This report does not constitute a rating action

Primary Credit Analysts

Felix Ejgel London +44-20-7176-6780

Noa Fux London +44-20-7176-0730

The post-COVID-19 economic recovery, alongside waning government support and related additional costs, will lead to lower local and regional government (LRG) borrowings in developed markets (DM).

We expect LRGs will increase spending to meet rising long-term infrastructure needs and promote the green agenda.

We anticipate that DM LRGs will remain reliant on capital markets, with bond issuances expected to account for about 75% of gross borrowings in 2022.

In our view, borrowings may increase beyond our forecast due to high inflation and slower than previously projected economic growth, amplified by the Russia-Ukraine conflict.

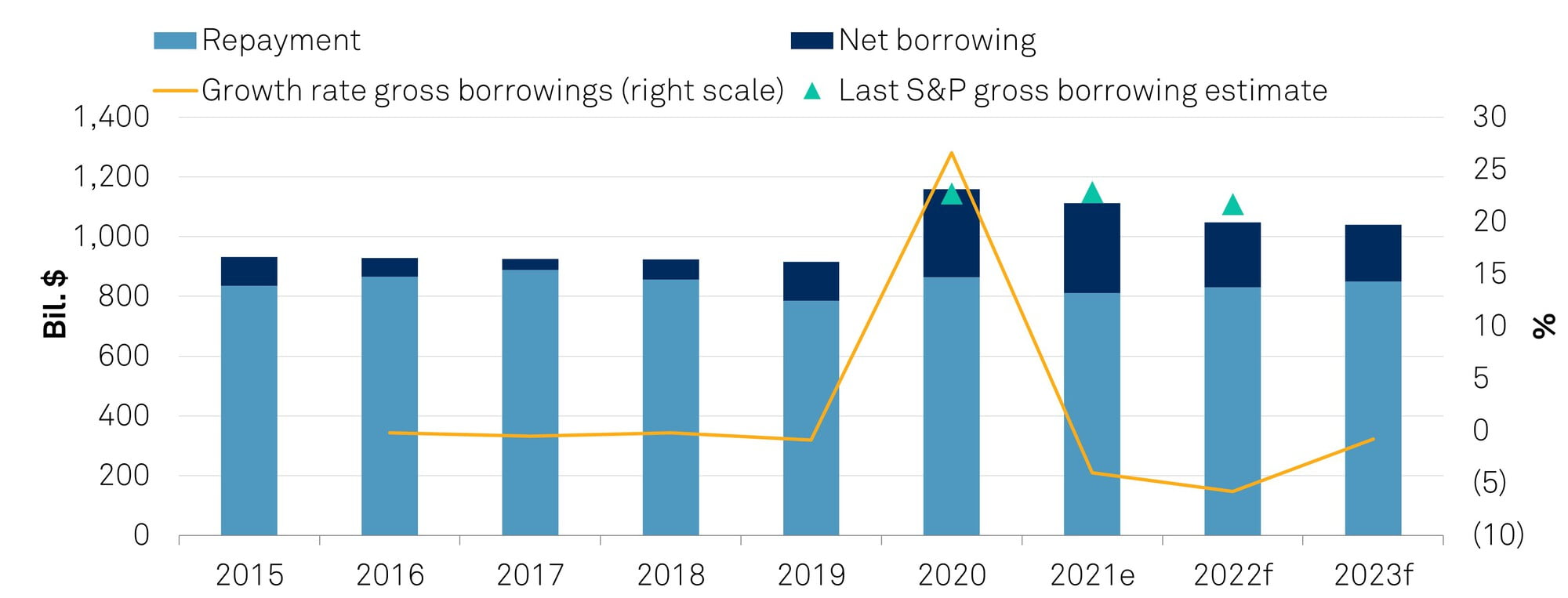

S&P Global Ratings projects that a post-pandemic economic recovery in developed markets (DMs) will lead to lower local and regional government (LRG) borrowings than in previous years.

Reduced pandemic-related risks will allow subnational governments to shift their focus to longer-term issues, such as demographic trends, investments in infrastructure, and the decarbonization agenda. In turn, we anticipate gross borrowings will decline this year, before stabilizing at about $1 trillion, which is still about 15% higher than pre-pandemic (see chart 1).

Chart 1 | Developed Market LRG Gross Borrowings Will Remain Above $1 Trillion In 2022-2023

e--Estimate. f--Forecast. Source: S&P Global Ratings.

However, we see increased risks to our base-case forecast from higher inflation and slower economic growth, exacerbated by the Russia-Ukraine conflict. Pandemic-induced disruptions to global trade and supply chains have already increased prices worldwide. Although inflation often helps LRGs balance their budgets in the short term due to higher revenue, the subnational cost base is quite rigid. In the long term, increasing wage pressure and costs of providing services, at a time of slower economic growth, might not be balanced by a rising tax base. Furthermore, material and labor shortages could result in delays and cost overruns on existing infrastructure projects.

We anticipate gross borrowings will decline this year, before stabilizing at about $1 trillion, which is still about 15% higher than pre-pandemic.

European LRGs are likely to be hardest hit by the effects of Russia's invasion of Ukraine, particularly if there is an accelerated timetable to reduce reliance on fossil fuels, which would require increased investments in housing and transport. Some countries may also reconsider the pace at which subnational deficit restrictions and budget consolidation targets are reintroduced, which will eventually result in higher debt. That said, more EU funds may become available for LRGs than incorporated in our forecasts.

Regional governments in federal countries, primarily Australia and Canada, and to some extent Belgium, will see continued fast debt intake due to their large capital programs. In contrast, we expect Germany and Austria will likely progress more toward budget consolidation after applying expansionary countercyclical fiscal policy during the pandemic to support their local economies and employment levels.

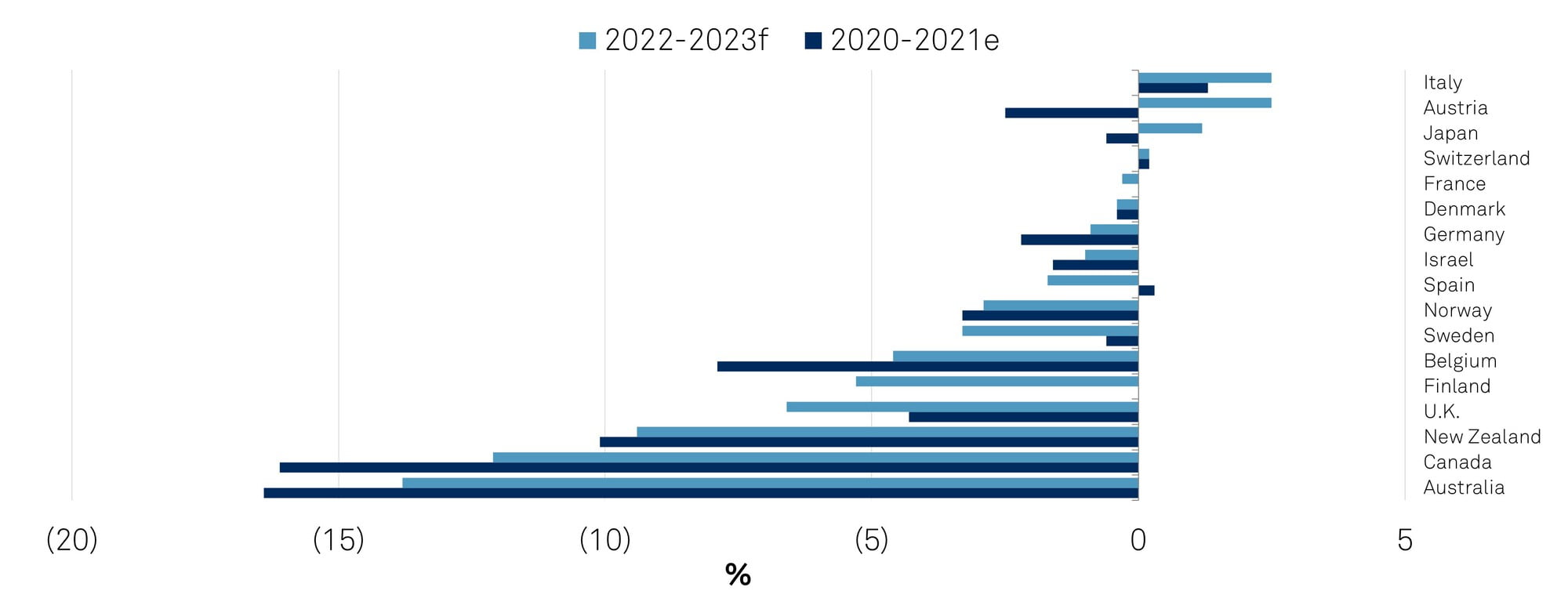

Subnational budget deficits in unitary countries remain more modest overall, although we expect borrowings to pick up in 2022 as the generous government support during 2020-2021 winds down (see chart 2). This, together with rising populations in the Nordics (Denmark, Finland, Norway, and Sweden), an infrastructure backlog in France, Japan, and the U.K., and the delayed budgetary impact in Spain, will likely expand subnational deficits post-pandemic.

Chart 2 | Most Subnational Governments Are Set To Shrink Their Funding Gap Budget balance to revenue

Note: Fiscal year in Australia ends on June 30, in Canada and the U.K. March 31. e--estimate. f--Forecast. Source: S&P Global Ratings.

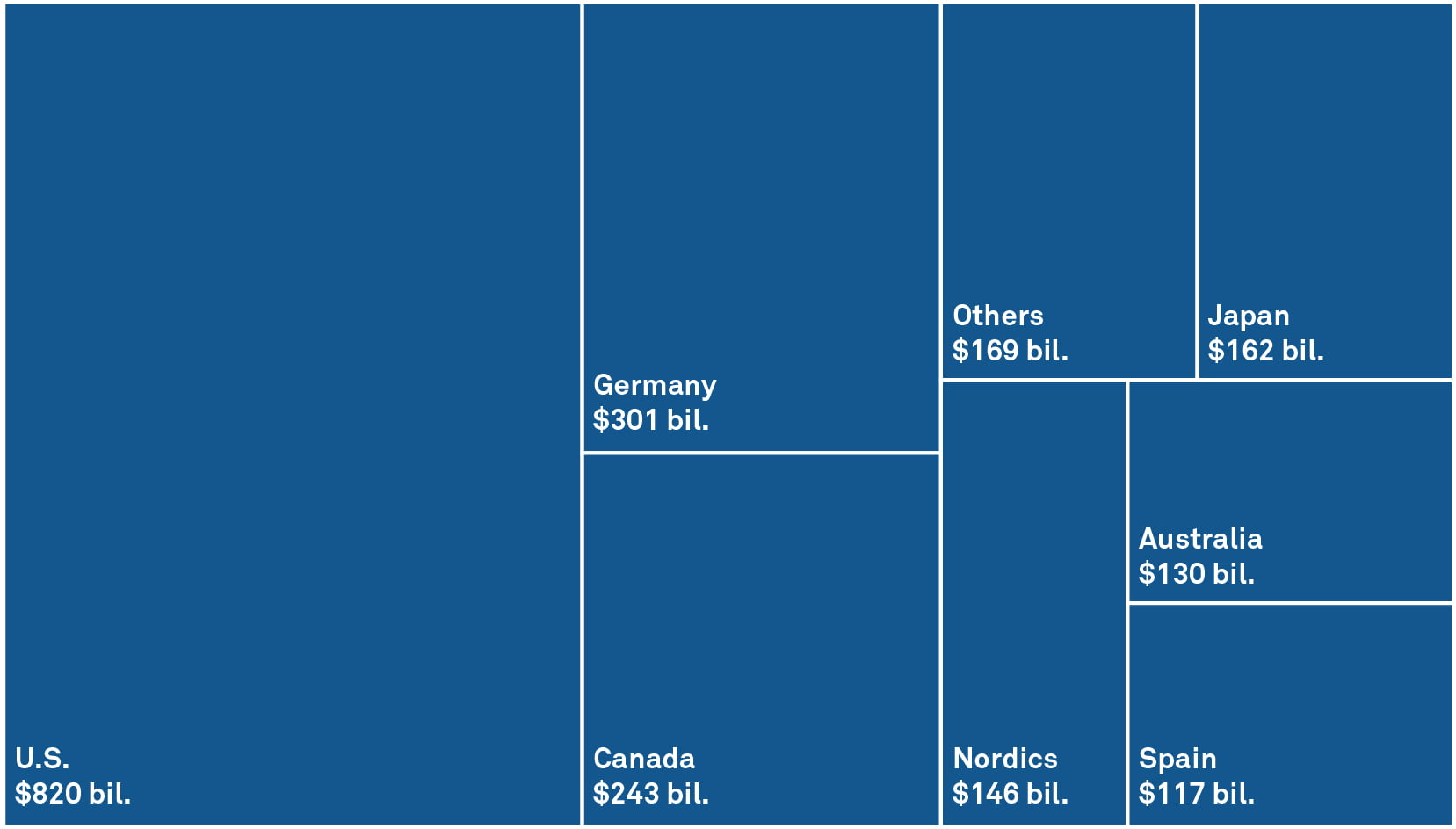

In the U.S., where inflation was already at a 40-year high in January 2022, we expect the highest nominal gross borrowings, albeit with a modest 2% increase.

Outside the U.S., we expect Germany’s gross borrowing to be the highest, although it will likely decrease to pre-pandemic levels (see chart 3). COVID-19-related borrowing requirements spurred extraordinary issuance volumes in 2020 and, to a much lesser degree, in 2021. We anticipate Germany's solid fiscal revenue growth will continue, following a V-shaped recovery in tax revenue last year, supporting budget consolidation efforts. In turn, we predict that the combined annual gross borrowing of German states, state-sponsored winding-up agencies for former public-sector banks and other state-guaranteed financing vehicles, and municipalities will fall further in the next two years.

We see increased risks to our base-case forecast from higher inflation and slower economic growth, exacerbated by the Russia-Ukraine conflict.

We expect a similar trend in Canada, supported by a stronger economic recovery at the provincial level and improved fiscal outcomes. These will temper projected borrowing by Canadian LRGs overall in fiscal 2022 and, to a lesser degree, 2023. The pandemic’s effects on income statements will take longer to unwind, such that borrowing will primarily be used to refinance maturing debt. However, debt will also remain fueled by operating deficits at the provincial level and deficits after capital accounts overall.

Although Australian LRGs' gross borrowings will be lower nominally than those in Germany and Canada, we expect the fastest increase in debt stock. With little direct government support, Australian LRGs' budgets were hit harder than those of DM peers during the pandemic. Going forward, we expect the states will ramp up investments in large infrastructure projects, in line with their long-term financial plans.

Chart 3 | The U.S., Germany, And Canada Will Continue To Dominate Subnational Borrowings In 2022-2023

LRG--Local and regional governments. Source: S&P Global Ratings.

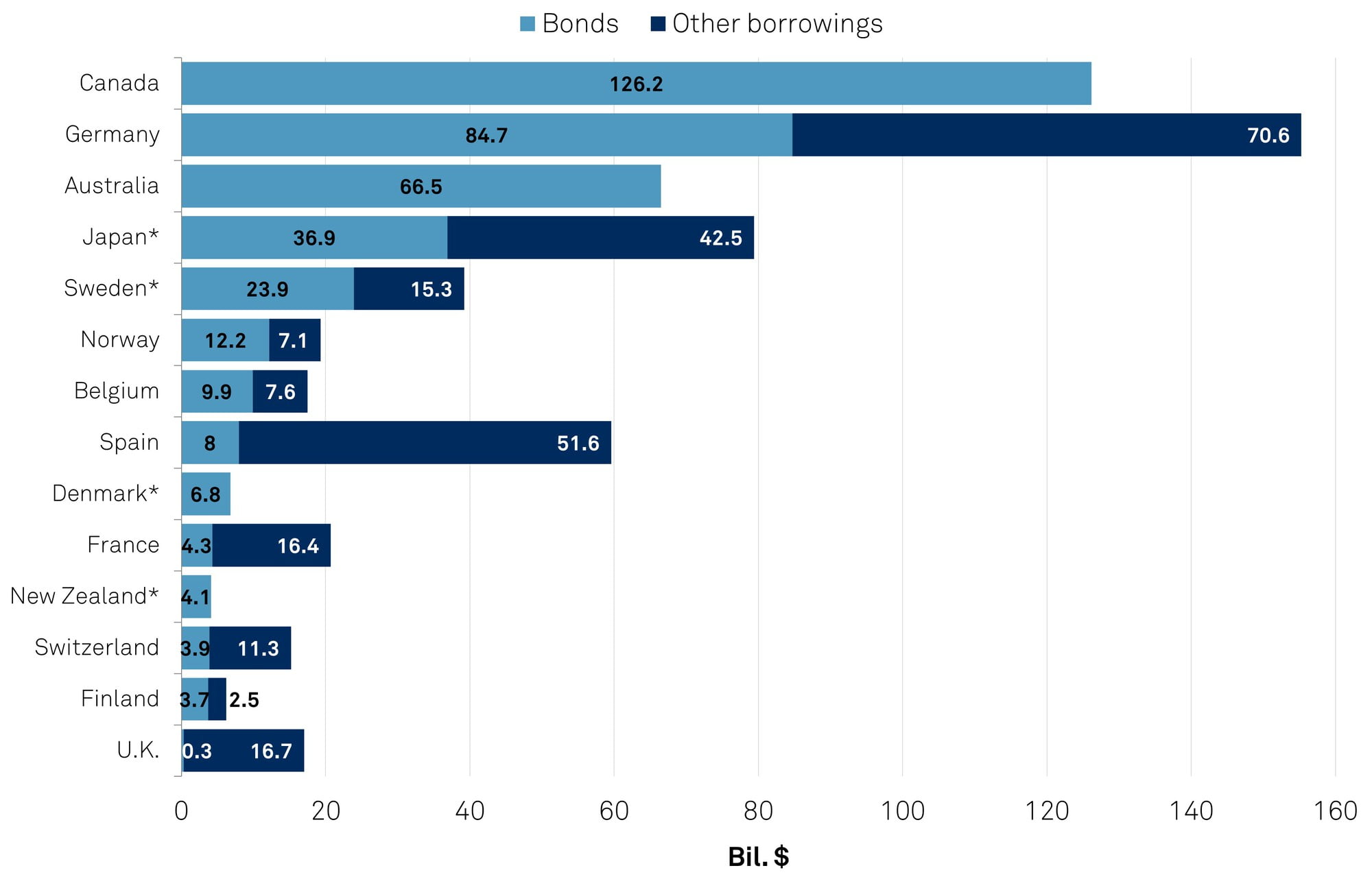

Globally, funding for DM LRGs is dominated by bonds, although sources vary by country. We expect subnational DM bond issuances to reach the equivalent of $800 billion in 2022, which would cover close to 75% of LRGs' funding needs. Overall, we think the funding environment remains favorable for subnational borrowers, with low, albeit increasing, interest rates globally to help absorb rising funding needs.

About half of the expected LRG bond issuances in 2022 will come from the U.S. followed by Canada, Australia, and Germany (see chart 4).

Chart 4 | Only Australian States And Canadian Provinces Rely Solely On Bonds 2022 forecast

Note: Data includes bonds issued through public sector funding agencies. Source: S&P Global Ratings.

Although most LRGs raise debt directly, those in the Nordics and New Zealand mostly refinance via public-sector funding agencies (PSFAs). Japanese LRGs also benefit from access to Japan Finance Organization for Municipalities (JFM; a PSFA) lending, as well as the large domestic banking sector and the central government’s direct lending scheme. In most cases, LRGs place bonds domestically and in local currency, while PSFAs, Australian states, and some Canadian provinces place bonds in different currencies. Canadian provinces, Australian states, and U.S. public-sector entities also rely entirely on capital markets.

In contrast, Austrian, Italian, and U.K. LRGs cover almost all their funding needs by borrowing from the central government and its agencies. Most Italian subnational borrowings in recent years were 30-year liquidity anticipations from state lending arm Cassa Depositi e Prestiti to fund arrear payments. We expect these will still be used for this purpose and to fund long-term investments. Until recently, U.K. LRGs covered most of their funding from the government's Public Works Loan Board (PWLB). However, due to still-low interest rates and additional constraints imposed on borrowings through PWLB for commercial activities, we may see some shift toward other sources.

We also forecast increasing adoption of green and sustainable bonds by DM LRGs, given the increasing emphasis on the decarbonization agenda. Large issuers, such as the Canadian province of Ontario and German state of North Rhine-Westphalia issued green or sustainability linked bonds previously. They were joined by Tokyo Metropolitan Government, which issued Japan’s first ever municipal social bond in 2021. Some smaller LRGs are also testing the markets, with Swedish municipality Helsingborg issuing a sustainability-linked bond and French region Ile-de-France issuing green bonds. We expect that sustainably linked or green debt will become more common as LRGs' primary responsibilities and investment programs mean most are eligible.

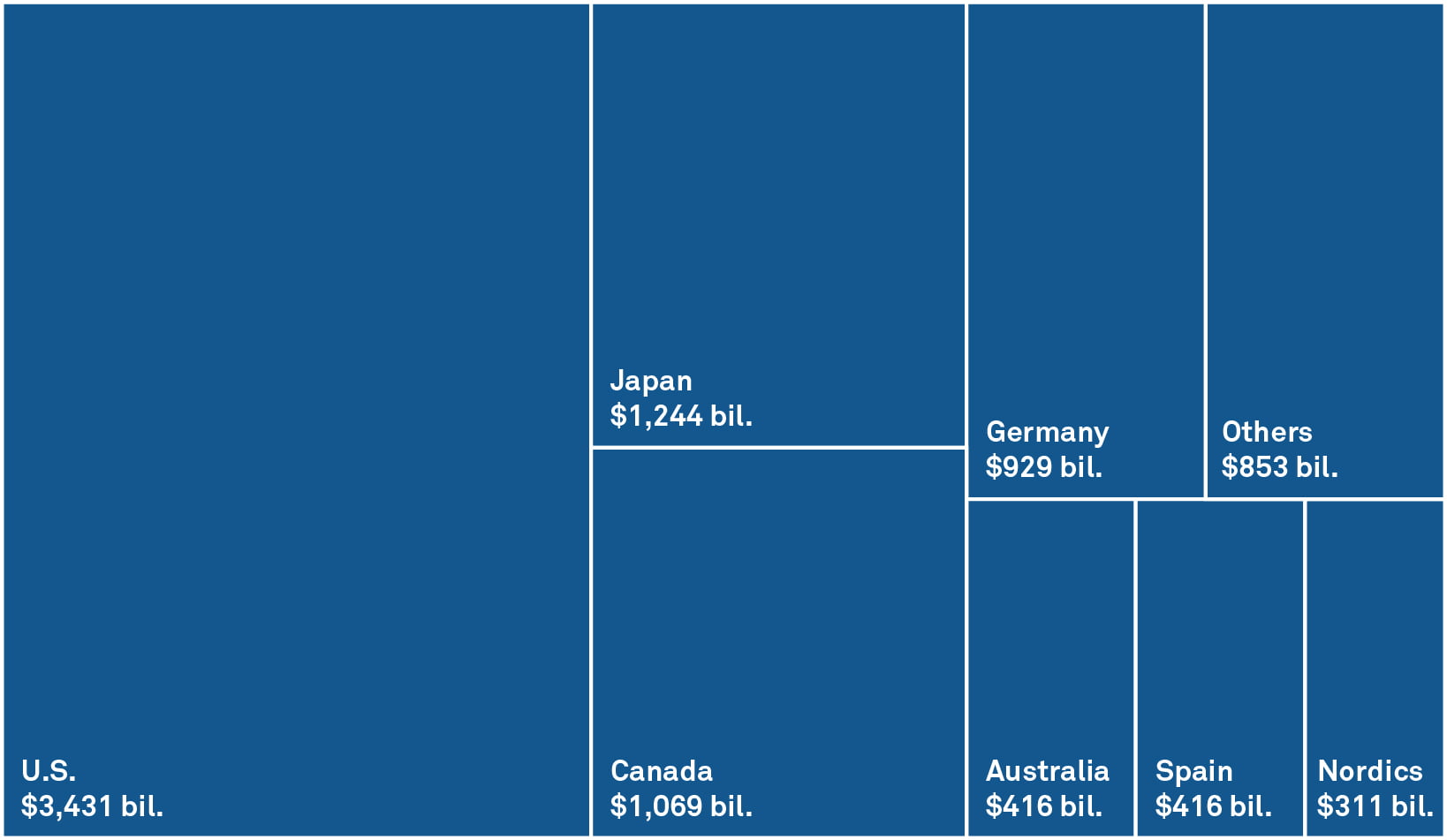

Elevated borrowing will lift DM LRGs' outstanding debt to a record high of over $8.7 trillion by year-end 2023. The global LRG debt stock remains very concentrated, with the U.S. accounting for about 40% of DM subnational debt, followed by Japan, Germany, and Canada at just under 40% combined (see chart 5).

Elevated borrowing will lift DM LRGs' outstanding debt to a record high of over $8.7 trillion by year-end 2023.

Chart 5 | Canada And Germany Are Catching Up With Japan's Subnational Debt Levels 2023 forecast

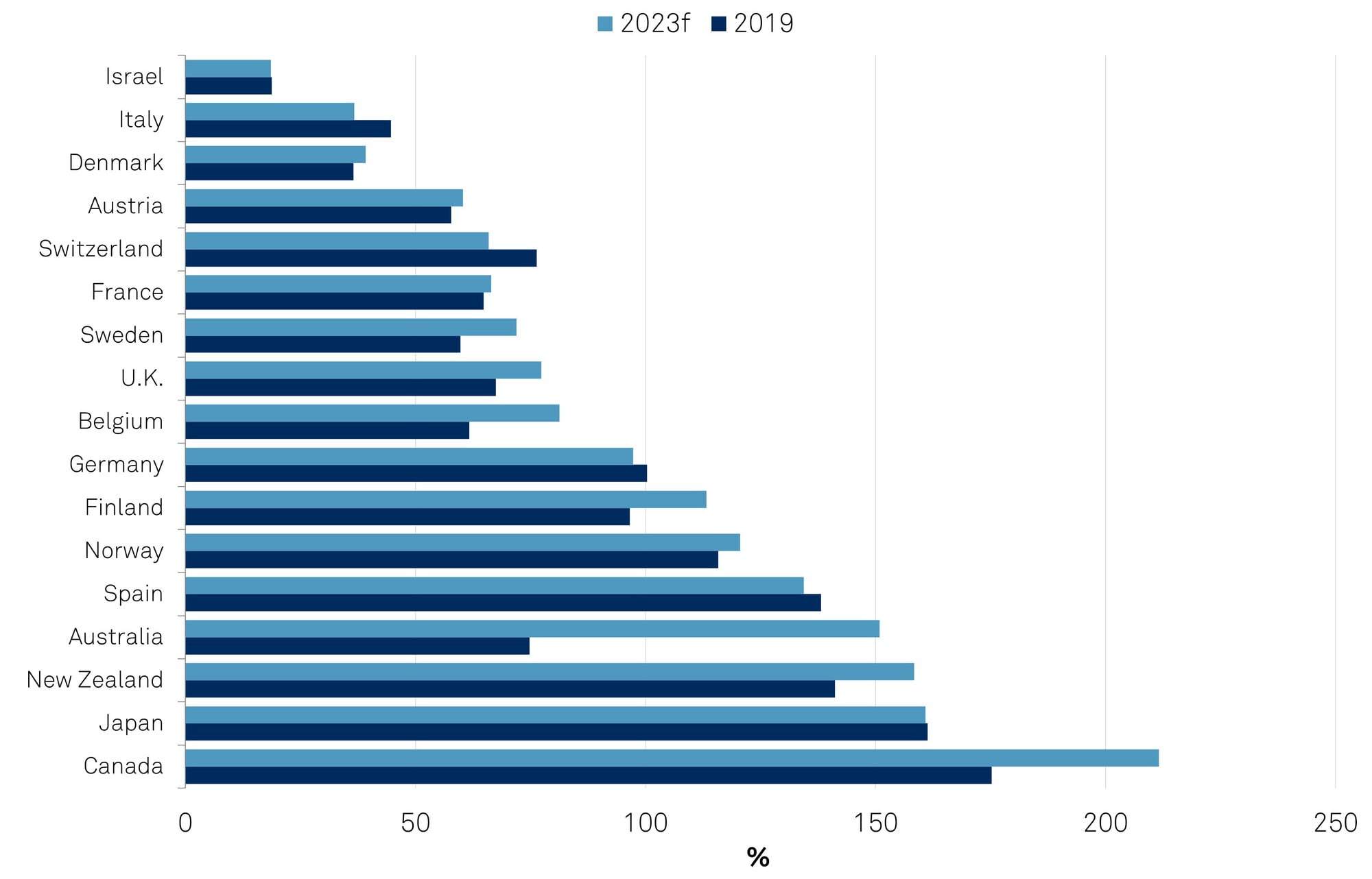

Outside the U.S., DM LRG debt is expected to average about 115% of total revenue in 2023. Canadian LRGs will remain the most indebted globally, with debt to revenue exceeding 210% by year-end 2023, followed by Japan, Spain, and Australia (see chart 6). Canada and Australia have recorded the biggest debt burden change from pre-pandemic.

Chart 6 | Subnational Debt Burden Will See The Fastest Increase In Australia And Canada Debt stock to revenue

f--Forecast. Source: S&P Global Ratings.

Table 1 | Annex

Our survey on DM LRG borrowing encompasses 18 countries: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Israel, Italy, Japan, New Zealand, Norway, Spain, Sweden, Switzerland, the U.K., and U.S. We consider this sample representative of DM LRG debt.

We base our survey on data collected from statistical offices, as well as on our assessment of the sector’s borrowing requirements and outstanding debt, which includes bonds and bank loans. The reported figures are our estimates and do not necessarily reflect LRGs’ own projections. For comparison, we present our aggregate data in U.S. dollars.

Secondary Contacts

Bhavini Patel Toronto +416-507-2558

Jane H Ridley Centennial +1-303-721-4487

Alejandro Rodriguez Anglada Madrid +34-91-788-7233

Carl Nyrerod Stockholm +46-8440-5919

Anthony Walker Melbourne +61-3-9631-2019

Kensuke Sugihara Tokyo +81-3-4550-8475

Stephanie Mery Paris +33-14-420-7344

Thomas F Fischinger Frankfurt +49-693-399-9243

Michael Stroschein Frankfurt +49-693-399-9251