This report does not constitute a rating action

Primary Credit Analysts

Martin J Foo Melbourne +61-3-9631-2016

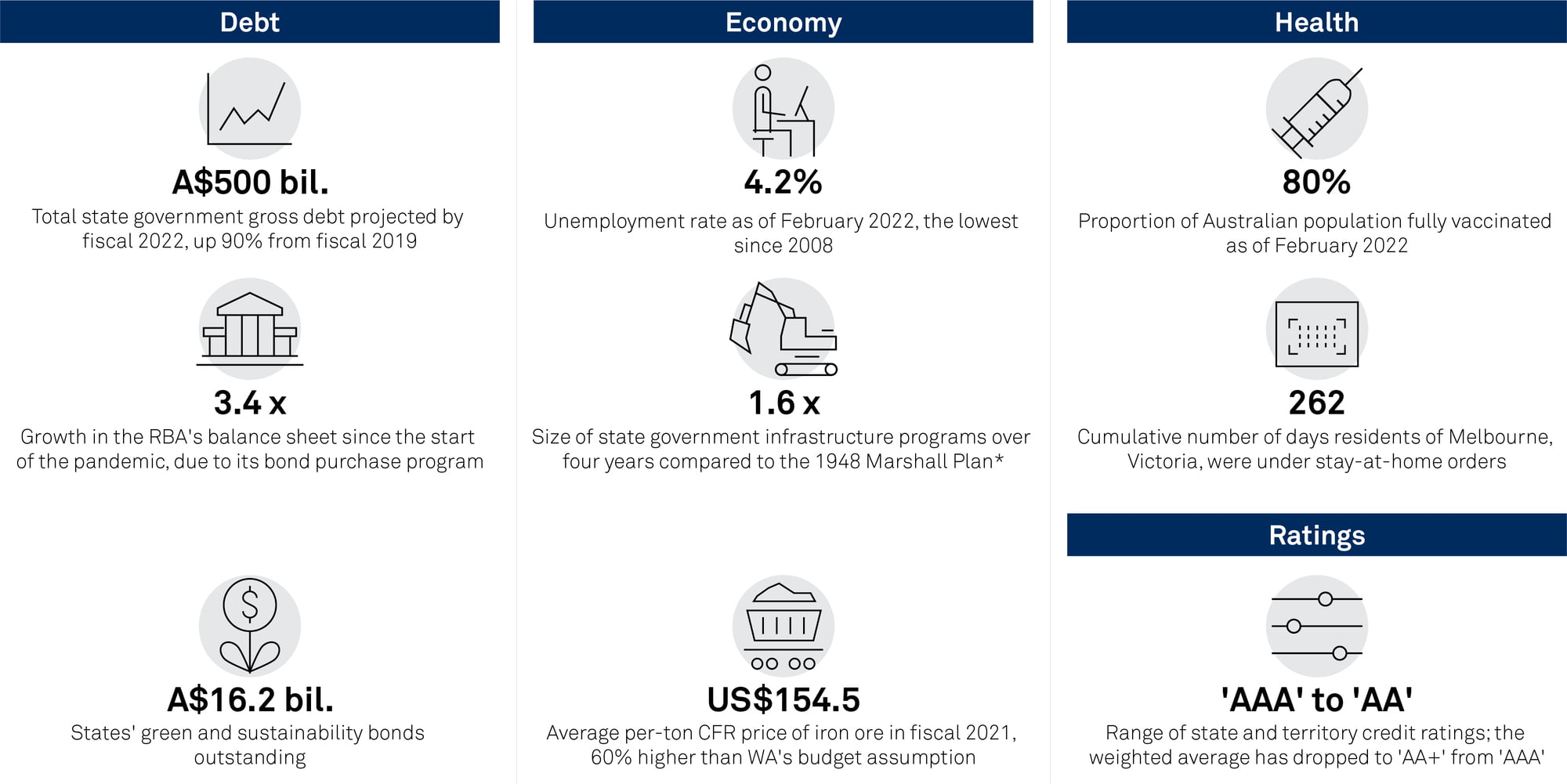

Total Australian state government debt is on track to pass A$500 billion (about US$360 billion), or 23% of GDP, in 2022.

As tax revenues and pandemic-related emergency spending normalize, new borrowing will still be needed to finance historically large infrastructure programs.

Credit trends are diverging: Victoria and New South Wales will record the largest increases, while Western Australia's debt is steady.

In a matter of months, Australia's combined state government debt will exceed half a trillion dollars. That's US$360 billion, or 23% of GDP, in 2022. It is yet another extraordinary statistic to pile on the tumult of the past two years. Indeed, every passing month of the pandemic has spawned a dizzying new superlative: the lowest cash rate ever; the highest iron ore price; the widest state election victory margin; the largest federal deficit since World War II; the deepest downturn since the Great Depression.

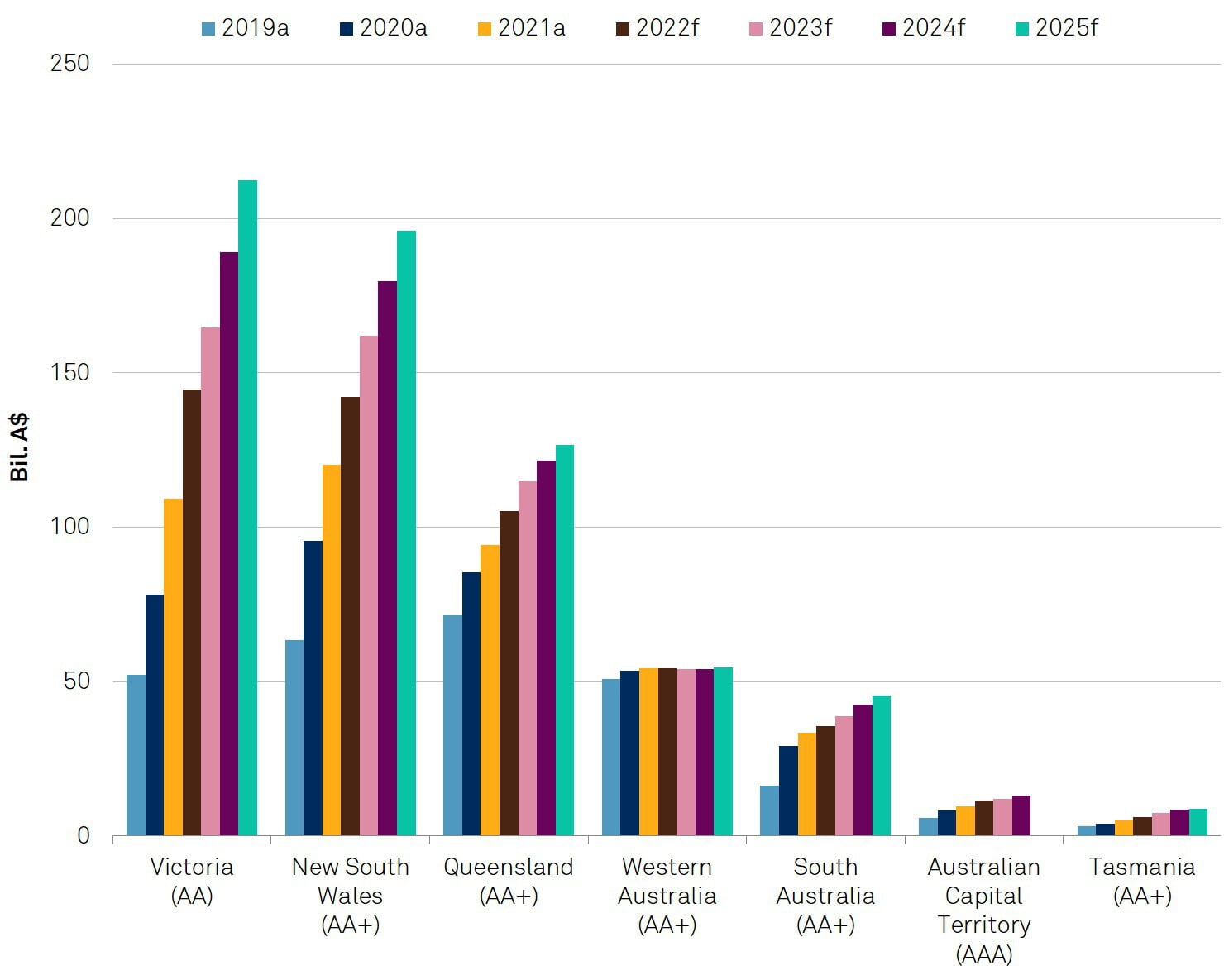

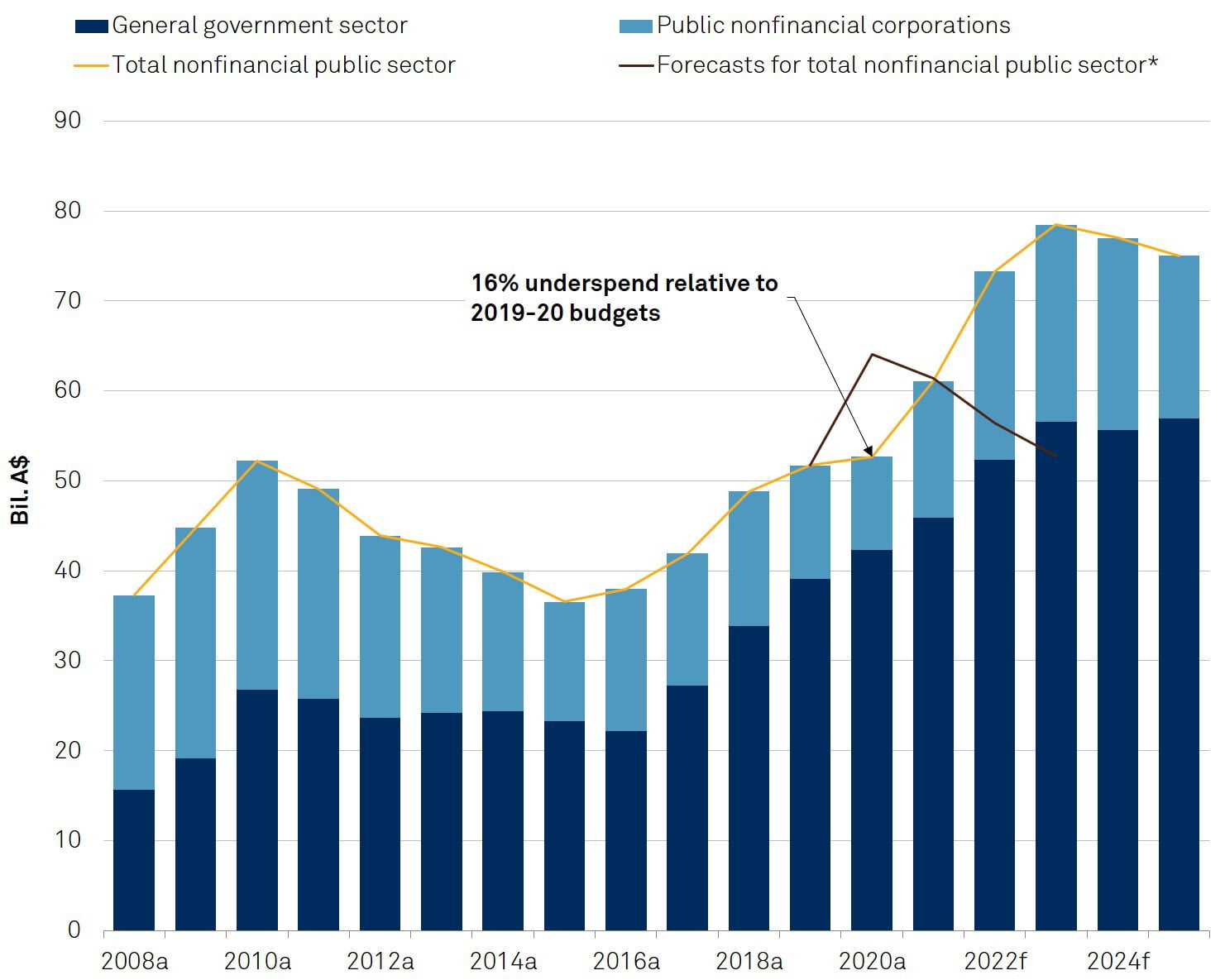

We expect the debt burdens of most Australian states to rise (chart 1) as they grapple with the aftershocks of the pandemic and ramp up infrastructure investment. Aggregate gross debt is budgeted to reach exactly A$500 billion by the end of fiscal 2022 (June 30, 2022). While chart 1 tallies projections from each state's most recent budget update, under-delivery of capital works may mean the half-trillion-dollar milestone will occur a little later, perhaps by the end of the calendar year.

This report encompasses the seven states rated by S&P Global Ratings (see table 1). Together, these rated entities account for 98.7% of Australia's GDP. We exclude the unrated Northern Territory.

We forecast that the southeastern states of Victoria and New South Wales will have the greatest borrowing needs. This was an important factor behind our rating actions on both states in December 2020 (see "Credit FAQ: Why We Downgraded The Australian States Of New South Wales And Victoria," published Dec. 7, 2020).

Two Years Of Extraordinary Numbers In Australia

*Adjusted for inflation. RBA--Reserve Bank of Australia. CFR--Inclusive of cost and freight. WA--Western Australia. Bil.--Billion. Fiscal year ends June 30. Source: S&P Global Ratings.

Chart 1 | Public Debt Is Rising Steeply Across Several Australian States Gross debt, nonfinancial public sector

a--Actual. f--Forecast. Forecasts are from state budgets and may differ from our own base-case scenarios. Fiscal year ends June 30. Source: Most recent state budget updates and annual reports.

Table 1 | Australian States Are Highly Rated

Source: S&P Global Ratings.

Australian state government debt is on track to pass A$500 billion, or 23% of GDP, in 2022.

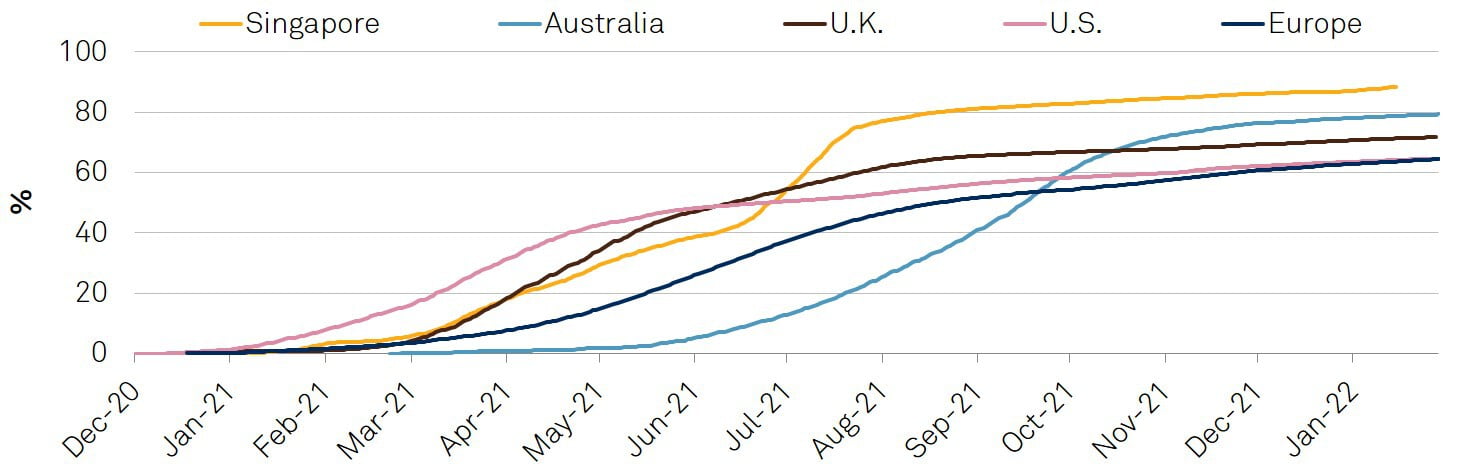

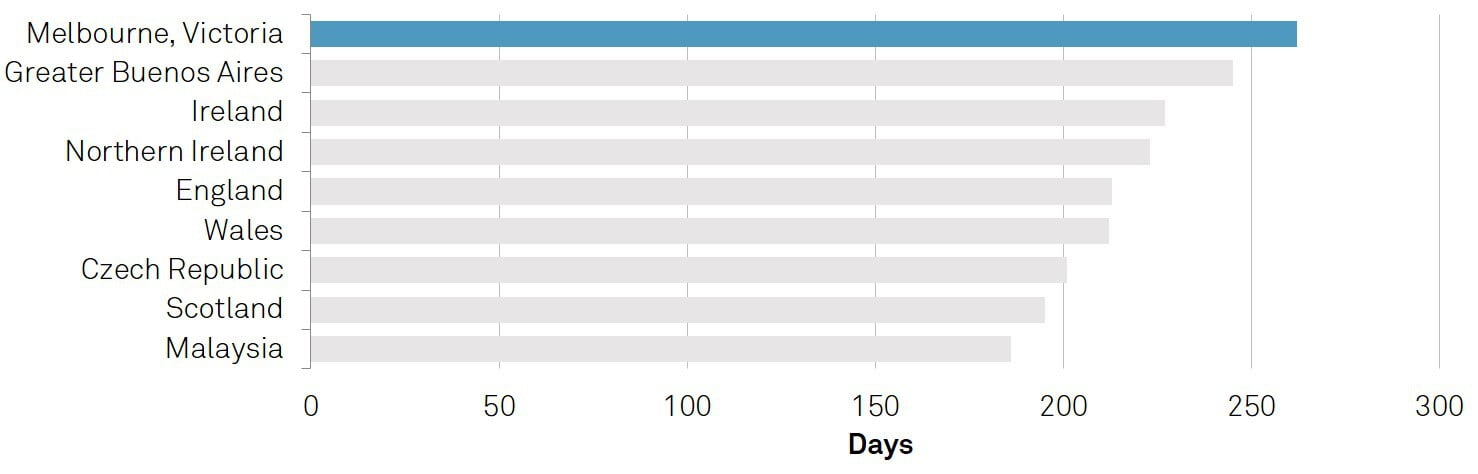

Most conspicuously, Victoria's gross debt is set to quadruple between fiscal years 2019 and 2025. Victoria bore the brunt of a second wave of infections in the latter half of 2020. With vaccines slow to roll out (chart 2), its capital Melbourne has faced some of the world's longest and strictest confinement orders (chart 3), to the detriment of its services-oriented economy. An impressive nationwide economic rebound in 2021 then endured the arrival of the delta variant and a new round of public health restrictions, principally affecting New South Wales, Victoria, and Australian Capital Territory.

Australia's federal and state governments rolled out a series of massive support packages to help keep businesses and households afloat (chart 4). Relative to GDP, the combined fiscal response has been one of the world's largest. The risk now is that pandemic budgets become election budgets. (Three states go to the polls in the next 12 months.) We will closely monitor whether states bake in recurrent spending under the guise of temporary stimulus. Doing so could have negative implications for ratings.

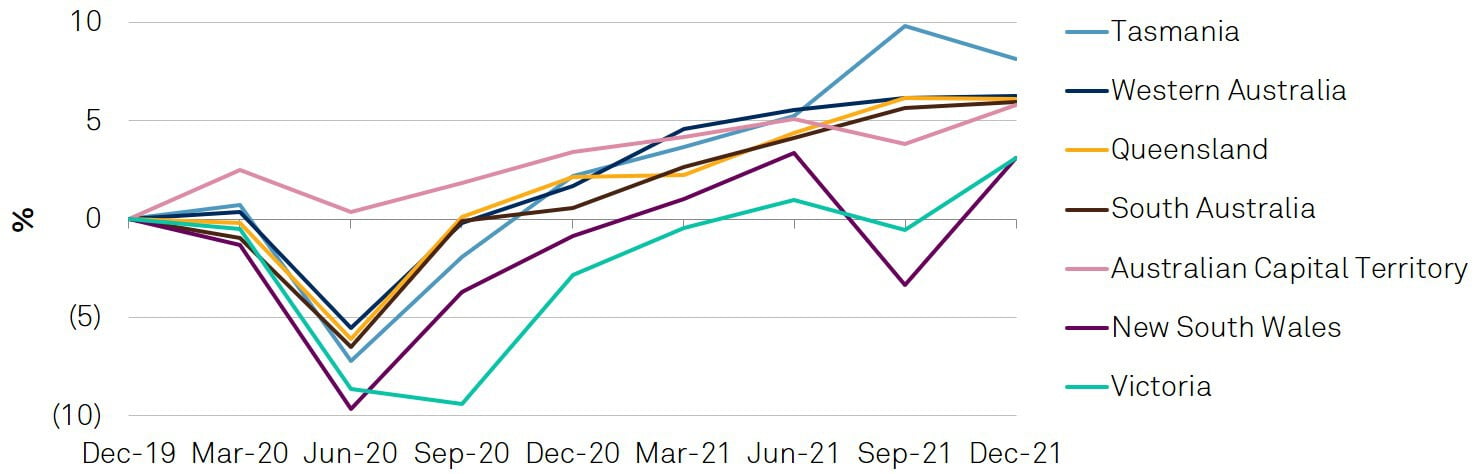

As the current omicron wave crests, we expect states' taxation bases to benefit from a tight labor market (chart 5), buoyant property sector (chart 6), and elevated, albeit volatile, commodity export prices. The upturn remains imbalanced, though. Lockdowns in the September 2021 quarter severely dented private demand in New South Wales and Victoria, resulting in a two-speed recovery (chart 7). And as interest rate liftoff looms, the property market faces some risk of correction. Any significant fall in transaction volumes or prices would hurt stamp duty collections, one of the states' main revenue lines.

Chart 2 | After A Belated Start, Vaccination Coverage Is Now High Share of population fully vaccinated against COVID-19

Source: Our World In Data.

Chart 3 | Melbourne Locked Down Six Times To Slow The Spread Selected areas with longest cumulative lockdowns*

*As of Oct. 21, 2021. Numbers are not perfectly comparable because different countries have differing definitions. Sources: Statista, 7 News.

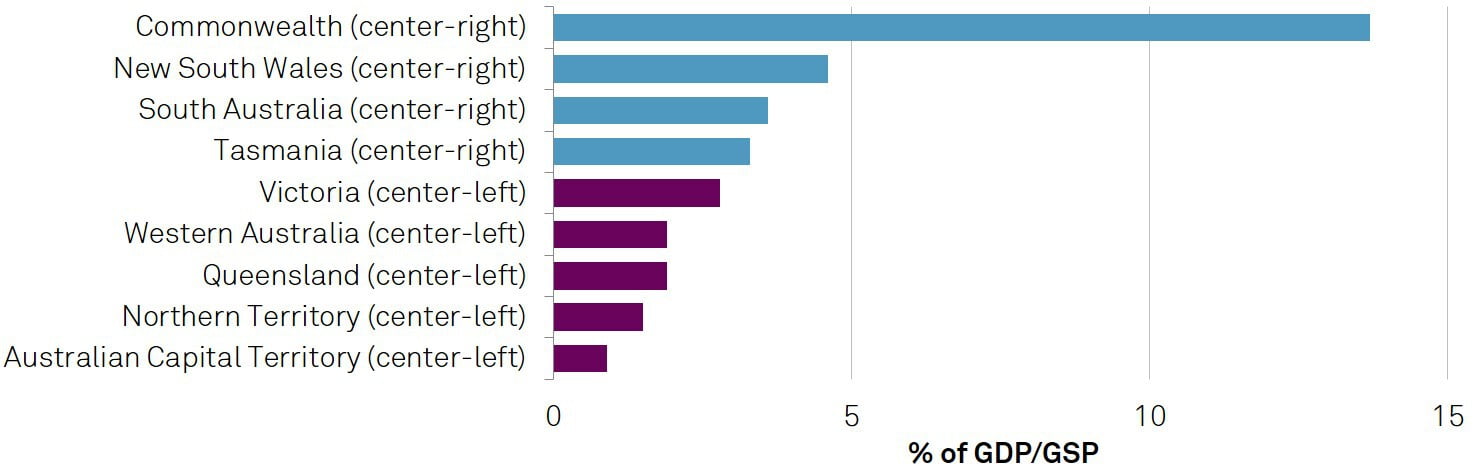

Chart 4 | Conservative Governments Spent Most Liberally Health and economic support packages announced*

*As of March 2021. GSP--Gross State Product. Source: Parliamentary Budget Office.

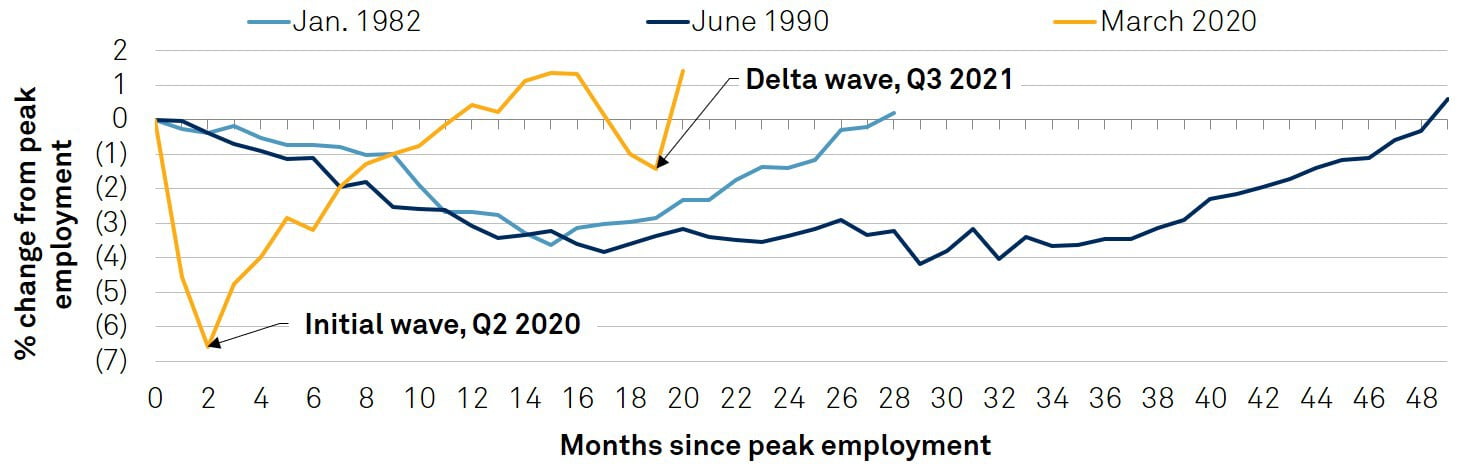

Chart 5 | The Labor Market Resurgence Is A Bright Spot % fall in employment compared to past recessions

Data are seasonally adjusted. Source: Australian Bureau of Statistics.

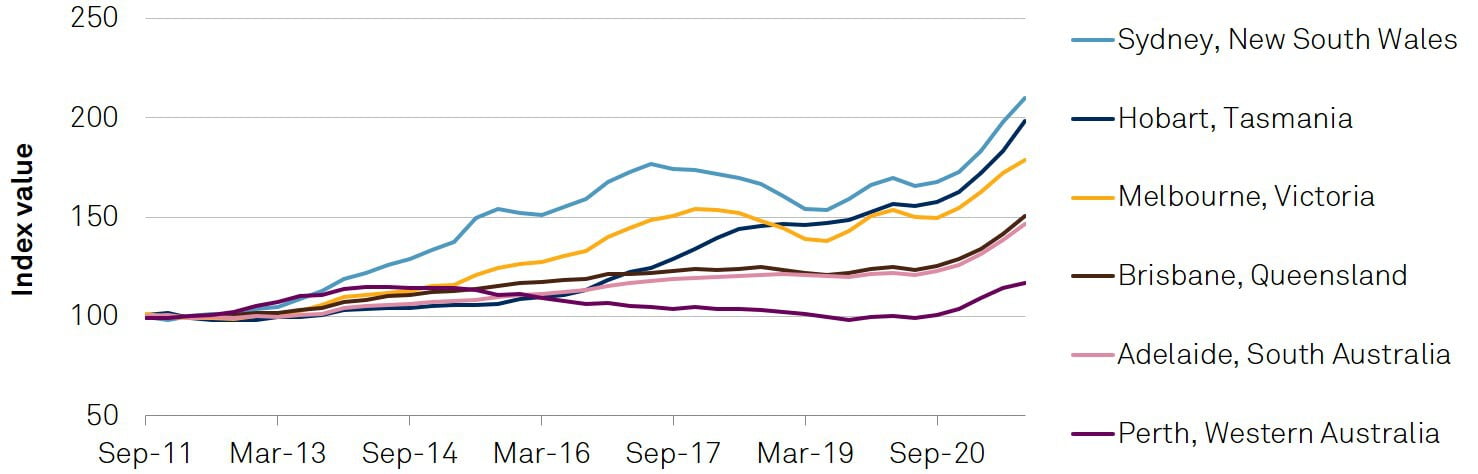

Chart 6 | A Buoyant Property Market Supports Stamp Duty Revenue Residential property price indexes*

*Selected state capitals. Source: Australian Bureau of Statistics.

Chart 7 | The Recovery Is Uneven Across States Quarterly growth in state final demand

The escalation in debt across eastern Australian states is proportionally larger than that of most comparable overseas peers, such as German states and Canadian provinces. As we have noted previously (see "Shock And Ore: Surging Debt To Test Australian States," published Sept. 30, 2020), there are several common factors behind the upsurge. We update our views here:

Countercyclical fiscal policy. Like some other federal countries, Australian states have assertively used their balance sheets to prop up the macroeconomy. State treasurers have "put the economy before the budget" and are "putting our credit rating to work when it is needed most," to quote from budget speeches. Solid public finances meant they had ample fiscal space to act.

Less aversion to debt. In June 2021, South Australia's treasurer summed up the extraordinary change in political sentiment: "No one would have ever contemplated framing budgets with a backdrop of the governor of the reserve bank, federal treasury secretary, and national business and economic commentators all urging governments to keep spending and incurring massive increases in debt and deficit." In an "only Nixon could go to China" moment, big spending by center-right governments and intervention by the Reserve Bank of Australia (RBA) provided political cover for states to go large.

Low borrowing costs. With monetary policy at its zero lower bound, fiscal policy has been the main game in town. In addition, ultralow interest rates (for now) may reduce hurdle rates, expanding the number of viable infrastructure projects added to the budget pipeline.

Public infrastructure boom. Debt was projected to rise even prior to the pandemic, to finance new infrastructure. In March 2020, the value of road and rail projects being built across the country exceeded A$120 billion for the first time, according to the Grattan Institute. Following recent budget updates, the states' aggregate capital budget over the next four years has swelled to A$303 billion (chart 8), roughly 1.6 times the size of the 1948 Marshall Plan after adjusting for inflation.

No binding fiscal rules. There are no real constraints on the size of state government deficits--beyond what politicians, voters, and the bond markets can digest. In contrast, in some federal systems such as Germany and the U.S., states are required by constitution or statute to run balanced budgets (with limited exemptions for natural catastrophes).

No mechanisms to make up shortfalls. There has been little direct aid for state budgets from the Australian government, beyond a few billion new dollars for capital grants and agreements to share certain public health response and business support costs. In contrast, in some other jurisdictions, subnational governments received significant top-up grants from their sovereigns.

By announcing vast "city-shaping" and "state-shaping" infrastructure programs, Australian states appear to be rehashing their post-financial crisis playbook of a decade ago. Back then, they poured billions of dollars into new projects, partly funded by ad hoc Commonwealth grants, ramping up capital investment by 40% between fiscal years 2008 and 2010.

We aren't yet sure if infrastructure spending will peak within the next few years, as implied by chart 8. Changes to office work patterns, rising interest rates, and price inflation in building materials and land values could alter the cost-benefit calculus of transport megaprojects. On the other hand, some states have sizable aspirations beyond the four-year forecast horizon. These include Victoria's Suburban Rail Loop and Queensland's hosting of the 2032 Olympic Games. One recent study estimates the infrastructure cost of hosting a Summer Olympics can range from US$5 billion to more than US$50 billion.

A word of caution: states typically under-deliver relative to budget, which should mean shallower but more prolonged growth in debt. The upcoming pipeline will severely stretch the capacity of industry and government. There is also wide disparity across states. Tasmania's and Victoria's four-year capital budgets are more than twice the size of Western Australia's, relative to gross state product.

Chart 8 | A Long Road Ahead For Public Infrastructure Aggregate state infrastructure investment, nonfinancial public sector

*As of Feb. 2020. Forecasts are from state budgets and may differ from our own base-case scenarios. Excludes some projects delivered via leases/service concessions. Fiscal year ends June 30. a--Actual. f--Forecast. Source: Most recent state budget updates.

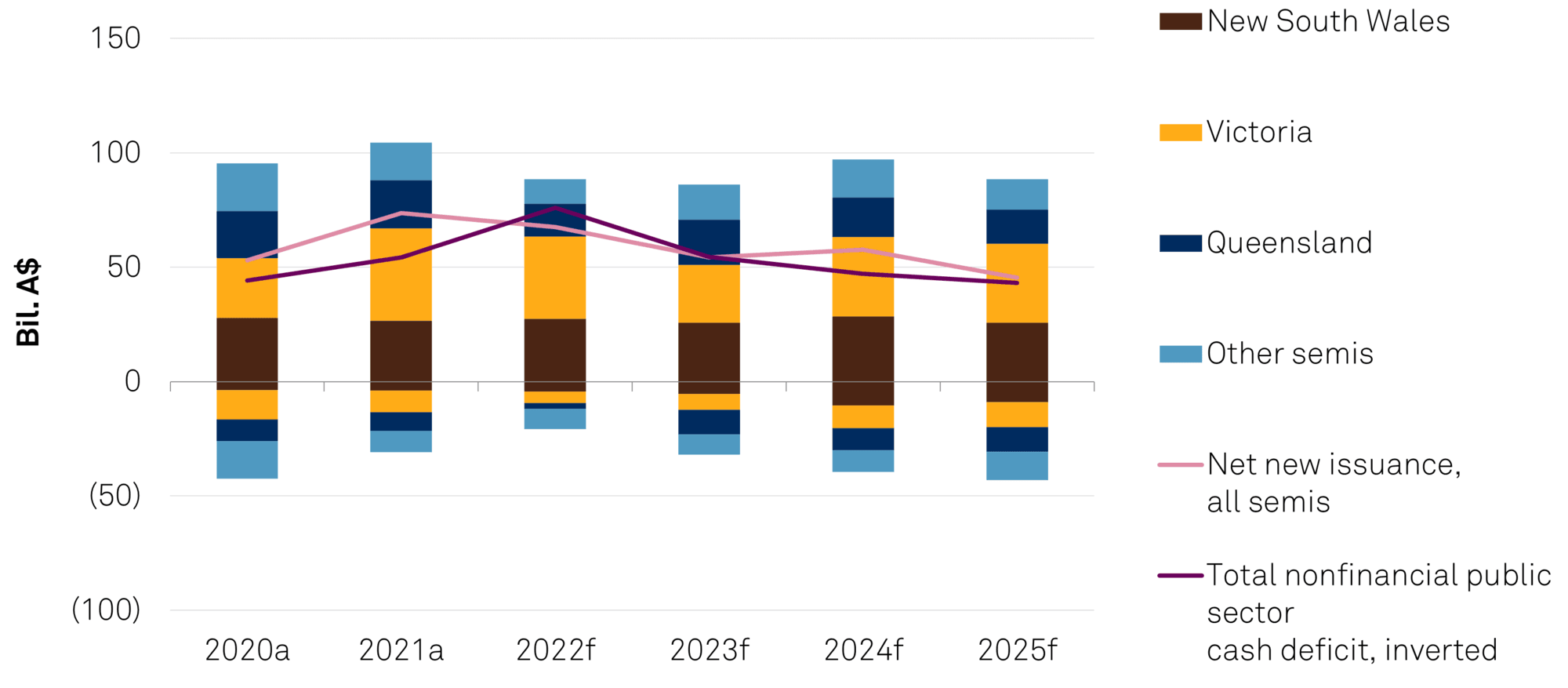

Net new bond issuance by the states is likely to stay elevated at about A$70 billion this fiscal year. This is roughly in line with last year's total, according to market guidance released after the latest round of midyear budget updates. Borrowing needs should then moderate in subsequent years (chart 9).

Chart 9 | Net Borrowing Needs Should Gradually Normalize Estimated gross bond issuance (positive figures) and term maturities (negative figures)

Forecasts are from issuers and may differ from our own base-case scenarios. Fiscal year ends June 30. a--Actual. f--Forecast. Source: Most recent state budgets and data supplied by state central borrowing authorities.

We see the balance of risks tilted to the upside--i.e., toward smaller deficits and lower borrowing requirements. Upside risks include a stronger than expected economic bounceback; likely under-delivery on states' capital budgets; the possibility of new asset privatizations, concessions, or long-term leases; and drawdowns by New South Wales on its Debt Retirement Fund to buy back debt. More recently, the Russia-Ukraine conflict adds a tailwind to global energy demand and is likely to boost state royalties from thermal coal and liquefied natural gas.

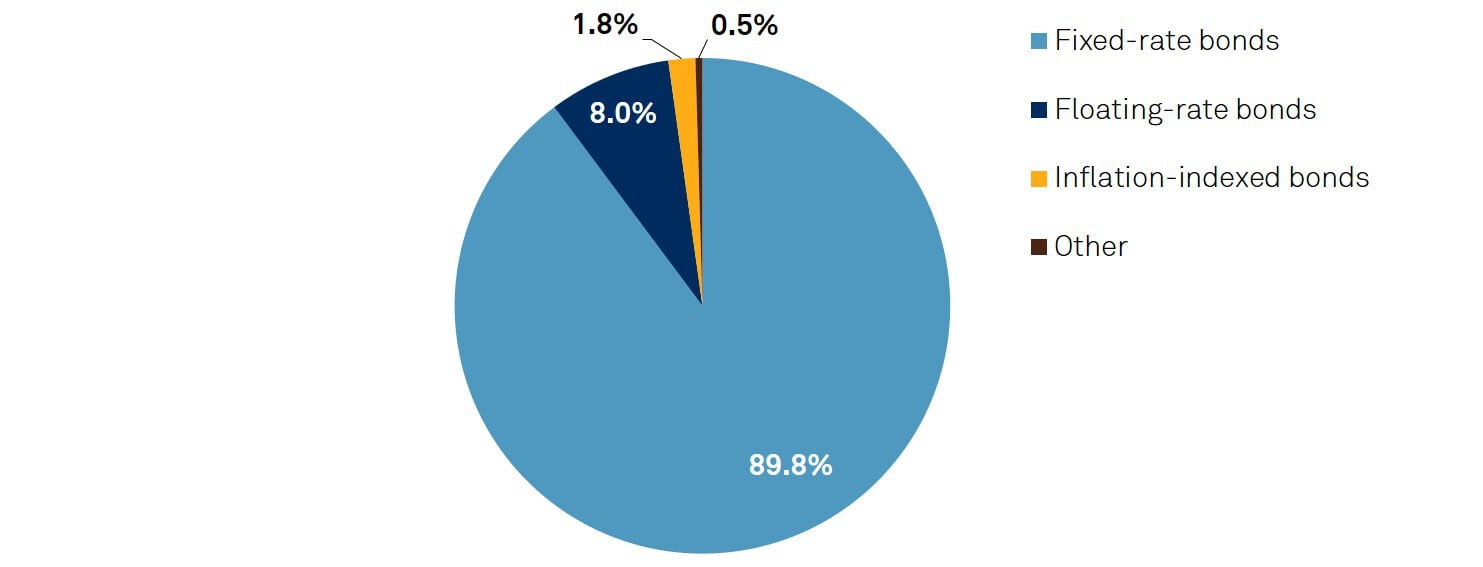

We expect Australian states to continue prudently managing their treasury risks, helping to support high credit ratings. States source almost all their debt from the capital markets. Most issuance is in the form of fixed-rate domestic bonds. State borrowing authorities (sometimes known as semi-government issuers, or "semis") aim to develop large, "benchmark" bond lines at regular intervals across the yield curve. They commit to maintaining a minimum amount outstanding in these bond lines to support secondary market liquidity.

There is a smaller quantum of floating-rate, inflation-linked, and retail bonds outstanding (chart 10), to meet demand from public corporation clients and certain investors for these products. Notably, SAFA in recent years has issued floating-rate notes referencing the Australian risk-free rate, known as AONIA. AONIA is being published as part of a "multiple rates" approach in Australia alongside the existing benchmark bank bill swap rate (BBSW), even as benchmarks in other countries are phased out.

States are locking in historically low borrowing costs, mitigating their interest rate and refinancing risk. Many are seeking to extend the duration of their yield curves. Some of the bigger semis engage in "switches" by actively repurchasing and terming out their own short-dated benchmark bonds. Again, this serves to reduce rollover risk. For the smaller states, building and infilling benchmark curves could become easier as supply ramps up.

Rising interest rates and capacity constraints could alter the cost-benefit calculus of infrastructure, causing states to scale back their ambitions.

Chart 10 | States Focus On Building Liquidity In Plain-Vanilla Bonds Breakdown by market instrument*

*As of June 30, 2021. Other category includes retail bonds and Commonwealth-guaranteed bonds. Source: S&P Global Ratings analysis of data supplied by state central borrowing authorities.

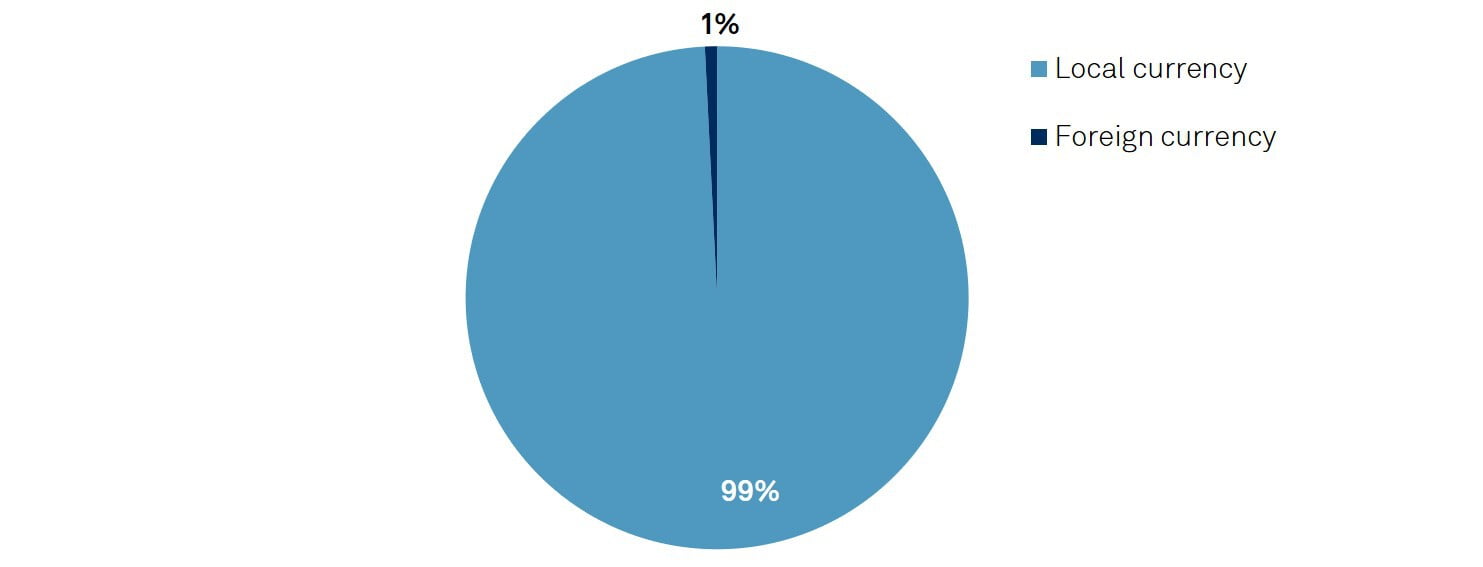

Chart 11 | Virtually All Borrowing Is Denominated In Australian Dollars Currency composition of states' long-term bonds*

*As of June 30, 2021. Source: S&P Global Ratings analysis of data supplied by state central borrowing authorities.

Currency risk is negligible as almost all borrowing is conducted in Australian dollars. Only the larger treasury corporations have multicurrency euro medium-term note (EMTN) and euro commercial paper (ECP) programs. Issuance via EMTNs is negligible (chart 11). In the past, currencies of choice have included euros, renminbi, sterling, Swiss francs, U.S. dollars, and yen. Some offshore borrowing occurs at ultralong tenors (e.g., bonds maturing in 2050), matching demand by offshore liability-driven investors such as insurers and pension funds. Foreign-currency EMTNs are fully hedged.

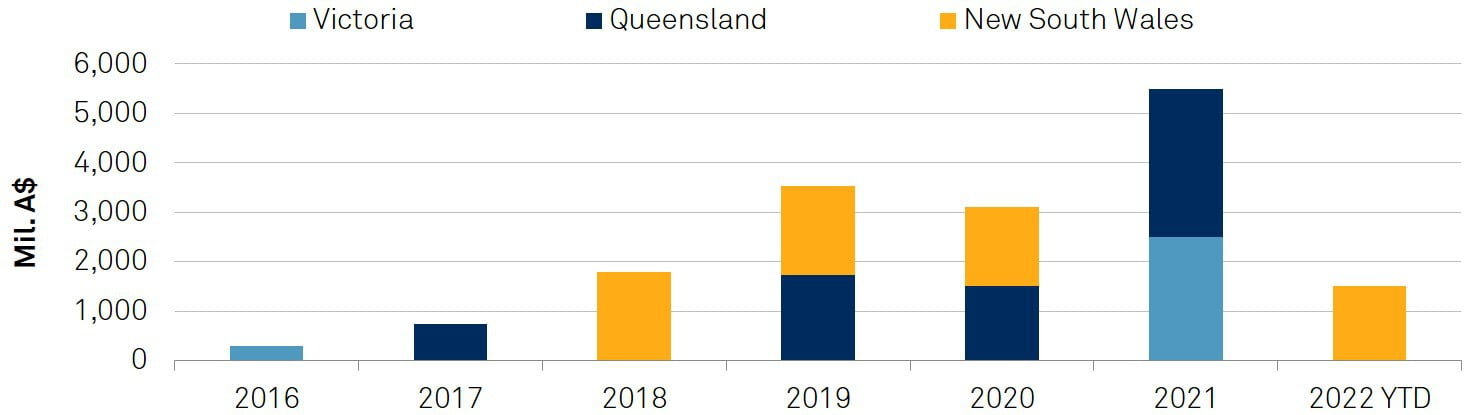

We anticipate that Australian states will issue more green, social, and sustainable (GSS) bonds in coming years. This will be spurred by larger eligible asset pools, a heightened desire to showcase environmental, social, and governance (ESG) credentials, and refinancing of GSS maturities due around 2024-2025. The three largest states are already seasoned ESG-themed issuers (chart 12). Queensland's green bond transaction in 2019 was the largest of any subnational government in the world that year, according to the Climate Bonds Initiative.

Chart 12 | Thematic Issuance Is Taking Off States' annual issuance of green, social, and sustainability bonds

Queensland has issued in green format; Victoria and New South Wales have issued in green and sustainability format. YTD--Year to date. Sources: KangaNews, state central borrowing authority websites.

Chart 13 | States' Climate Footprints Vary Widely Emissions per capita (tons CO2-equivalent per person), 2019

Source: Department of Industry, Science, Energy and Resources.

We assess GSS issuance as being neutral to marginally positive for credit quality. We understand that past issuances have priced roughly in line with existing yield curves. They have also diversified states' investor bases by bringing new pools of money (particularly "real money" asset managers) into the fold. We assign identical issue credit ratings to GSS bonds as states' other unsecured debt instruments. They rank equally, and repayment is not linked to performance of the underlying eligible assets.

Semis can likely issue in GSS format without fracturing liquidity in their mainstream bond lines, thanks to an annual borrowing cadence now structurally larger than prepandemic levels. Some state issuers see GSS bonds as forming part of their benchmark yield curves, rather than sitting alongside them. The RBA has bought some GSS bonds as part of its asset purchase program.

Growth in this market is likely because states have "longlisted" large project and asset pools that could be earmarked against future use-of-proceeds bonds. GSS bonds align neatly with states' inherent responsibilities in areas such as mass transit, renewable energy, and social housing. Some semis that haven't issued in GSS format, like WATC, are currently developing sustainability bond frameworks of their own, though Western Australia's flat debt profile will limit its opportunities to issue.

So far, we have not detected any material shift in investor appetite for Australian sovereign or subnational bonds because of ESG-related concerns, with a few well-publicized exceptions. In 2019, Sweden's Riksbank announced that it had divested holdings of bonds issued by Queensland, Western Australia, and the Canadian province of Alberta due to their larger climate footprints. Some investors have also raised allegations of "greenwashing," pointing to Australia's fossil fuel exports and high per-capita emissions (chart 13). We believe investors will increasingly look beyond issue-level use of proceeds to ask questions about issuer-level ESG metrics.

We expect demand for semi-government securities by Australian banks and other investors will help fill the void left by the RBA. In February 2022, the central bank announced that it would end its 15-month bond purchase program. (This doesn't yet imply quantitative tightening: the RBA will wait until its May 2022 board meeting to consider whether to reinvest the proceeds of future bond maturities.) Since the start of quantitative easing in November 2020, it has bought about A$56 billion of semis (chart 14), on top of separate purchases earlier in 2020 to support market functioning.

Chart 14 | The Central Bank Was A Major Buyer In 2021 Cumulative holdings of semis by Reserve Bank of Australia

Source: Reserve Bank of Australia.

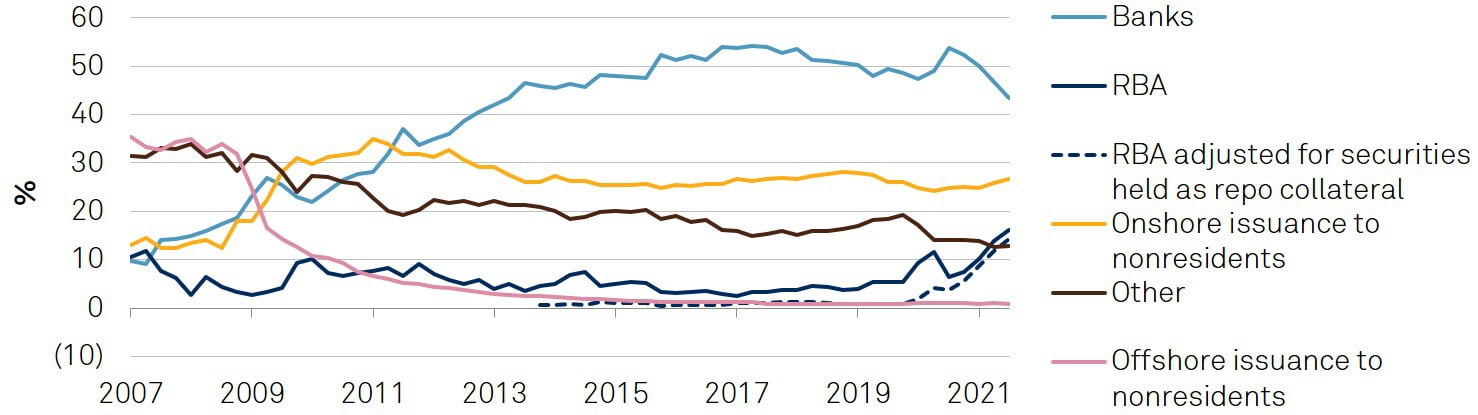

Chart 15 | Post-Financial Crisis, Banks Emerged As Large Investors Ownership of state government bonds

RBA--Reserve Bank of Australia. 'Other' category includes domestic investment funds, superannuation funds, and insurance companies. Sources: Australian Bureau of Statistics, Reserve Bank of Australia.

The closure of the RBA's Committed Liquidity Facility by the end of 2022, a gradual future reduction of exchange settlement balances, and organic growth in bank balance sheets should all help generate demand for semi-government bonds by Australian banks. These bonds are among the few instruments to qualify as highly liquid assets under Australian Prudential Regulation Authority regulations. Banks already hold about half of all semi-government debt on issue (chart 15).

The presence of foreign investors in the domestic market is sizable. Many are attracted to Australian names by their higher yields (relative to high-grade opportunities in other countries), credit quality, and offer of diversification. Feedback from market participants suggests some international investors have amended their mandates to no longer be constrained to 'AAA'-rated names.

Overall, though, the share of nonresident ownership of semis is lower than for Australian Commonwealth government bonds (ACGBs). International investors may be more familiar with, or prefer, holding sovereign over subnational names. Australian-dollar assets comprise about 1.7% of the world's official foreign exchange reserves.

There was significant dislocation in government bond markets at the onset of the pandemic in March 2020. States briefly concentrated their borrowing in short-term markets and private placements, before resuming syndicated benchmark bond issuance in April 2020. Semi-to-ACGB spreads subsequently compressed over the course of 2020 before widening a little through 2021 (chart 16). Overall yields are also rising (chart 17), mirroring global trends. Modeling by RBA staff estimates that the bond purchase program reduced longer-term ACGB yields by about 30 basis points and semi-to-ACGB spreads by 5-10 basis points, relative to where they would otherwise have been.

If future crises cause market turbulence, we see RBA intervention as more likely than the Australian sovereign offering to provide a guarantee over state government borrowing, as occurred during 2009-2010. This is because states' offshore issuance has declined markedly since the global financial crisis (chart 15). The last of the sovereign-guaranteed state bonds is due to mature in May 2023.

The first wave of the coronavirus in 2020 abruptly ended Australia's 29-year run of growth without a technical recession--the longest such stretch of any advanced economy in modern history. A health response lauded as among the best in the world in 2020 gave way in 2021 to a lethargic vaccination rollout and a costly second wave of infections. The labor market has whipsawed from predictions of double-digit unemployment to complaints of staff shortages. Australia has boasted one of the most locked-down cities in the world and some of its freest.

Interstate borders slammed shut for the first time since the 1918 Spanish flu pandemic. As borders closed, a remarkable fiscal divide opened: while the southeastern states posted historic deficits, Western Australia curiously delivered a chart-busting surplus on the back of soaring commodity prices and a favorable grant redistribution. COVID-19 overturned old political shibboleths. Center-right administrations at federal and state level, who might once have bemoaned the debt hangover from the 2008-2009 financial crisis, rolled out a Keynesian fiscal response of unprecedented speed, scope, and scale.

Today, the states exist in a kind of liminal zone. While the worst of COVID-19 may be behind us, the transition from pandemic to (possibly) endemic has been far from smooth. And while officials have seemingly ruled out further lockdowns in favor of "living with the virus," the recent omicron wave prompted a shadow lockdown, as cautious workers and consumers voluntarily disengage from the economy. Omicron, in our view, has disrupted but not derailed the recovery.

Credit trends are diverging, with resource-rich Western Australia the only state to carry a positive outlook.

Chart 16 | Spreads Have Widened A Little From 2021 Lows Spreads to ACGB, selected semi-government issuers

ACGB--Australian Commonwealth government bond. Source: Bloomberg.

Chart 17 | Borrowing Costs Are Starting To Normalize Bond yields, selected semi-government issuers

Source: Bloomberg.

Our preferred perimeter for measuring gross debt is at the "nonfinancial public sector" (NFPS) level, or total territory level in the case of Australian Capital Territory. This perimeter consolidates the general government sector and public nonfinancial corporations (which are sometimes referred to as public trading enterprises). Examples of the latter include rail operators, ports, and energy and water utilities. In our credit rating reports, we may occasionally make other analytical adjustments to arrive at our measure of tax-supported debt.

While chart 1 references NFPS gross debt, charts 9-12 and 14-17 relate to commercial debt raised in capital markets. States' central borrowing authorities issue bonds and on-lend the proceeds to public entities. As such, the stock of NFPS debt is usually roughly equal to the stock of outstanding bonds.

Sometimes there are variances. NFPS debt may be larger because it includes debt-like financial liabilities incurred by states, such as the present value of lease commitments and certain service concessions. Changes to accounting standards in fiscal 2020 brought the majority of operating leases on-balance sheet and mean there is no longer a distinction in Australia between operating and finance leases. Sometimes the stock of outstanding bonds is larger (particularly for QTC and TASCORP) because central borrowing authorities may also raise debt to lend to entities outside of the NFPS perimeter, such as public universities, grammar schools, water boards/entities, and local councils.

Secondary Contacts

Anthony Walker Melbourne +61-3-9631-2019

Rebecca Hrvatin Melbourne +61-3-9631-2123

Sharad Jain Melbourne +61-3-9631-2077

Australian States Embark On The Recovery Path, Nov. 29, 2021

Credit FAQ: Why We Downgraded The Australian States Of New South Wales And Victoria, Dec. 7, 2020

Institutional Framework Assessment: Australian States And Territories, Nov. 10, 2020

Shock And Ore: Surging Debt To Test Australian States, Sept. 30, 2020

Checks And Imbalances: Delayed Australian State Government Budgets Will Embrace More COVID-19 Stimulus, Sept. 7, 2020

S&P Global Ratings Australia Pty Ltd holds Australian financial services license number 337565 under the Corporations Act 2001. S&P Global Ratings’ credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).