This report does not constitute a rating action

Primary Credit Analysts

Martin J Foo Melbourne +61-3-9631-2016

Felix Ejgel London +44-20-7176-6780

We expect the 15 largest subnational government borrowers in advanced economies ex U.S. to begin fiscal consolidation. Average deficits should narrow from about 14% of revenues in fiscal 2022 to 7% in fiscal 2023.

Debt burdens are climbing for several Canadian provinces and Australian states. Interest costs will rise, but remain manageable, as monetary policy tightens.

None of the top-15 regions retains a 'AAA' rating. After four downgrades over the past two years, ratings are stabilizing at lower levels.

As the world enters the third year of the COVID-19 pandemic, many state and provincial governments in advanced economies continue to issue debt at an elevated pace. Borrowing is needed to finance healthcare spending, economic stimulus, and new infrastructure.

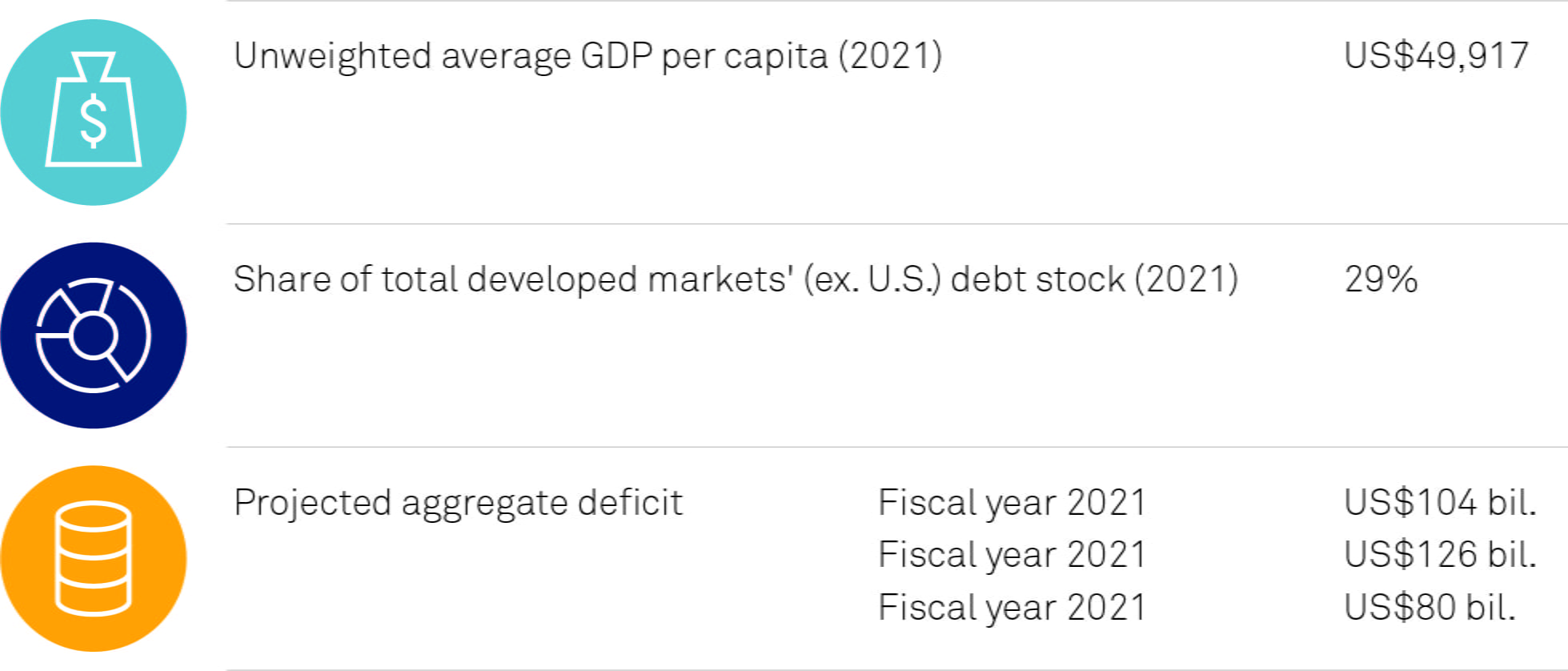

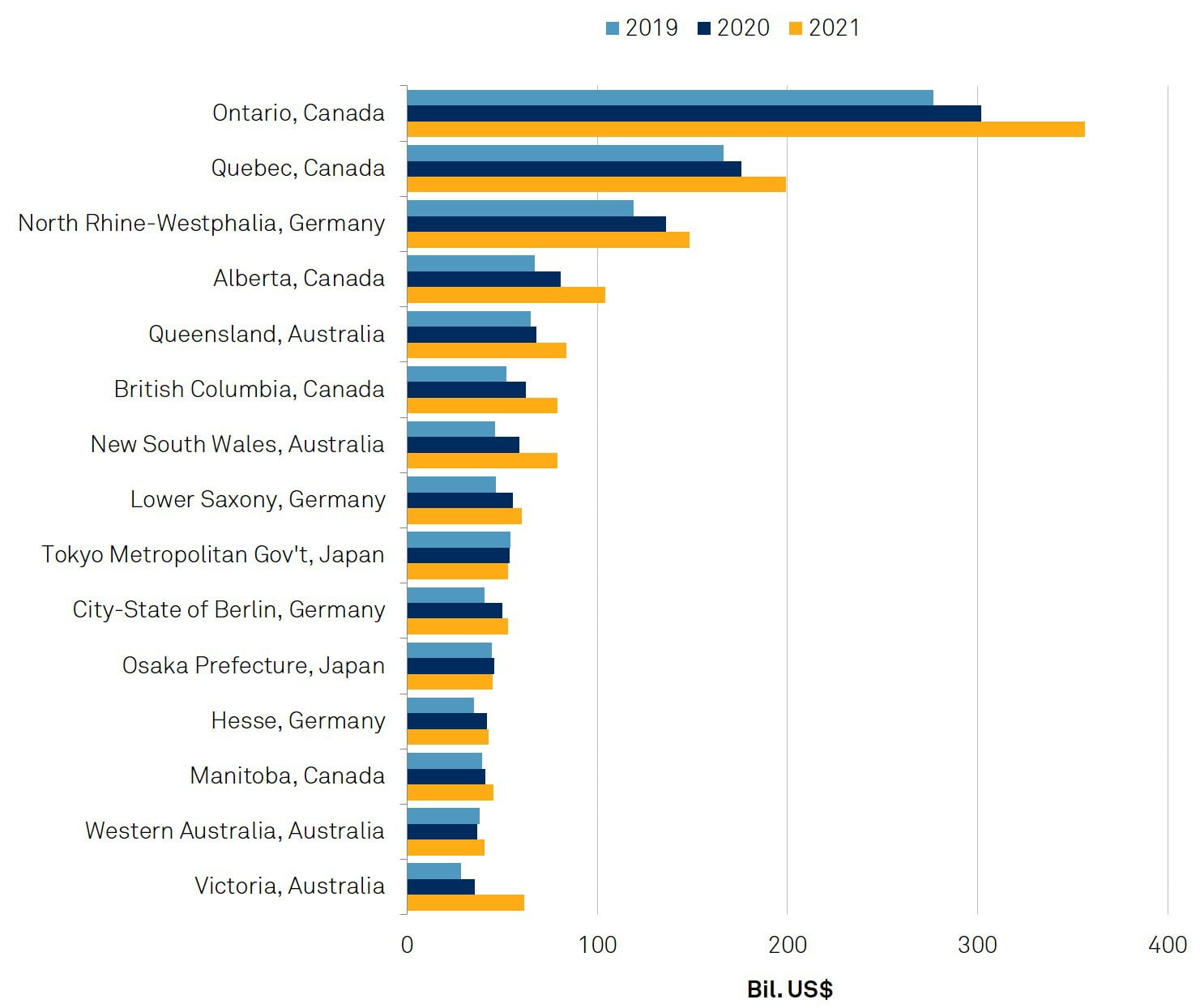

S&P Global Ratings estimates that net new borrowing by the 15 largest regions (as proxied by their after-capital-account deficits) will total about US$126 billion in fiscal year 2022, up slightly from US$104 billion last year. In dollar terms, Canadian provinces and Australian states will likely have the largest financing needs (see chart 1).

We expect 13 of the top-15 regions will report deficits across fiscal years 2021-2022. The average deficit will be about 13%-14% of total revenues in both years. Regional governments in Australia, Canada, Germany, and Japan have pursued expansionary and countercyclical fiscal policies. This has attenuated the COVID-19 shock and laid the foundations for an economic rebound. Yet it has also caused some subnational budget deficits to widen to record levels, especially in Canada and Australia.

Chart 1 | Local Government Net Borrowing Is Set To Edge Higher In 2022

*Entities not rated by S&P Global Ratings. The fiscal year in this chart refers to the year ending March 31 in Canada and Japan, June 30 in Australia, and Dec. 31 in Germany. Borrowings are converted to U.S. dollars at current market exchange rates. Note that for some issuers we may make analytical adjustments, such as deducting the haircut balance of debt retirement funds, to arrive at our measure of tax-supported debt. Cons. op--Consolidated operating. Source: S&P Global Ratings.

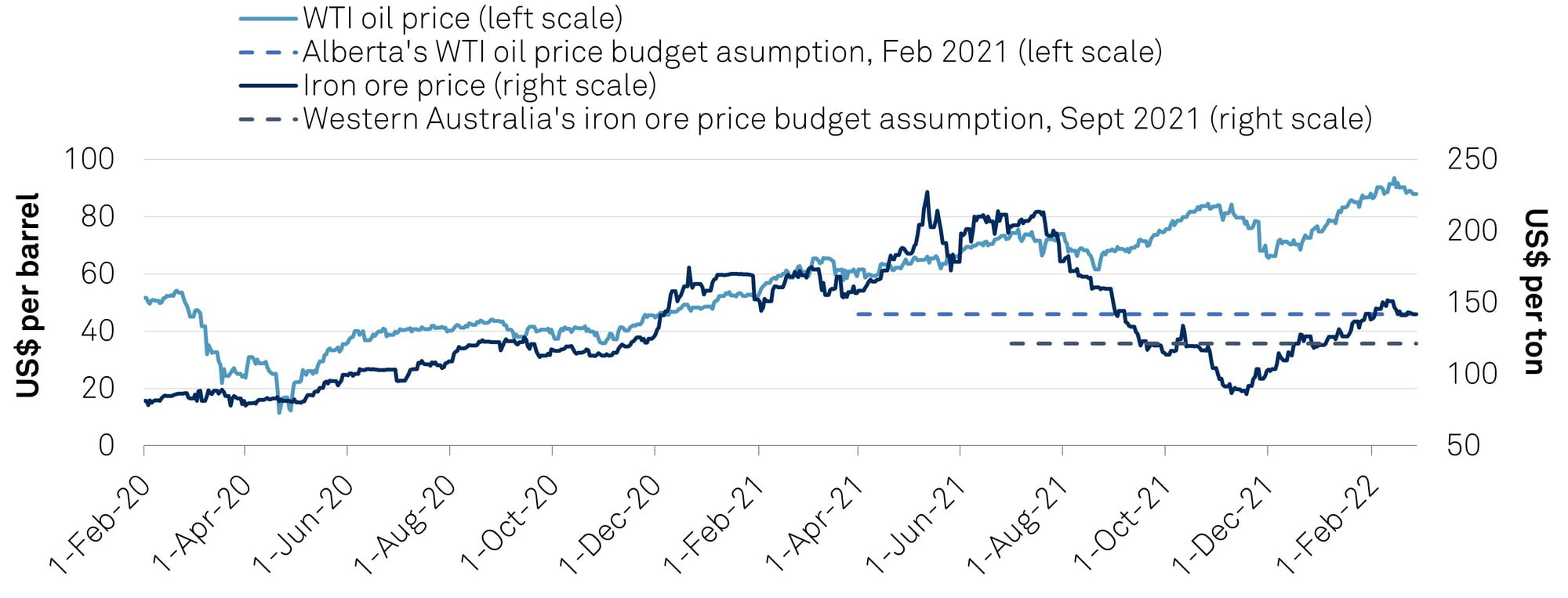

The data in chart 1, and throughout this report, are based on our most recent published base-case forecasts. For some regions, such as Alberta, the relatively recent surge in oil prices, compared with the assumptions we used in formulating our base case, mean operating and after-capital-account performance in fiscal years 2022-2023 should turn out significantly better.

Developed markets have attained high vaccination coverage and are reopening their economies. This will help propel a recovery in tax revenues and fiscal consolidation. We forecast that net new borrowing by the top-15 regions will consequently decline to US$80 billion in fiscal 2023. While an improvement, the pace of deficit reduction will be measured. In some regions, rising infrastructure investment will offset reductions in temporary pandemic-related operating spending. There will be no rush to austerity.

Subnational governments in Australia, Canada, Germany, and Japan are shifting their focus from expansionary fiscal policies to post-pandemic budget consolidation.

We have taken 11 negative rating actions on the top-15 regions since the onset of the pandemic (table 1). This includes downgrades of two Canadian provinces in 2021 and two Australian states in 2020. Today, none of the entities in the top-15 grouping is rated 'AAA'. (For context, we also lowered our ratings on two German states outside the top-15 grouping--Baden-Württemberg and Saxony-Anhalt--in 2020.)

Table 1 | List Of Rating Actions On Top-15 Regions Since The Start Of The Pandemic

Note that for State of New South Wales, State of Victoria, and Tokyo Metropolitan Government, the outlook revisions in the first half of 2020 were driven by outlook revisions on their respective sovereign governments. Source: S&P Global Ratings.

Further downgrades appear unlikely over our two-year forecast horizon. This is because all the top-15 regions rated by S&P Global Ratings now carry a stable outlook, except Western Australia, for which we revised our outlook to positive. However, the possibility of new coronavirus variants remains a downside risk. The widening economic fallout from the Russia-Ukraine conflict is an emerging one.

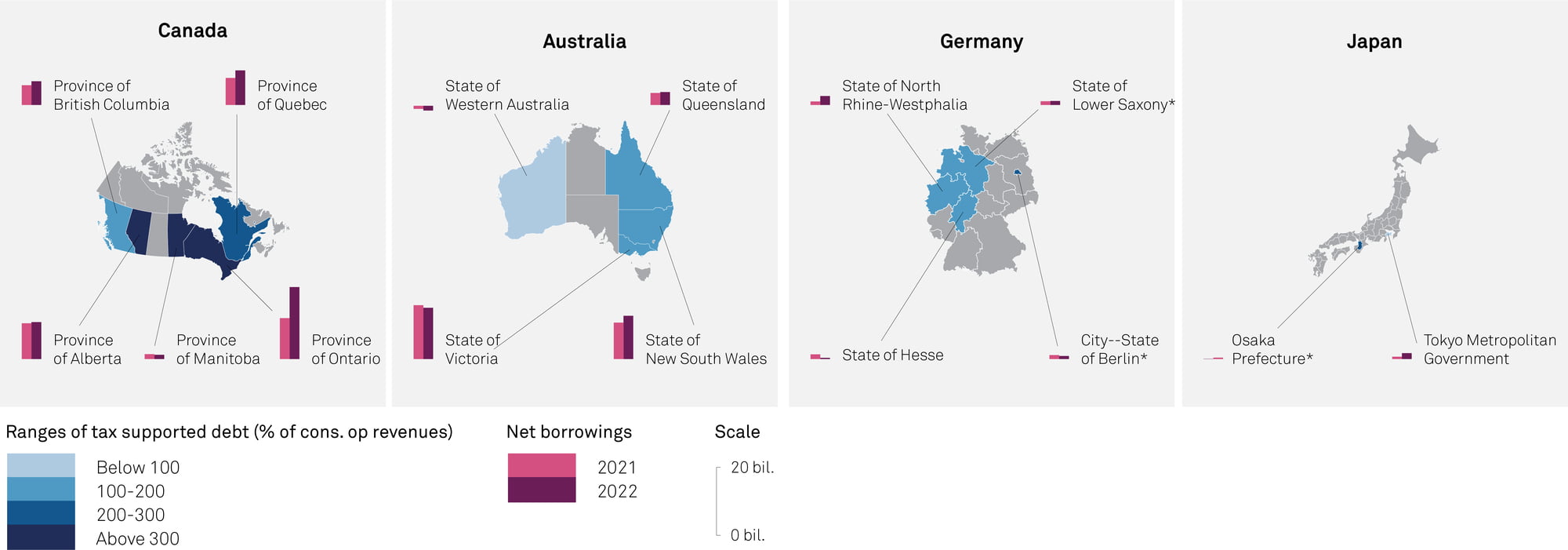

The scope of this report encompasses the 15 largest subnational government bond issuers in advanced economies outside of the U.S. These include five Canadian provinces, four German states, four Australian states, and two Japanese prefectures. The list is almost identical to those in our last report ("Local Government Debt 2021: The Pandemic Takes More Of The Shine Off Large Developed Regions' Credit Quality," published on RatingsDirect on March 25, 2021), except that the German state of Lower Saxony has entered the top-15, replacing the Japanese prefecture of Aichi. We generally use terms like "subnational" and "regional" interchangeably.

Japan (US$1.3 trillion), Canada (US$946 billion), Germany (US$885 billion), and Australia (US$323 billion) have among the highest subnational government debt stocks, in dollar terms, in the world. These four countries account for 71% of all subnational government debt in developed markets ex-U.S., as of 2021. The top-15 regions alone have combined direct debt of about US$1.4 trillion, or 29% of all subnational government debt in developed markets ex-U.S.

Chart 2 | Selected Statistics On Top-15 Regions

Figures converted to U.S. dollars at current market exchange rates. Source: S&P Global Ratings.

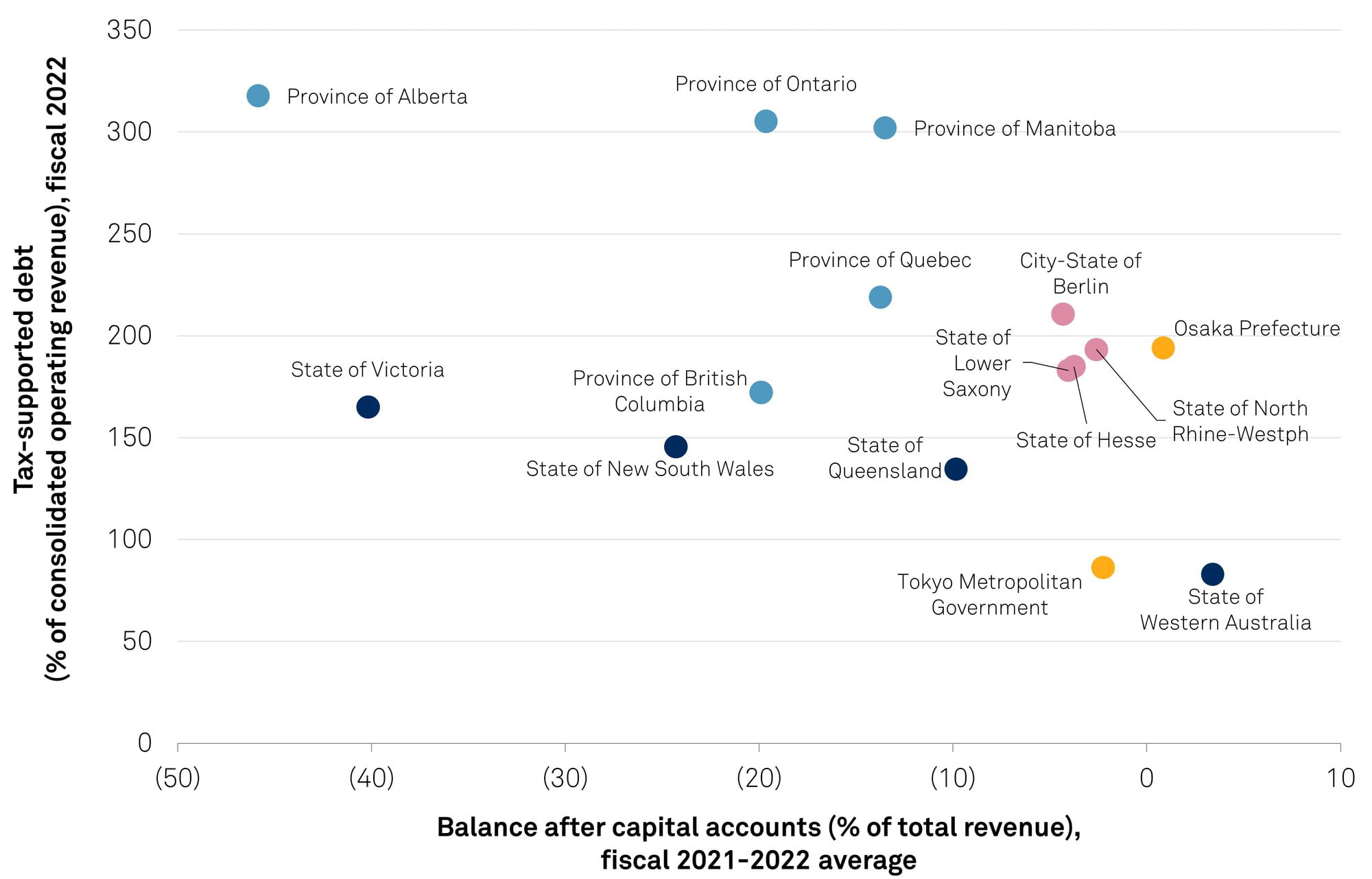

It will take time for budgets to recover. Alberta and Victoria experienced the most severe shortfalls, with remarkably high deficits exceeding 40% of their total revenues in fiscal 2021 (see chart 3). Only Western Australia has managed to remain in surplus throughout the pandemic, aided by strong commodity prices and a "hard border" policy keeping the coronavirus at bay. We anticipate that the German states of Hesse and North Rhine-Westphalia, along with Tokyo Metropolitan Government and Osaka Prefecture, will be first to revert to surplus by fiscal 2023.

Chart 3 | The Pace Of Fiscal Consolidation Will Be Uneven Balance after capital accounts (% of total revenue)

Note: The fiscal year in this chart refers to the year ending March 31 in Canada and Japan, June 30 in Australia, and December 31 in Germany. Forecasts are from our most recent published reports, and in some cases do not yet account for developments such as the Russia-Ukraine conflict and commodity price surge. a--Actual. e--Estimate. bc--Base case. Source: S&P Global Ratings.

Expansionary fiscal stances are most evident in Canada and Australia. Their regional governments are spending big to support households, businesses, and affected industries such as tourism and hospitality. In Australia, the states with the largest deficits (Victoria and New South Wales) are also those that imposed the longest and most stringent lockdowns. In Alberta, the onset of the pandemic was compounded by plummeting oil prices, though these have since dramatically rebounded.

Fiscal rules are an important point of differentiation. All German states suspended their zero-deficit ("debt brake") rules over 2020-2022. The reimposition of these rules next year should provide a solid anchor for Hesse and North Rhine-Westphalia to achieve small surpluses by 2023. We think a recent court decision on Hesse's COVID-19 special-purpose account reinforces our assumption of a relatively quick fiscal consolidation (see "Ruling On German State Of Hesse's COVID Spending Envelope Could Support Budgetary Performance," Nov. 11, 2021).

At the time of writing, though, German states face the possibility of weaker growth and hence lower tax revenue because of the influence of the Russia-Ukraine conflict on energy prices and supply chains. Higher costs for refugee intakes could also marginally weaken the states' budget balances.

Rising capital spending may prolong deficits. Most of the top-15 regions reported an uptick in capital spending over the past two years, as they accelerated projects to stimulate hard-hit economies. However, for some like British Columbia and Victoria, we expect annual capital spending to remain substantially above pre-pandemic levels out to fiscal 2023. Their governments have made big medium-term commitments to public transport, health, and education infrastructure. Meanwhile, we anticipate a drop in capital spending for Tokyo Metropolitan Government following the Summer Olympics in 2021, and a leveling off for Manitoba as large-scale projects at Manitoba Hydro-Electric Board wind down.

Direct government-to-government support in federal countries has been modest. Ad hoc federal transfers (beyond what would ordinarily have been distributed) to German states, Canadian provinces, and, to a lesser extent, Australian states, have helped bolster their budgets. These transfers include new capital grants and the sharing of costs for certain COVID-19 response spending. But in all three federal countries, we calculate that the additional transfers are only a fraction of the "excess deficit" precipitated by the pandemic (see "Non-U.S. Local Governments: To What Extent Did Sovereign Support Offset The Pandemic Downdraft?," July 19, 2021).

As we previously flagged, subnational governments in federal countries will generally be slower to repair their budgets than those in unitary ones (see "Local And Regional Governments Outlook 2022: Long-Term Challenges Resurface As The Pandemic Eases," Feb. 3, 2022). This reflects their greater revenue and spending autonomy.

Pre-pandemic changes to equalization systems have bolstered some regions. In Germany, for example, reforms that took effect at the start of 2020 replaced horizontal interstate transfers with higher transfers from the federal level, thereby overcompensating weaker states. On the other side of the world, Western Australia is benefiting from reforms legislated in 2018 that establish a relativity "floor" of 70% of its population share of the national goods-and-services tax (GST) pool. Western Australia will receive billions in GST top-up grants as a result.

The pandemic will drive public debt upward in Canada and Australia. Canadian provinces entered the pandemic with already-high leverage (see chart 4). We rate in the 'A' category all three provinces with projected debt-to-revenue ratios exceeding 300%. (Of note, updated provincial estimates for fiscal 2022 reflect stronger revenue growth, which we think will result in lower-than-expected debt burdens in the current year.)

The higher indebtedness of east-coast Australian states brings them more in line with German peers, whose debt ratios should hold roughly steady. Meanwhile, Tokyo Metropolitan Government's fiscal discipline underpins its strong 'aa+' stand-alone credit profile, though its issuer credit ratings are constrained by the sovereign ratings on Japan.

Chart 4 | Canadian Provinces Are The Most Highly Leveraged Fiscal performance vs. projected debt burden, selected subnational governments

Color coding denotes different countries. Forecasts are from our most recent published reports, and in some cases do not yet account for developments such as the Russia-Ukraine conflict and commodity price surge. Note that for some issuers we may make analytical adjustments, such as deducting the haircut balance of debt retirement funds, to arrive at our measure of tax-supported debt. Source: S&P Global Ratings.

Debt servicing will remain manageable thanks to the secular plunge in global interest rates. We expect interest-expense-to-revenue ratios to remain well below 5% for top German states, and below 1% for Tokyo Metropolitan Government, anchored by ultra-accommodative monetary policy in the eurozone and Japan. Unsurprisingly, Canadian provinces with high debt ratios also have the greatest interest costs (see chart 5). Canada and Australia are entering monetary tightening cycles, with the Bank of Canada recently lifting its cash rate by 0.25% to 0.50%.

Chart 5 | Canadian Provinces Face The Highest Debt-Servicing Costs Interest expense as a proportion of revenues, selected subnational governments (%)

a--Actual. e--Estimate. bc--Base case Source: S&P Global Ratings.

German states and Japanese prefectures should be first to surplus. Higher capital investment in Canada and Australia may prolong borrowing.

Central banks intervened to soak up bond supply. In the three federal countries, quantitative easing programs helped to backstop demand for subnational government bonds and to keep a lid on domestic bond yields. These programs included:

Uniquely, the BoC's Provincial Money Market Purchase Program saw it acquire treasury bills and short-term promissory notes in the primary market. (Other programs were all conducted in secondary markets.) Though a part of the ECB's toolkit for many years, the 2020-2022 period saw the first foray by the BoC and RBA into outright asset purchases. The BoC and RBA also supported provincial and state government bond markets through reverse-repo facilities.

We expect top-15 regions to finance themselves predominantly in capital markets. Canadian provinces borrow only through bond issuance (see table 2). In addition to their Canadian-dollar programs, the provinces have sizable foreign-currency programs, regularly issuing in U.S. dollars, euros, pounds sterling, Australian dollars, and even Norwegian krone. Ontario is by far the largest issuer, singlehandedly accounting for one-third of a trillion U.S. dollars (see chart 6). Australian states concentrate on domestic issuance, with only a tiny quantum of foreign-currency term borrowing. Some also have significant lease or service concession liabilities.

For German states, the relative importance of bond markets has gradually risen. We believe this is because bond-market debt can be raised more quickly and reliably during crises, has benefitted from favorable pricing dynamics caused by central bank activity, and has become relatively more attractive for key investors in the insurance and pension sector due to changed accounting and regulatory practices. Bonds represent about 70% of all German states' debt; "Schuldschein" loan certificates and money-market borrowings account for the rest. Japanese prefectures borrow through a mix of bond issuance in the huge domestic municipal market, bank loans, offshore bond issuance, loans from the central government, and via the Japan Finance Organization for Municipalities (JFM, a public-sector funding agency).

Table 2 | Bonds Represent A Large Share Of Subnational Governments' Debt Stock

Subnational Government

Bonds/Bills As % Of Direct Debt Stock

Value Of Bonds Outstanding 2021 (Bil. US$)

Province of Ontario

100

356,379

Province of Quebec

199,337

State of North Rhine-Westphalia

78

148,571

Province of Alberta

103,992

State of Queensland

83,814

Province of British Columbia

79,185

State of New South Wales

88

78,935

State of Victoria

76

61,728

State of Lower Saxony

79

60,300

City-State of Berlin

72

53,054

Tokyo Metropolitan Government

92

52,867

Province of Manitoba

45,154

Osaka Prefecture

80

45,021

State of Hesse

64

42,589

State of Western Australia

40,499

Source: S&P Global Ratings.

Chart 6 | Top-15 Regions Have Outsized Bond Programs Stock of bonds by largest subnational governments in developed markets ex. U.S.

Note: The fiscal year in this chart refers to the year ending March 31 in Canada and Japan, June 30 in Australia, and December 31 in Germany. Borrowings converted to U.S. dollars using year-average exchange rates. Bil.--Billion. Source: S&P Global Ratings.

Physical risks remain manageable. Several of the top-15 borrowers have been buffeted by environmental disasters during the past two years. These include the 2021 floods in North Rhine-Westphalia, the 2019-2020 "Black Summer" bushfire season across New South Wales and Victoria, and flooding in Queensland at the time of writing.

Costs are usually shared between central and subnational governments and can be easily met by the balance sheets of highly rated borrowers (see "Germany And Affected States Can Absorb Response To Devastating Floods," July 22, 2021, and "Australia Sovereign And State Ratings Can Accommodate Bushfire Impact," Jan. 13, 2020). One side effect will be heightened public debate about climate change, which may prompt further investment in resilience and energy transition.

Regional governments are at the vanguard of green, social, and sustainable (GSS) bond innovation. Many of them are years ahead of their respective central governments in tapping the GSS market. Ontario has C$10.25 billion of green bonds outstanding at the time of writing, making it the largest subnational green bond issuer over the past decade, according to the Climate Bonds Initiative. Tokyo Metropolitan Government has been active in green bonds, too, and issued Japan's first-ever municipal social bond in 2021. North Rhine-Westphalia has issued eight sustainability bonds. Mining-oriented Alberta and Western Australia are among notable absences from the market.

These use-of-proceeds bonds fit comfortably with policy responsibilities for subnational governments in areas as diverse as public transport, electricity networks, hospitals, forestry management, and climate-change adaptation. Regional governments are frontline providers of infrastructure and key social services, often more so than sovereigns. In some cases, GSS bonds have attracted larger or more diverse order books at primary issuance and priced at a marginal "greenium".

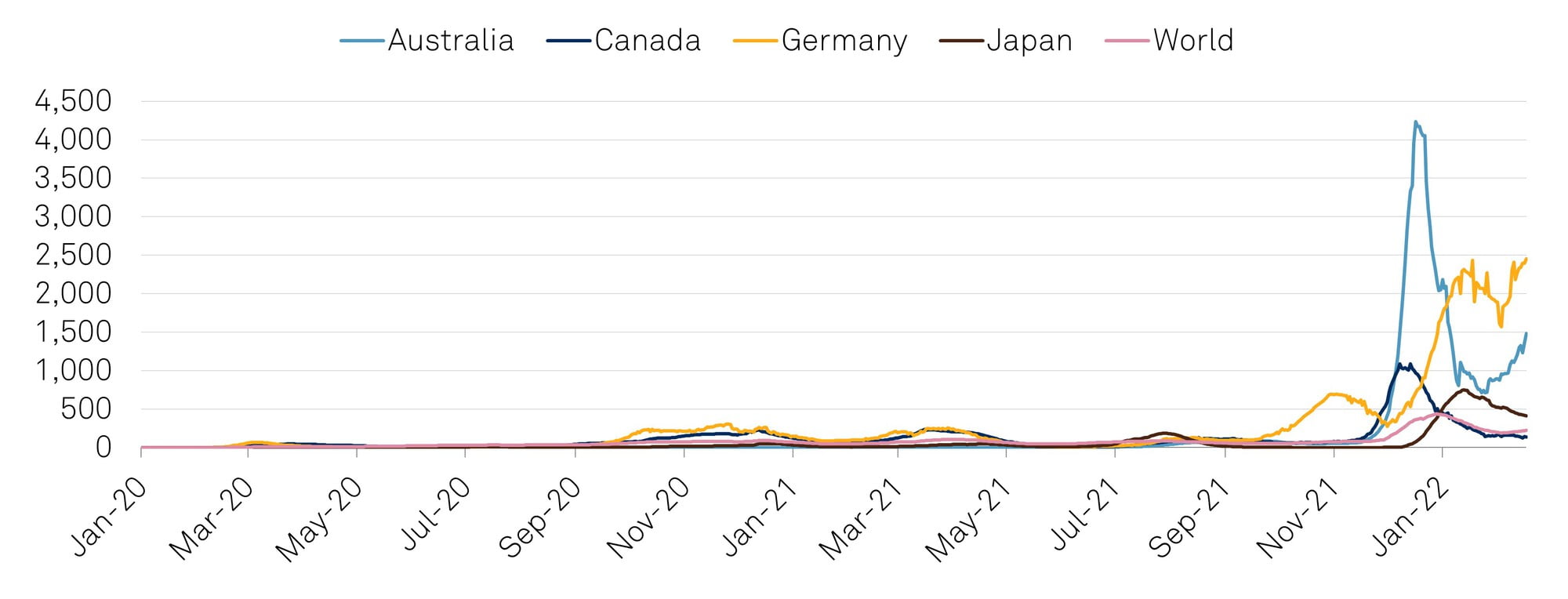

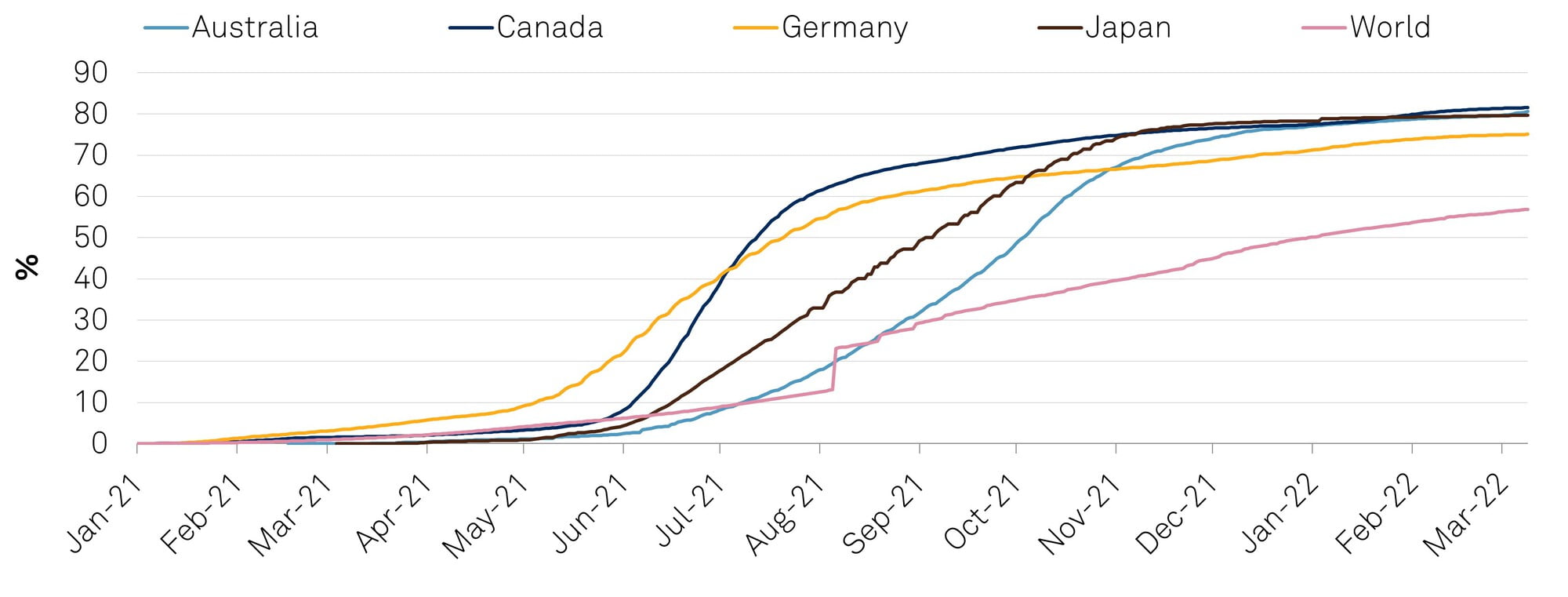

Governments are learning to live with the virus. Though omicron case numbers soared at the start of 2022 (see chart 7), vaccination coverage is high in advanced economies (see chart 8), severing the link between infections, hospitalizations, and deaths. Consequently, subnational governments are now firmly in the deregulatory phase of the pandemic. We think this will help tax receipts and budget balances to normalize.

Chart 7 | The Omicron Wave May Be Peaking In Some Advanced Economies New cases per million, smoothed

Sources: Johns Hopkins University and Our World In Data.

Chart 8 | About 80% Of Advanced Economies' Populations Are Protected % of population fully vaccinated against COVID-19

Source: Our World In Data.

At a national level, the island countries of Australia and, more cautiously, Japan, are reopening to certain categories of foreign travelers. This will be positive for regions with significant services export industries, like Victoria.

Table 3 | S&P Global Key Macroeconomic Forecasts, March 2022

*European Central Bank refinancing rate. a--Actual. F--Forecast. Source: S&P Global Economics.

Windfalls from commodities may be credit positive. High commodity prices have already boosted the budget bottom lines of regions with large mineral export industries, such as Alberta and Western Australia. Market prices have generally exceeded budget assumptions through the past two years, resulting in higher royalty revenues (see chart 9). Note that we use our own house assumptions when constructing our forecasts (see "S&P Global Ratings Raises Near-Term Oil And Gas Price Assumptions Following Russian Invasion Of Ukraine," March 1, 2022, and "Metal Price Assumptions: Shortages Worsen And Prices Spike As Conflict Roils Metals Trading," March 18, 2022).

Chart 9 | Surging Commodity Prices Are A Boon To Resource-Rich Regions Market price of commodities relative to initial budget assumptions

WTI--West Texas Intermediate. Iron ore prices are for benchmark 62% fines inclusive of cost and freight (CFR). The fiscal year ends March 31 in Canada and June 30 in Australia. Sources: Provincial and state government budget papers, S&P Global Ratings.

Russia's invasion of Ukraine has ramifications for financial and energy markets. These may include energy-supply disruptions or price shocks, particularly in Europe, and sustained inflationary pressures more broadly. Energy security is the Achilles heel of the European economy, given its heavy reliance on Russian energy imports (see "The Macro And Credit Effects Of Russia's Invasion Of Ukraine," published Feb. 25, 2022). Russia provides Germany with 55% of its imported gas.

In this report, we refer to developed markets or advanced economies outside of the U.S. These include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Italy, Japan, New Zealand, Norway, Spain, Sweden, Switzerland, and the U.K.

Deficits referred to in this report are our measure of after-capital-account balances, in cash terms. We do not rate the City-State of Berlin, State of Lower Saxony, or Prefecture of Osaka, but have incorporated our estimates of their deficits and borrowing in this report.

Secondary Contacts

Michael Stroschein Frankfurt +49-693-399-9251

Kensuke Sugihara Tokyo +81-3-4550-8475

Bhavini Patel Toronto +1-416-507-2558

Stephen Ogilvie Toronto +1-416-507-2524

Satoru Matsumoto Tokyo +81-3-4550-8673

Noa Fux London +44-20-7176-0730

S&P Global Ratings Australia Pty Ltd holds Australian financial services license number 337565 under the Corporations Act 2001. S&P Global Ratings' credit ratings and related research are not intended for and must not be distributed to any person in Australia other than a wholesale client (as defined in Chapter 7 of the Corporations Act).