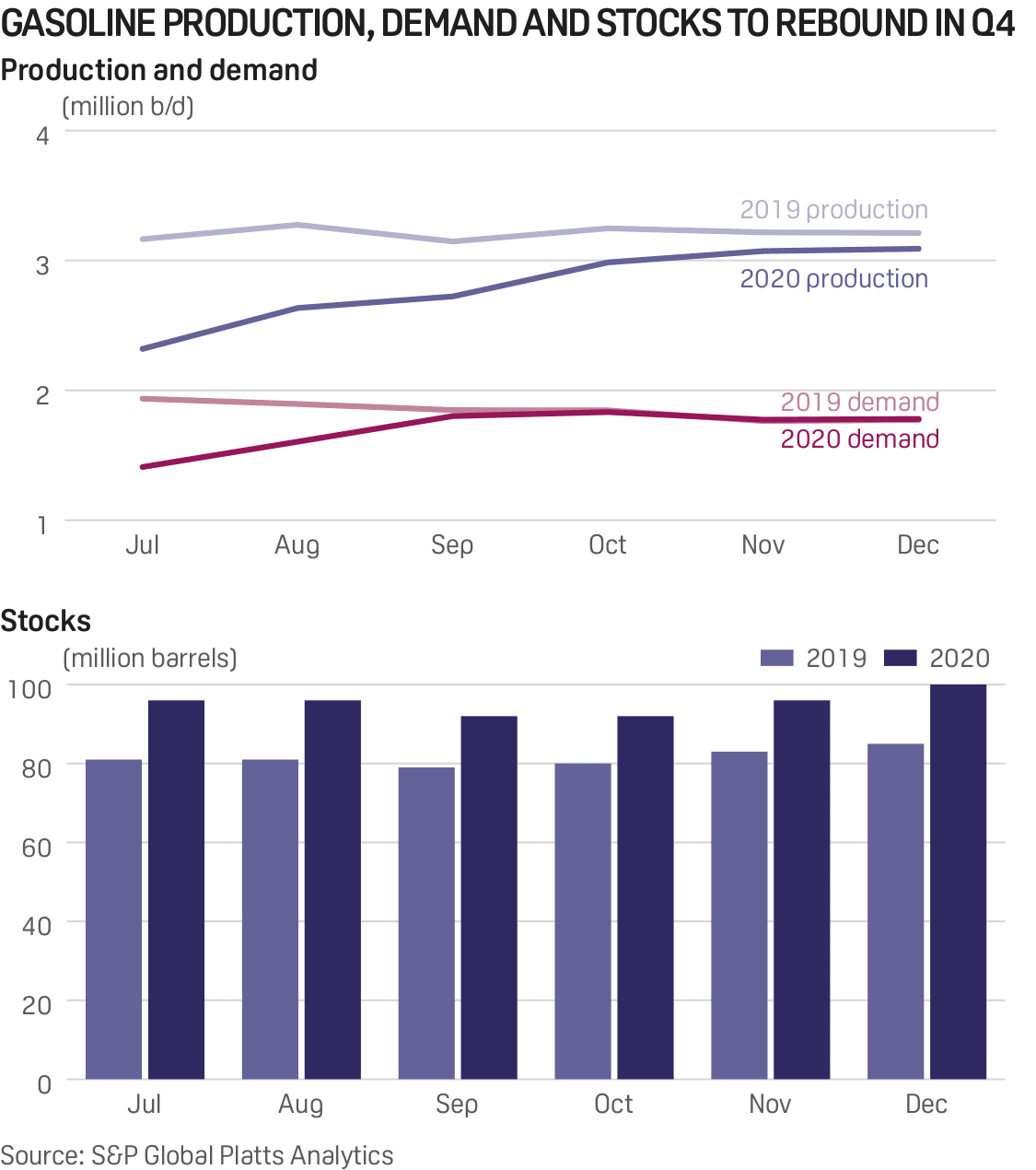

European gasoline markets plunged in the first half of the year, but according to S&P Global Platts Analytics demand will increase gradually to reach around 85% of the 2019 level in Q3 2020 and almost at parity to 2019 by Q4. On a positive note for MTBE, gasoline production is expected to reach 80% of 2019 levels in Q3 and 95% in Q4. However, gasoline stock levels increased in H1 and are expected to be almost 17% higher year on year in H2 2020.

A similar pattern is expected in the MTBE market, with high inventories and limited space availability set to be the main challenges.

“[There is] no solution for the storage, the material at some point has to be consumed, production has to be reduced,” a producer said.

Asian remains in the doldrums, glimmer of hope in H2 Asian MTBE is projected to be in the doldrums at least until early Q3 due to the extended and ongoing lockdowns in many countries in the region.

FOB Singapore MTBE nose-dived to a historic low at $165.80/mt on April 22, while the 92 RON crack spread to ICE Brent crude futures, one of key parameters for measuring blending economics, plunged to an all-time low at minus $13.95/b on April 13 and remained in the red as of mid-May. The net monthly MTBE export value in Singapore, the largest gasoline blending hub in Asia, plummeted to a multi-year low of $858,000 in March, down 93% on February, according to the latest data from Enterprise SG.

Market participants said they were expecting Asian MTBE to gradually rebound in late Q2-Q3, with lockdown measures eased, unless major second waves of the virus occurred.

According to Platts Analytics, 92 RON gasoline is expected to bottom out after hitting $15.25/b in May. However, the price will remain lower than that of 2019 through the year-end. Demand-wise, gasoline in seven major Asian countries hit 5.75 million b/d in March, down 14% year on year. However, this is set to recover to above 6 million b/d from July onwards, although this would still be down compared with previous years.

Market players said they were also worried about the aftermath of COVID-19 on global economies.

One market trader said “[MTBE] will be improved from the current situation, but, [price will be] much lower than 2019s”.

The IMF predicted China’s GDP growth rate at 1.2% this year, the slowest in more than four decades, with India at 1.9% and ASEAN 5 at minus 0.6%.

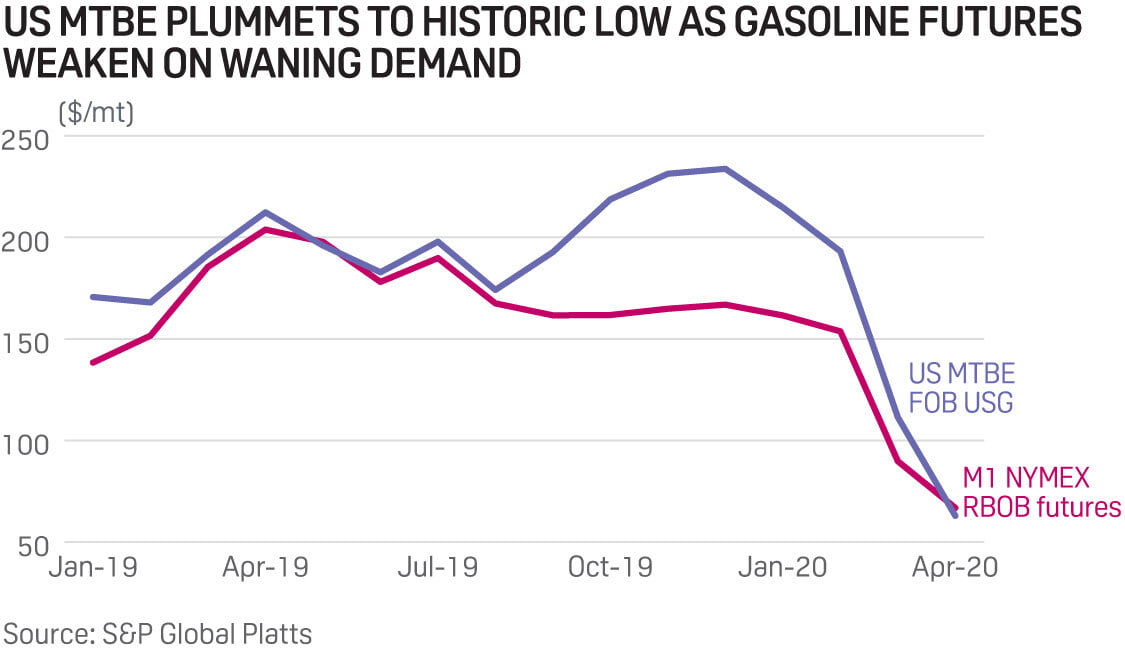

US to see slow recovery as margins improve The US market also expects a slow rebound in the MTBE price, due to lagging transportation fuel demand from Mexico as well as the country’s renewed focus on domestic refining activities.

US MTBE has also seen prices nosedive, recently hitting their lowest since Platts first began assessing the commodity in 1989, with margins venturing into negative territory in mid-March, pressured lower by coronavirus-related demand destruction in Mexico, a primary destination for US gasoline exports blended with MTBE. Gasoline demand in Mexico dropped to a multi-year low in the week ended April 10, following the halt of all non-essential industrial activity in the country and the implementation of social distancing rules.

Demand for gasoline is expected to rebound once normal economic activities resume, which is likely to begin in stages from around June 1, according to guidance from the Mexican government.

US production of MTBE could be slow to rebound as well, with several regional producers having announced cuts as a result of negative product margins.

Both Enterprise Products and Lyondell Chemical Co., in their Q1 earnings communications, announced lower utilization rates for their MTBE production units amid poor demand and weak margins. Indorama in its Q1 earnings report said its MTBE business had been adversely affected by low margins, although the company gave no further guidance regarding production rates.

— Stergios Zacharakis, Michelle Kim, Mary Hogan