This report does not constitute a rating action

Primary Credit Analysts

Felix Ejgel London +44-20-7176-6780

Sarah Sullivant Austin +1-415-371-5051

Noa Fux London +44-20-7176-0730

Susan Chu Hong Kong +852-2912-3055

We project local and regional government (LRG) borrowings will stay inflated, at about $2.35 trillion per year globally in 2022-2023.

This will be supported by increasing refinancing needs of Chinese LRGs as well as infrastructure needs in Australia and certain other developed markets.

We estimate this will push total global LRG debt to a new peak of $16.1 trillion by 2023, with Indian and Canadian LRGs being the most indebted compared with the size of their budgets.

We expect LRGs in developed markets, China, and India to continue tapping the debt capital markets, while those in other emerging markets will stay away, maintaining unused capacity to borrow.

We see increased risks to our base-case expectations stemming from higher inflation and slower economic growth, amplified by the Russian invasion of Ukraine.

Persistent infrastructure needs, rising demand for services, high refinancing requirements, and reduced central government financial support will keep LRG borrowing high over the next two years. We estimate annual gross borrowing will reach over $2.4 trillion in 2023 (see chart 1). As a result, global subnational debt will reach a new record high of $16.1 trillion by the end of 2023--40% higher than pre-pandemic levels. Indian and Canadian LRGs will collectively remain the most indebted in the world in relation to their revenues, followed with a large gap by those in Japan, Australia, and New Zealand.

Chart 1 | Global LRG Borrowings Will Stay High In 2022-2023 After The Pandemic-Induced Surge

e--Estimate. f--Forecast. Source: S&P Global Ratings.

Our current forecast for new borrowings globally is slightly higher than our previous projection from March 2021, mainly driven by higher forecasts for Chinese LRG gross borrowings. We see heightened uncertainty surrounding global subnational borrowings, owing to higher inflation and slower than previously expected economic growth in North America and Europe, both exacerbated by the Russian invasion of Ukraine. In the short term, inflation often helps LRGs balance their budgets by increasing revenues, while spending lags behind. In the long term, however, increasing prices of typically rigid cost bases, at a time of slower economic growth might mean budgets will be more difficult to balance. Globally, and especially in Europe, the Russia-Ukraine conflict may also see central governments targeting accelerated reduction in reliance on fossil fuels. If implemented, this policy will increase demand for new energy and energy-saving investments in housing and transport. These developments could lead to looser restrictions on subnational deficits and hamper budget consolidation paths. For emerging markets (EM) in particular, the COVID-19 pandemic also continues to pose a risk to our forecast, although more moderately than previously.

Our estimate of annual gross borrowing by 2023

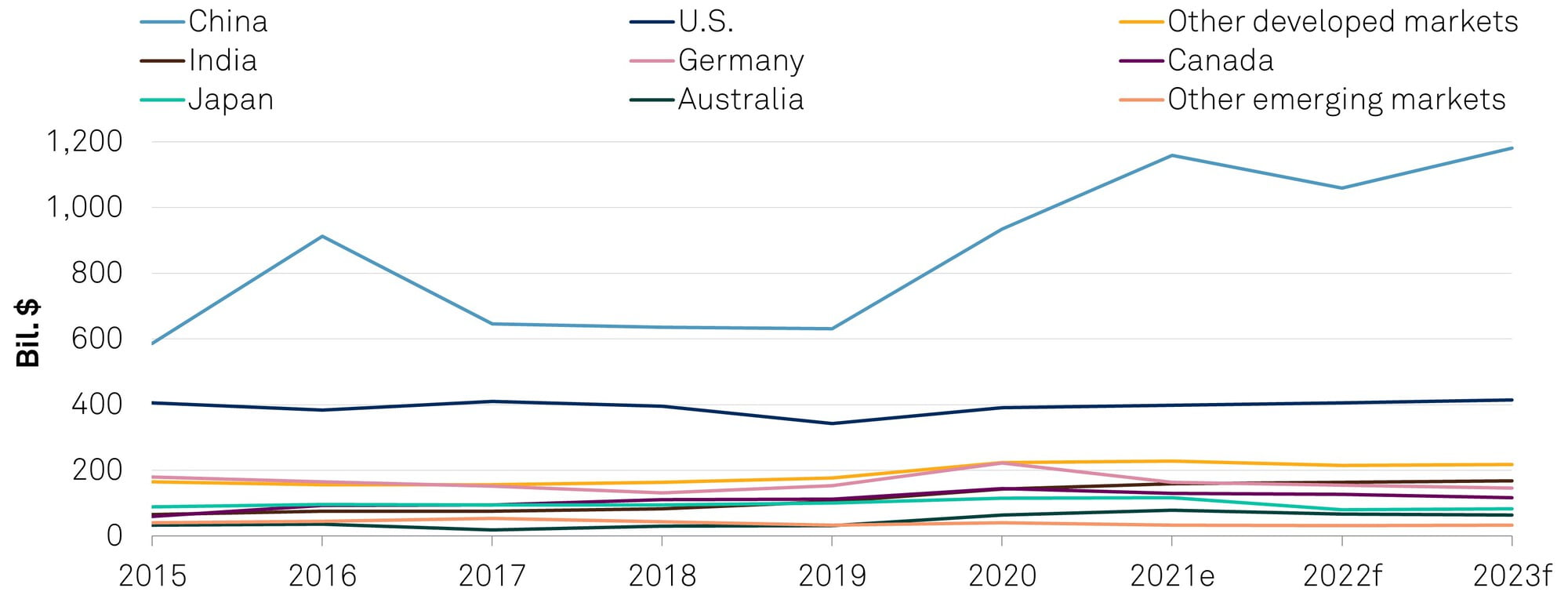

We expect subnational governments in Australia, Canada, and China to substitute the fiscal stimulus provided through the pandemic with rising spend on infrastructure (see chart 2). Together with refinancing needs, this will keep these governments' gross borrowing elevated. In India, we expect that sticky operating costs incurred during the pandemic will impact operating performance for longer, which will eventually push up the states' borrowing needs. By contrast, we expect gross borrowing to stabilize in German and Austrian states, as they work toward budget consolidation.

Chart 2 | China Continues To Drive Gross Subnational Borrowing

e--estimate. f--Forecast. Source: S&P Global Ratings.

Investments will also largely drive borrowings of local governments in other developed countries, although at a more modest pace (see charts 3 to 6). Extraordinary government support in many unitary countries shielded the impact on budgets and debt levels throughout the pandemic. As this support and related costs wind down, we expect some LRGs in these countries to resume their central role of delivering capital projects and investments in national infrastructure, which will drive up future borrowings.

We see heightened uncertainty surrounding global subnational borrowings, owing to higher inflation and slower economic growth in North America and Europe.

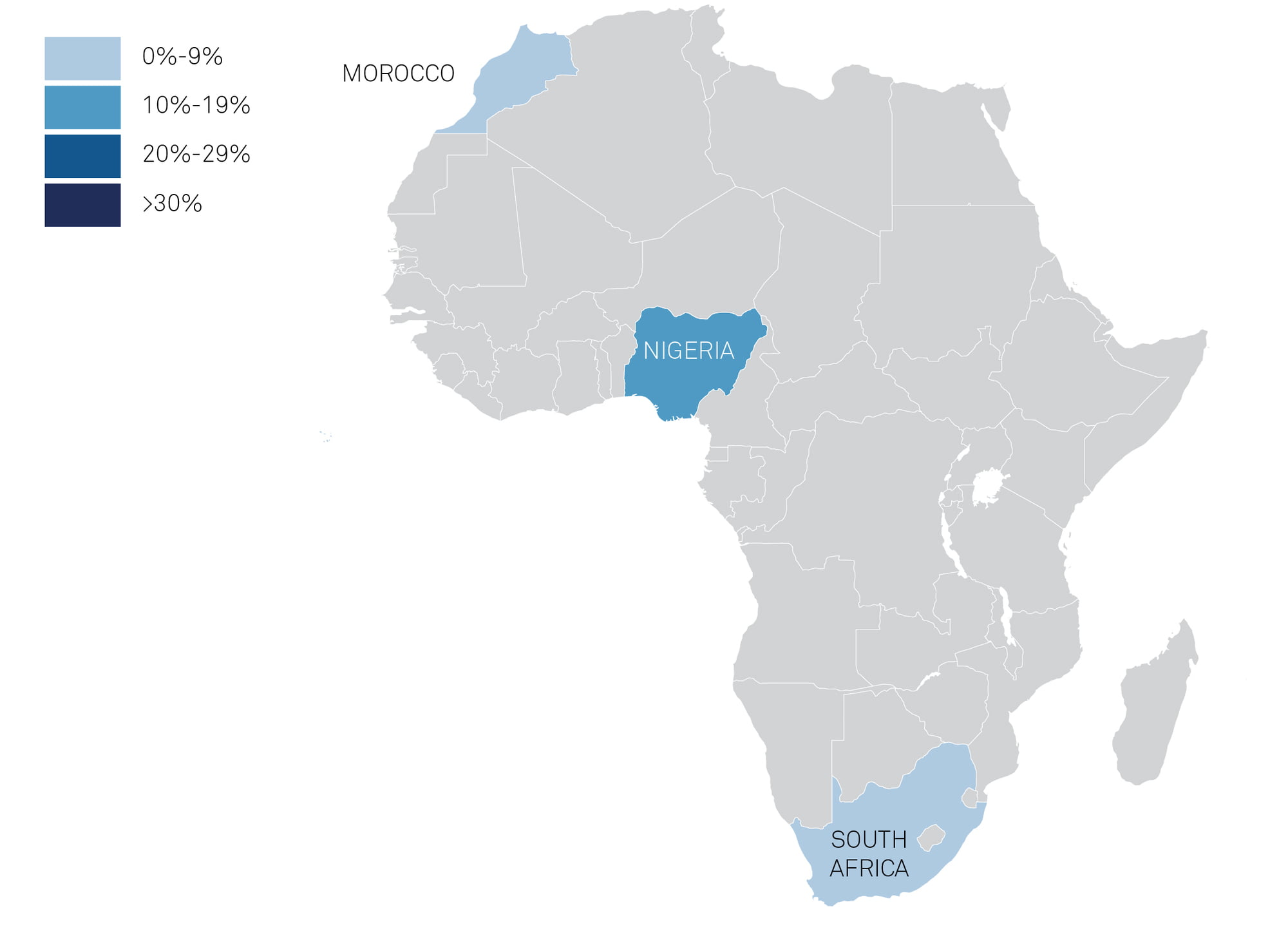

Beyond China and India, we expect borrowings in emerging markets to stay contained to refinancing needs. Although infrastructure investments increased in Europe during the pandemic, we expect many regional governments to scale back spending in real terms as the pandemic ebbs. The large infrastructure backlog and the continuous pressure on operating expenditures will also likely constrain subnational budget flexibility in Latin America. Executing local capital projects in the region is increasingly difficult, owing to poor access to financing, high procedural hurdles, and incentives that are not well aligned with undertaking long-term planning and investment.

Chart 3 | Africa Gross Borrowings As % of LRG total revenues, 2022

LRG--Local and regional governments. Source: S&P Global Ratings.

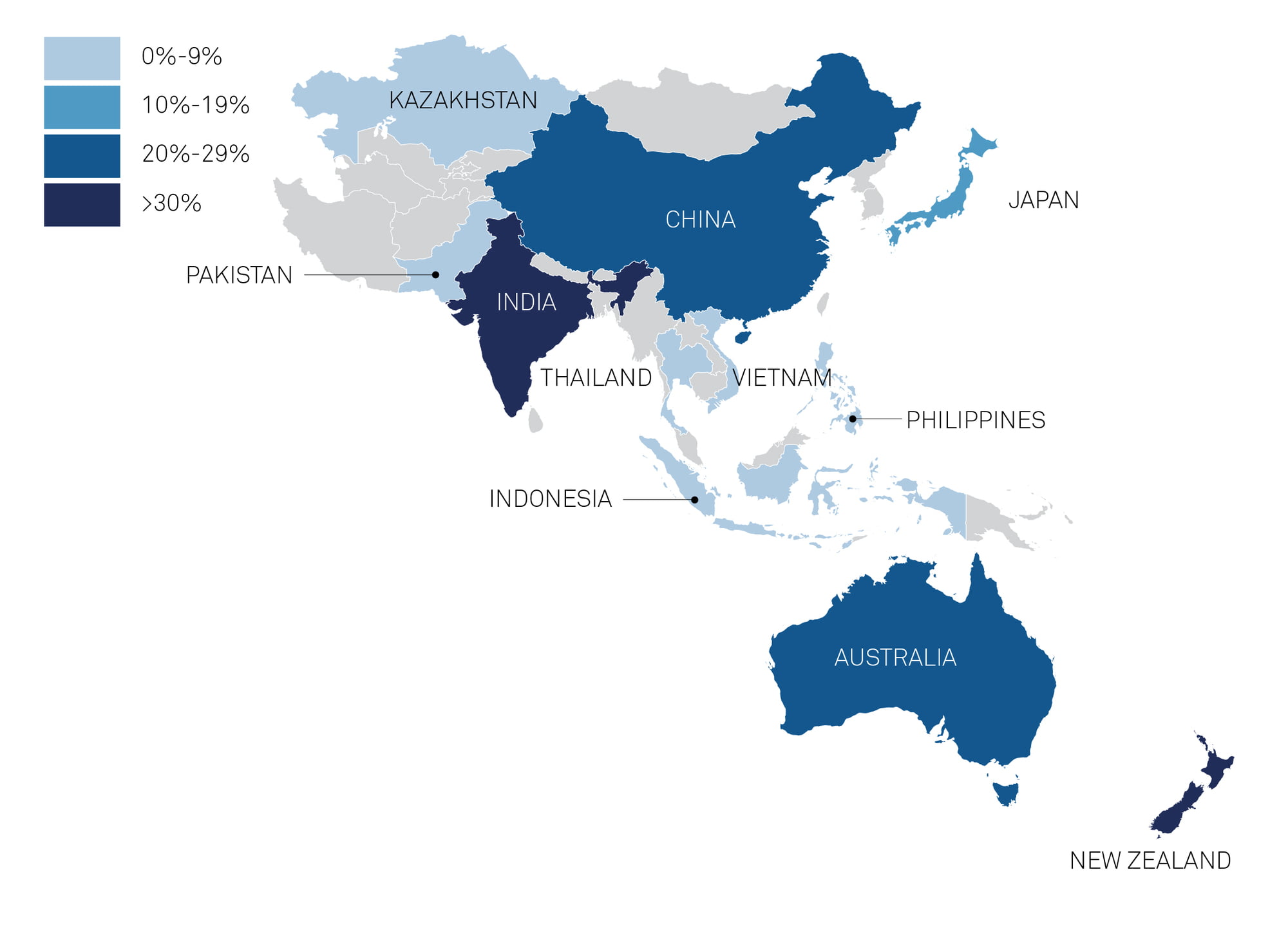

Chart 4 | Asia-Pacific Gross Borrowings As % of LRG total revenues, 2022

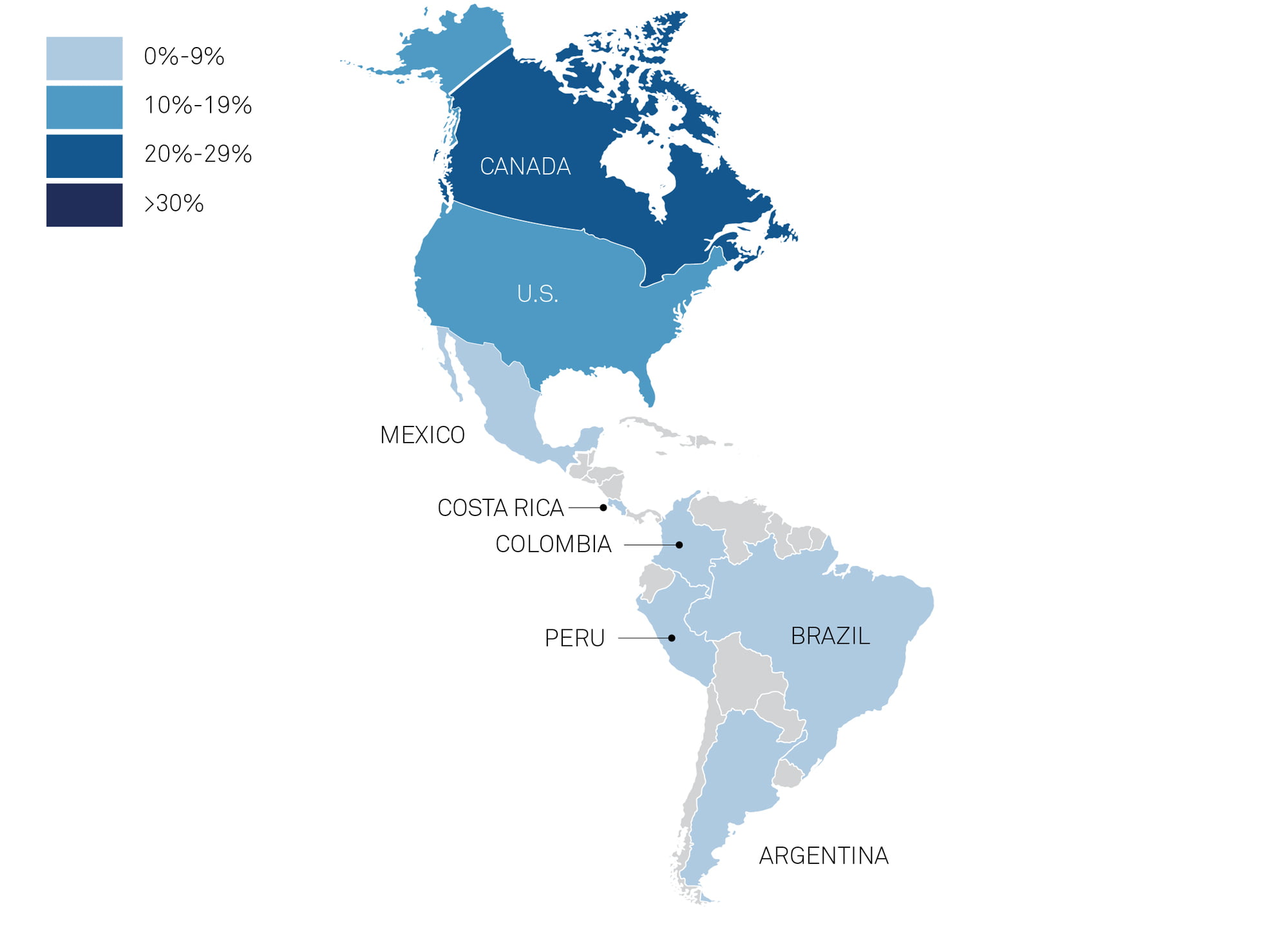

Chart 5 | Americas Gross Borrowings As % of LRG total revenues, 2022

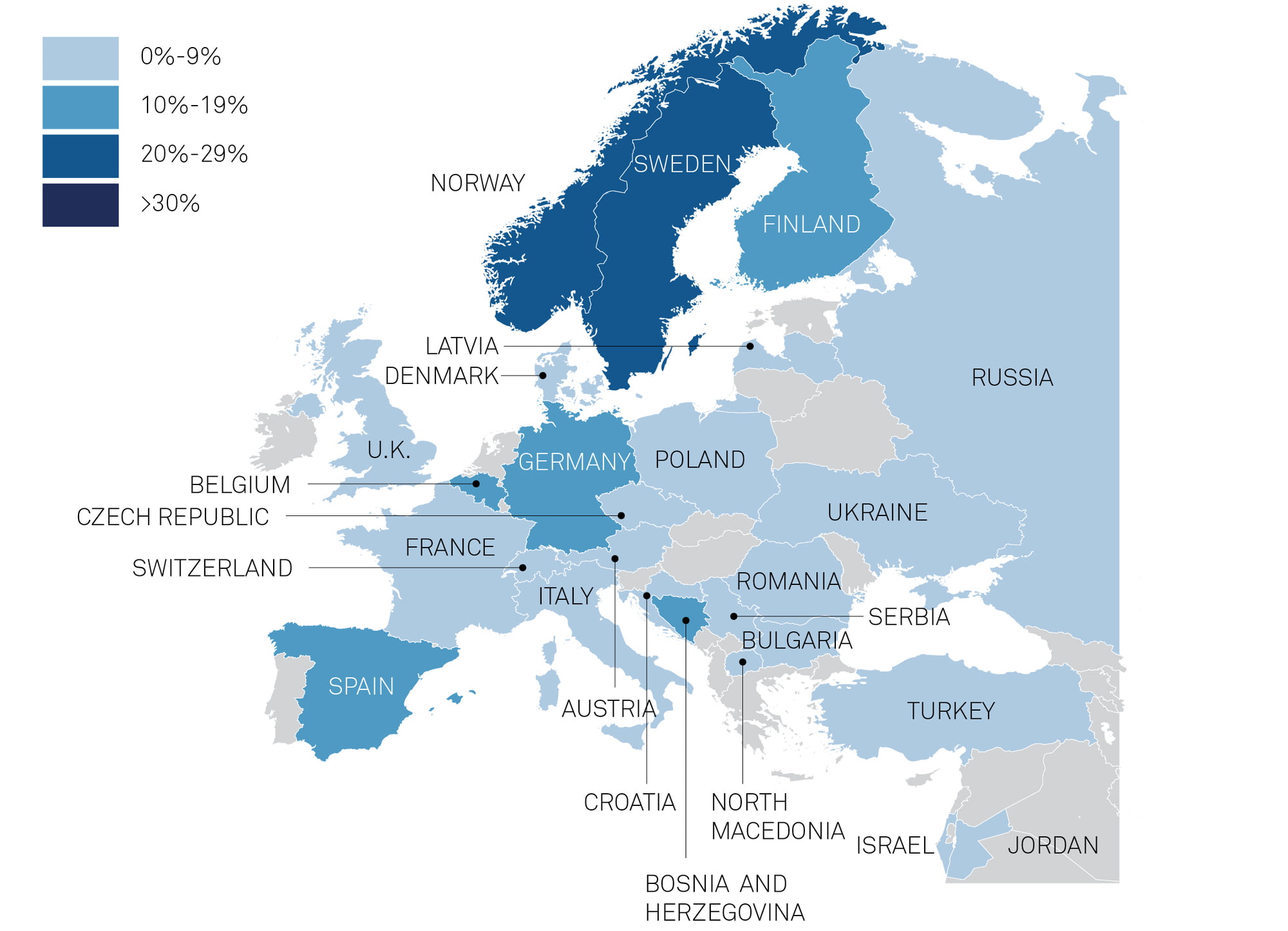

Chart 6 | Europe And Middle East Gross Borrowings As % of LRG total revenues, 2022

We anticipate global bond issuance will average $2 trillion per year in 2022-2023 and cover around 85% of LRGs' funding needs on average. This follows a new peak in bond issuance in 2021, when we estimate subnational bonds issuance will have reached close to $2.1 trillion. Issuances are expected to remain very concentrated, with around 55% of them placed by Chinese provincial governments, and around 20% by U.S. entities.

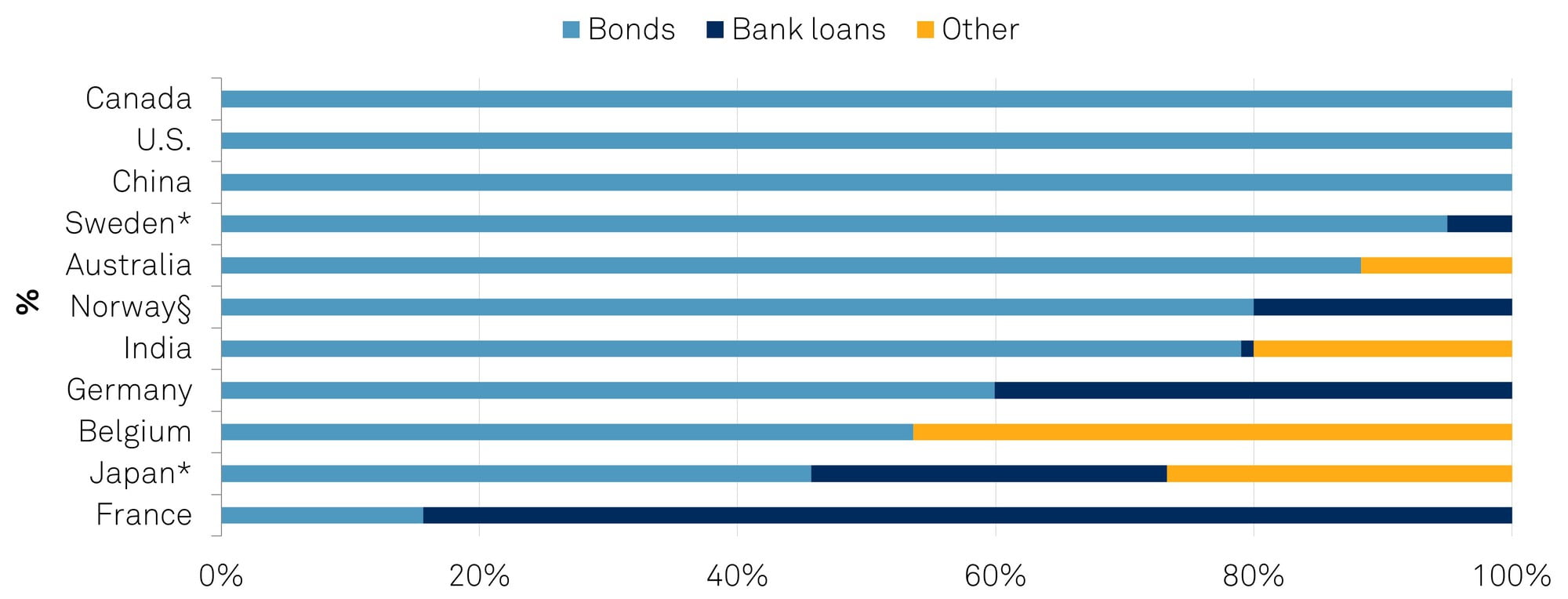

In developed markets, most LRGs raise debt directly, except in the Nordics, which typically use public sector funding agencies (PSFAs), as do some Japanese LRGs. In most cases globally, LRGs place bonds domestically in local currency, while PSFAs, Argentine provinces, some Canadian provinces and Australian states place bonds in different currencies. Chinese and Canadian provinces, Australian states, and U.S. public sector entities rely entirely on the capital markets (see chart 7). We expect that bond proceeds will cover more than one-half of Indian and German LRG borrowings, and over 40% of Japanese LRG borrowings will be issued through own-name bonds (excluding PSFA debt).

Chart 7 | Bonds Are Still The Dominant Funding Source For LRGs As % of total debt 2022f

*Loans from PSFAs (Japan Finance Organization for Municipalities and Kommuninvest) are viewed as bonds. §Loans from Kommunalbanken are viewed as bonds, whereas loans from KLP are viewed as bank loans.

In contrast, Austrian, Italian, and U.K. LRGs cover almost all their funding needs by borrowing from the central government and its agencies: Österreichische Bundesfinanzierungsagentur (OeBFA), Cassa Depositi e Prestiti, and the Public Works Loan Board, respectively.

In emerging markets, where stricter limitations on debt intake typically apply, most LRGs rarely tap the international capital markets. Chinese provinces may issue bonds in the international markets via local government funding vehicles (LGFV), while Indian states’ bonds are served by the Reserve Bank of India. We note, however, that bonds issued by Chinese and Indian LRGs are mostly owned by domestic investors. Only Argentinian provinces and several entities in Central and Eastern Europe have a track record of issuing bonds in foreign or domestic currency, available for global investors.

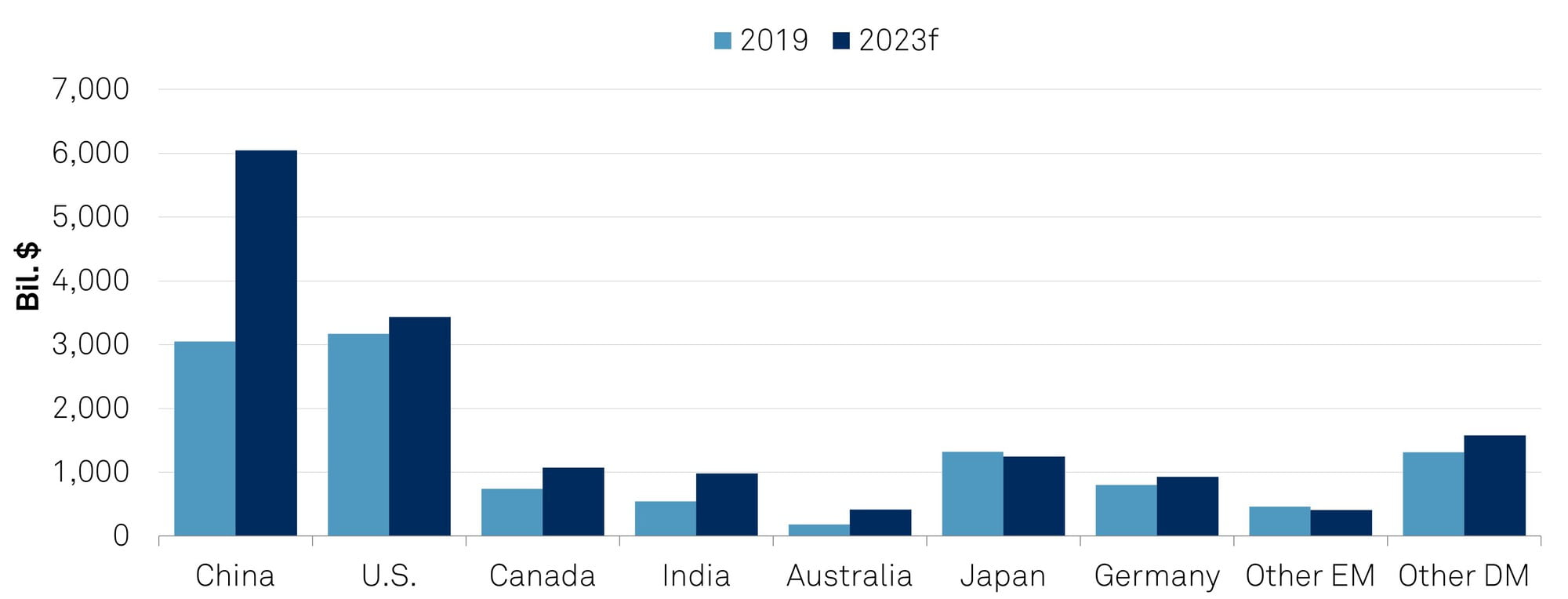

Increased borrowing will push global LRGs' outstanding debt to a record high of about $16.1 trillion by the end of 2023. Global LRG debt remains very concentrated geographically, with China and the U.S. comprising close to 60% of the global LRG debt stock by 2023 (see chart 8). Together, Japan, Canada, Germany, and India account for close to 25%.

Chart 8 | Chinese And Indian Subnational Debt Set To Double From Pre-Pandemic Levels

f--Forecast. EM--Emerging market. DM--Developed market. Source: S&P Global Ratings.

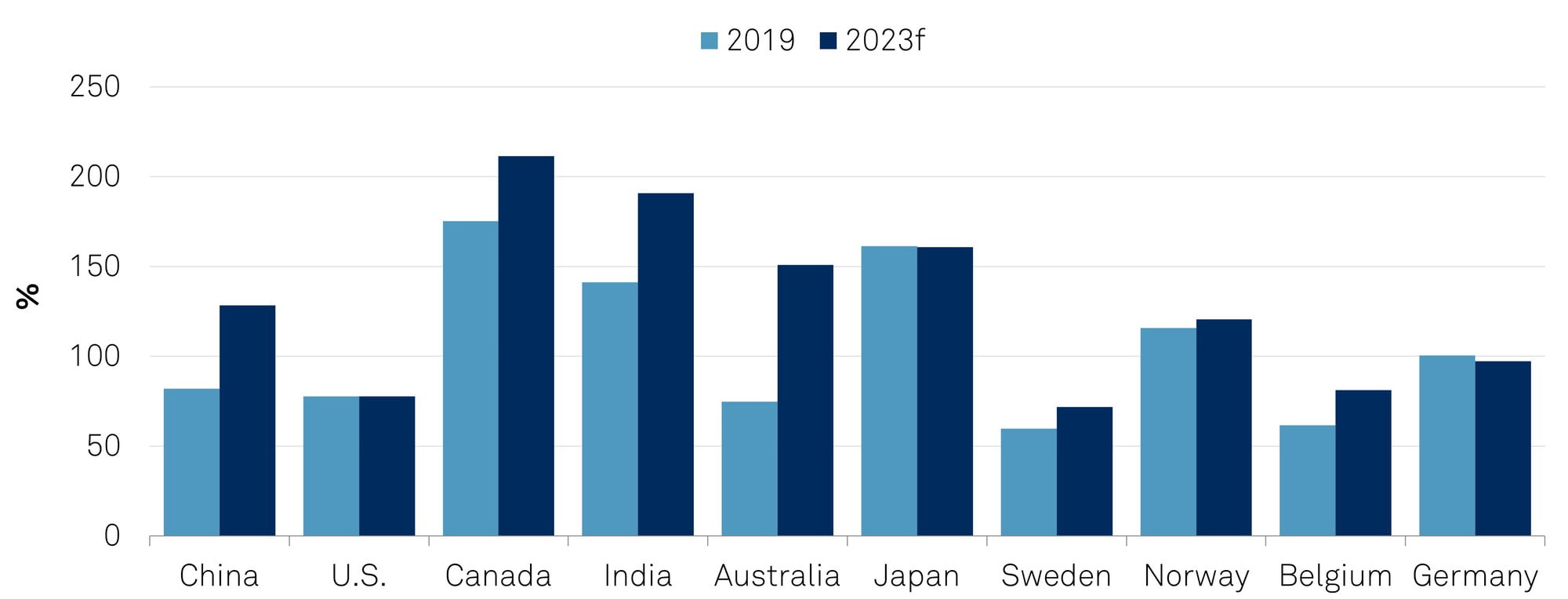

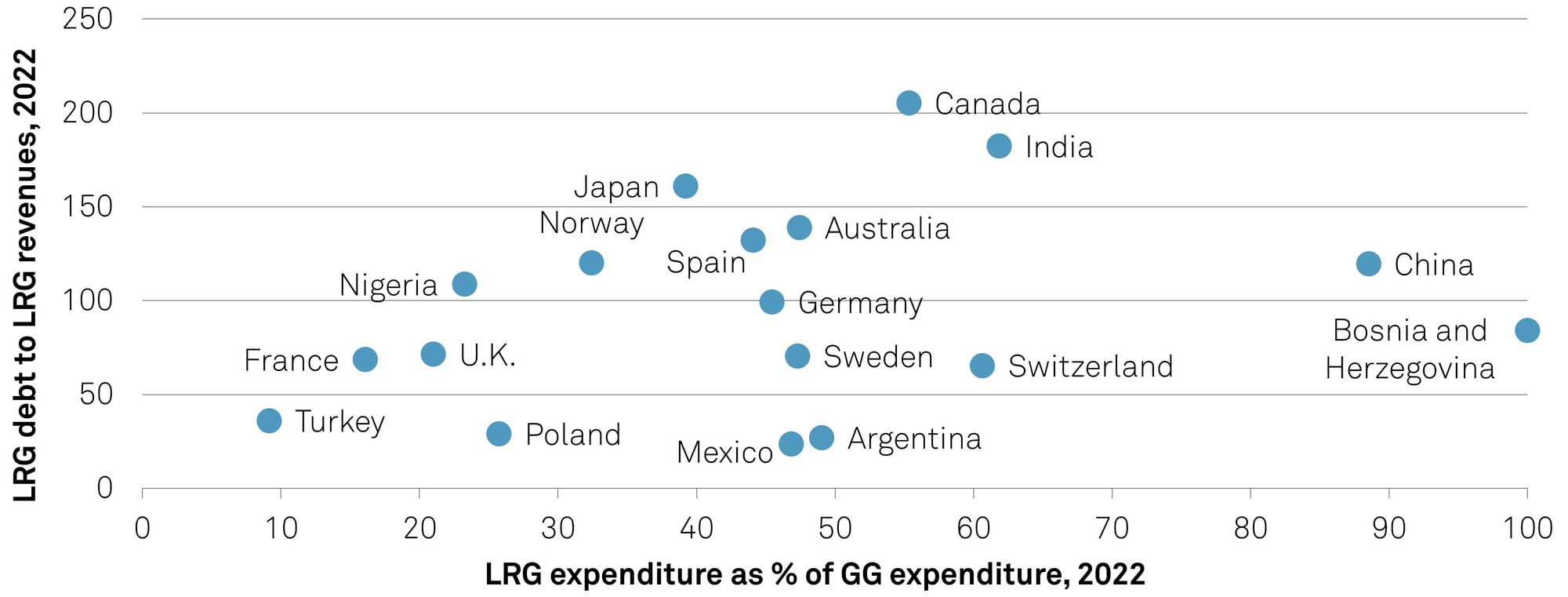

Collectively, Indian and Canadian LRGs will remain the most indebted globally, with debt to revenue of close to 200% (see chart 9) by the end of 2023. Compared with pre-pandemic levels, Australian indebtedness weakened the most, followed by the LRGs in Canada, China, and India. Despite rapidly increasing borrowings, the consolidated debt of Chinese LRGs (excluding LGFVs) still slightly lags that of peers, but including debt of key state-owned enterprises with high dependence on LRGs, would be comparable with that of Canadian peers.

Increased borrowing will push global LRGs' outstanding debt to a record high of about $16.1 trillion by the end of 2023.

Chart 9 | Canadian And Indian LRGs Are The Most Indebted

f--Forecast. Source: S&P Global Ratings.

Despite the projected increase in borrowings, we believe that many LRGs are underutilizing their borrowing capacity at a time when interest rates remain very low, although now increasing. This limits investments in local infrastructure. We define borrowing capacity as the additional amount of debt that LRGs could raise without a material impact on their credit quality.

Chart 10 | Borrowing Capacity Not Fully Utilized By Many LRGs

GG--General government. LRG--Local regional government. Source: S&P Global Ratings.

Globally, we think LRGs could borrow an additional $850 billion. Borrowing capacity remains extensive in emerging markets because, in most countries, subnational debt remains well below what we consider a relatively modest 60% of annual budget revenue. However, limited development of domestic capital markets, generally low predictability and transparency of fiscal policy, inefficient equalization systems, and restrictions on borrowings or debt levels hinder increased subnational borrowing in emerging markets.

The leverage starting point for LRGs in developed markets is higher than for emerging markets. However, we think developed markets can absorb and manage higher debt than EMs.

Table 1 | Top Issuers--Developed Market

*As of April 7, 2022. Source: S&P Global Ratings.

Table 2 | Top Issuers--Emerging Markets

NR--Not rated. Source: S&P Global Ratings.

Our survey on global LRG borrowing encompasses 49 countries: Argentina, Australia, Austria, Belgium, Bosnia and Herzegovina, Brazil, Bulgaria, Canada, China, Colombia, Costa Rica, Croatia, Czech Republic, Denmark, Finland, France, Germany, Guatemala, India, Indonesia, Israel, Italy, Japan, Jordan, Kazakhstan, Latvia, Mexico, Morocco, New Zealand, Nigeria, North Macedonia, Norway, Pakistan, Philippines, Peru, Poland, Romania, Russia, Serbia, South Africa, Spain, Sweden, Switzerland, Thailand, Turkey, Ukraine, the U.K., the U.S., and Vietnam. We consider this sample as representative of global LRG debt.

We base our survey on data collected from statistical offices, as well as on our assessment of the sector's borrowing requirements and outstanding debt, which includes bonds and bank loans. The reported figures are our estimates and do not necessarily reflect the LRGs' own projections. For comparison, we present our aggregate data in U.S. dollars.