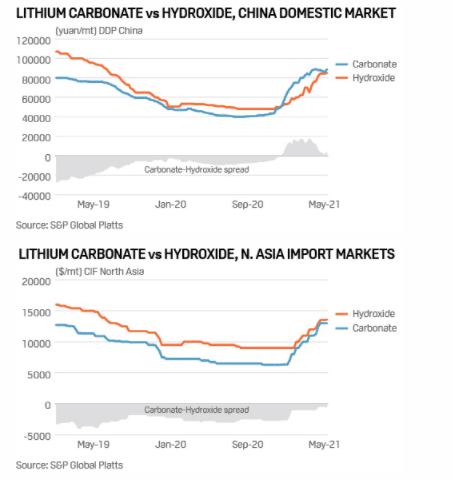

In China, where the lithium spot market is much more active than in other regions, the share of hydroxide volume traded under long-term contracts is much bigger than that of carbonate. The limited liquidity on the hydroxide spot market, as a result of the predominance of long-term contracts in this segment, reduced volatility. This was observed during the 2018-2020 lithium bear run, when carbonate prices fell faster than those of hydroxide, and is being proved again in the bull run, with carbonate moving up more rapidly too.

Nevertheless, as nickel-rich chemistries grow in importance, given the expectations of adoption across Europe and the Americas, demand for hydroxide will certainly increase. This will undoubtedly bring with it price instability, given the inherent risk of demand outpacing supply in years to come, but to a far lesser extent than what will likely be seen in the carbonate markets.

Chemistries in the future

The LFP resurgence in China was one of the key factors driving lithium carbonate prices above lithium hydroxide, but with the global EV axis progressively moving to Europe – the region is expected to become the biggest market by the end-2021—the LFP story was expected by many to fade out.

The European market is still expected by several industry participants to be largely dominated by nickel-rich batteries such as the NCM 8:1:1, which provides higher energy density. The typical European consumer, being concerned with the range of an EV, would be expected to pay a higher price tag than the typical Chinese consumer. However, promoters of the nickel-rich battery are potentially overestimating a typical commute in Europe (especially