A rise in European styrene imports and weak demand weighed on the European spot market in 2019, resulting in a growing disconnect between the spot and the industry-settled contract price. In response, buyers are said to have pushed for amendments to contract formulas to reflect more spot pricing elements.

Styrene contract volumes are typically negotiated annually, with pricing determined monthly through the industry contract price (CP) mechanism, usually at a pre-agreed discount expressed as the CP minus a fixed percentage. Participants look to the relationship between spot and contract prices throughout the year as a measure of relevance for these contractually agreed discounts.

In 2017, 2018 and 2019, spot styrene prices averaged around 12%, 14% and 17% below contract settlement prices respectively, whereas the 2020 average between January and February stood at 25%, Platts data shows. Negotiated contract discounts were said to be in a 12%-15% range in 2019, with buyers heard to be seeking wider discounts in 2020.

The current push for greater discounts is a function of a variety of factors. First, the European styrene market has been largely bearish since the second quarter of 2019, following an influx of US imports, as market participants sought to bolster inventory levels amid a spate of European maintenance. At the same time, polystyrene demand has tapered off with market participants relying on material purchased at the end of 2019. Furthermore, regional acrylonitrile-butadiene-styrene (ABS) demand has been sapped by weak end-user consumption, particularly from the automotive sector, as well as competitively priced imports from Asia.

From December to January, the regional styrene contract price rose Eur64/mt, driven by stronger benzene feedstock pricing, though sources in the styrene market argued that the increase did not reflect the relatively weak, oversupplied market. With benzene strong and styrene fundamentals unfavorable, the European spot styrene-benzene spread fell to $33/mt on January 13, its lowest level since July 2012 and well below the breakeven level estimated at $250/mt by industry participants.

Increased self-sufficiency in China has also hit global demand and pressured spot pricing in Europe. New capacity in China is expected to reduce the country’s reliance on imports and ultimately curtail demand for European styrene cargoes.

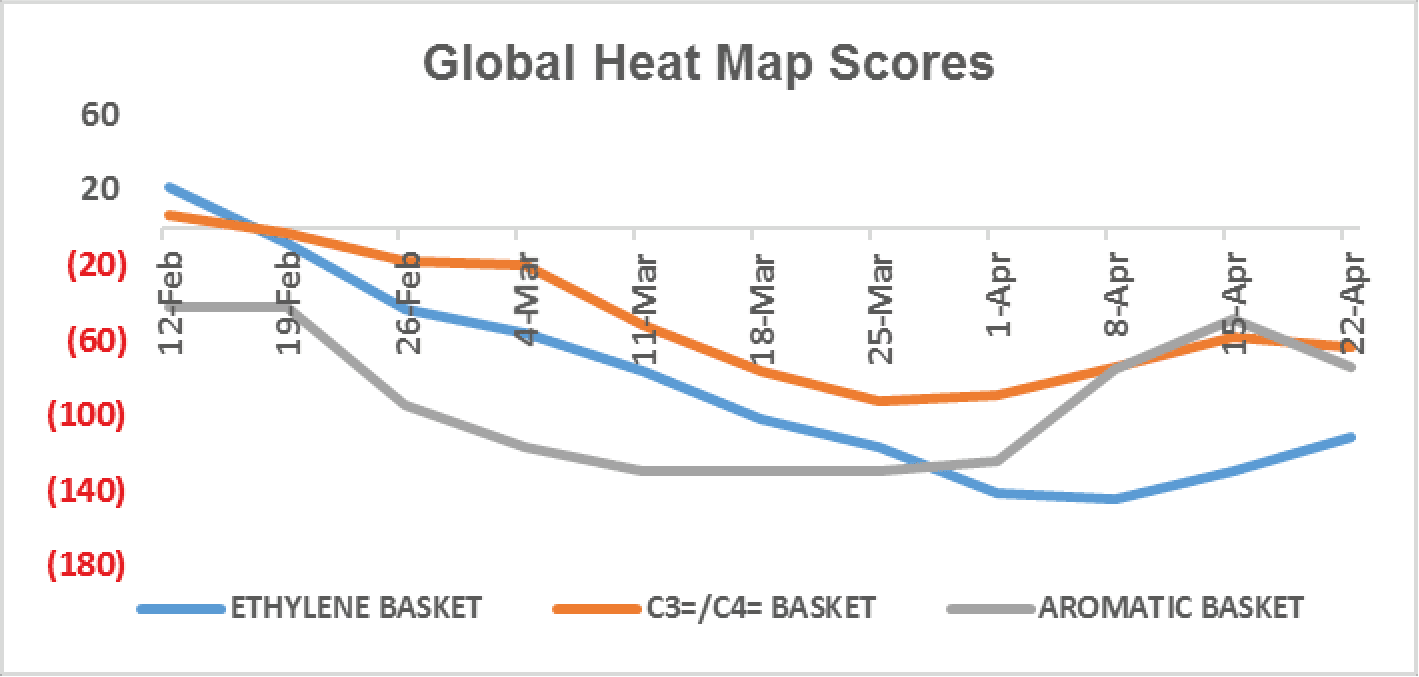

Global Petrochemicals Weekly Heat Map as on April 23, 2020

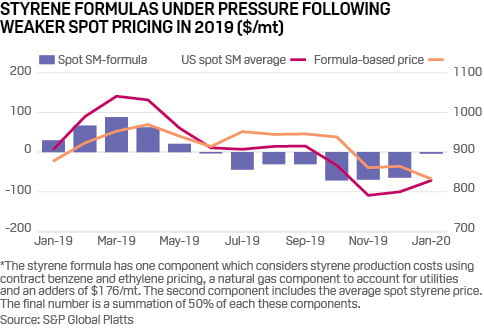

Similarly in the US, a significant differential between spot and contract styrene pricing during 2019 has put pressure on formula-based pricing. Formula-based buyers took losses in 2019 with average spot styrene prices discounted to the contract formula from May through December.

The US styrene contract formula includes components for production costs, spot average and natural gas, as well as an adder, which in 2019 was at $176/mt or 8 cents. US spot styrene prices began to move lower in the second quarter of 2019 amid improved supply and diminished demand with an ongoing trade dispute between the US and China weighing heavily on styrene derivatives.

By September, average spot US styrene prices had fallen to $869/mt and the spot average was discounted to formula-based pricing by $71.53/mt, Platts data showed. To put this number into perspective, a 5,000 mt parcel of styrene in September would cost the buyer roughly $4.345 million, using the monthly spot average. That same parcel for formula-based buyers would cost nearly $4.703 million, meaning that formula-based buyers overpaid by roughly more than $357,000 per 5,000 mt parcel. These dynamics persisted throughout the remainder of the year though the formula-based premium slipped to just under $48/mt in December, Platts data showed.

With formula-based buyers paying a premium during the second half of 2019, buyers sought lower adders to the formula in 2020. Sources have said that adders ranged from 4-6 cents ($88-$132) for 2020 although multiple sources have noted that it would be difficult to get 6 cents in the current environment. In the near term, it appeared this dynamic was unlikely to change as spot styrene prices in the US remained soft with pricing averaging near $785/mt for the first 20 days of February.

This comes at a time when a major US producer is down for planned maintenance from the second half of January through March while a second US producer is slated to undergo planned works in March. Further pressure was expected from new Asian styrene capacities with the start-up of Zhejiang’s 1.2 million mt/year unit and Hengli’s new 720,000 mt/year styrene plant. This, coupled with previously implemented anti-dumping duties from China as well as the recent coronavirus outbreak, has dampened sentiment and is expected to keep the styrene market depressed in 2020, sources have said.

Despite China’s new supply coming online in 2020, total contract volumes in Asia were relatively stable on the year, according to market sources.

China, the major importer in Asia, imported around 3.2 million mt of styrene in 2019, approximately 2% from the US and 4.5% from Europe, while its styrene demand stands at more than 10 million mt/year.

Since late 2019 and into early 2020, the market has seen a closed arbitrage from Europe to Asia due to weakness in Asian styrene and increased freight costs. Firmness in benzene has also held back Asian buyers from signing contracts with US producers based on any cost-linked formulas. With the expectation of fewer deep-sea cargoes available in the Asian market, Asian producers gained some bargaining power in the course of contract negotiations.

One of the major South Korean producers has increased both the prices and volumes for 2020 contracts. However, producers in other Asian regions faced supply competition, with the Middle East remaining the main source of Asia’s styrene imports, and some have opted to concede discounts to buyers. The pricing gap between cargoes subject to anti-dumping duties (ADD) and other non-ADD cargoes was thus narrowed in contract conclusion.

—Kevin Allen, Sophia Yao, Olu Shaw