This report does not constitute a rating action

Primary Credit Analysts

Michael Stroschein Frankfurt +49-693-399-9251

Thomas F Fischinger Frankfurt +49-693-399-9244

Table 1 | Local And Regional Government Gross Borrowing And Bond Issuance By Country

*Including state-guaranteed winding-up agencies for former public-sector banks and other guaranteed financing vehicles. §Including state-guaranteed financing vehicles. e--Estimate. CHF--Swiss franc. Source: S&P Global Ratings.

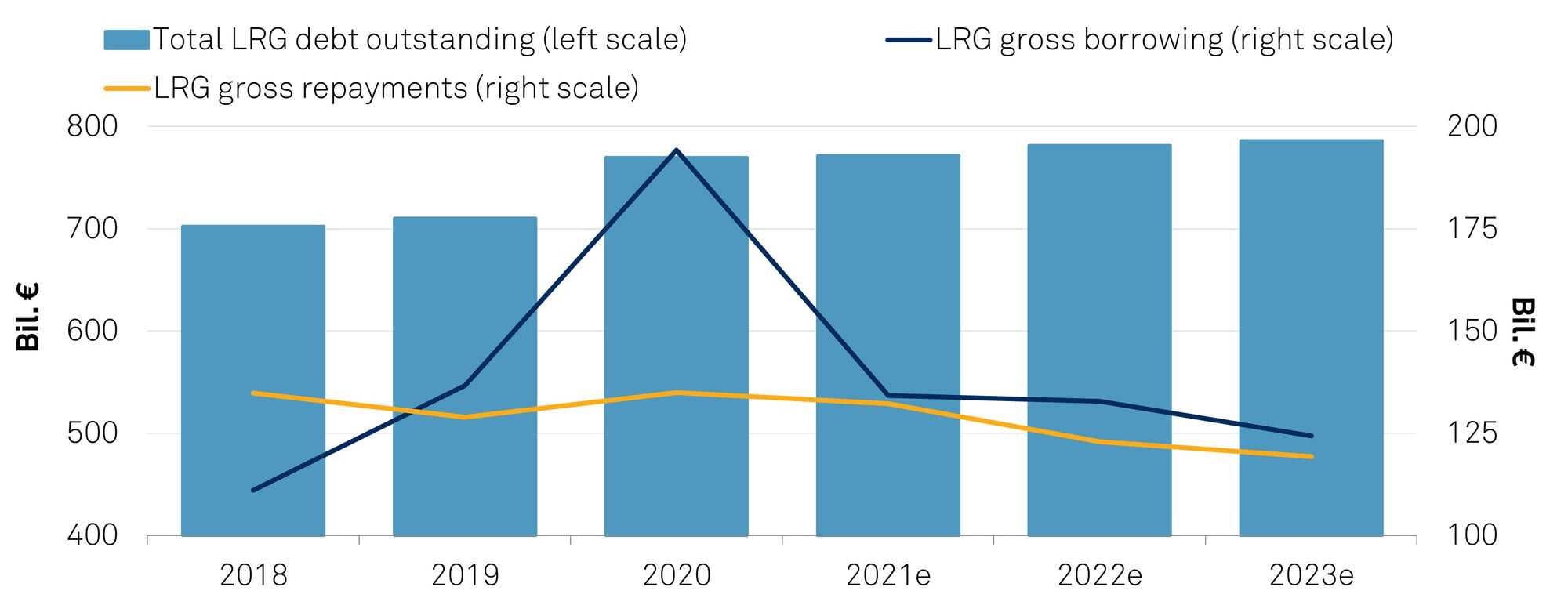

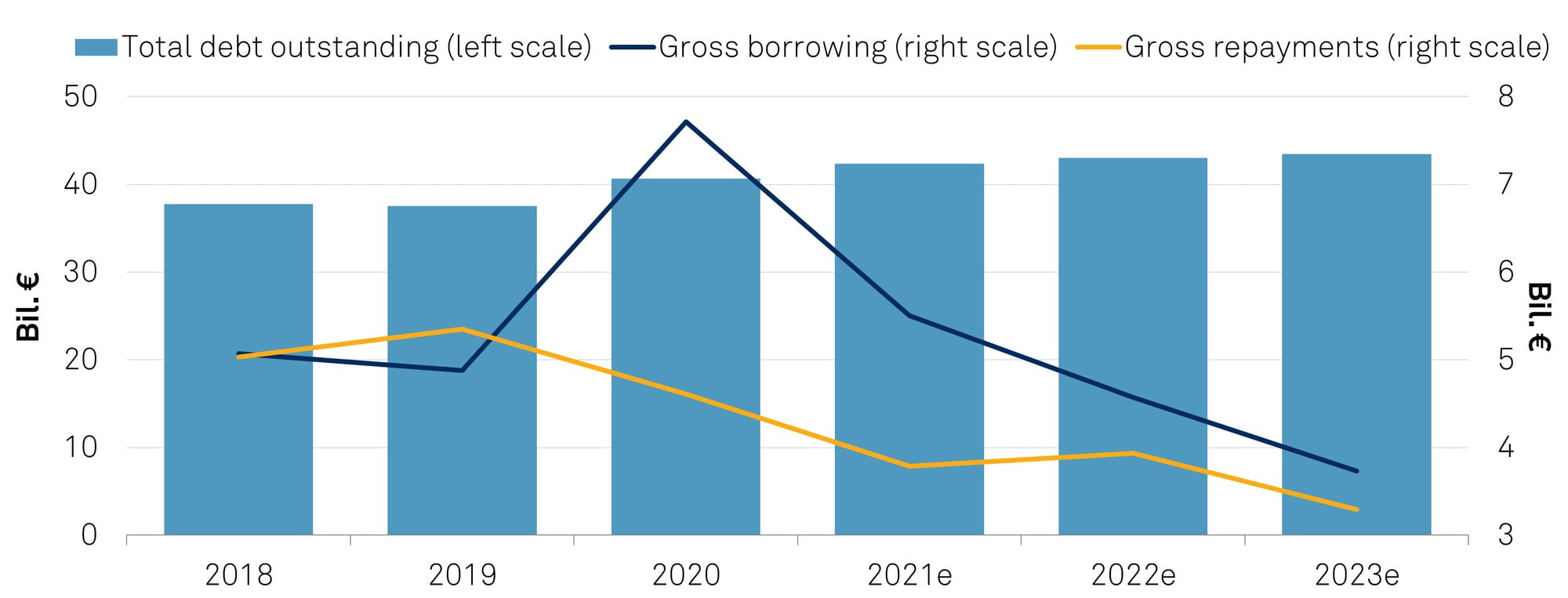

The economic and fiscal consequences of the Russia-Ukraine war will certainly delay and dampen the full healing of German subnational governments’ budgets from the impact of COVID-19. However--subject to progression of the conflict--we currently do not forecast a major relapse into the heavy borrowing patterns of the recent past. Rather, S&P Global Ratings believes the funding activities of German local and regional governments (LRGs) and their auxiliary budgets will normalize slightly further this year, after COVID-19-related borrowing requirements drove up issuance volumes to extraordinary levels in 2020.

In our view, the combined annual gross borrowing of German states, state-sponsored winding-up agencies for former public-sector banks and other state-guaranteed financing vehicles, and municipalities will retreat to €133 billion in 2022 and €124 billion in 2023, despite the new macroeconomic headwinds.

At these levels, new borrowings would nevertheless still exceed projected repayments. Consequently, we forecast that the German LRGs’ total amount of outstanding debt--across loans and bonds--will climb to more than €785 billion at the end of next year.

The anticipated increase in the volume of outstanding debt in 2022 would surpass the growth observed in 2021 but fall far short of the extreme upward jump of 2020.

Chart 1 | German LRG Debt: Gross Borrowing To Continue Normalizing In 2022

e--Estimate. LRG--Local and regional governments, including state-guaranteed winding-up agencies for former public-sector banks and other guaranteed financing vehicles. Sources: Destatis, S&P Global Ratings.

The remarkable V-shaped rebound in German tax revenue in 2021, the belief that COVID-19 has ceased to be a major impediment to economic activity, and the hope that the economic impact from the Russian invasion of Ukraine can eventually be contained represent the key drivers behind our current predictions for German LRG borrowing volumes. However, as the geopolitical situation develops rapidly, visibility regarding the resulting budgetary consequences for subnational governments is arguably limited at this point in time. Notably, our projection does not yet factor in any consequences of Russian gas supplies to Germany being completely and suddenly cut off, which arguably has become the biggest digital risk to German economic development in 2022 over the last few days.

In 2021, German states recorded growth in the amount of taxes collected of about 13% over the prior year, while in 2020 they had to cope with a drop of almost 5%. Preliminary data indicates a similar development at the municipal level. Thanks to this strong fiscal rebound, German states, while still having had to finance their various own COVID-19-related support programs for local enterprises and infrastructure in 2021, did not have to cover tax revenue shortfalls in their own accounts and at the municipal level with new debt to the same degree as in 2020. This explains a large part of the observed decline in last year’s net borrowing. While we understand that states have continued various COVID-19-related stimulus and compensation programs for their local economies in 2022, we expect these to have declined markedly in volume from 2021.

We forecast that the German LRGs’ total amount of outstanding debt will climb to more than €785 billion at the end of next year.

Furthermore, we find that the segregated COVID-19-targeted budget envelopes at some of the regional authorities we rate hold “leftover” liquidity, resulting from precautionary overfunding in 2020 and 2021. German states should therefore be able to finance large parts of any residual COVID-19-related spending in 2022 with such funds rather than new debt, before then closing their special COVID-19-funding vehicles for “new business” at the end of the year and reinstating the currently suspended zero deficit requirement under their respective debt brake legislation from 2023. The Russia-Ukraine conflict now overshadows the initially very positive revenue and borrowing outlook created by Germany’s most recent official tax forecast, performed in November 2021. In response to the outbreak of hostilities, S&P Global Ratings cut its forecast for German annual real GDP growth in 2022 by 1.4 percentage points to 2.9% (see “Economic Outlook Eurozone Q2 2022: Healthy But Facing Another Adverse Shock,” published on RatingsDirect on March 28, 2022). While we currently find it challenging to quantify the impact from the geopolitical crisis on German LRGs’ budgets, we expect lower tax revenue growth and the accommodation cost for refugees to be the primary initial transmission channels. We note that corporate tax (about €21 billion of revenue for states in 2021) and the trade tax (more than €55 billion of revenue estimated for municipalities in 2021, prior to redistribution) tend to be most susceptible to sudden changes in the business climate, but these are not the materially most relevant taxes. If a protracted war had a sustained impact on consumption spending and hence VAT collection (LRGs’ share in 2021: about €126 billion), or if it caused meaningfully higher unemployment and hence lower payroll tax flows (LRGs’ share in 2021: also about €126 billion), the budgetary impact could become more severe. Higher-than-anticipated inflation, on the other hand, could turn out to be an important mitigating factor in this respect, by boosting tax collection amounts even without underlying real growth. Absorbing the direct cost for supporting the about 300,000 Ukrainian refugees that so far have arrived in Germany will, initially, fall upon the state level, even though municipalities carry out most of the actual activities. However, like in the refugee crisis of 2015, significant, but not yet quantified federal reimbursements are widely expected. With the per-capita-and-month refugee cost claimed to amount to €1,000 by the German Association of Towns and Municipalities, the eventual number of refugees and the allocation of cost can be material for LRG’s budgetary results and funding needs. Second-round effects created by Germany’s response to the crisis, for example, through a possible acceleration of its Green Agenda, make the estimation of the war’s impact on LRG borrowing even less reliable. Germany’s newly announced €100 billion defense investment program, however, is exclusively a federal matter and does not affect LRGs’ budgets.

The link between German LRGs’ budgetary deficits--which, for the purpose of forecasting borrowing amounts, we provisionally and with currently only very limited data assume to not exceed €10 billion for 2022 and €5 billion for 2023--and the actual net borrowing volume in the loan and bond market is blurred by numerous stock flow adjustments. Funding needs resulting from allocations to internal pension reserve accounts; unpredictable movements in cash collateral posted or received for derivative transactions; and decisions on the creation or use of existing liquidity reserves, for example, in the above-mentioned earmarked COVID-19 accounts are among the key reasons for such discrepancies. We note that particularly in 2020, German states have displayed a far larger actual net borrowing amount (€59 billion) than would have been implied by their accounting deficit (€23 billion, according to Eurostat). For the most part, this reflects precautionary funding in the heat of the crisis, when liquidity buffers were increased significantly. For 2021, the--still incomplete--data released so far appears to indicate that setting and executing debt market funding volumes early in the year, while tax revenue recovery only occurred primarily in the last quarter, probably has produced a similar effect again, albeit at a smaller scale.

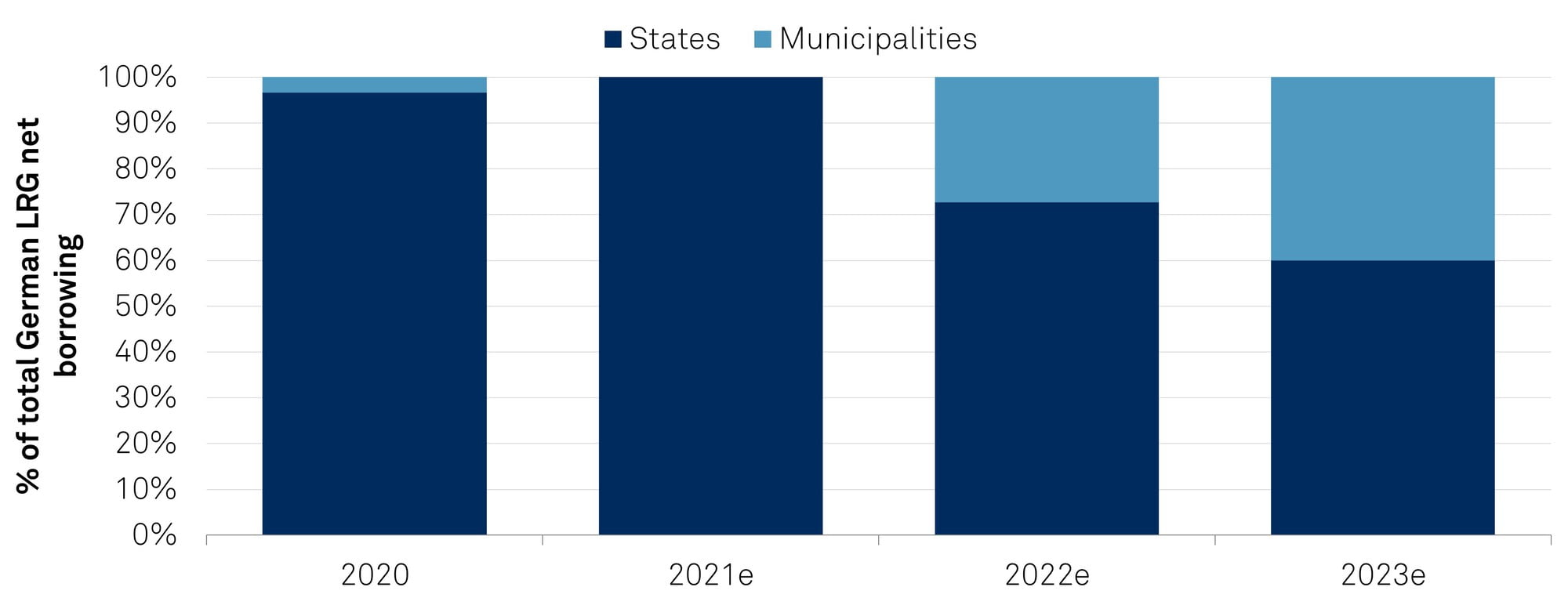

Only minor change expected to the debt split between states and municipalities and to largest borrower ranking

We believe that the traditional 80:20 split in outstanding German LRG debt volume between the state and the municipal level will be retained in the next few years. Already, the large volume and average tenor of outstanding debt implies that several years of significantly altered borrowing behavior would be required to cause a material change. That said, we notice that the German states (and the federal government), rather than municipalities, have shouldered the required debt-financing of COVID-19 measures almost exclusively in 2020. States temporarily were responsible for practically all of German LRGs’ elevated net borrowing in that year. However, we expect that this relationship is now returning to a more balanced split again, after municipalities, on aggregate, apparently managed to fully avoid net new borrowing in 2021. Additionally, several of the states--namely Hesse, Saarland, Rhineland-Palatinate, and Lower Saxony (the latter already in 2016)--have implemented or are still implementing programs to restructure municipalities’ “Kassenkredite” short-term loans into financing arrangements with a longer tenor, whereby these states then regularly take over a certain percentage of the restructured local government debt. All else being equal, both developments marginally shift the split in debt between the regional and the local level slightly toward the states, but this is barely noticeable against the large volume of already outstanding debt.

Chart 2 | German LRG Net Borrowing: States, Not Municipalities, Have Debt-Financed COVID-19 Support

Factoring in recent developments, we predict that the German state level will be responsible for €103 billion, or 78%, of gross LRG borrowings in 2022, while municipalities will contribute the remaining 22%, equivalent to €30 billion.

Deducting maturing debt, we forecast that €645 billion or almost 83% of outstanding German LRG debt will be owed by the states and just 17% or €136 billion by the municipalities at the end of 2022.

Already by virtue of having to refinance its portfolio’s maturities, the State of North-Rhine Westphalia (NRW; rated AA/Stable/A-1+) is practically guaranteed to remain Germany’s largest subnational government borrower for the foreseeable future. With an outstanding amount of debt of about €160 billion at year-end 2021, the core budget of NRW actually owes more to its creditors than all German municipalities combined. This is true even without consolidating the state’s two largest auxiliary budgets Erste Abwicklungsanstalt (EAA, the wind-down agency for former West/LB, rated AA/Stable/A-1+) and Bau- und Liegenschaftsbetrieb NRW (BLB, the state’s funding and management vehicle for government-used real estate, not rated).

Table 2 | Rated German States´ Adjusted Gross Borrowing--2022 Estimates

Bil. €

Adjusted gross borrowing

Ratings*

Baden-Wuerttemberg (State of)

4.5

AA+/Stable/A-1+

Bavaria (State of)

0.5

AAA/Stable/A-1+

Hesse (State of)

8.3

North Rhine-Westphalia (State of)

14.9

AA/Stable/A-1+

Saxony (State of)

1.7

AAA/Negative/A-1+

Saxony-Anhalt (State of)

5.2

*As of March 31, 2022; Source: S&P Global Ratings.

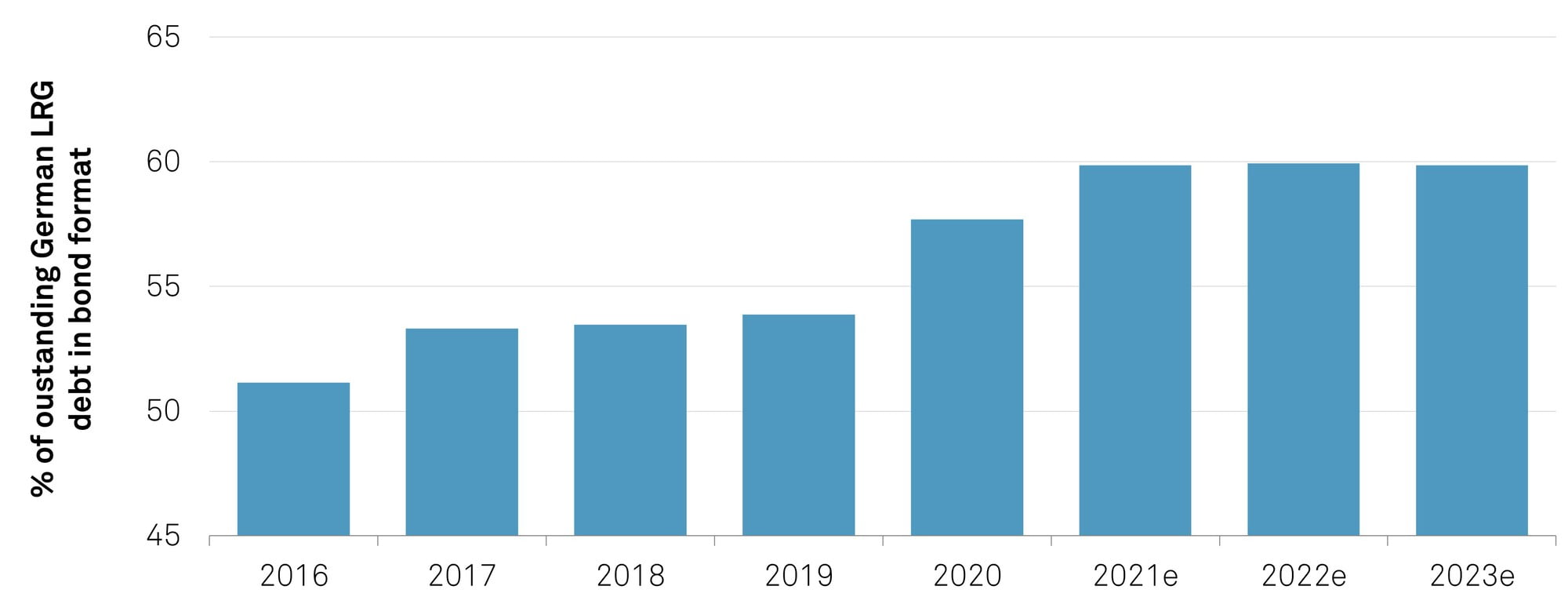

Not uniquely caused by COVID-19-related funding needs, but certainly exacerbated by it, we observe that the relevance of bond market funding has increased for German LRGs. We estimate that the share of outstanding German LRG debt in bond format has grown to 60% currently, from about 50% still in 2016. If one looks only at the state level and ignores the mostly still bank-funded municipal sector, this percentage rises to 73%. We attribute the increased importance of public-market bond issuance to:

Chart 3 | German LRG Funding Mix: Relevance Of Bond-Format Debt Has Risen

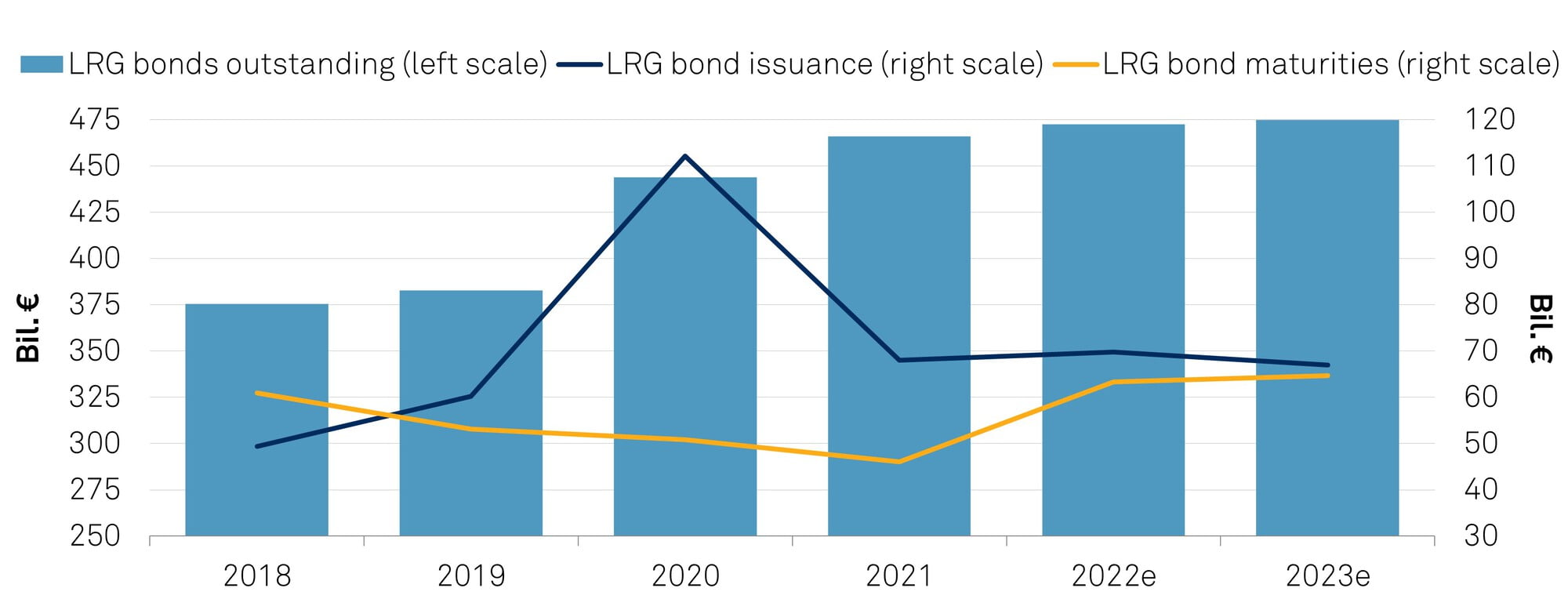

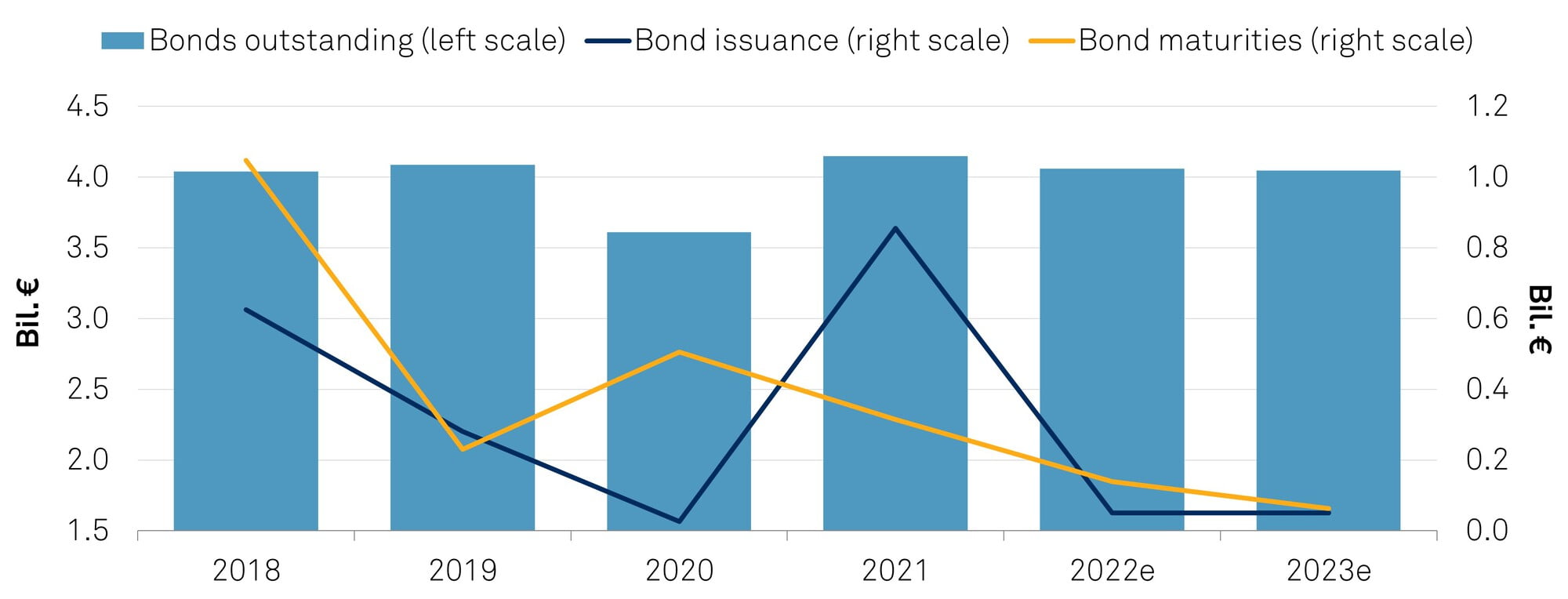

We forecast that German subnational government bond issuance in the public market in 2022 and 2023--excluding any “Schuldschein” certificates, which legally are loans--will amount to almost €70 billion annually. At this level, public bond issuance would meet just above 50% of the periods’ total gross borrowing needs of German states, municipalities, and LRG auxiliary budgets. We anticipate the volume of outstanding LRG bonds to marginally exceed €470 billion. New Issuance in 2022 and 2023 will, in our view, reflect net new borrowings as well as refinancings, with a first portion of COVID-19-related bonds issued in 2020 already becoming due. Even when factoring in a more negative impact of the Russia-Ukraine conflict than currently assumed, 2022 and 2023 bond issuance volumes will, in all likelihood, range far below the 2020 peak. At that time, almost twice the currently forecasted annual volume was placed, showing the depth of the market and the strong credit standing of German LRGs.

Chart 4 | German LRG Bond Market Activity: Refinancing And New Borrowing Will Jointly Drive New Issuance

e--Estimate. LRG--Local and regional governments, including state-guaranteed winding-up agencies for former public-sector banks and other guaranteed financing vehicles. Sources: Bloomberg, Destatis, S&P Global Ratings.

Bonds continue to be issued almost exclusively by the German states and state-related entities, with municipal issuance playing practically no role. For 2021, we count 111 individual bond issues by German states and state-attributed financing vehicles, but not a single one from the municipal level. In fact, the outstanding amount of city-issued bonds amounted to only €3.4 billion at end-2021, less than 1% of the total volume of German LRG bonds in the market. In 2021, issuance sizes of German LRG bonds ranged from just €20 million to €3 billion. Notable structural features in the 2021 vintage again comprise a €3 billion 100-year issue by NRW, but also the first green bond issued by the State of Baden-Württemberg, besides NRW’s eighth social bond issue.

Below the two top spots, which continue to be occupied by NRW and the State of Bremen, the ranking of German subnational government bond issuers by annual issuance volume in 2021 has undergone some changes compared to 2020. This can be explained by the different approaches the various German states took to funding their COVID-19-mitigating measures at the height of the pandemic.

However, it would be premature in our view to derive judgment about structural changes to budgetary performance from these movements. In fact, most German states display annual issuance volumes in a narrow range of €2 billion-€5 billion, so that limited changes in annual funding needs can quickly affect their relative position. NRW’s top spot in the issuer ranking (€15 billion of 2021 issuance volume in 20 public market transactions) is easily explained by the size of the state, comprising over 20% of Germany’s GDP and population, and its large debt stock that requires refinancing annually. The surprisingly high annual issuance volume (€13 billion of total funding) of the rather small city-state of Bremen with its fewer than 700,000 inhabitants can, according to our understanding, be linked to the rollover of short-term financing of collateral posting requirements for Bremen’s activities in the derivatives market.

We expect Austrian real economic growth to be subdued as well by the Russia-Ukraine war and the observable rise in energy prices. However, higher and persistent inflation rates should help to keep nominal growth rates at comparably solid levels.

This should preserve a pick-up in tax revenues for all three government tiers, with practically all material tax revenue shared among the federal government, states, and municipalities. We estimate that economic growth will more than offset the tax losses stemming from the federal tax reform implemented in early 2022. States and municipalities (LRGs) in Austria additionally benefit from ad hoc transfers from the federal government, which should also help to contain budgetary deficits. We therefore believe that the sector’s aggregate deficit will reduce to €650 million in 2022, down from about €1.8 billion in 2021, driving total debt burden of states to almost €33 billion and debt of municipalities to nearly €10 billion.

Chart 5 | Austrian LRG Debt: Lower Funding Needs As Economy Recovers From Pandemic

e--Estimate. LRG--Local and regional governments, including state-guaranteed winding-up agencies for former public-sector banks and other guaranteed financing vehicles. Sources: Statistik Austria, S&P Global Ratings.

Unlike German and Swiss peers, the public bond market plays only a minor role in Austrian subnational government financing. In 2021, Lower Austria was the only Austrian subnational government that issued bonds at all, involving four transactions totaling €277 million. We assume that identifiable redemptions of just €170 million in 2022 and €250 million in 2023 will still exceed new issuance in these two years. The currently outstanding volume of bonds issued by Austrian subnational governments should therefore keep reducing gradually, in our view. Based on information from the states we rate, we believe that the relevance of bank funding will also decline, given favorable funding terms offered by the federal treasury, and a more opportunistic than strategic approach to funding from banks. We expect--if funding via bond issuance takes place at all--only small issuances by selected states and no further issuances by municipalities, given their reduced deficits in 2022. Our forecast is contingent on the pandemic fading further and subnational governments aiming to reduce spending.

Table 3 | Rated Austrian States´ Adjusted Gross Borrowing--2022 Estimates

Mil. €

Adjusted Gross Borrowing

Burgenland (State of)

105

Lower Austria (State of)

446

Styria (State of)

375

Tyrol (State of)

268

AA+/Negative/A-1+

Upper Austria (State of)

258

Vorarlberg (State of)

214

All Austrian states, except for Tyrol (AA+/Negative/A-1+), cover practically all their funding needs by borrowing from the central government and its federal debt management agency (OeBFA).

These states have signed agreements with the federal treasury, effectively granting them the refinancing of all local currency debt falling due within one year, plus any funds the states need for financing their budgetary deficits as long as these deficits stay within the framework of the national stability pact.

This institutional arrangement gives participating states access to cheap funding at the same rates that the sovereign itself pays for its debt, with no surcharge to the federal government’s funding cost added. We therefore expect this to remain Austrian states’ preferred funding option, implying only limited room for bank or bond market financing on a larger scale.

If states choose not to fund themselves via OeBFA--for example, to diversify their funding sources or for political reasons--they predominately take loans from banks. Consequently, outstanding bonds of Austrian states account for only 10% of their direct debt. Three outstanding bonds each have been issued by the states of Vienna and Carinthia (both not rated), while the lion’s share of 41 bonds, totaling €3 billion, has been placed by the state of Lower Austria (AA/Stable/A-1+). The latter is the only Austrian state to have regularly issued bonds in local currency over the past four years.

Chart 6 | Austrian LRG Bond Market Activity: Opportunistic Bond Issuances Limit Market Activity

e--Estimate. LRG--Local and regional governments, including state-guaranteed winding-up agencies for former public-sector banks and other guaranteed financing vehicles. Sources: Bloomberg, S&P Global Ratings.

Austrian municipalities do not have access to funding via OeBFA, but their individual funding needs are usually too small to justify the issuance of a bond in the capital markets. The only municipality with bonds outstanding is Austria’s second-largest city, the Styrian capital of Graz, with four issues existing in the market at the beginning of 2022. Austrian municipalities benefit from states making need-based grants available to them, occasionally propped up by special transfers from the federal government--as most recently demonstrated during the pandemic--to enable municipalities to keep capital expenditures at high levels.

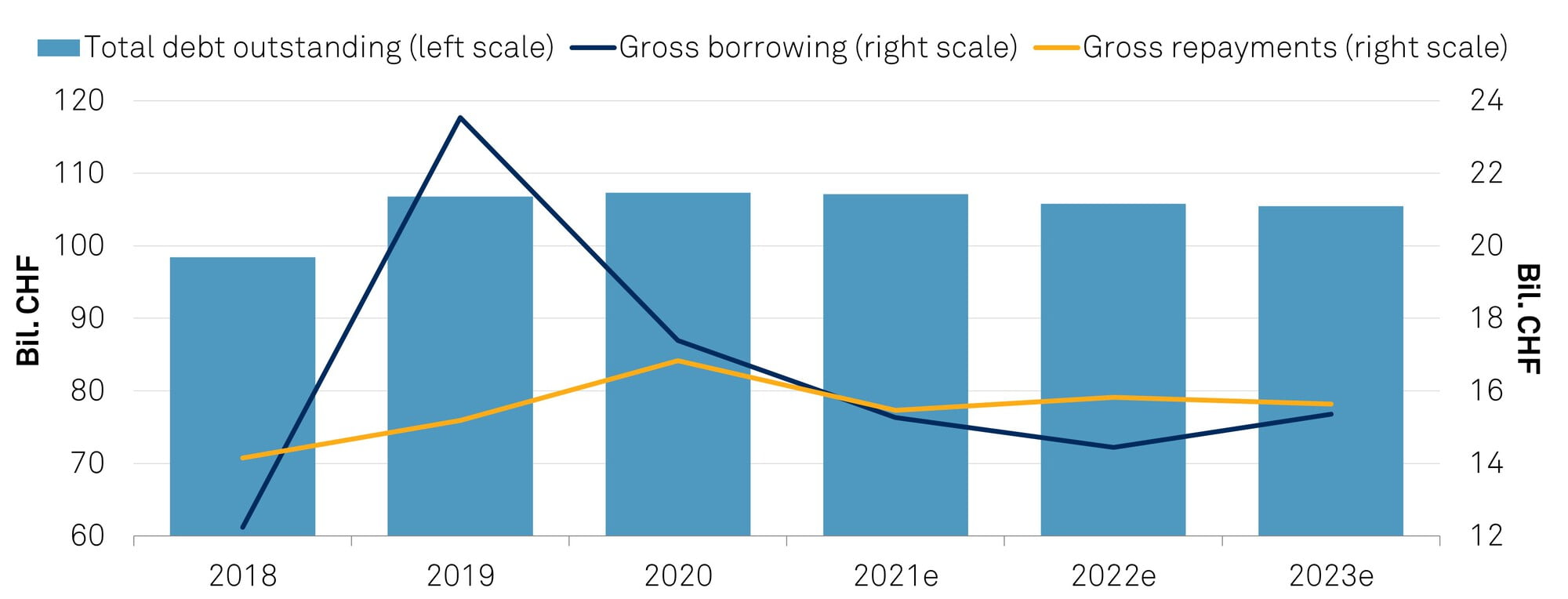

We forecast that annual gross borrowing of Swiss cantons and municipalities will amount to about Swiss franc (CHF) 14 billion-15 billion, across all debt types, in 2022 and 2023. With estimated maturities slightly higher, expected at just below CHF16 billion in each year, a marginal decline in outstanding Swiss LRG debt to CHF105 billion by the end of 2023 would result. These figures do not include the borrowing activities of cantonal hospitals.

Ignoring the blip in the LRG gross borrowing amount in 2019, to our knowledge caused by the recapitalization of the pension fund of the Republic and Canton of Geneva (AA-/Stable), the borrowing and repayment volumes of Swiss cantons and municipalities are characterized by great stability. Unlike in Germany and Austria, funding needs have not at all shot up during the COVID-19 pandemic, and we currently do not foresee the Russia-Ukraine war to have a major impact in this respect, despite forecast slower GDP growth also for Switzerland due to the conflict. We believe that the anticipated small net repayments of the sector will mainly be driven by surpluses at the cantonal level, outweighing minor deficits of the Swiss municipalities over the two-year forecast horizon.

Chart 7 | Swiss LRG Debt: Small Net Repayments Projected

CHF--Swiss franc. LRG--Local and regional government. e--Estimates. Sources: Federal Statistics Office, S&P Global Ratings.

Our estimate of the next two years’ funding and repayment volumes of Swiss LRGs is informed by various recent developments that we consider relevant and influential.

The remarkable resilience of the Swiss economy during the COVID-19 pandemic so far--demonstrated in 2020 when real GDP decreased only by 2.4% compared with, for example, 4.6% in Germany or even 8.0% in France--has translated into stable tax revenue, generating a positive base effect for 2022 and 2023. Swiss LRG budgets have not been severely burdened by COVID-19-related expenditures, as they were mostly paid with federal funds and the last remaining programs are now expiring. In most cantons, the peculiarities of local tax collection mechanics delay and distribute the fiscal impact of negative economic shocks better than, for example, in Austria and Germany. Given our reduced prediction of Swiss real GDP growth of only 1.8% in 2022, 1.5 percentage points lower than previously assumed, this should prove helpful again.

The Swiss National Bank (SNB) has been profitable over the last years and accumulated a substantial distribution reserve of more than CHF100 billion at end-2021. Therefore, cantons stand a good chance of receiving their maximum share of CHF4 billion under the revised SNB profit distribution agreement not only in 2022, but also in 2023. That said, a “perfect storm” of, simultaneously, a sharp correction in equity prices, rising U.S. and European interest rates, and a swiftly appreciating Swiss franc--as temporarily observed during the outbreak of the war in Ukraine--could impose material losses upon the SNB, given the size of its asset portfolio, and push reserves down toward the prespecified thresholds below which disbursements to cantons would be cut. Notably, the volume of the current SNB profit distribution payment is sufficiently large to turn what would otherwise be a net borrowing requirement for the combined Swiss LRG sector into our predicted small net repayments.

Our recent discussions with selected cantonal treasurers anecdotally point to current liquidity in excess of perceived needs. This suggests that maturing debt of Swiss cantons may in many cases be retired rather than refinanced in 2022. However, we note that in response to positive budgetary outlooks at the end of 2021, many Swiss LRGs have enacted--or are at least discussing--reductions in their local tax multipliers, or similar measures, which will weigh on cash flow.

Reflecting the deeply federal nature of Switzerland, where significant responsibilities are devolved to the local and regional level, Swiss municipalities owe a larger proportion of overall LRG debt than in many other nations. We expect that the currently observable split of about 56% of LRG debt sitting at the cantons, while 44% is borne by municipalities, will not change structurally in coming years. For end of 2020, Swiss official statistics put the volume of cantonal and municipal debt at CHF60 billion and CHF48 billion, respectively.

The existence of very small Swiss cantons--Obwalden, Uri, and Appenzell Inner Rhoden, for example--makes for the interesting fact that major Swiss cities like Zurich (AA+/Stable), Bern (not rated), Geneva (AA-/Stable), or Lausanne (A+/Stable) outrank the smaller cantons multiple times in population and budget size, and, therefore, funding volumes.

Table 4 | Rated Swiss Cantons´ And Cities´ Adjusted Gross Borrowing--2022 Estimates

Bil. CHF

Aargau (Canton of)

0.3

AA+/Positive/A-1+

Basel-City (Canton of)

0.6

Basel-Country (Canton of)

0.1

Geneva (Republic and Canton of)

1.1

AA-/Stable/--

Solothurn (Canton of)

0.2

St. Gallen (Canton of)

-

Vaud (Canton of)

AAA/Stable/--

Zurich (Canton of)

1.3

Geneva (City of)

Lausanne (City of)

A+/Stable/--

Zurich (City of)

1.0

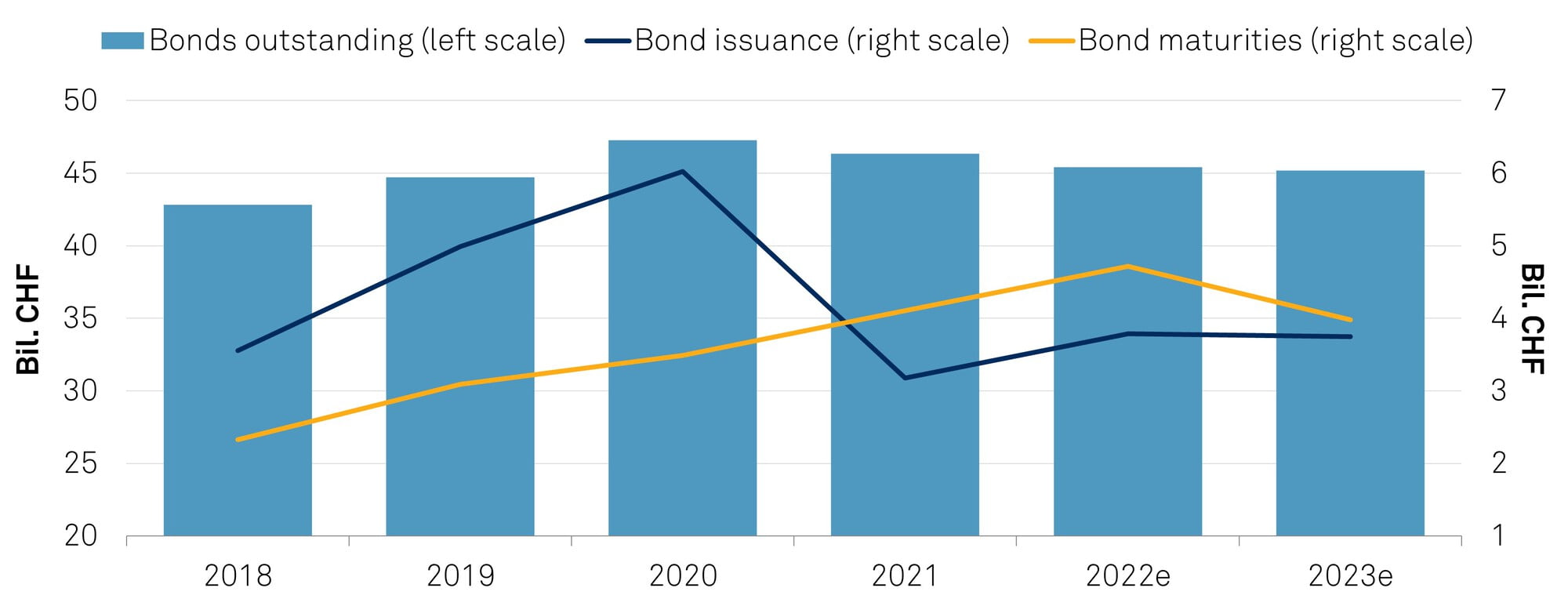

Of the outstanding CHF46 billion in Swiss LRG debt at end- 2021, about 43% has been sourced in the public bond market, according to Bloomberg data.

For 2022 and 2023, we expect annual public bond market issuance volume for cantons and municipalities of just below CHF4 billion each year. As the currently identifiable bond maturities of slightly exceed this projected new issuance, we anticipate the volume of Swiss LRG bonds will fall slightly to CHF45 billion in 2022 and 2023.

Due to the currency--Swiss LRG bonds are exclusively denominated in Swiss francs--capital market funding for Swiss LRGs remains largely a domestic affair, provided by local investors.

Chart 8 | Swiss LRG Bond Market Activity: Redemptions Likely To Exceed New Issuance

CPI--Consumer price index. GG--General government. Sources: S&P Global Ratings, Bloomberg.

A notable feature of the Swiss LRG bond market is the large number of issuers, albeit often with only small individual issuance volumes and not more than one or two bonds outstanding. This separates Switzerland from Germany, for example, where practically only the 16 states, a few state financing vehicles, and a handful of municipalities have ever tapped the public bond market. For Swiss LRGs, we can trace 255 individual issuers with bonds outstanding in the public market as of end-2021. Consequently, the average Swiss LRG bond issuer has placed just above CHF180 million in this market segment, compared with almost €15 billion for German LRGs. However, we suspect that future Swiss LRG bond issuance will be more concentrated at the local “heavyweights,” while smaller municipalities may find other borrowing formats more attractive.

Research Contributors

Didre Schneider Frankfurt +49-693-399-9244

Marius Schulte Frankfurt