This report does not constitute a rating action

Primary Credit Analysts

Susan Chu Hong Kong +852-2912-3055

Local governments' heavy reliance on China's domestic bond markets has created a rising maturity wall in 2022-2023, with about US$1 trillion-equivalent coming due in the two years.

These governments have flexible liquidity options, such as bond issuance and the sale of assets; funding for most regions will be robust.

The volume of maturities may, however, test the liquidity plans of highly indebted local governments in low-income regions.

With about US$1 trillion-equivalent in bonds coming due in 2022-2023, some Chinese local governments may finally be hitting the limits of their liquidity. S&P Global Ratings has long assumed these local and regional governments (LRGs) had ample funds to settle obligations. However, given the sheer volume of debt coming due, we now believe a handful of weaker provinces and municipalities may be stretched to repay maturing bonds. This prompts us to reexamine liquidity data of LRGs, particularly as the data are often opaque and incomplete.

Governments have ramped up issuance since Beijing deregulated this market in 2015. The LRG sector reported borrowings (including refinancing) of Chinese renminbi (RMB) 7.5 trillion (US$1.2 trillion) for 2021, and direct debt stock of RMB30.5 trillion as of end-2021. Chinese LRG debt stock is the second biggest in the world, behind only that of the U.S.

Local governments' heavy bond issuance has created a rising maturity wall, with about US$1 trillion-equivalent coming due in 2022-2023.

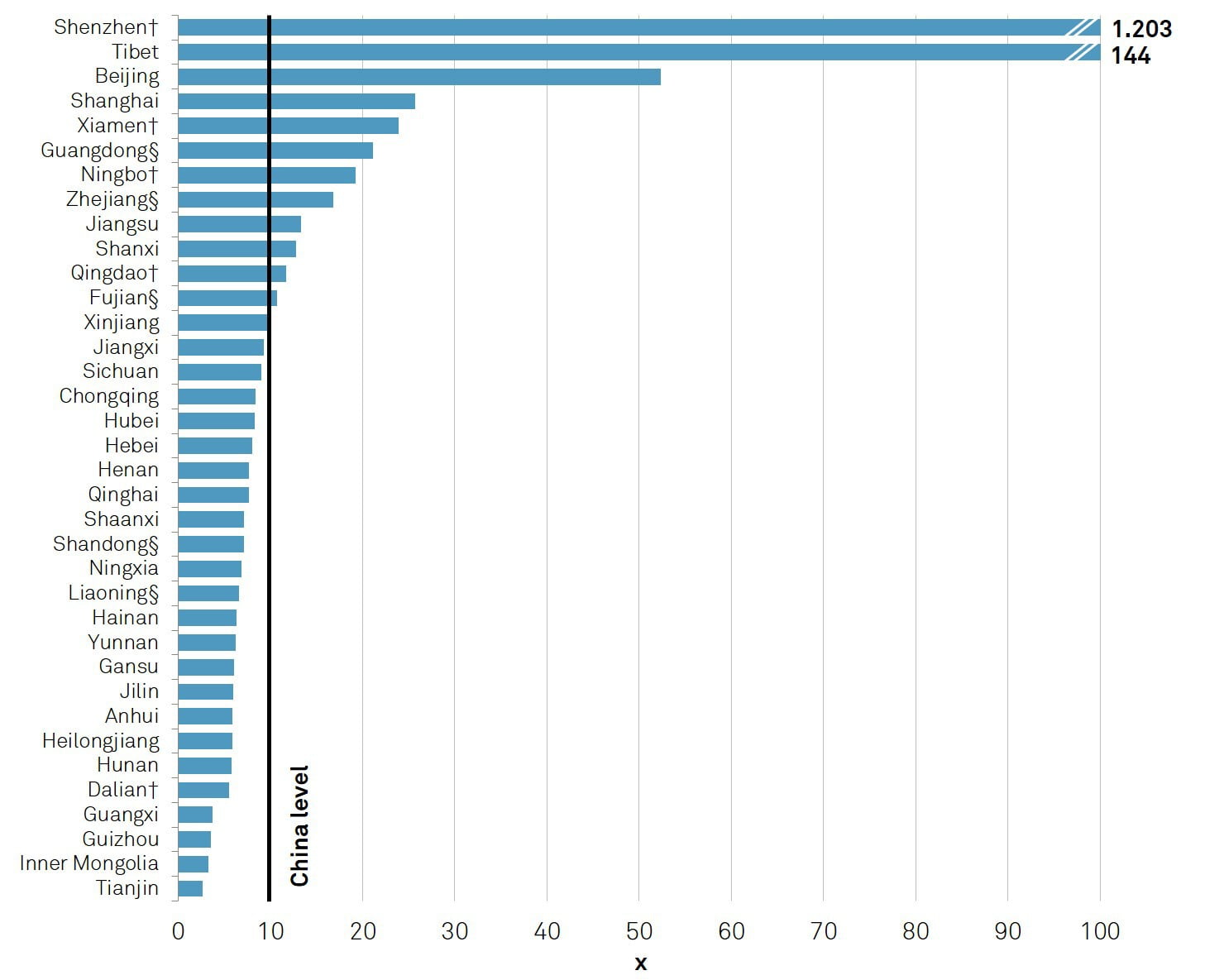

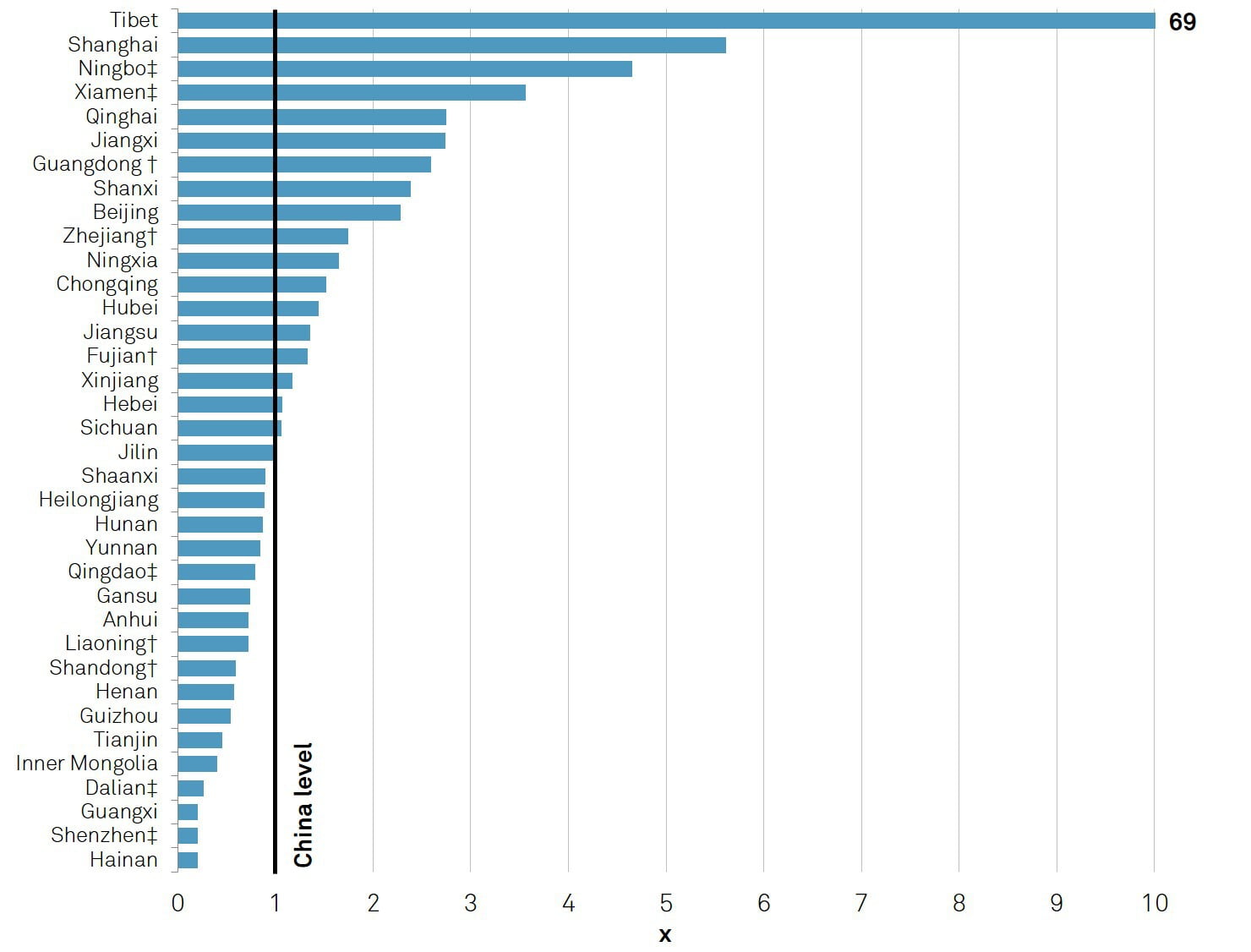

Chart 1 | LRGs Are Diverging Widely In Their Capacity To Repay Debt Total deposits to LRG debt*

*LRG debt maturing in 2023 relative to total deposits as of 2021 year-end, in respective regions. §Data do not include respective cities under state planning. †Cities under state planning. LRG--Local and regional government. Sources: Wind, local governments' fiscal reports, S&P Global Ratings.

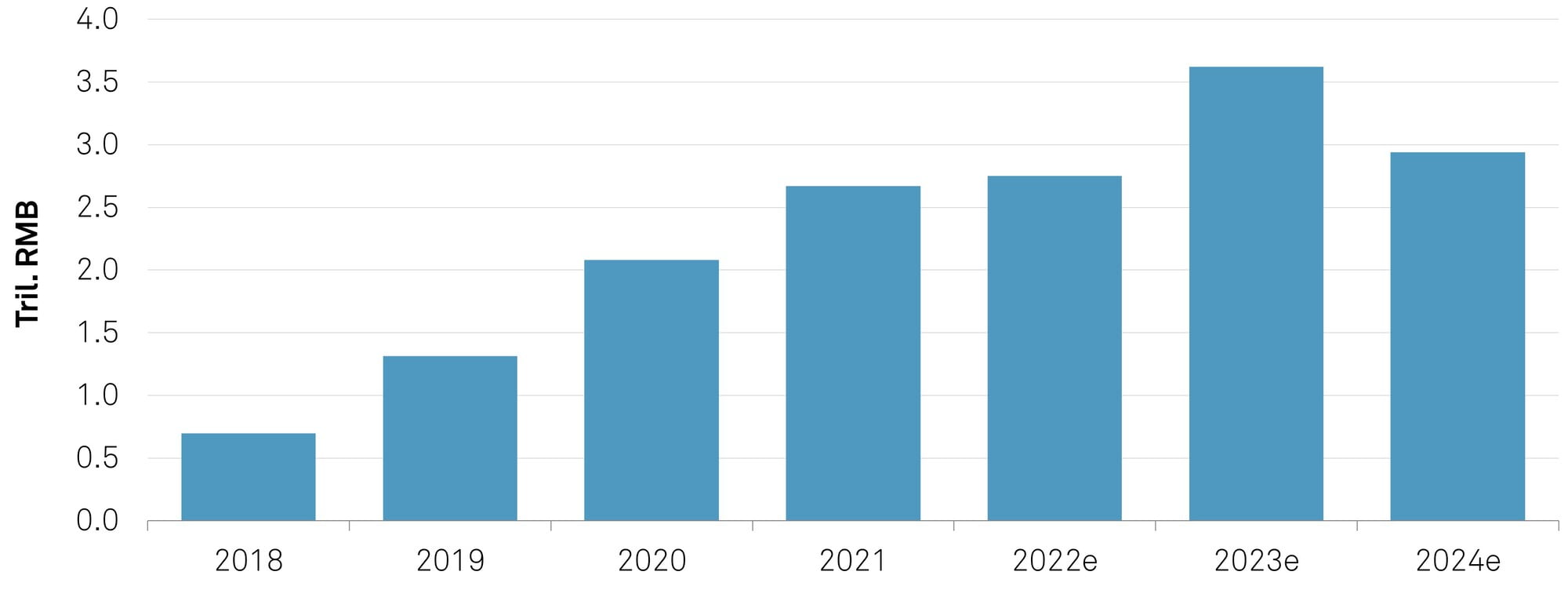

The debt repayment obligations of most Chinese LRGs will likely peak in 2022 and 2023 (see chart 2). Chinese LRGs, meanwhile, are not transparent about the state of their balance sheets. They disclose limited data on their cash and liquid assets, and their statements do not follow international standards. Investors find it difficult to identify the controllable liquid resources that LRGs can use for debt repayment, for example. Chinese LRGs also do not use accrual standards in their financial accounting, which further hinders the scrutiny of investors.

Chart 2 | A Maturity Wall Looms For China LRGs Amount coming due each year

LRGs--Local and regional governments. RMB--Chinese renminbi. Tril.--Trillion. e--Estimate. Source: National Bureau of Statistics of China, Ministry of Finance, S&P Global Ratings.

In the absence of concrete data, we use estimates and proxy data to create a liquidity profile of Chinese LRGs. We believe the overwhelming majority of these governments have sufficient resources to support daily operations and debt repayment for the next two years and beyond. Some highly indebted regions, however, may need to roll over a large part of their debt in this maturity-heavy period.

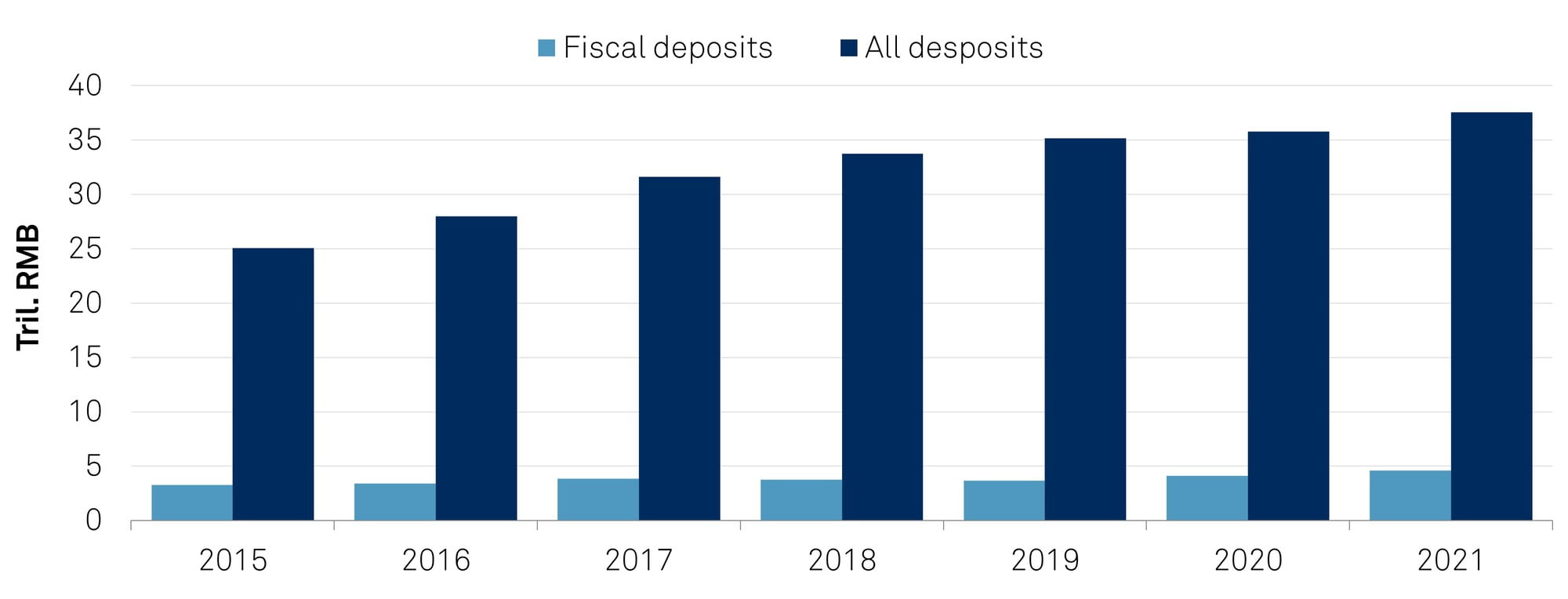

Most provincial LRGs regularly release deposit data. The figures encompass fiscal deposits and all deposits. Fiscal deposits are cash reserves used to meet LRGs' coming fiscal activities. All deposits further incorporate deposits under government institutions--usually nongovernment divisions. The divisions include institutions that perform public services, such as government-sponsored funds and schools.

LRGs likely have a high level of control over most deposits in their regions, even if some of the cash is not immediately accessible. In our view, these deposits will grow as their economies expand (see chart 3). We estimate fiscal deposits at an aggregate level was RMB4.6 trillion as of end-2021, and that of all deposits at RMB37.6 trillion. In contrast, RMB2.8 trillion of LRG debt will mature in 2022, and RMB3.6 trillion will come due in 2023, by our calculations.

Chart 3 | Most Local Governments Control Sizable Deposits

Note: Data encompasses all regions, except for Hainan, Shenzhen and Jilin. Tril.--Trillion. RMB--Chinese renminbi. Source: Local governments' work reports, S&P Global Ratings.

LRGs rely heavily on the domestic bond market. The LRG sector accounts for about one-quarter of China's onshore bond market, one of the largest capital markets in the world. Investors typically oversubscribe to new offers of LRG bonds. This strong demand means most LRGs can easily roll over their bonds upon maturity.

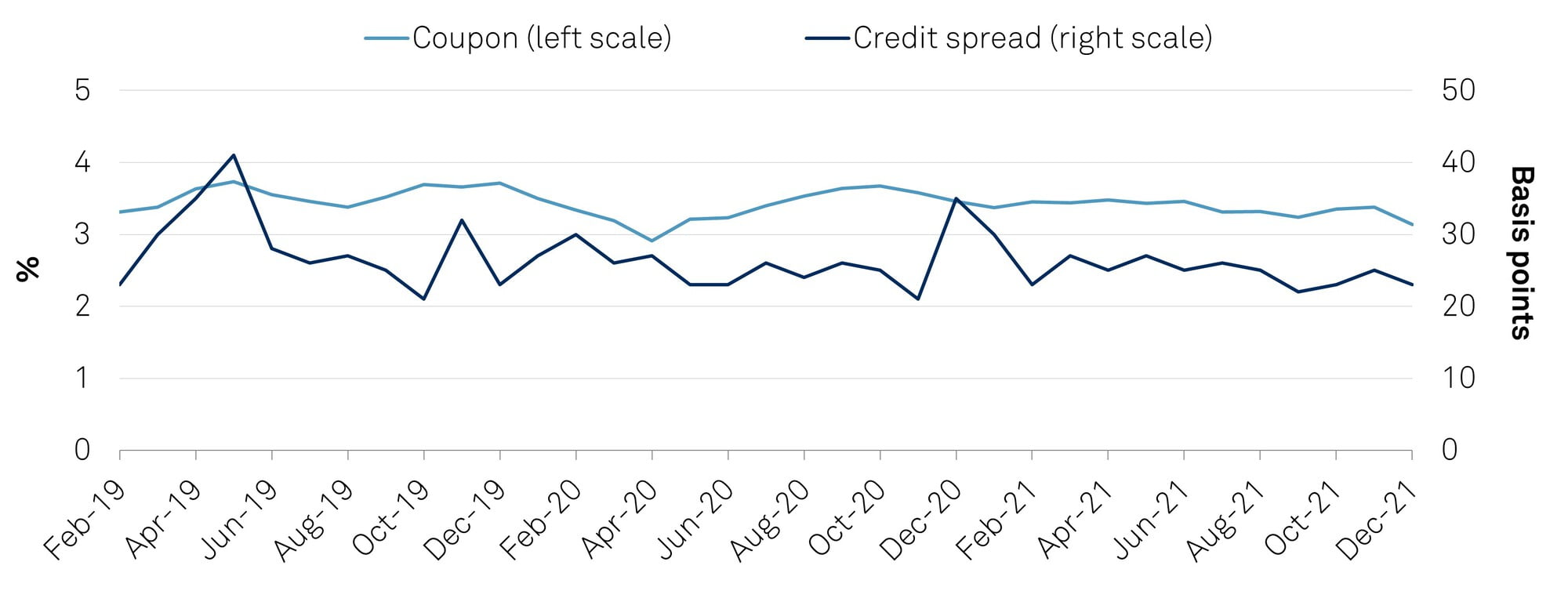

LRGs also consistently issue bonds at low coupon rates and low credit spreads (see chart 4). The credit spreads on 10-year LRG bonds have typically held at 20-30 basis points wide of the 10-year sovereign bond. This was true even during the worst of China's COVID-19 outbreak, in the first half of 2020.

Chart 4 | Onshore Bond Market Remains Receptive To Local Government Bonds Weighted averages on newly issued 10-year LRG bonds

Note: Coupon rates are the weighted average of interest rates of new issues by LRGs; credit spreads are the average spread of newly issued 10-year LRG bonds over 10-year government bonds. LRG--Local and regional government. Source: Ministry of Finance, S&P Global Ratings.

Commercial banks usually hold more than 80% of a given LRG issue. Banks controlled by the central government are main buyers of LRG bonds. This includes policy banks and state-run lenders. This suggests the central government is ready to support an LRG in a liquidity crunch.

SOEs can support LRGs in stress scenarios. LRGs' control of sizable state-owned enterprises (SOEs) is a two-edged sword. SOEs add to regions' debt burden. The governments may need to support stressed SOEs and, indeed, most of our discussion of LRG debt in the past has focused on this scenario. However, some well-run and commercially focused SOEs can provide stable cash dividends to their LRG owners. If LRGs experience their own liquidity crunch, the SOEs are also valuable assets that can be sold, if needed.

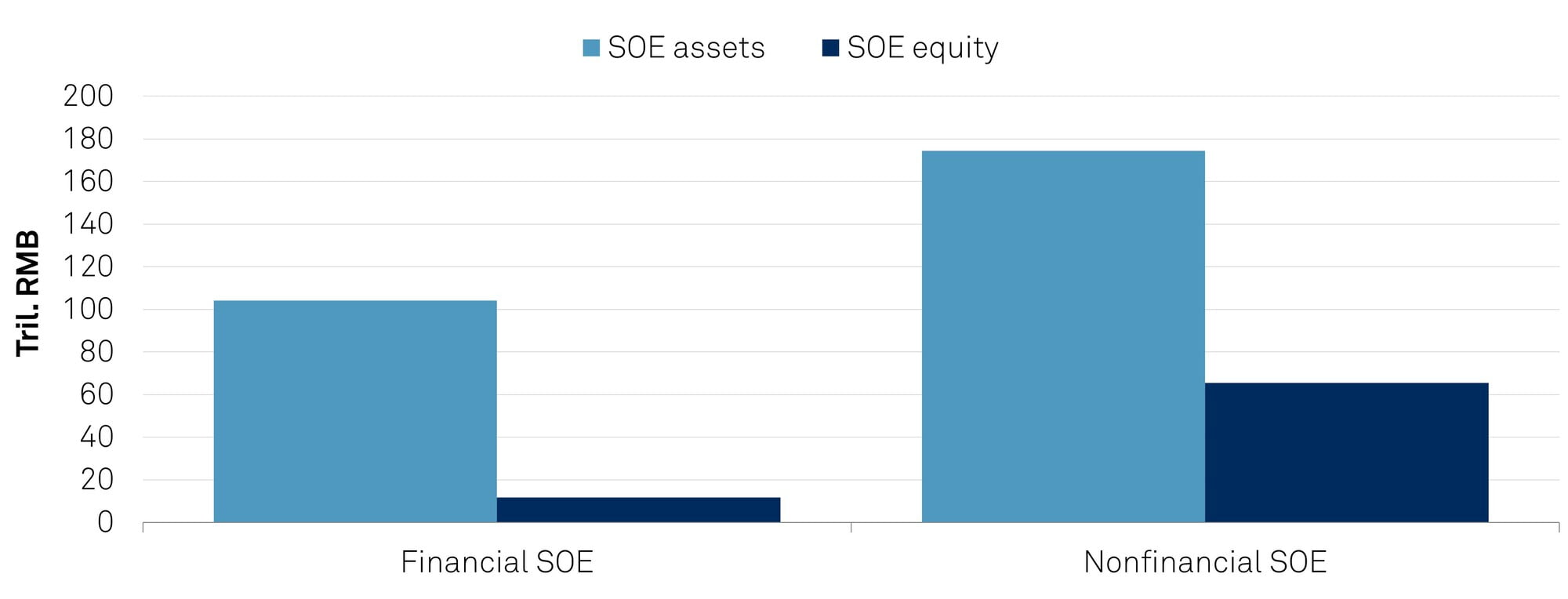

SOEs controlled by LRGs are growing bigger. The entities' aggregated assets were worth RMB279 trillion, as of end-2020, and the equity value was RMB77 trillion (see chart 5). Some SOEs are locally listed, and we estimate these firms have an aggregated market capitalization of RMB18 trillion. In addition, many LRGs control valuable assets, such as land banks and franchise licensing rights.

LRGs are unlikely to embark on a mass monetization of their most valuable assets, given the governments often view the holdings as strategic. However, we believe these assets would give LRGs a buffer to carry them through a liquidity crunch.

Chart 5 | LRGs Control Sizable SOEs That Could Be Monetized To Repay Debt

Note: Estimates accounted for SOEs controlled by local governments. LRG--Local and regional government. Tril.--Trillion. RMB--Chinese renminbi. SOE—State-owned enterprise. Source: State Council, S&P Global Ratings.

Our research indicates that desposit growth trends across LRGs are diverging. Most LRGs aim to expand new borrowings, and roll over bonds upon maturity even as Beijing tightens discipline on LRG balance sheets.

Central authorities are likely homing in on the ratio of debt stock of LRGs over LRG revenues. This ratio rose to around 100% at 2021 year-end by our esimate. About one-quarter of governments are likely to report that this ratio was above 120% at end-2021, and some may find it difficult to sustain their cash position through new borrowings. The central government controls the volume of bonds that LRGs can issue, and has slashed this quota for highly indebted governments in the past two years.

When looking at the credit standing of LRGs, we consider the volume of debt maturing in a given 12 months, along with key metrics. We generally view low-income LRGs as being more reliant on external funding, particularly bond markets. Such governments (often in western or northern China) have weak internal cash generation and limited ownership of valuable assets that could be sold during a cash crunch. The upshot is that some of these more highly indebted LRGs may be heading for a liquidity squeeze, particularly if the central government limits their access to bond markets.

Chart 6 | Local Governments Raise Debt To Increase Deposits

Note: Estimates accounted for SOEs controlled by local governments. †Data do not include respective cities under state planning. ‡Cities under state planning. LRG--Local and regional government. Tril.--Trillion. RMB--Chinese renminbi. SOE—State-owned enterprise. Source: State Council, S&P Global Ratings.

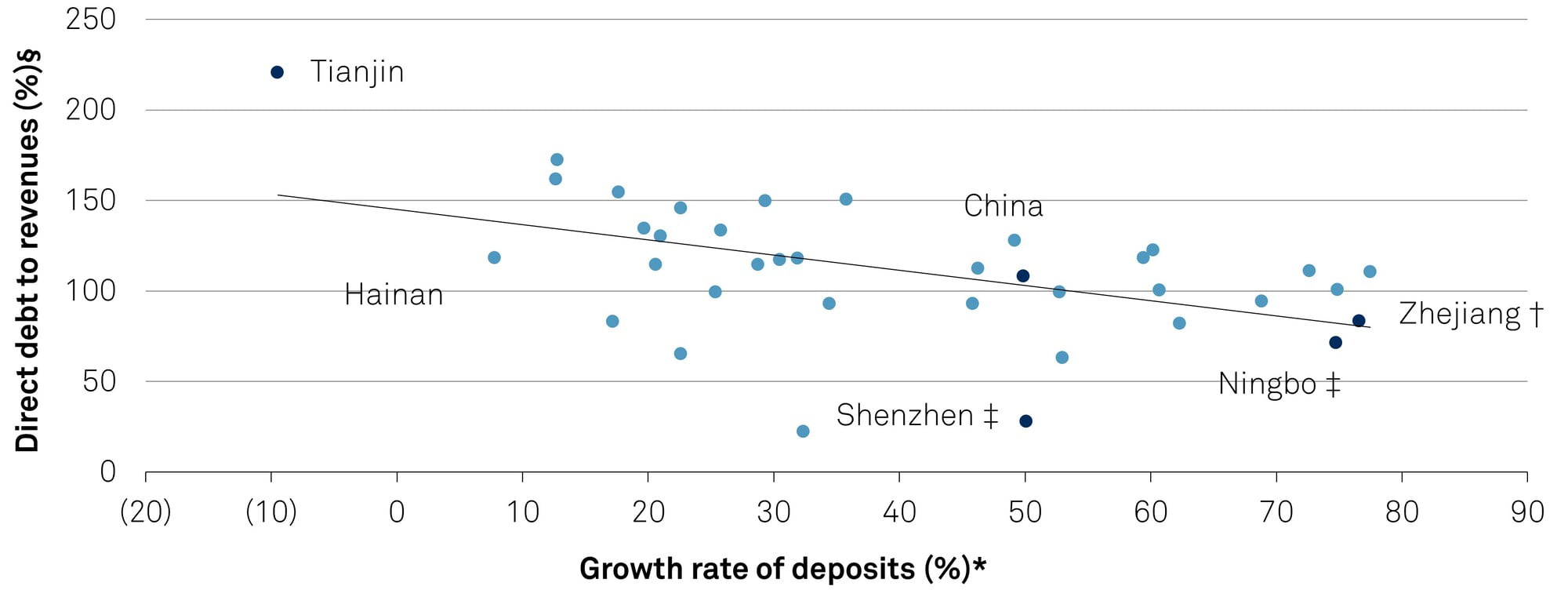

Chart 7 | The Weaker LRGs May Experience Liquidity Strains As Bonds Come Due Final deposits to LRG debt*

*LRG debt maturing in 2023 relative to fiscal deposits as of 2021 year-end, in respective regions. †Data do not include respective cities under state planning. ‡Cities under state planning. LRG--Local and regional government. N.A.--Not available. Sources: Wind, local governments' fiscal reports, S&P Global Ratings.

Secondary Contacts

Felix Ejgel London +44-20-7176-6780

Research Assistant

Yunbang Xu Hong Kong