This report does not constitute a rating action

Primary Credit Analysts

Bhavini Patel Toronto +1-416-507-2558

Stronger economic recovery at the provincial level and improved fiscal outcomes will temper projected borrowing by Canadian local and regional governments (LRGs) in fiscal 2022 and, to a lesser degree, in 2023.

S&P Global Ratings expects that total provincial and municipal debt will increase by about 7% in fiscal 2023, reaching about C$1.25 trillion by the end of the next fiscal year.

Borrowing will primarily fund the refinancing of maturing debt, capital investment, and operating deficits.

Debt issuance will remain bond-based, dominated by fixed-rate provincial bonds issued in the domestic market.

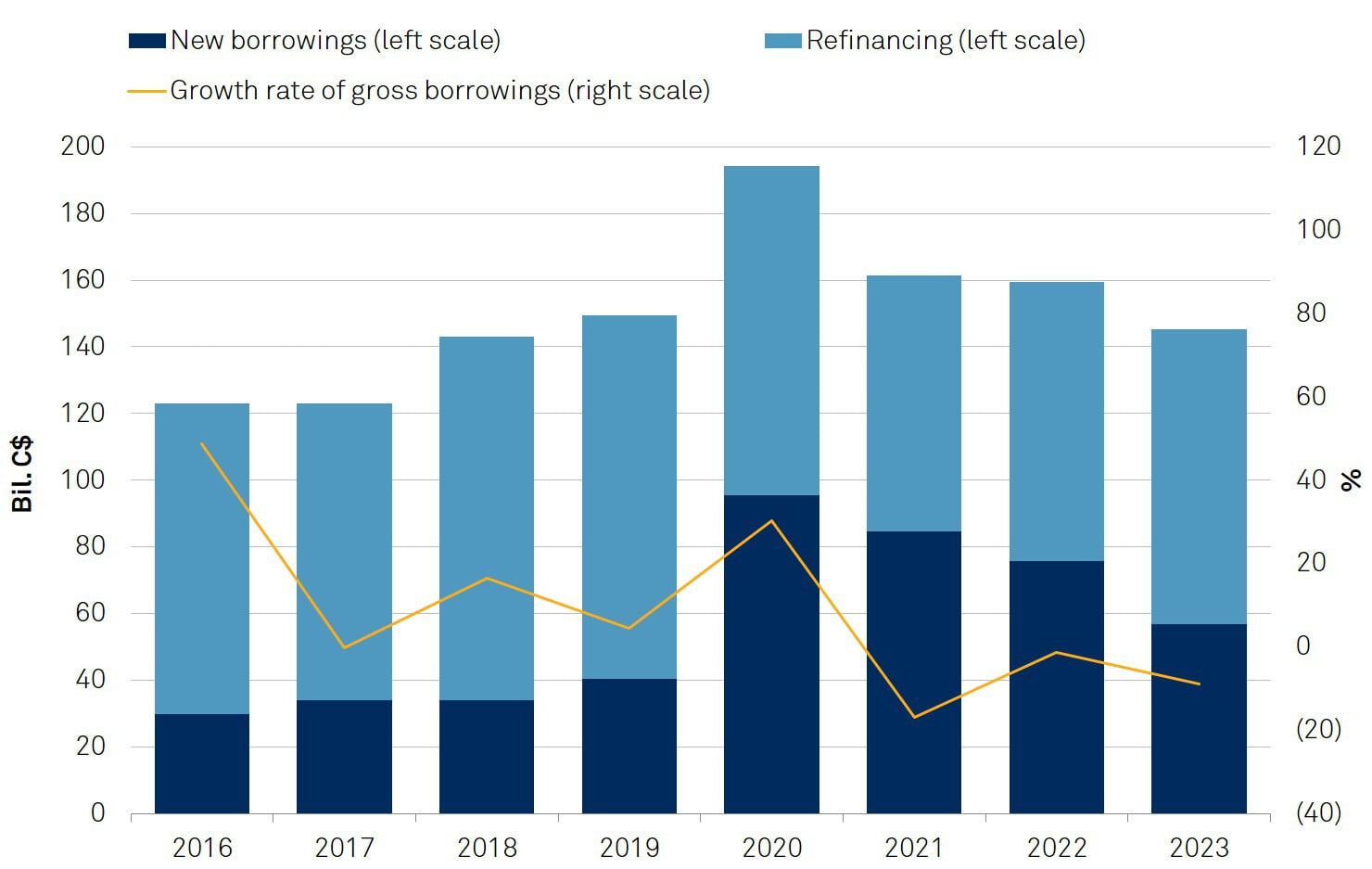

We expect that Canada will continue to experience above-average growth of 3.7% in 2022, following the significant recovery of 4.6% expected in 2021 (see “Economic Outlook Canada Q2 2022: Growth Forecasts Hold Up As Global Risks Rise,” published March 28, 2022, on RatingsDirect). Provincial growth projections typically converge toward the national level and, as a result, we believe that the economic recovery for most provinces will follow the same trajectory. With the rising price of oil, gas, and other commodities, provinces with a concentration in energy and other commodities will see stronger growth than peers. As a result, higher-than-expected tax and resource-related revenues and relatively modest expenditure increases will spur improvement in operating and after-capital deficits and temper growth in total LRG debt in the next two years. In fiscal 2022, we expect provincial and municipal gross borrowing will total almost C$161 billion, which is about 20% lower than last year’s borrowings. Net borrowing (gross borrowing less refinancing) will be about C$77 billion, also substantially lower on a year-over-year basis (see chart 1). Of note, based on midyear provincial fiscal updates, which factor in stronger economic recoveries and better budgetary performance, we expect that borrowings will decline more than initially expected, from the elevated levels recorded in fiscal 2021. Considering a more moderate pace of issuance in the next two years, we expect total debt will reach approximately C$1.25 trillion by the end of fiscal 2023.

Chart 1 | Borrowings, 2016-2023

Source: S&P Global Ratings.

S&P Global Ratings expects gross borrowing and the increase in total debt will moderate somewhat in fiscal 2022 as high vaccination rates help to lower severe outcomes and health and safety measures are lifted. Nevertheless, Canadian LRGs remain among the largest issuers globally. We project that total LRG debt could represent about 42% of Canada’s GDP in 2022, which is significantly higher than that of other federal nations, such as Australia or Germany.

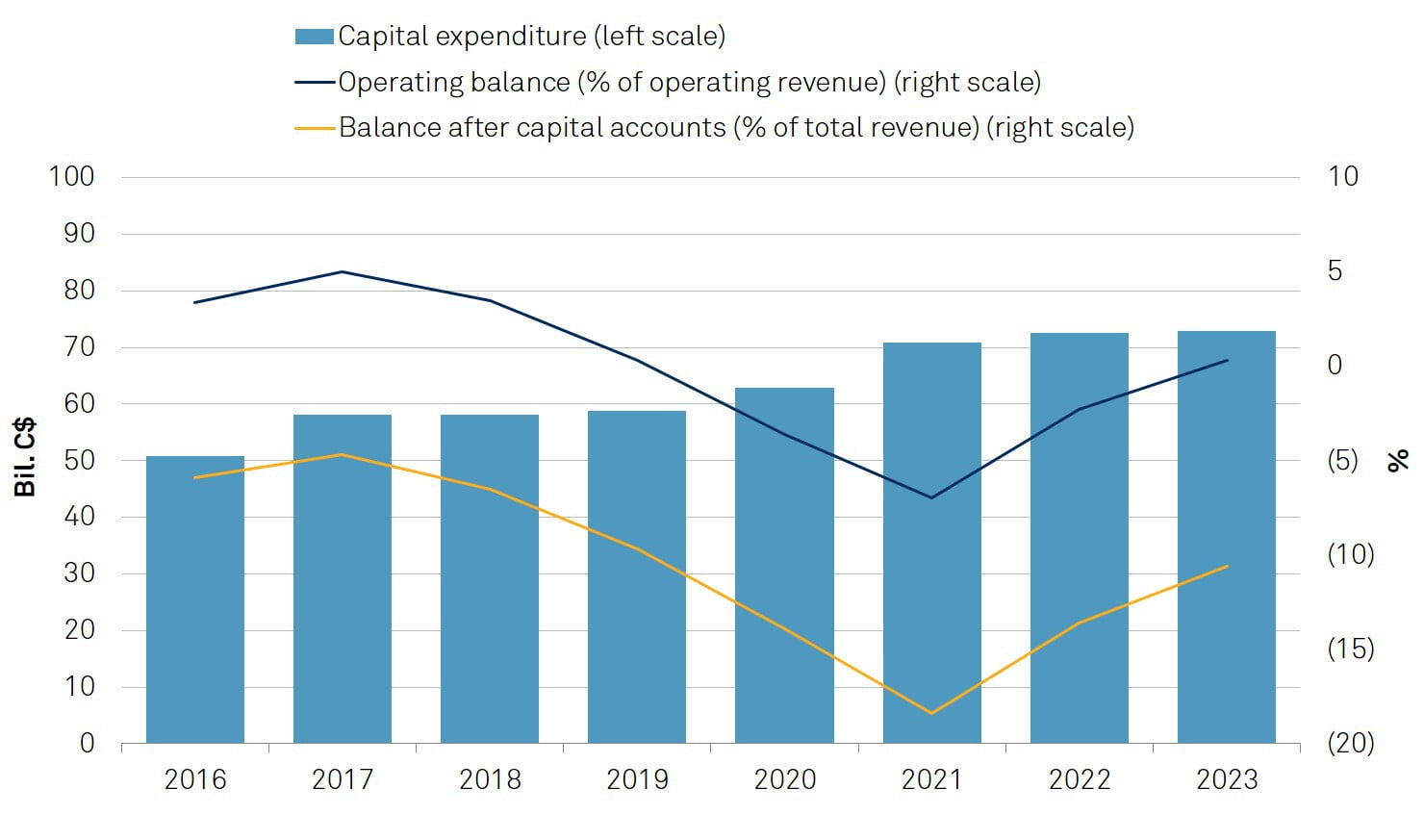

While the pandemic’s effects were felt on both sides of provincial and municipal income statements, the impact on provinces has been greater than on municipalities, and will take more time to unwind. Generally, measures to control the spread of the coronavirus lowered the own-source revenues of both provinces and municipalities but those losses were moderated by ad hoc transfers from senior levels of government, primarily through direct support (government to government) and indirectly through support to individuals and businesses. Nevertheless, the pandemic’s effects on budgetary results will linger for many LRGs (see chart 2). Although smaller than initially projected, provincial operating deficits, and after-capital deficits for all Canadian LRGs, will lead to moderate increases in gross borrowings and total debt.

Higher-than-expected tax and resource-related revenues and relatively modest expenditure increases will spur improvement in operating and after-capital deficits and temper growth in total Canadian LRG debt in the next two years.

The overwhelming majority of Canadian LRG borrowing is through public bond markets, largely domestic, and mostly at fixed rates. Private placement financing is typically only a small and infrequent component of total bond market financing, although notably, for some provinces, private placements were the first bonds issued at the onset of the pandemic. Bank lending is minimal. We don't expect any significant change in the sources of funding in the next two years.

Chart 2 | Capital Expenditures And Fiscal Balances, 2016-2023

At more than 90% of total debt, provincial debt dominates. Canadian provinces are not bound to any fiscal framework by the federal government, which is in line with our institutional framework assessment of ‘2’ for all provinces (see “Public Finance System: Canadian Provinces,” May 12, 2020). Notably, provincial service-delivery responsibilities, such as health care and education, are significantly more onerous than those of municipalities and, not surprisingly as a result, provincial debt stocks are larger and have risen faster than those of the municipalities.

Borrowing by Canadian LRGs will primarily fund the refinancing of maturing debt, capital investment, and operating deficits at the provincial level.

Provinces impose fiscal frameworks on municipalities through their respective Municipal Acts. Legislation requires that municipalities balance their operations and issue debt only for capital purposes, the bulk of which is allocated to infrastructure. In addition, debt at the municipal level is typically amortizing. As a result, Canadian municipalities’ debt burdens are generally much lower than those of the provinces. Nevertheless, this is less so for some fast-growing municipalities that have substantial capital-intensive local infrastructure responsibilities, such as water, sewer, and transit networks. Notably, only one municipality, Montreal, is among the top 10 most indebted Canadian LRGs.

Twin economic and fiscal shocks, such as the 2008 financial crisis, the fall in the price of oil in 2014-2015, and the COVID-19 pandemic, have pushed up most provincial debt burdens over the long term. In addition, for some provincial governments with electric utilities, historically large investments in new generation capacity have further increased their debt burdens. Municipal revenues and expenditures, on the other hand, are more insulated from economic shocks.

In the next two years, we expect that municipal budgetary performances will, generally, remain strong and that any increase in municipal borrowing requirements and debt burdens will be moderate. We also expect that, compared with 2021 levels, the borrowing requirements of the provinces will fall in the current fiscal year and then moderate as provincial economies recover, and that budgetary performance improves and financial management remains focused on fiscal sustainability. We also expect that the borrowing needs of the four largest provinces, Alberta, British Columbia, Ontario, and Quebec, will continue to dominate Canadian LRG borrowing.

The overwhelming majority of Canadian LRG borrowing is through public bond markets, largely domestic, and mostly at fixed rates.

Secondary Contacts

Stephen Ogilvie Toronto +1-416-507-2524

Adam J Gillespie Toronto +1-416-507-2565

Dina Shillis Toronto +1-416-507-3214

Additional Contact

Claudia Piron New York