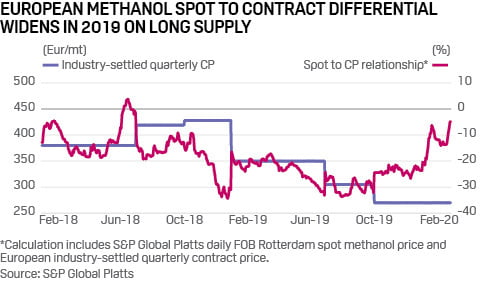

Methanol consumers have also started looking at the spot market, notably in Europe. During the second half of 2019, the price differential between the FOB Rotterdam spot methanol price and the European industry-settled contract price widened beyond typical discount levels for 2019 contracts of 22-24%. As shown in the graph, between July and August 2019, European spot prices were at a 30% discount or higher to the quarterly contract price and averaged 25% below contract prices in 2019, according to Platts data. Bearish fundamentals included weaker downstream demand due to slower economic growth and additional methanol capacity coming online in other regions, with Europe becoming the lowest priced region in October. This has led to a reduction of contractual intake in 2020, as buyers are hoping to buy cheaper spot volumes, if underlying demand improves, several sources said.

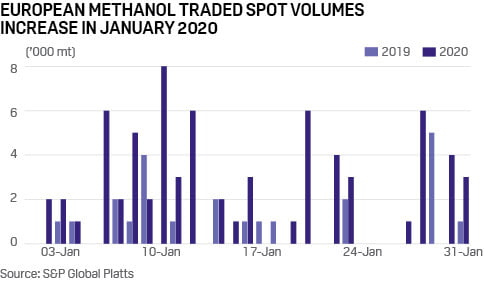

“It is also due to flexibility…consumers can play this by having different purchase contracts in place,” a source said, adding that several customers are more exposed to spot buying this year. At least 70,000 mt were sold in the spot market in January 2020, which was above levels seen a year ago, sources said.

Despite the uptick in spot activity, several sources said consumers still prefer to stick to contractual agreements as negotiated discounts have widened this year to range from 24% to above 25% in some cases, making net contractual prices more attractive than spot. European spot prices averaged Eur238.50/mt in January and February, 13% below the Q1 quarterly contract price of Eur270/mt.

Sources have attributed the surge in spot trading in early 2020 to favorable arbitrage economics between Europe and the US, with several vessels heard fixed out of Rotterdam. However, market participants believe that when US production improves and the arbitrage is shut, spot activity is likely to slow down in Europe.

In the US domestic market, contract pricing structures still appeal more to methanol consumers, looking to minimize pricing fluctuations and lock in a relatively predictable price month to month.

Despite recent and upcoming increasing methanol capacity in the US, spot prices in the US have retained their strength, remaining the highest-priced region amid turnarounds. Between January 1 and February 25, the FOB USG spot price averaged around $314/mt, up $52/mt from the December average. Throughout 2019, monthly contract values maintained a relatively stable premium to average monthly spot prices. In H1 2019, contract values averaged $97.20/mt over spot values, and in H2 2019 they averaged $89.90/mt over monthly average spot values.

Meanwhile in China, while the portion of spot activity done on a yearly basis is above European and US levels, 2020 has seen no change in buying pattern. Chinese methanol buyers have agreed 80% of their 2020 volumes on term contracts, with 20% bought from the spot market, unchanged on the year. Chinese methanol contracts are typically indexed to spot prices. New Iranian methanol capacities — Bushehr Petrochemical Company’s 1.65 million mt/year and Middle East Kimiaye Pars Company’s methanol plant of the same capacity starting up this year — held out the promise that Chinese buyers would allocate more purchases to spot in 2020, but this was in the end conjecture. Some buyers even increased the proportion of their term cargoes to 90% from 80%, which turned out to be very prescient with a series of unplanned plant outages in Asia, Iran and the Middle East in January tightening supply across Asia. Others in China opted to buy more term cargoes to sell into the domestic market where margins are healthier, trade sources said. China is expected to import less than 10 million mt of methanol in 2020, like it did last year, as the coronavirus epidemic has dampened economic growth in the country.

—Lara Berton, Esther Ng, Mary Hogan