This report does not constitute a rating action

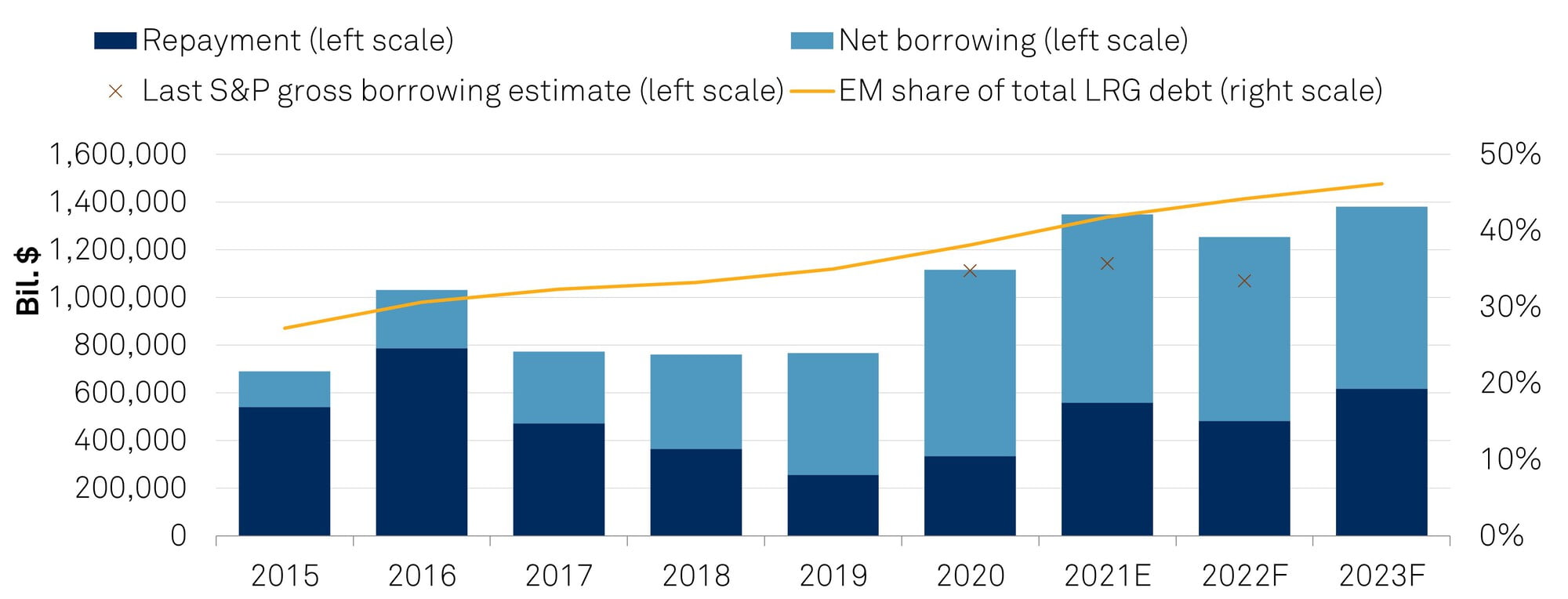

We expect emerging market local and regional governments' borrowing to stay elevated at more than $1.2 trillion over the next few years after substantial increases in 2020 and 2021.

We forecast China and India to maintain positive net borrowing, primarily to finance infrastructure spending and operating costs, respectively, while the rest of emerging markets (EMs) will borrow to refinance existing debt.

Although many subnational governments in EMs are still disconnected from the international capital market, many possess the capacity to increase borrowing and thus finance much needed infrastructure development.

Primary Credit Analysts

Sarah Sullivant Austin + 1-415-371-5051

Constanza M Perez Aquino Buenos Aires +54-11-4891-2167

Felix Ejgel London +44-20-7176-6780

S&P Global Ratings projects that net borrowing (excluding refinancing) of subnational governments in emerging markets will moderate somewhat in 2022 from a peak in 2020. We estimate that EM debt will increase its participation and reach just above 40% of global LRG debt by 2023.

In Europe, borrowings will be subdued in the next year or so, particularly in Russia, Ukraine, and Kazakhstan, as the military conflict and its ramifications for neighboring countries unfold. S&P Global Ratings acknowledges a high degree of uncertainty about the extent, outcome, and consequences of the military conflict between Russia and Ukraine. In the aftermath of the conflict, local borrowings in the zone of conflict could increase, although we would expect a large share of the funds to finance rebuilding Ukraine to be secured and disbursed at the sovereign level. Other LRGs in Central Europe have largely finalized projects from the previous EU budget cycle, with the peak in implementation coinciding with the pandemic. Borrowings in the Middle East and Africa are likely to be constrained by rising borrowing costs, low investor appetite, and high energy prices that benefit commodity exporters such as Nigeria.

The evolution of the pandemic continues to be a risk, albeit moderating, in our view. Borrowing will be moderately higher than we expected in our last report, “Local Government Debt 2021: China's Dominance Overshadows Borrowing Capacity In Other Emerging Markets,” published March 25, 2021, given that rising debt financing needs and still large fiscal deficits in China and India will likely keep annual gross subnational borrowing in EMs well above $1.2 trillion (see chart 1). Sustained high energy prices and a prolonged conflict in Europe could stimulate renewed borrowing if these factors lead to more investments to rebuild infrastructure and foster energy independence from Russia.

Chart 1 | LRG Borrowings In EM Will Remain High In 2022-2023, Driven By China And India

e--Estimate. f--Forecast. Source: S&P Global Ratings.

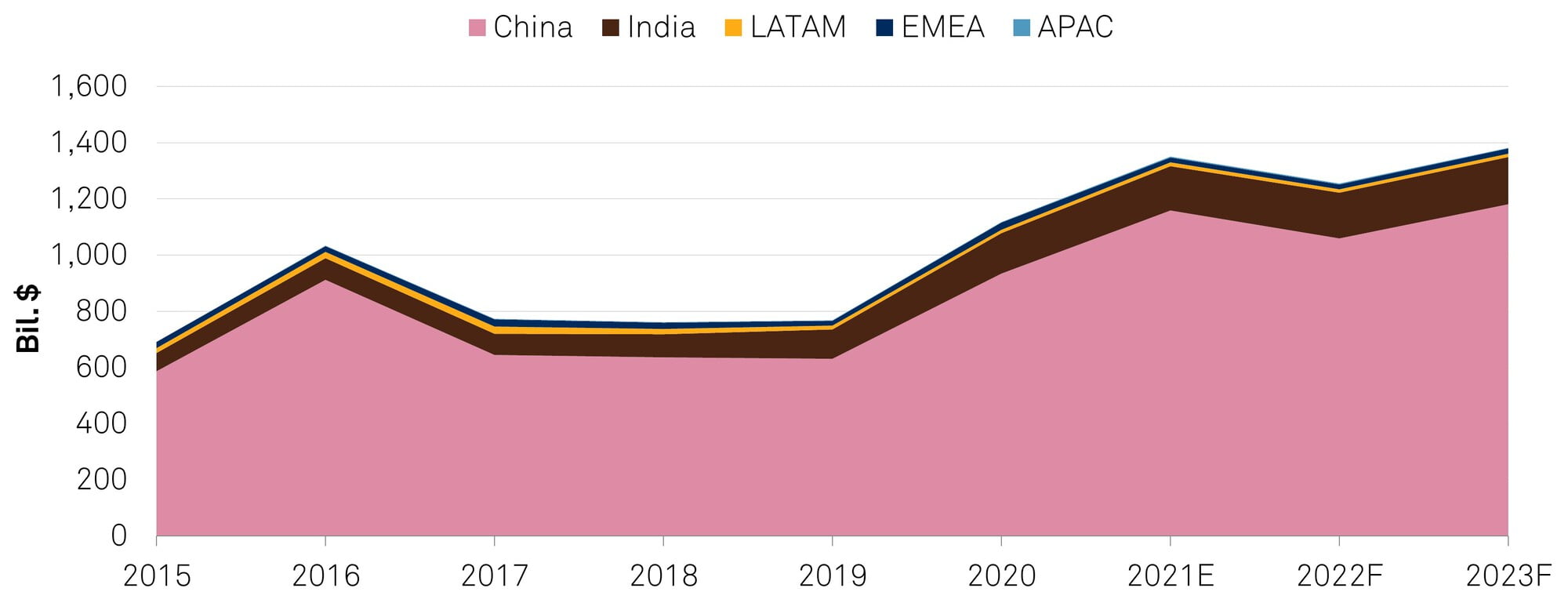

In China and India, which combined account for 95% of total EM LRG borrowing (China 85%, India 10%), we expect positive net borrowing in the next two years. This is explained by China’s promotion of a more investment-led growth strategy that continues to rely heavily on LRGs and their associated financing vehicles. Chinese authorities have set a GDP growth target of 5.5% for 2022.

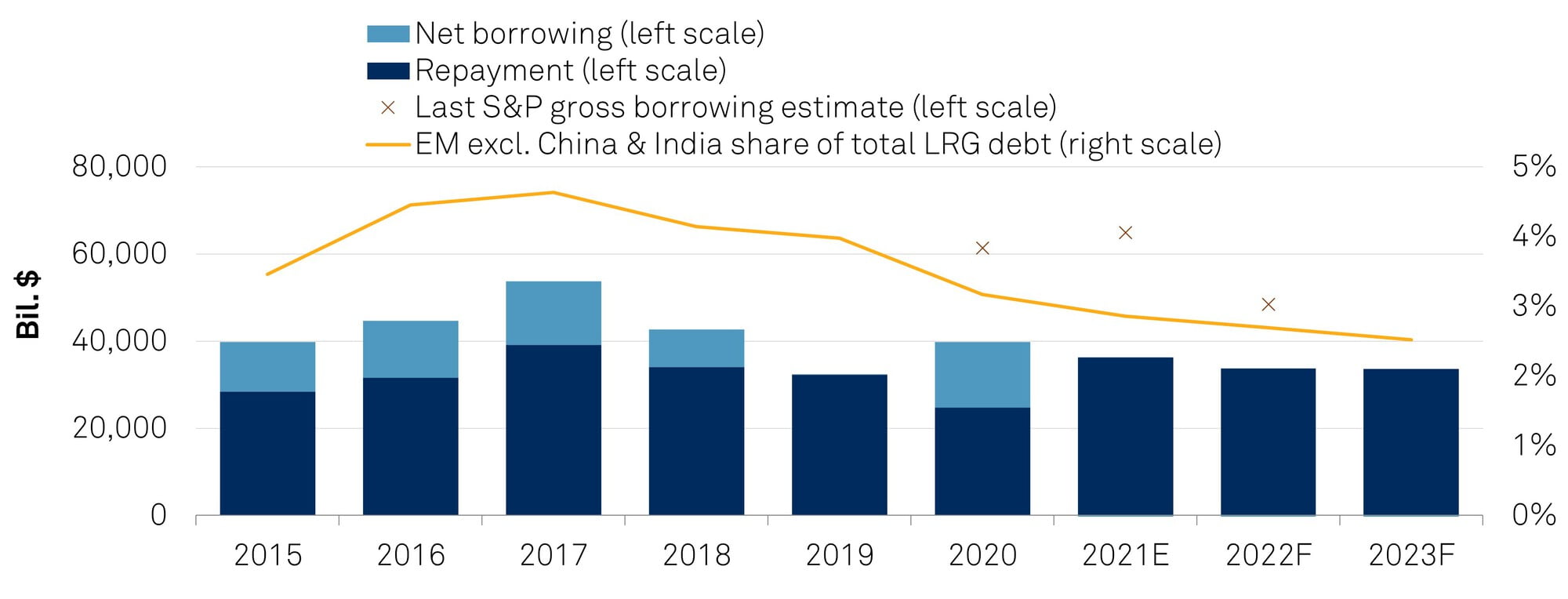

Outside of China and India, EM subnationals’ net borrowing will be close to zero in 2022-23

Excluding China and India, we expect EM LRGs’ net borrowing will be zero in 2021-2023 after the spike in 2020. Record high levels in recent years for this group of countries followed debt issuances in U.S. dollars from Argentine provinces as well as higher borrowing in Eastern Europe amid the pandemic.

Given that infrastructure investments increased in EM Europe during the closing years of the previous 2014-2020 EU budget cycle, we expect many regional governments to scale back spending in real terms in 2022. The large infrastructure backlog will also likely constrain subnational budget flexibility in Latin America. Executing local capital projects in the region is increasingly difficult because of poor access to financing, high procedural hurdles, and incentives that aren't conducive to undertaking long-term planning and investment.

Chart 2 | Outside China and India, EM LRGs Borrow For Refinancing Only in 2021-2023

The difference between projected and actual borrowings in Latin America is largely explained by Brazil LRGs, which receive large federal government transfers that have led to cash accumulation and no need for additional borrowing, although spending pressures could mount in 2022. We had also included in our previous forecasts new debt from Argentina amid the provincial restructurings, but only the province of Buenos Aires replaced its old bonds with new ones, while other provinces changed the terms of existing contracts and issued smaller amounts to cover past-due interest.

We expect Chinese gross borrowing to decrease this year following a temporary slowdown of refinancing needs, but it will begin to rise again in 2023. Most Chinese LRGs can easily roll over the majority of their debt upon maturity at low interest rates in the domestic capital market. Looking at net borrowings, which are largely to support new investment, Chinese LRGs will borrow moderately after three years of large increases as some LRGs with high debt levels approach their borrowing quotas, which the central government slashed in an effort to rein in LRG liabilities. (See: “China Local Governments' Escalating Issuance May Finally Be Testing Liquidity,” published March 1, 2022).

We expect Indian states’ net borrowing to grow modestly in the next two years (2.3%-3.0% year-over-year) as their focus turns from infrastructure investment to sustaining higher operating spending following the pandemic. A large share of the additional costs the states incurred during the pandemic have become almost committed, and we expect it will take them longer to reduce and consolidate these costs compared to peers that had more temporary pandemic-driven operating costs.

The central government, in turn, has taken on more of the burden of infrastructure investment and increased capital grants to states to alleviate budgetary pressure.

China and India combined account for 95% of total EM LRG borrowing

Chart 3 | China And India Continue To Dominate Subnational Gross Borrowings

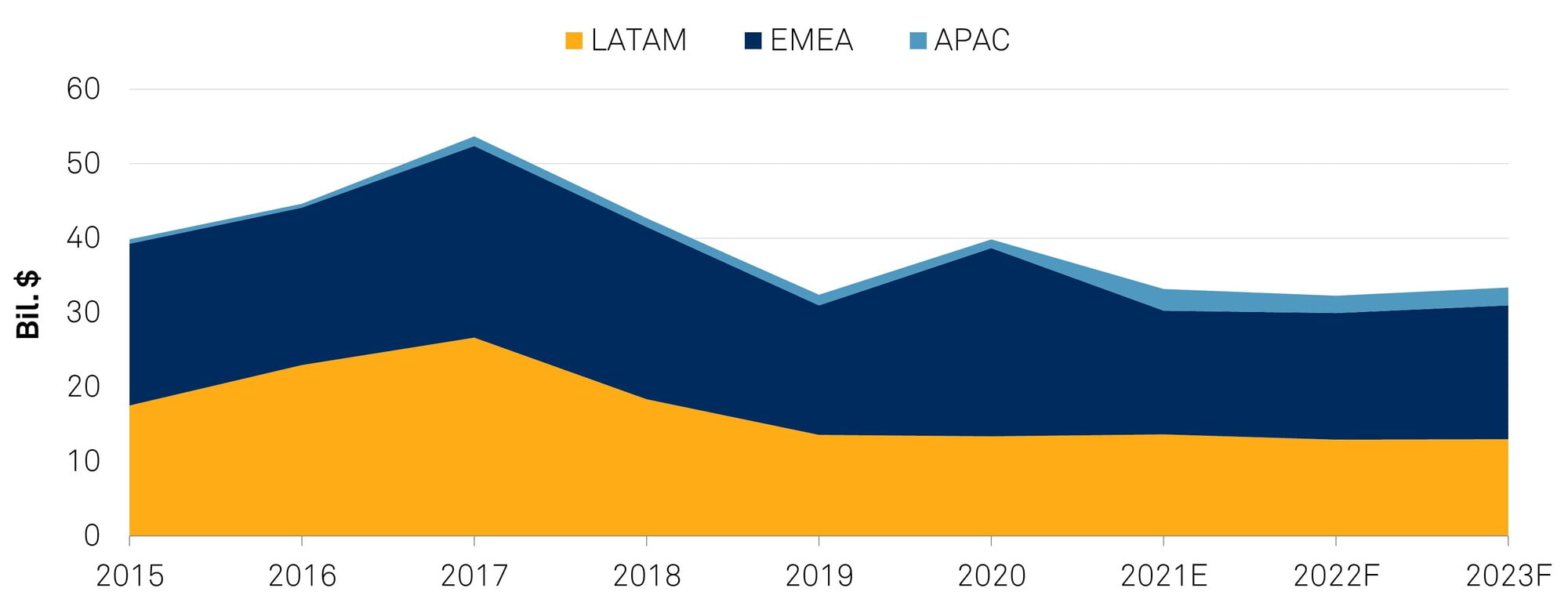

EM EMEA local governments have used available capacity to increase borrowing to support spending in the last EU budget cycle. However, EM borrowing in other regions has been falling. Latin American LRGs' gross borrowing has been declining since 2018. In Brazil, lower borrowing is due to government support in the form of transfers amid the pandemic. In Argentina, lack of access to the market following the default of the sovereign and most provinces explains the decline. And in Mexico, public debt reduction remains a pillar of central government policy, compounding a steep decline in infrastructure investment underpinned by weak capital execution and other structural limitations. In addition, borrowing in EM APAC (excluding China and India) has remained very low because of relatively underdeveloped domestic debt markets and low investor appetite.

Chart 4 | Latin America Gross Borrowing Has Been Declining Since 2018, While EMEA EMs Increased Borrowings In 2020 Amid Pandemic

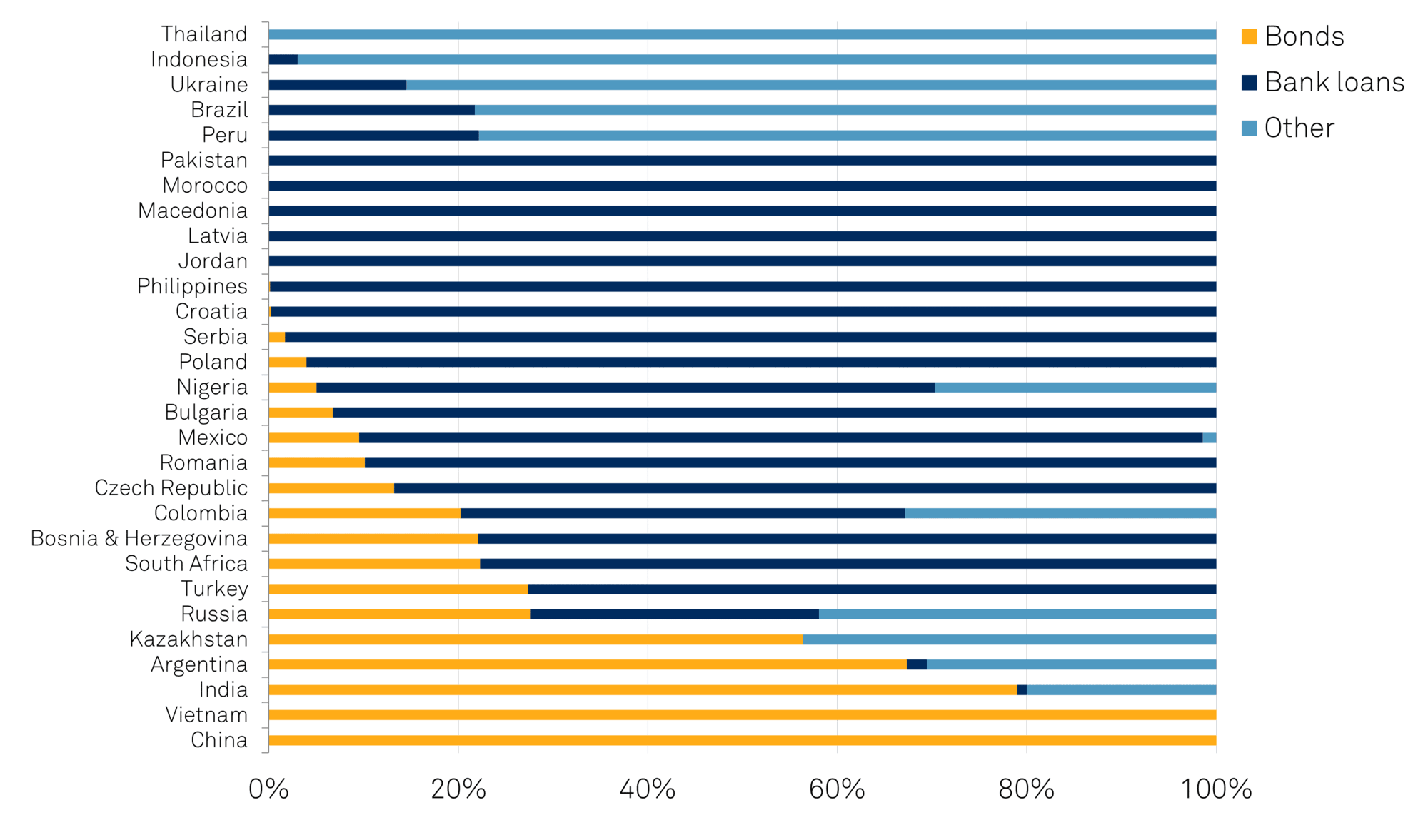

Across EMs, LRGs face severe limits on raising debt. Most of them must rely on their sovereign governments to provide direct lending from their budgets or to borrow from multilateral institutions and lend on to LRGs, or rely on state agencies and state-owned or national banks (see chart 5). At the same time, while LRGs in China and India rely heavily on bonds, issuance is almost entirely in local currency, and international investors have very limited if any access to this issuance type. Though China and India recently relaxed rules to allow nonresident investors to purchase LRG bonds, the uptake remains low.

Access to international capital markets not only broadens the investor base, but also creates a solid incentive for governments to improve transparency and predictability of financial policy. The issuance of foreign currency bonds, though, exposes borrowers to the volatility of domestic currency exchange rates and requires careful and active management to avoid undue pressure on local finances.

Chart 5 | In Most EMs, LRGs Rarely Tap Capital Markets

Estimates for 2022. Source: S&P Global Ratings.

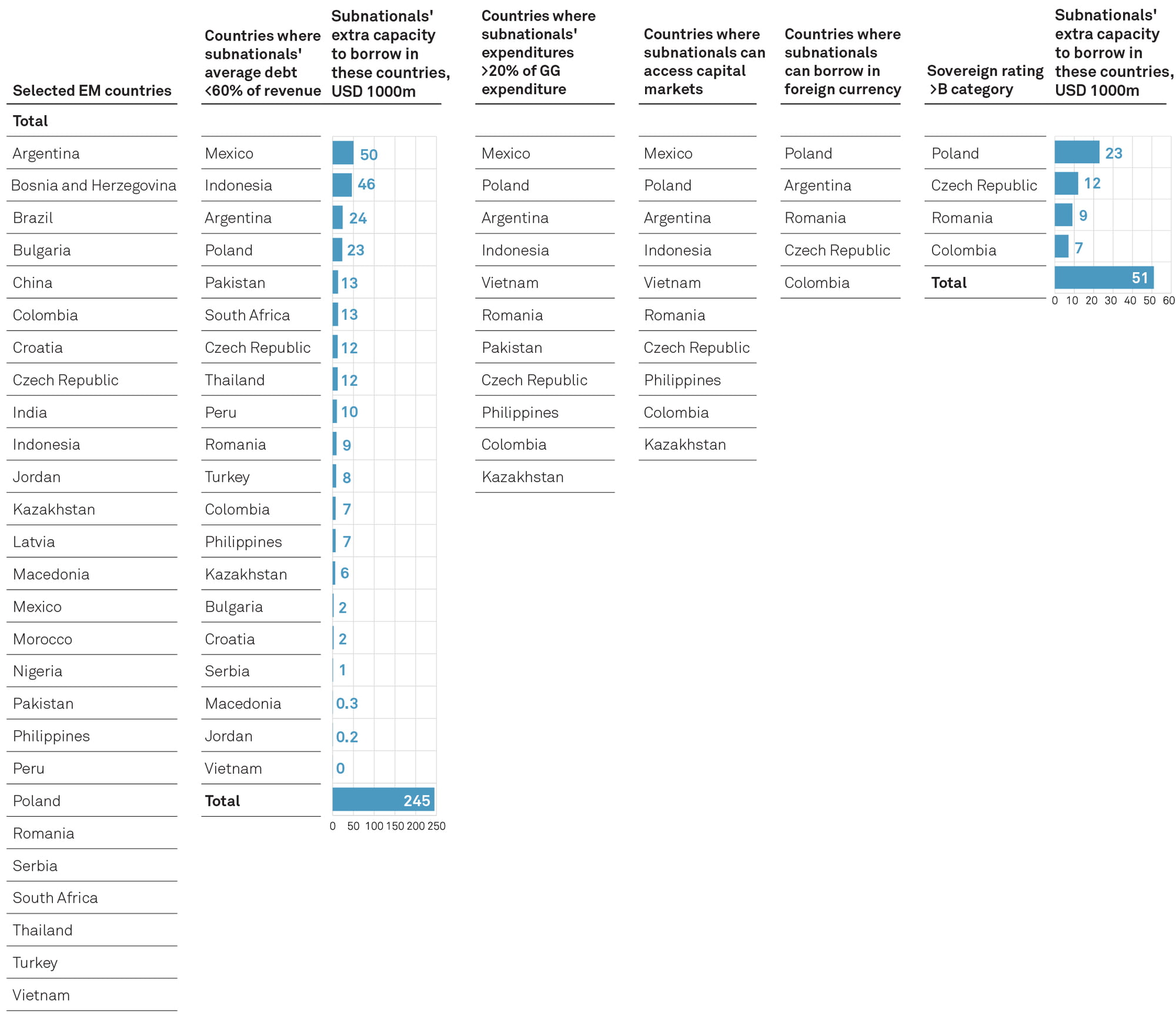

EM subnationals have an implied capacity to borrow between $50 billion and $250 billion to meet critical infrastructure needs

EM LRG debt as a share of the global LRG debt stock doubled over the past decade, to 40% estimated by 2022 from 20% in 2012.

In dollar terms, debt is three times larger than 10 years ago, mostly explained by the increase amid the pandemic.

Chart 6 | LRGs Have Borrowing Capacity In Most EMs

Data is local currency. Source: S&P Global Ratings.

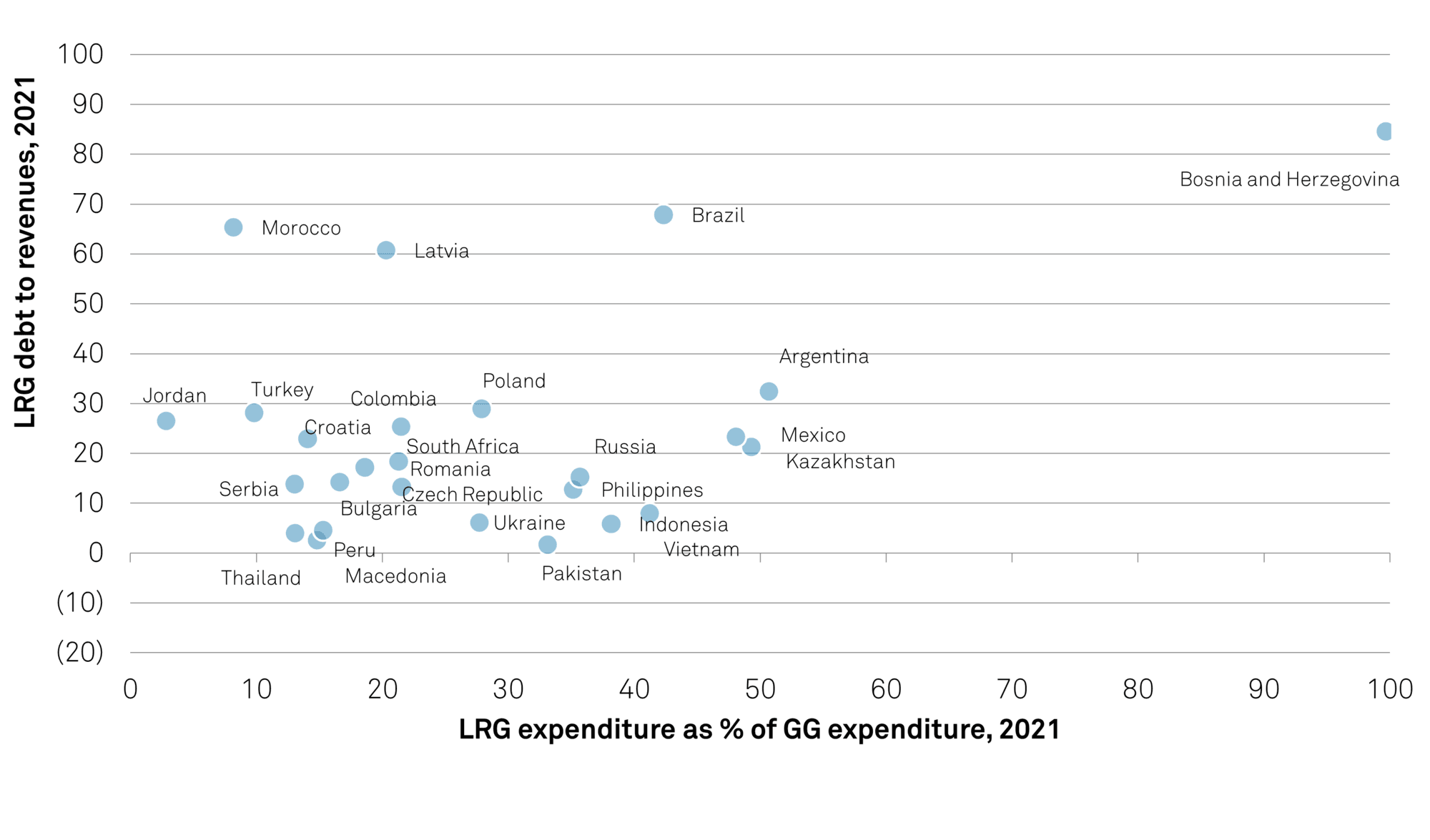

Still, we think there's room to increase borrowing in many EMs given that LRG debt doesn't usually represent a large burden on the local budgets, and LRG spending doesn't largely contribute to national spending to address infrastructure needs, because it represents a small portion of general government expenditure. For most of the EM countries in this report, LRG debt represented less than 30% of total revenue in 2021 and less than 50% of general government (GG) expenditure (see chart 6).

While we believe there is space for additional borrowing, we also analyze capacity for LRG debt intake holistically. We consider debt levels and institutional factors; the government’s capacity to maintain a healthy fiscal position that allows for debt repayment; and the administration’s ability to manage debt and liquidity, weather potentially adverse economic conditions, and have continued access to external sources of funding.

If LRGs pursued their implied capacity to borrow, we estimate they could absorb an additional debt capacity of between $50 billion and $250 billion, especially Poland, Romania, Czech Republic, and Colombia. Our estimate considers LRG debt levels, the level of decentralization in the country as a sign of capacity (how much LRG spending makes up total GG spending), institutional framework considerations including the ability to access the capital market and borrow in foreign currency, and the sovereign rating, which signals macroeconomic challenges and potential risks for subnational governments.

Borrowers that rely on external financing are likely to see rising financing costs, and higher interest rates could also pressure currencies

Although we think there's room in borrowing capacity, we also consider that subnational governments face restrictions on types and amounts of debt they can issue or borrow (refer to Appendix Table 2):

Chart 7 | EM LRGs Could Absorb U.S. $50-250 Billion In Debt

Source: S&P Global Ratings.

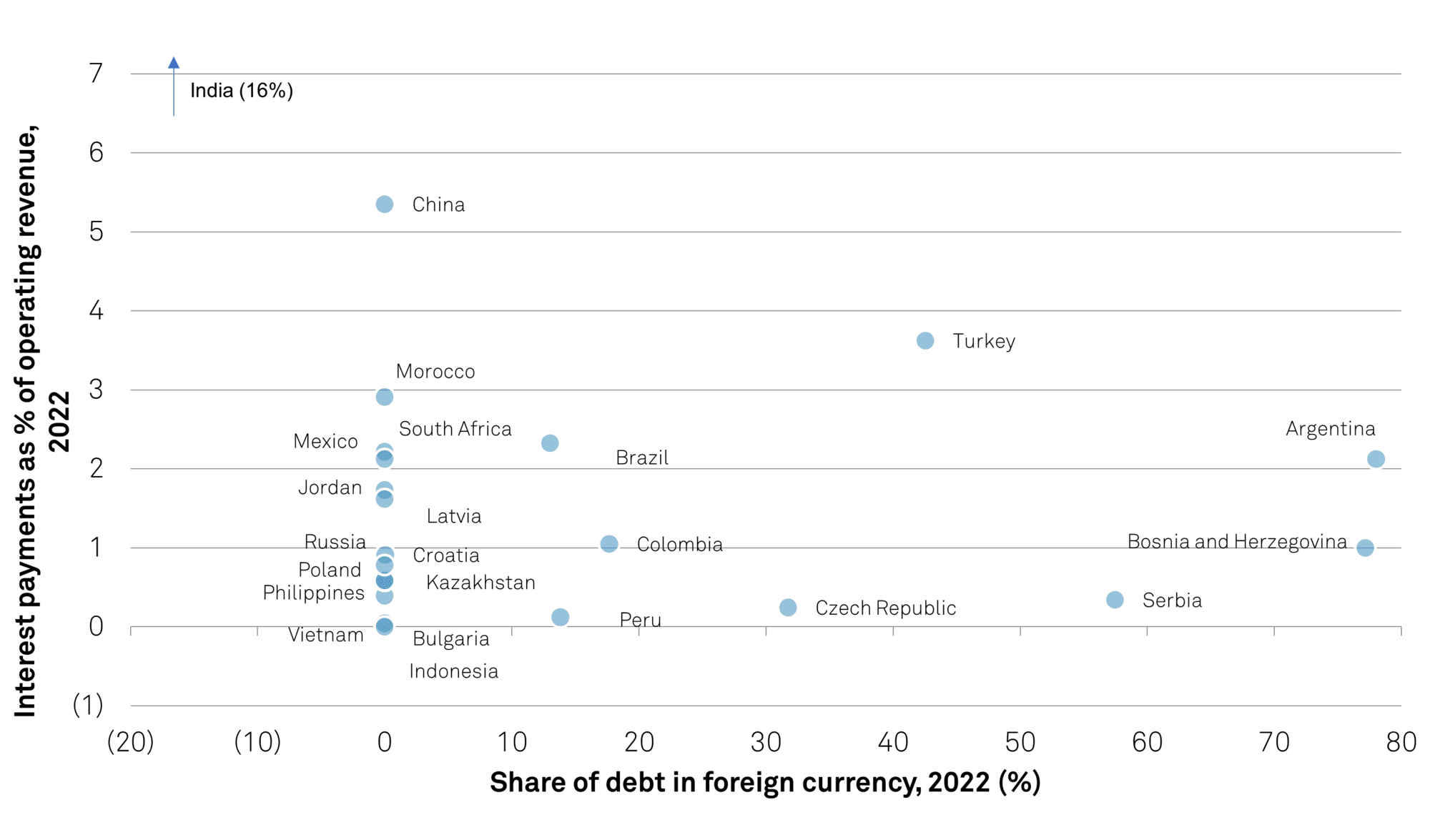

Interest rates in developed markets will start to rise in 2022, while the rate hikes have already started in EMs. Borrowers that rely on external financing are likely to see rising financing costs, and higher interest rates could also pressure currencies. Thus, vulnerability to this risk can be reflected in LRGs' share of foreign currency debt and how much interest payments weigh on the budget (as a percent of operating revenue).

Most EM countries have no foreign currency debt (60% of countries in this report). However, Argentine and Turkish local governments will be more exposed due to higher exposure to foreign currency in their debt stock of 78% and 43%, respectively, along with moderately higher interest payments versus other countries. While Indian LRGs don't have any foreign currency debt, interest payments represent 15% of operating revenue. Budgetary pressure in this case could increase in the event of interest rate hikes, but may be mitigated by India’s monetary policy, which tends to be anchored by domestic economic conditions rather than global factors (i.e. a Fed rate hike). In addition, we think the high inflation and the RBI's strong implicit support for state bonds will mitigate budgetary impact on states if monetary policy in India turns hawkish.

Chart 8 | Turkey And Argentina Will Be The Most Vulnerable To An Increase In Fed Interest Rates

Data in local currency. Source: S&P Global Ratings.

Meanwhile, the direct effects from rising inflation on EM local governments' financials will depend in part on the level of spending and debt repayment indexation. While inflation in the long term could result in economic and financial distortions, in the short term we think LRGs' fiscal positions could benefit from the effects, depending on how and when increases in prices lead to higher revenue and expenditure.

Table 1 | Gross Borrowings And Projected Debt Of LRGs In Select EM Countries

Table 2 | Statutory Limits On LRG Borrowing In Select EM Countries

Y--Yes. N--No. FX--Foreign exchange. DS--Debt stock. CG--Central government. Source: S&P Global Ratings.

Secondary Contacts

Susan Chu Hong Kong 852-2912-3055

Noa Fux London 44-20-7176-0730

YeeFarn Phua Singapore +65-6239-6341 Yotam Cohen RAMAT-GAN Martin J Foo Melbourne +61-3-9631-2016

Omar A De la Torre Ponce De Leon Mexico City +52-55-5081-2870

Alejandro Rodriguez Anglada Madrid +34-91-788-7233 Manuel Orozco Sao Paulo +55-11-3039-4819