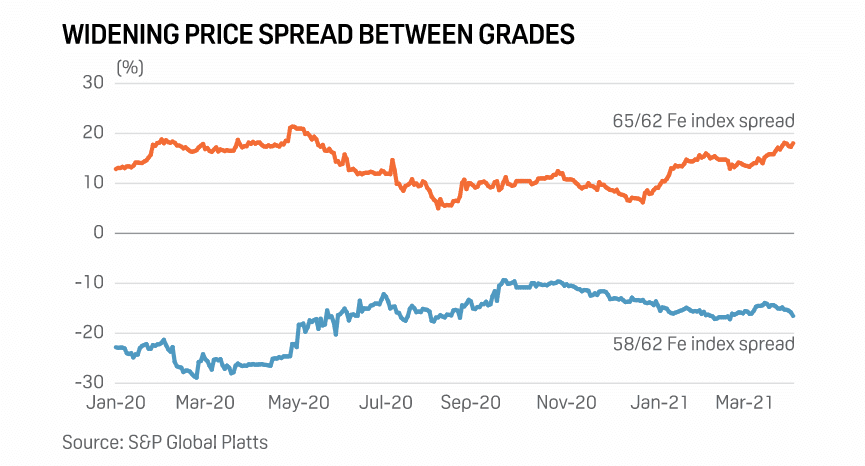

Rising coke prices drove the initial divergence; as the price of coke, which can remove impurities in iron ore, reached record highs, blast furnace economics started to favor higher iron content, lower-impurity ores, as their savings on coke more than offset the extra cost of higher-grade ore.

The indexes diverged again in late March, this time due to widening steel margins. As steel demand continued to recover, the curbs in Tangshan tightened supply, lifting steel prices and margins. Mills elsewhere in China reacted to these price signals by switching ore blends to higher grades to maximize output.

This was a double whammy for the 58% Fe index, both reducing demand for lower-grade ore and increasing prices for the 65% Fe index, in turn exerting further downward pressure on the 58% Fe index, as mills weighed the price of high-low grade combinations against the medium grade to optimize cost.

The spread between the indexes could remain wide in 2021 as curbs in Tangshan continue to support steel margins.