In the European ethylene supply chain, import competition from cheaper US derivatives has widened the disconnect between contract and spot prices, with contract pricing primarily reflecting the domestic feedstock slate and spot incorporating length in global markets.

At a time of falling global demand amid economic slowdown and the more recent coronavirus outbreak, cheaper US product flow into Europe has exposed high cost, naphtha-based European supply priced against the monthly ethylene contract price mechanism contrasting with weaker global spot price fundamentals. Nowhere has this been more dramatically felt than in the market for ethylene glycols, where the demand for US-produced mono-ethylene glycol imports has resulted in the collapse of European spot prices.

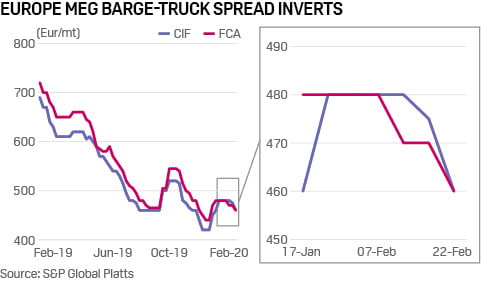

High European feedstock prices have fed through to the domestic MEG contract price while the MEG spot market has taken direction from pricing and supply availability beyond Europe. European ethylene contracts began 2020 above Eur900/mt, settling at Eur970/mt FD NWE in January — more than Eur300/mt above the MEG January contract price of Eur625/mt FD NWE. The MEG contract price was in turn commanding a premium of more than Eur125/mt, or 25%, over spot prices at the start of the year, with the FD NWE spot market averaging Eur495/mt for January and the CIF NWE spot barge market also pricing below Eur500/mt CIF NWE, having fallen from spot levels above Eur700/mt at the start of 2019, according to Platts data, continuing a trend of widening contract premiums to spot. The average MEG gross contract premium over FCA spot trucks amounted to Eur128/mt in 2019, up from Eur122/mt in 2018 and Eur106/mt in 2017. Trucks are the usual method for distributing the excess supply from European producers who sell into the spot market.

The widening spread has seen some participants increase their exposure to spot volumes. Buyers have reduced their overall contractual commitments for 2020 to as low as 30% in some cases, according to sources, with the bulk now sought from the spot market. Until 2019 contractual volumes accounted for approximately 90% of all trade.

“Consumers of MEG are relying [more] on the spot market. Most customers have less contracts in place, and in some cases they are still waiting to negotiate contracts. One customer has fixed one contract and we are willing to discuss the other term. 50 kt [has been] contracted and the other 50 kt they are trying to negotiate. Another 50 kt is on the spot market. Big end-users of MEG are relying on the spot market more than they did in 2017-2019.”

“They want the bigger parcel. [They] wouldn’t want to commit on contracts but they wanted a bigger portion of spot, to commit more…and to take advantage of falling [global prices], which they have. That’s what we have — the result of the oversupply from the US” an MEG trader said in February.

Increased interest in spot volumes since the start of the year, compounded by late settlement of 2020 contracts, has strained logistics systems set up to handle much smaller volumes. In a rare market occurrence brought about by the greater demand for spot barges, the CIF-FCA spot price relationship inverted, with domestic FCA trucks trading below imported CIF barges in February. “The output increased so remarkably but the [US] terminals did not grow with [it]…They have not been able to handle it. That has been driving freight rates up crazily. It was [around] $50/mt last year and now it is up to $100/mt so demand has exploded — [this being] the consequence of that increased export demand,” the trader said.

However, sources expect logistics systems to adjust eventually as they bed in to the new additional spot demand.

Platts assessed MEG FCA truck and CIF NWE barge spot prices at Eur470/mt and Eur480/mt, respectively on February 14, the first time the truck-barge premium has flipped to a discount since April 2013.

With spot prices below Eur500/mt in Europe despite higher barge demand, similarly steep spot market declines in the US and Asia, and contractual volumes significantly lower year on year, indexation for remaining contracts may tilt increasingly toward spot. While most European contract formulas price against a combination of the industry-settled monthly contract price and Asia spot, one glycols trader told Platts during 2020 negotiations that some contracts had been agreed on a spot-only basis. The same source said some market participants had stepped away from indexation based on the monthly contract price due to repeated late monthly contract price settlements. The MEG monthly contract price regularly settles after delivery, according to industry sources, with the February 2020 contract price only confirmed settled in early March.

—Miguel Cambeiro, Kristen Hays