This report does not constitute a rating action

Primary Credit Analysts

Stephanie Mery Paris +33-1-44-20-73-44

Etienne Polle Paris +33-1-40-75-25-11

Hugo Soubrier Paris +33-1-40-75-25-79

Louis Portail Paris

The economic recovery will help French local and regional governments (LRGs) to improve their budgetary performance by 2023, despite elevated capital investment.

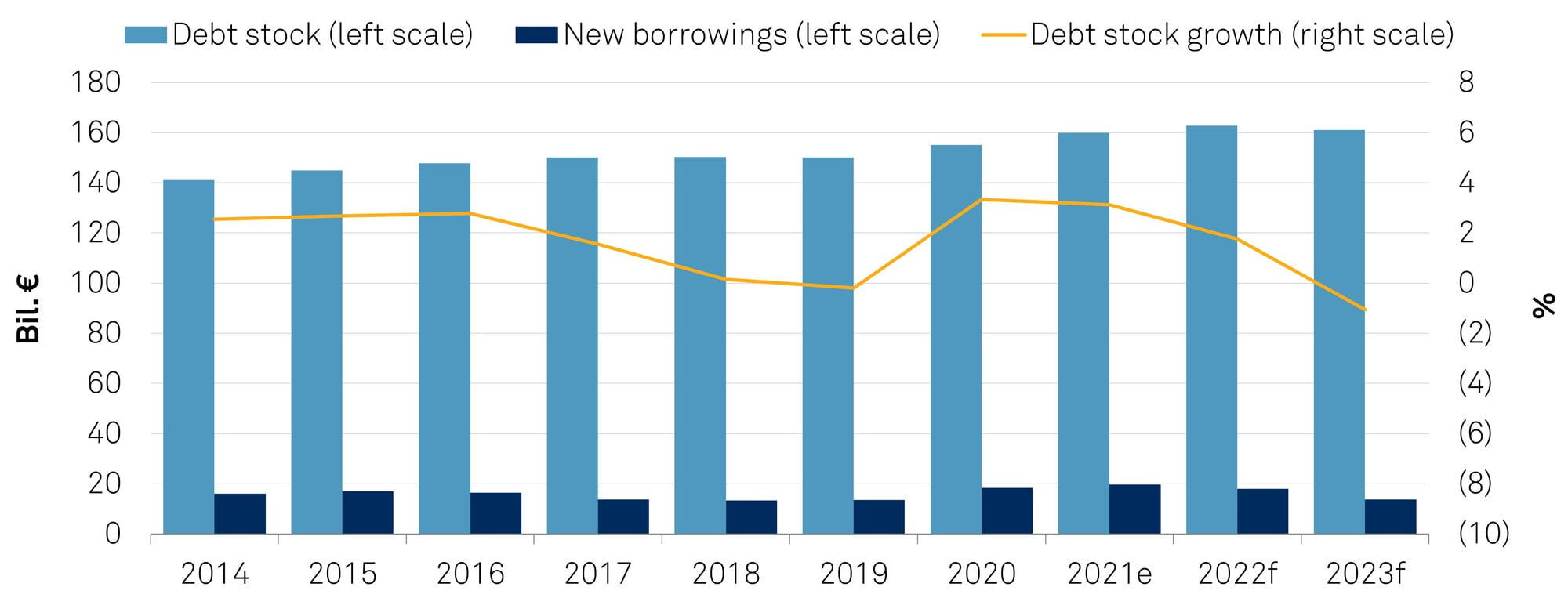

After peaking in 2021, net borrowing should decline as LRGs prioritize deleveraging.

We expect total debt to reach €162.7 billion in 2022 before declining in 2023.

Market liquidity and credit supply will remain abundant and at favorable terms, supporting LRGs' bond issuances in the markets despite the current inflationary pressures.

Downside risks to budgetary performance relate to the evolution of the pandemic and the spillover from the Russia-Ukraine crisis.

We expect the economic recovery to translate into improved budgetary performance among French LRGs compared with the pre-pandemic era. Revenue growth and tight budgetary controls will see operating balances trend upward. However, budget balances will exhibit volatility over the next three years because structural reforms have left LRGs exposed to greater economic cyclicality. Looking ahead, capital expenditure (capex) will feature prominently across all three levels of LRG, as local collectivities put their full weight behind the national investment-led recovery. We expect capex will peak in 2022 but remain elevated as pandemic-induced backlogs ease and project pipelines get underway. Debt will continue to grow in 2022, but taper thereafter, as LRGs post improving balances after capital accounts. French LRGs should continue to benefit from healthy liquidity when tapping financial markets all along the yield curve, despite interest-rate uncertainty.

We expect the geopolitical conflict involving Russia and Ukraine to affect French LRGs, namely through the impact of higher inflation on their budgetary performance. Specifically, we may see upward pressure on operating expenditures due to higher energy costs. In response, we could expect accelerated execution of green-agenda investment projects that would likely generate higher returns on investment due to rising energy prices. We may also see the central government increase social support in response to the rising energy prices, which would affect LRGs' budgetary performance. For example, as recently as March 14, the French government announced an increase in civil servants' pay following rising inflation.

S&P Global Ratings revised its global macroeconomic forecasts on March 8, 2022, to reflect the economic consequences of the Russia-Ukraine conflict. Specifically, we revised our GDP growth forecasts downward and our inflation forecasts upward. We have factored these updated forecasts into our analysis of French LRGs.

We may see upward pressure on operating expenditures due to higher energy costs.

Table 1 | Key National Economic Indicators

CPI--Consumer price index. GG--General government. Source: S&P Global Ratings.

Chart 1 | French LRGs' Debt Dynamic

e--Estimate. f--Forecast. Sources: French Observatory on Local Public Finances for 2014-2020; S&P Global Ratings' estimates for 2021 and forecasts for 2022 and 2023.

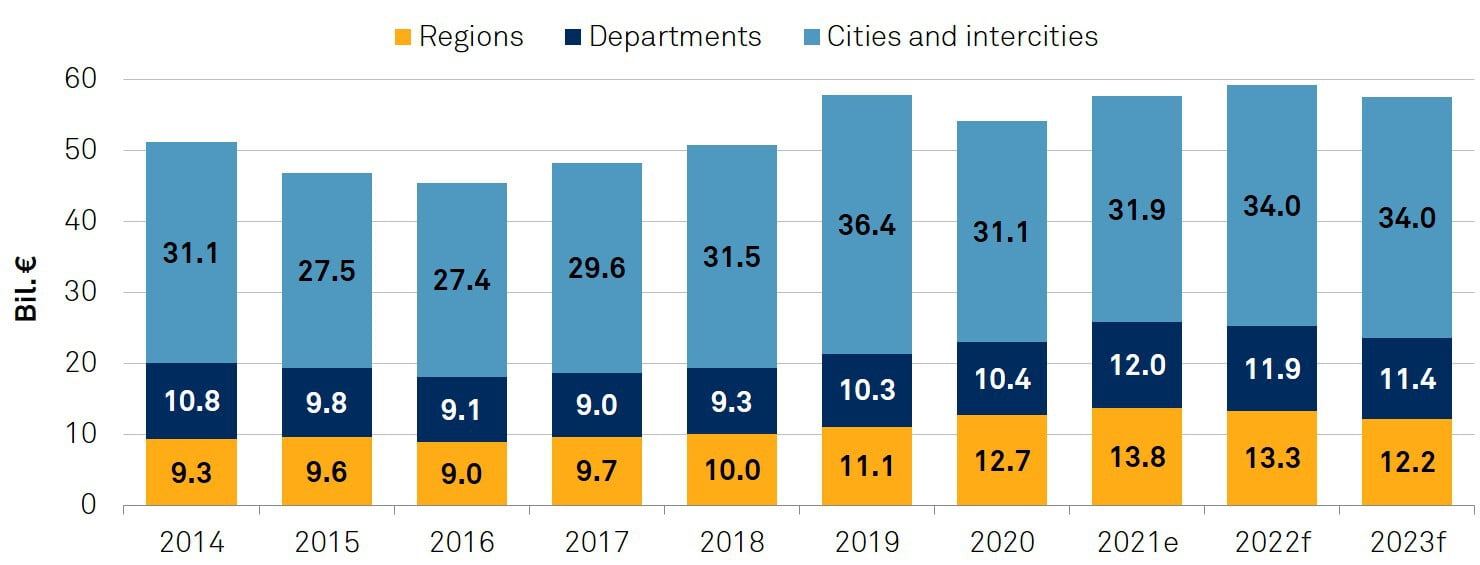

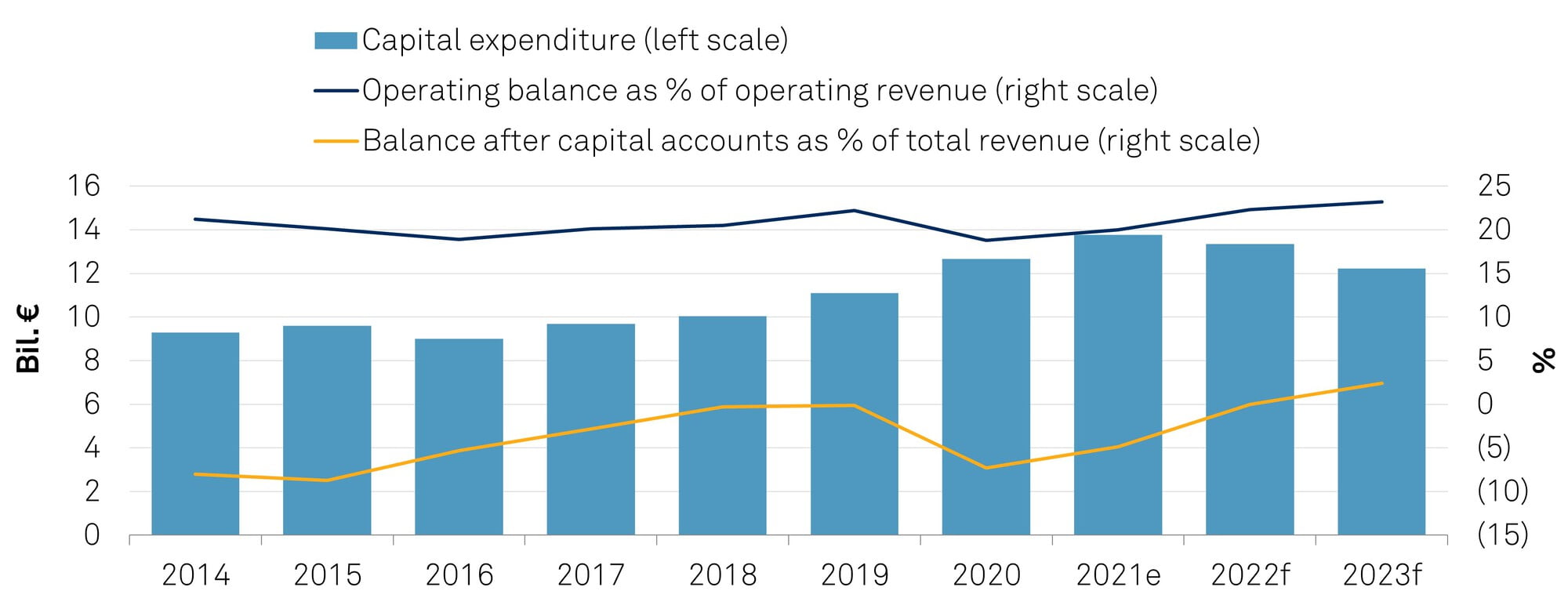

French LRGs remain pivotal to the national economic support plan, "France Relance". They execute about 60% of public investment, while capex represents about 24% of their total expenditure on average. We expect capex to remain very high over 2021-2023, accelerating to €59.2 billion in 2022 before declining moderately to €57.6 billion in 2023 (compared with the 2017-2019 average of €52.3 billion).

Chart 2 | French LRGs' Capital Expenditure

French regions and departments were the main drivers of capex growth in 2021. However, from 2022, we expect this trend to reverse. Instead, we expect cities and intercities to substantially increase capital spending, as their investment projects catch up following implementation delays during 2020 and first-half 2021. We believe that regions and departments will simultaneously taper their investment spending, albeit at elevated levels.

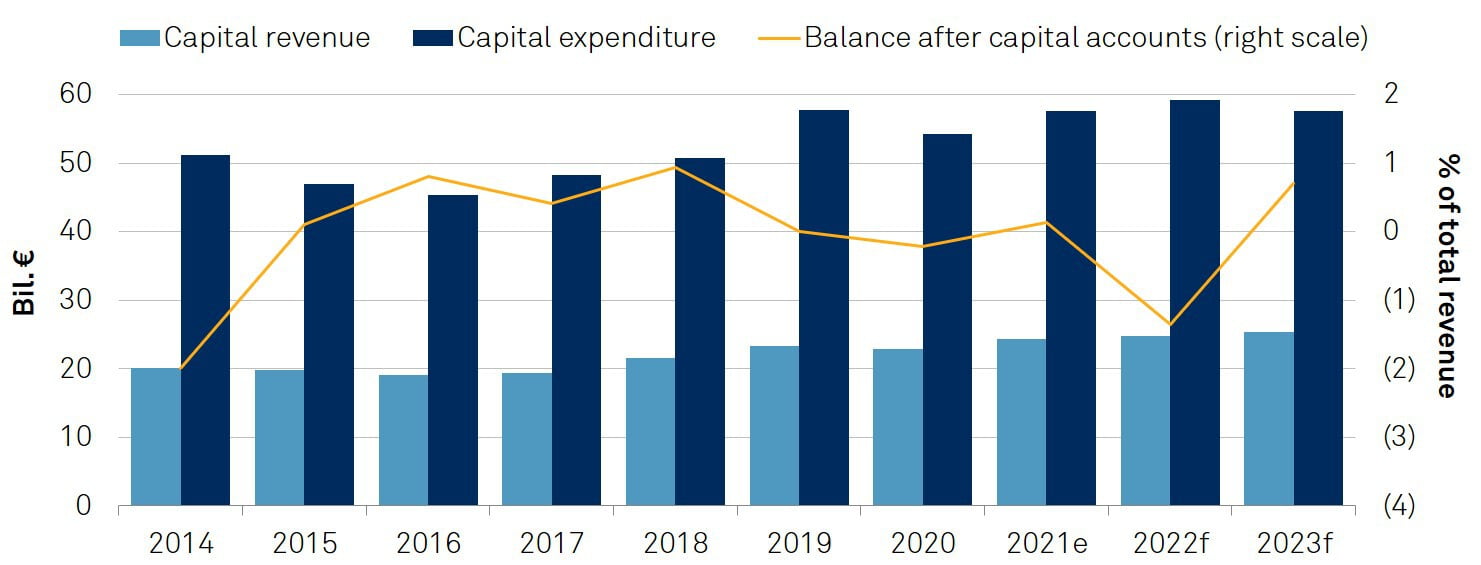

Chart 3 | French LRGs' Capital Accounts

e--Estimate. f-- Forecast. Sources: French Observatory on Local Public Finances for 2014-2020; S&P Global Ratings estimates for 2021 and forecasts for 2022 and 2023.

French LRGs posted a surplus after capital accounts in 2021 following a boost in operating and capital revenue (property transfer fees and investment grants from the central government), despite 6.4% greater capex. In 2022, however, we expect a significant deterioration because of the increase in capex linked to LRGs' role in implementing the national investment plan, resulting in a deficit after capital accounts of 1.4% of total revenue. As capex moderates and the operating balance improves in 2023, we expect the French LRG sector to move back to a surplus.

We expect capex to remain very high over 2021-2023, accelerating to €59.2 billion in 2022.

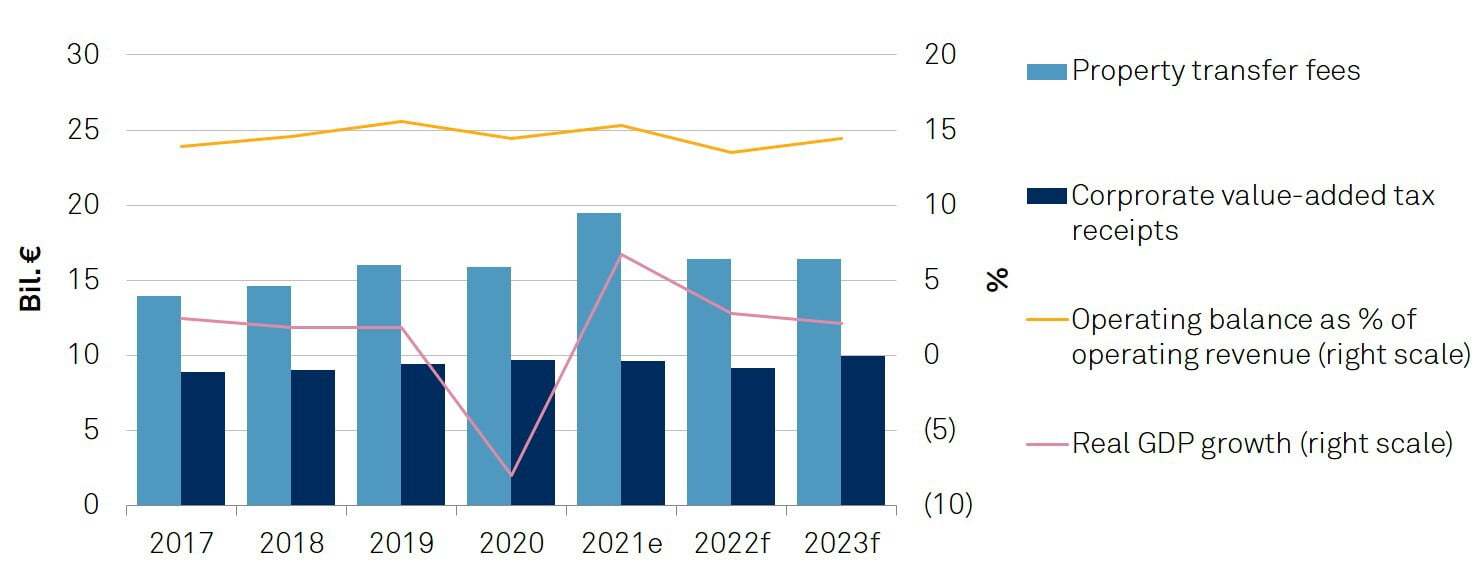

The easing of restrictions and the economic turnaround in the second half of 2021 released pent-up demand for real estate, which propelled both property prices and the number of transactions to record highs. Departments and municipalities subsequently benefitted from an estimated 22.7% increase in property transfer fees. While this windfall helped departments and municipalities to improve their collective operating balances by nearly 8% in nominal terms, we do not expect property-related revenue to remain structurally high. This year will also see a mechanical decline in corporate value-added tax (CVAE) receipts. The expected drop in CVAE receipts of €452 million in 2022 results from the 2020 economic contraction in France of 8%, which will likely prompt a drop in VAT due for 2020 and collected in 2022 owing to the way advance payments play out.

Additionally, all three levels of LRG are exposed to fluctuations in national output, because a large part of their operating revenue has been replaced by a proportion of the national value-added tax (VAT) (see chart 3 above).

On the expenditure side, we anticipate a contained increase in French LRG operating expenditure, thanks to tight budgetary controls and lower-than-anticipated social spending, particularly departments' minimum income support (RSA), because the number of beneficiaries is expected to decline in 2022 in line with the broader economic recovery.

Chart 4 | French LRGs' (Excluding Regions) Budgetary Dynamism

e--Estimate. f--Forecast. Sources: French Observatory on Local Public Finances for 2014-2020; S&P Global Ratings estimates for 2021 and forecasts for 2022 and 2023.

Therefore, despite benefiting from positive economic growth over 2021-2023, we expect an overall deterioration in operating balances in 2022. However, as property transfer fees stabilize, CVAE reverts upward, and the share of national VAT grows in line with the broader economy, we envision a material improvement in the consolidated LRG operating balance in 2023.

We expect the operating revenue of French cities and intercities to fluctuate in line with the broader economy through 2023, given that more than half of their tax receipts are sensitive to economic activity, including the substantial share of national VAT that varies with national economic growth. Specifically, we expect revenue growth to decline in 2022 due to the previously mentioned decrease in corporate VAT and a probable delay in traffic and service-related revenue (parking fees, visitor tax, and so on), because the daily flow of people may take longer than anticipated to revert to normality.

On the expenditure side, cities and intercities are mostly exposed to inflation-linked spending, adding further uncertainty to their budgetary performance. Overall, we expect cities' and intercities' operating balances to decline by 7.8% in nominal terms in 2022, before increasing by 12% in 2023.

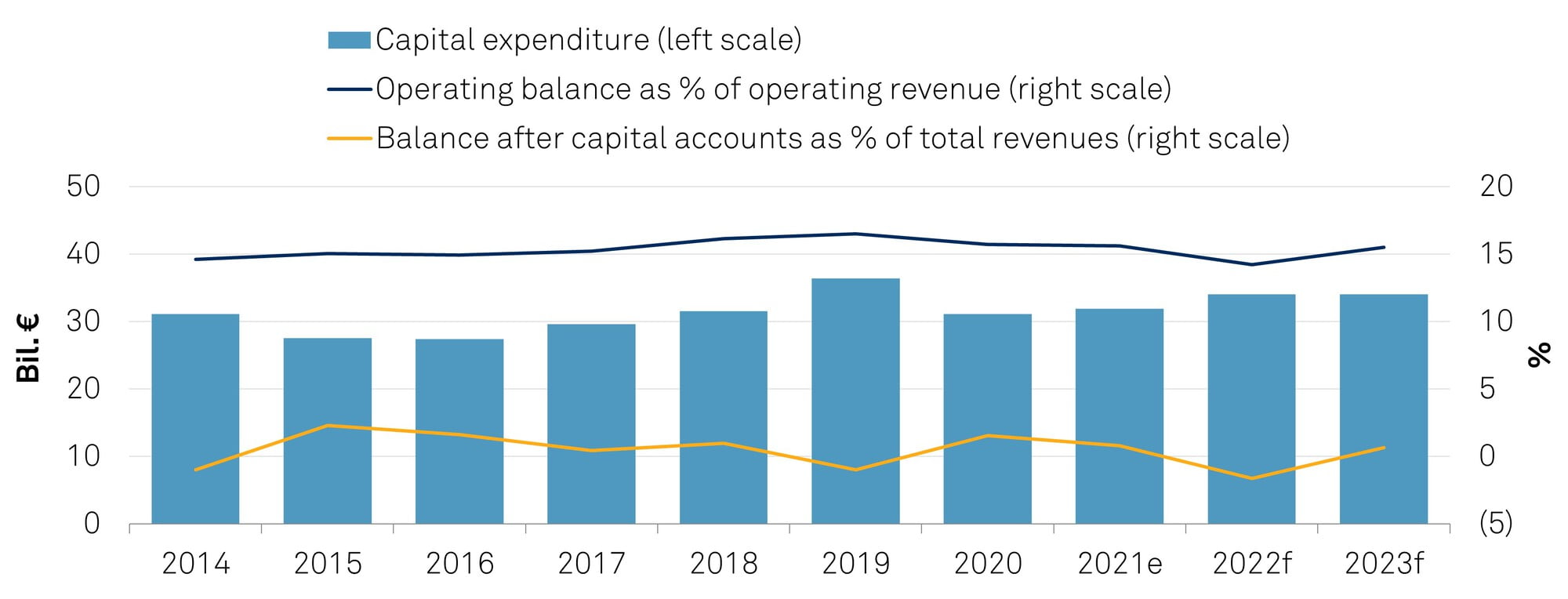

Cities and intercities will spearhead the French LRG contribution to the national recovery plan with a substantial increase in capex.

Chart 5 | French Cities' And Intercities' Budgetary Performance

In our view, cities and intercities will spearhead the French LRG contribution to the national recovery plan with a substantial increase in capex from €31.9 billion in 2021 to €34 billion in 2022 and 2023. We believe capex was subdued in 2021 because it was a planning year for the new investment mandates, and because pandemic-related mobility restrictions delayed many construction projects. We expect restrictions to ease in 2022, and cities and intercities to therefore accelerate capital spending and project delivery.

We expect capital revenue to grow by almost 7% in 2023 following an increase in investment grants from the central government and planned sales of nonstrategic assets. In 2022, a deteriorating operating balance and concurrent increase in capex will push cities and intercities into a deficit after capital accounts. But we expect a strong return to surplus in 2023 as capex stabilizes and operating revenue improves.

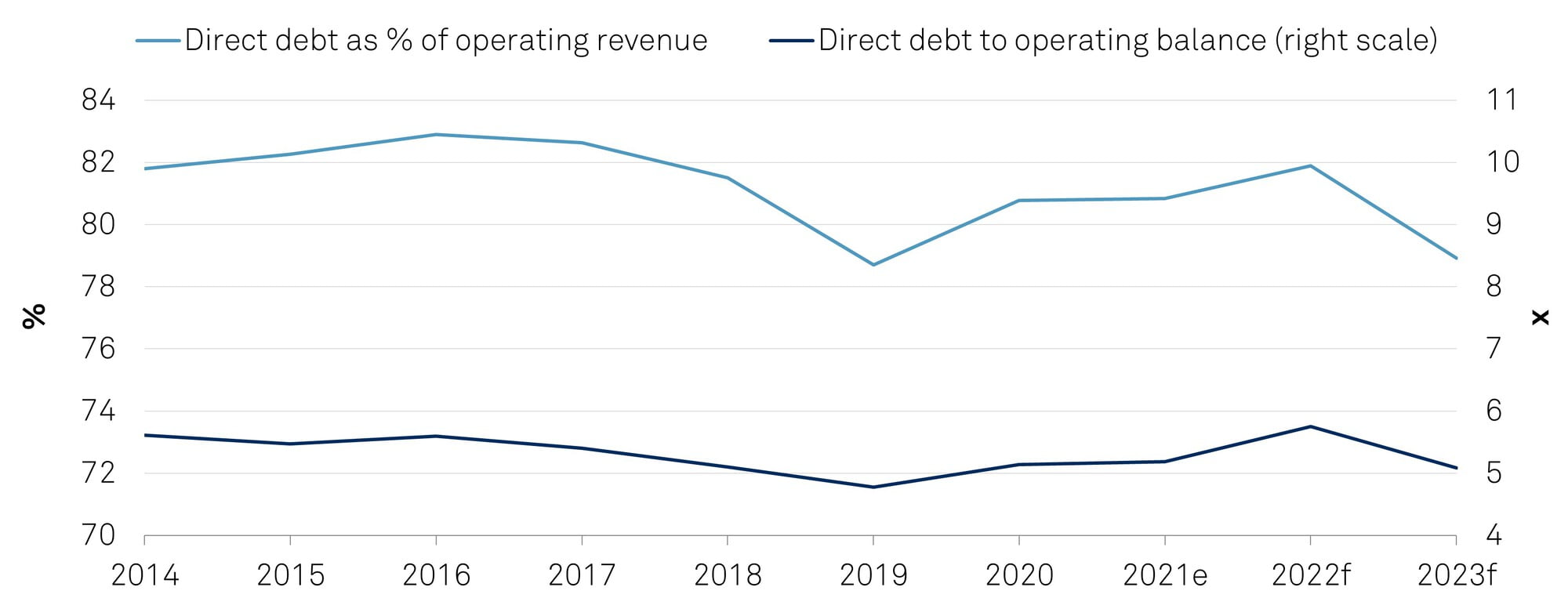

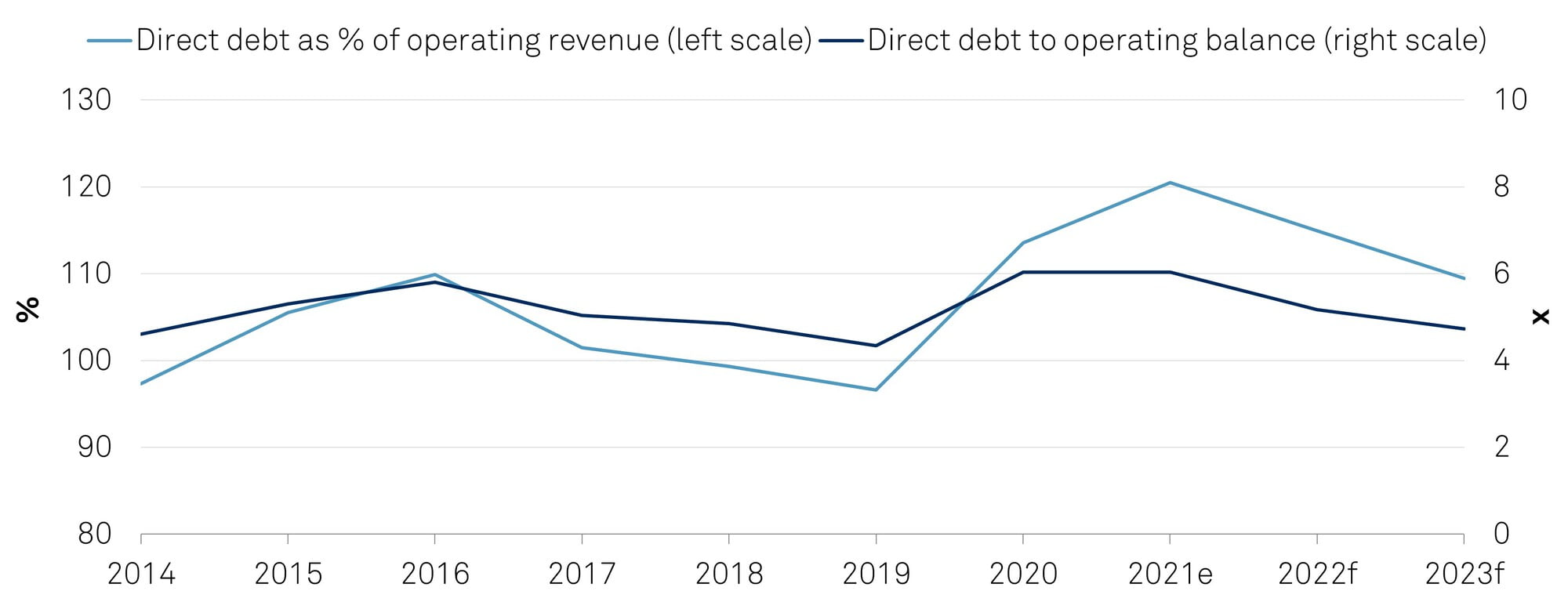

As a result of the deterioration in budgetary performance in 2022, borrowing will increase, but will decrease in 2023 as operating balances improve. We expect debt repayments to grow very marginally, while the debt stock should remain relatively stable at about €95 billion through to 2023. The debt-to-operating-balance ratio should also remain marginally above 5x on average, and debt-to-operating-revenue about 80%.

Chart 6 | French Cities' And Intercities' Direct Debt Dynamic

We expect the same budgetary dynamics to play out for departments as for cities and intercities. In contrast to cities and intercities and regions, however, departments can no longer determine their own tax revenue. The structural reforms to property taxes that came into effect at the beginning of 2021 have effectively eliminated departments' last remaining rate-setting powers. We believe that these reforms have weakened departments' budgetary flexibility and widened their structural revenue and expenditure imbalances, leaving departments even more exposed to economic and real estate cyclicality than before.

The 2021 reforms introduced a share of national VAT instead of property tax; we expect the nominal amount to be slightly larger than the property tax receipts in 2019, effectively shielding departments from the pandemic-induced drop in 2020 VAT receipts. Like cities and intercities, departments also benefited from the near 23% increase in property transfer fees as real estate activity rebounded. At the same time, on the expenditure side, the number of RSA recipients saw a smaller-than-anticipated increase given the economic turnaround. In 2021, nominal operating balances should consequently increase by nearly 30% with a surplus after capital accounts of 1.4% of operating revenue.

In 2022, we expect a 1.4% decline in operating revenue following the reversion of property transfer fees and the mechanical decline in corporate VAT receipts. At the same time, we expect operating expenses to continue growing at roughly 1.3% on average. As a result, the nominal operating balance is forecast to decline by 18.4% in 2022. In 2023, we expect an improvement in operating balance, albeit not to the levels observed in 2021.

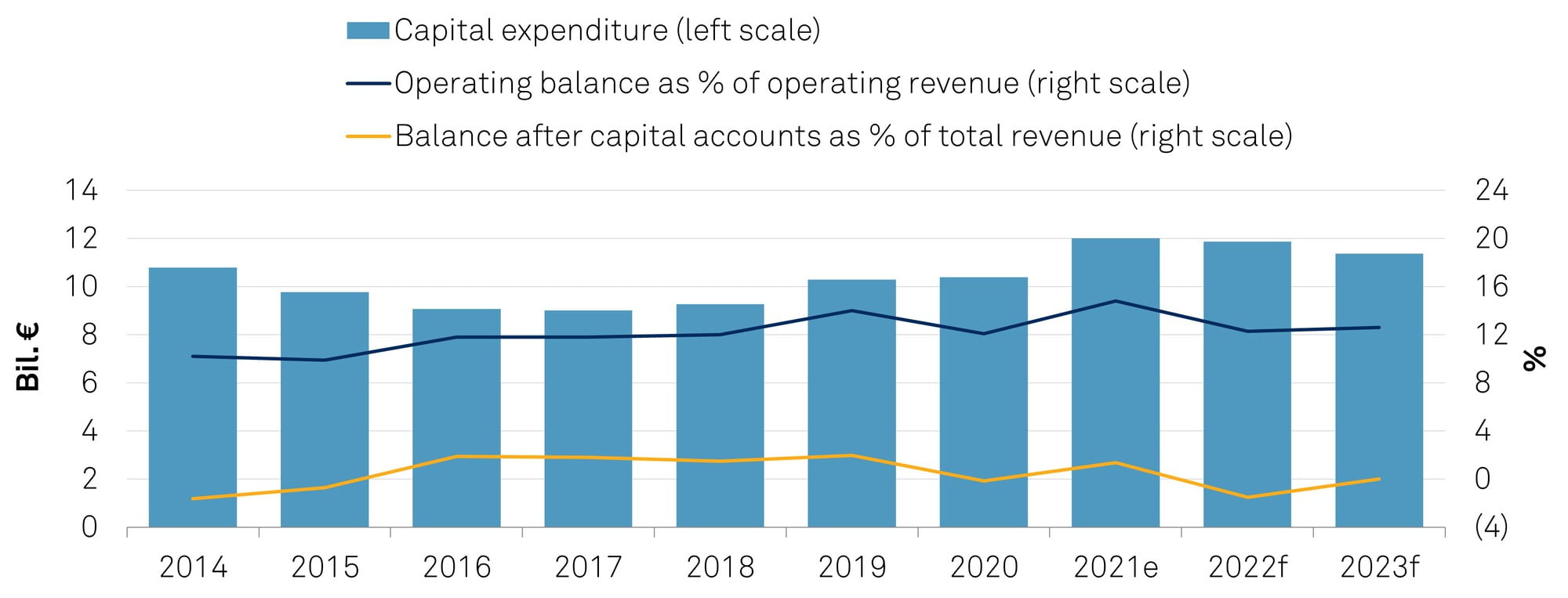

Last year saw capex rise significantly as work resumed on investment projects that were delayed in 2020 due to the pandemic-related shutdowns, and departments concentrated on the investment-led recovery. Departments' capex will trend downward by nearly 3% across 2022 and 2023, but remain at historically high levels. The deficit after capital accounts is expected to amount to 1.5% of total revenue in 2022 before balancing in 2023.

Chart 7 | French Departments' Budgetary Performance

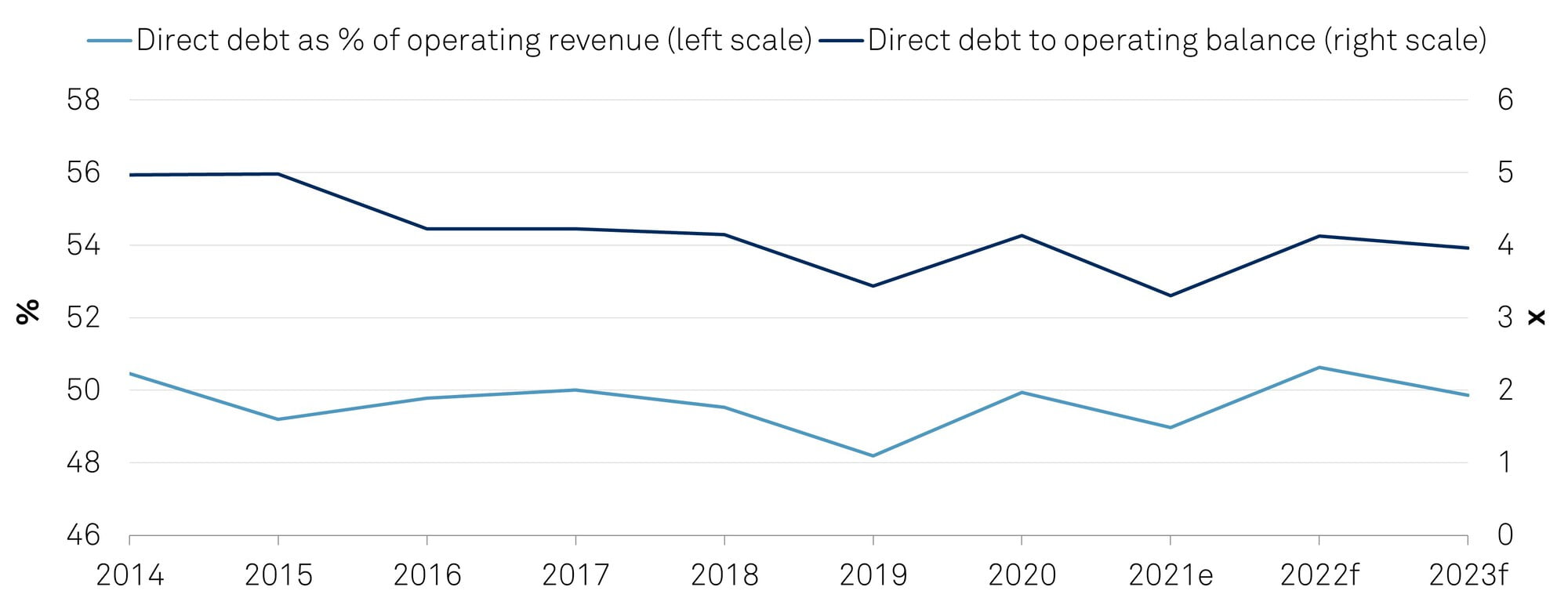

We expect borrowing to increase in 2022, as departments look to finance their sizable deficits after capital accounts, before a decline toward pre-pandemic levels in 2023 on the back of deleveraging efforts. Debt-to-operating-revenue ratio should rise from 49% in 2021 and stabilize at about 50% in 2022-2023.

Chart 8 | French Departments' Direct Debt Dynamic

In our view, French regions will continue to benefit from a favorable institutional framework. Successive reforms have strengthened the role of regions, granting them additional competencies and responsibilities, such as managing interurban and school transport, with corresponding funding from the central government. We also view as positive the budgetary impact of the central government transfer of an additional fraction of national VAT receipts in 2021, equal to the proceeds of the regional share of CVAE in 2020, as compensation for its removal in January 2021. The subsequent transfers will depend on national economic activity. Operating expenditure is expected to grow at an annual average of 1.3% through to 2023. As a result, we expect French regions will maintain a strong operating surplus in 2022-2023 of almost 23% of operating revenue on average, or roughly €6.5 billion.

In 2022, we expect capex to decline, albeit remaining at historically high levels. This reflects the time profile of investment outlays in the new regional mandates (signed in the second half of 2021) in which the execution of the project pipeline will be front-loaded.

Chart 9 | French Regions' Budgetary Performance

We expect French regions will maintain a strong operating surplus in 2022-2023 of almost 23% of operating revenue.

French regions are at the frontline of the economic recovery. They are the layer of government that can launch large-scale investments in rail transportation, road infrastructure, or energy transformation projects. For example, the regions of Occitanie (not rated) and Nouvelle-Aquitaine (not rated) are set to construct a new high-speed railway line between Bordeaux and Toulouse as part of the Major South-Western Railway Project. In the north of France, the region of Hauts-de-France (AA-/Stable/A-1+) will contribute substantially to the construction of a high-capacity canal to expand inland trade flows between the Seine basin and Belgium, Germany, and the Netherlands. We estimate regions' capital revenue to have increased by 26% to €6.6 billion in 2021, and we expect them to remain above €6 billion through 2023, considering the transfers from the central government, including €600 million in investment support and additional EU funds (NextGenerationEU). These significant investment initiatives and their accompanying funds should allow regions to steadily reduce their deficits after capital account and reach a surplus in 2023.

Chart 10 | French Regions' Direct Debt Dynamic

As capex declines and operating balances improve, we expect regions' funding needs to decrease.

As capex declines and operating balances improve, we expect regions' funding needs to decrease. We believe this will lead to a decline in debt stock in 2023.

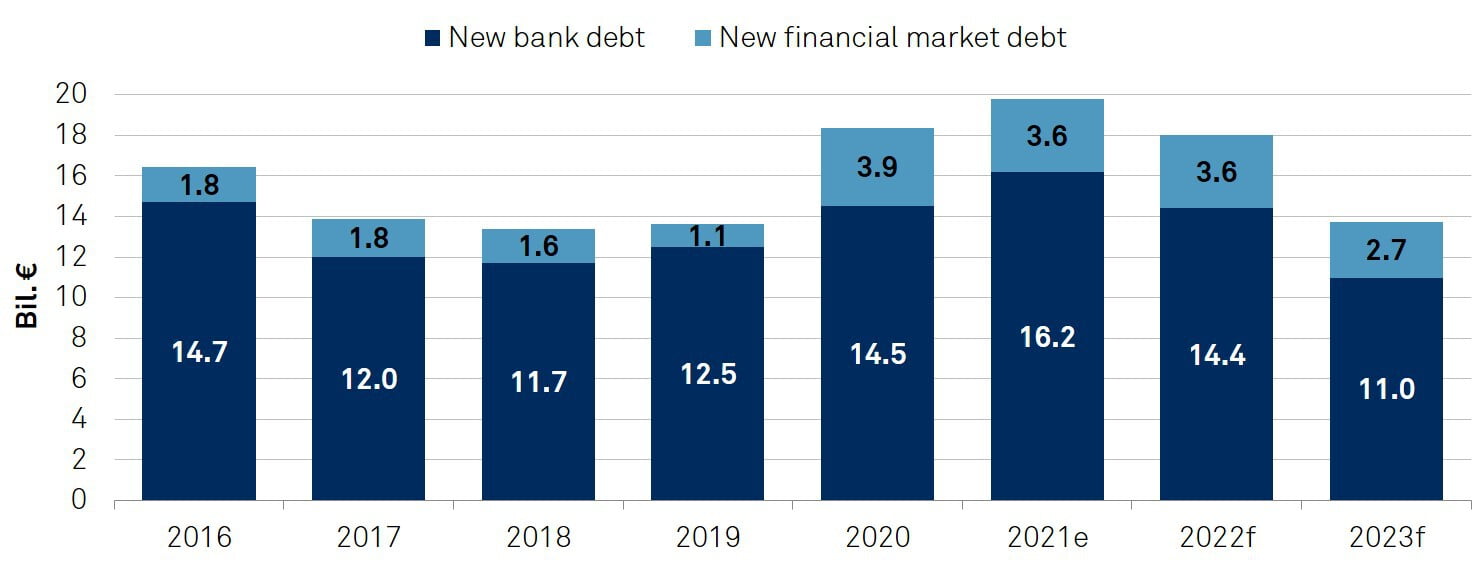

We estimate that French LRGs borrowed €19.8 billion in 2021, 8% more than in 2020, while bond issuance remained a significant proportion (almost one-fifth) of total borrowing. LRGs took a conservative approach in 2021 to ensure they held sufficient short-term liquidity for emergency spending, while increasing issuance maturities to capitalize on the low-interest rate environment. Short-term issuances also grew as LRGs sought to benefit from arbitrage opportunities in the money market. This is reflected in the 6% increase in commercial paper issuances to €36.9 billion in 2021.

Looking ahead, we expect LRGs to continue issuing short-term debt but at a shrinking proportion of total borrowing. We therefore expect substantial recourse to the bond market as a share of total borrowing, with roughly 20% of long-term funding coming from bond issuance in 2022-2023. In addition, a strong presence of public funding from the Caisse des Dépôts et Consignations or the European Investment Bank and lending from commercial banks (mostly French banks together with German banks) will remain at LRGs' disposal.

Funding costs should remain attractive over the three-year forecast horizon, despite the current uncertainty surrounding inflation and therefore benchmark rates, thanks to strong competition between lenders.

Chart 11 | French LRG Borrowing Composition

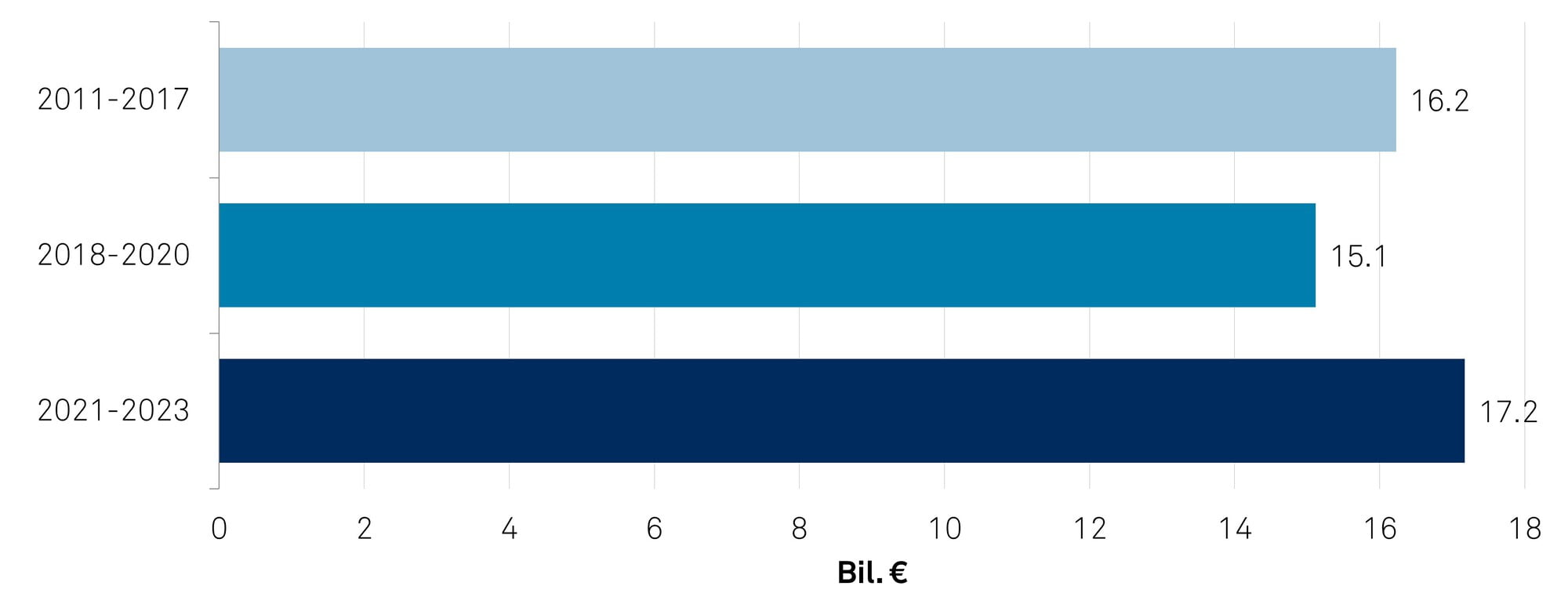

Chart 12 | French LRGs' Annual Average New Borrowing

Sources: French Observatory on Local Public Finances for 2011-2020; S&P Global Ratings estimates for 2021 and forecasts for 2022 and 2023.