This report does not constitute a rating action

Primary Credit Analysts

Karen Vartapetov, PhD Frankfurt +49-693-399-9225

Roberto H Sifon-arevalo New York +1-212-438-7358

We estimate sovereign borrowing will reach $10.4 trillion in 2022, nearly one-third above the average before the COVID-19 pandemic.

Despite an economic recovery, we expect borrowing to stay elevated, owing to high debt rollover needs, as well as fiscal policy normalization challenges posed by the pandemic, high inflation, and polarized social and political landscapes.

The global macroeconomic repercussions of the ongoing military conflict between Russia and Ukraine will put further upward pressure on government funding needs this year.

Tightening monetary conditions will push up government funding costs. This will pose additional difficulties to sovereigns that have been unable to restart growth, reduce reliance on foreign currency financing, and where interest bills are already critically high.

For advanced economies, borrowing costs this year, while on the rise, will likely remain below the effective interest rate on the existing debt stock, giving time to consolidate budgets and focus on pro-growth reforms.

The macroeconomic implications of the ongoing military conflict between Russia and Ukraine will add to fiscal consolidation challenges for many sovereigns this year. Even before the conflict erupted, governments were facing the difficult task of normalizing their fiscal policies amid the fragile growth outlook and widening socioeconomic gaps. We believe these factors will keep sovereign borrowing well above pre-pandemic levels this year and beyond. Rising interest rates will complicate the fiscal and funding outlooks even further, with some emerging market (EM) economies likely to face credit stress.

S&P Global Ratings acknowledges a high degree of uncertainty about the extent, outcome, and consequences of the military conflict between Russia and Ukraine. Irrespective of the duration of military hostilities, sanctions and related political risks are likely to remain in place for some time. Potential effects could include dislocated commodities markets--notably for oil and gas--supply chain disruptions, inflationary pressures, weaker growth, and capital market volatility. As the situation evolves, we will update our assumptions and estimates accordingly. See our macroeconomic and credit updates here: Russia-Ukraine Macro, Market, & Credit Risks.

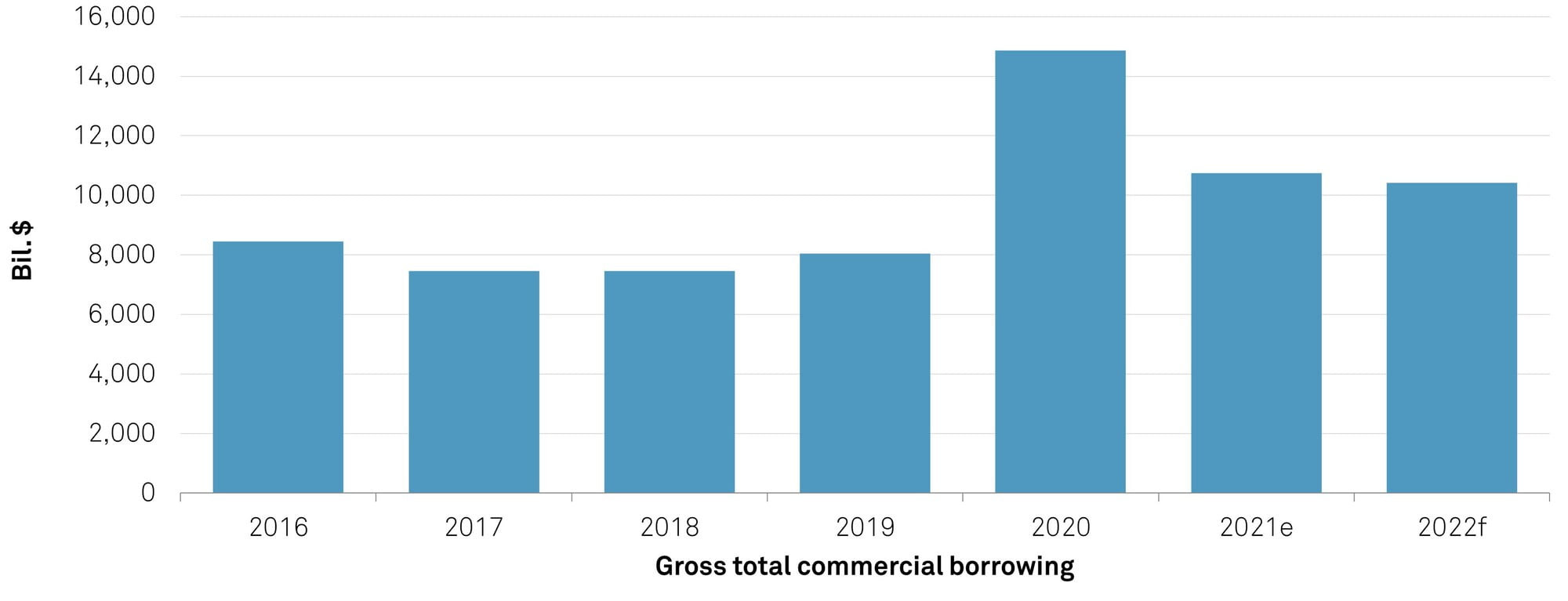

We project that the 137 sovereigns we rate will borrow an equivalent of $10.4 trillion from commercial sources in 2022. This is 30% lower than in 2020, when the adverse effects of the COVID-19 pandemic and the corresponding fiscal policy responses prompted an unprecedented rise in government financing needs. However, in a historical perspective, sovereign borrowings this year are projected to remain one-third above those in 2016-2019 on average (see chart 1).

Chart 1 | Total Sovereign Borrowing In 2022 Projected To Stay 30% Above The Pre-COVID-19 Levels

Note: Central government commercial borrowing, including short-term borrowing, of rated sovereigns. e--Estimate. f--Forecast. Source: S&P Global Ratings.

Table 1 | Sovereign Commercial Issuance And Debt

Total commercial borrowing = gross long-term borrowing + change in short-term debt stock. e--Estimate; f--Forecast. Source: S&P Global Ratings.

One factor explaining still-high borrowing is substantial debt-refinancing needs on the back of shorter average debt maturity. The pandemic-induced uncertainty led many sovereigns to accelerate short-term borrowings. The trend was especially visible, for example, in the U.S, Japan, and Germany, where the share of short-term borrowings increased to over one-third of the total during the pandemic. As a result, the rollover ratio for G7 nations has picked up to about 27% of total debt in 2021-2022 on average compared to 21% in 2019, according to our estimates.

The slow pace of fiscal consolidation is the other main driver of elevated issuance. While most economies are expected to return to pre-COVID-19 output levels by 2022, we forecast that even in 2023, average general government deficits to GDP will still be above their pre-COVID averages in nearly all regions (see "Global Sovereign Rating Trends 2022: Despite Stabilization, The Pandemic Threatens The Recovery," published Jan. 27, 2022, on RatingsDirect). This stems not only from the adverse effects of the ongoing pandemic, but also sociopolitical challenges governments are facing when trying to normalize their fiscal policies.

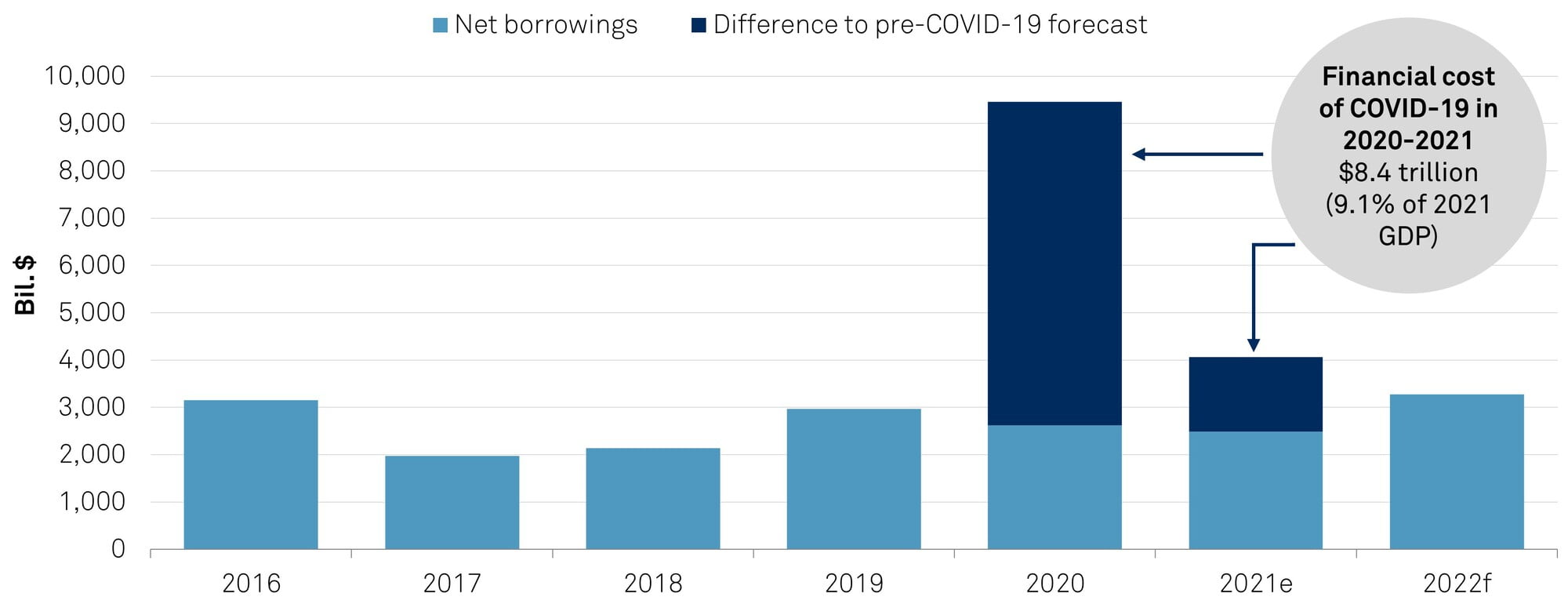

As a result, continued fiscal support will further increase the implied cost of the pandemic. We currently estimate the approximate effect of COVID-19 on public finances stemming from revenue contraction and higher spending in 2020 and 2021 at around $8.4 trillion combined, or slightly above 9% of global GDP (see chart 2). The new virus variants and uneven pace of vaccination could once again force some countries to impose lockdowns and extend fiscal support measures.

Chart 2 | The Fiscal Cost Of The Pandemic Has Exceeded 9% Of Global GDP

e--Estimate. f--Forecast. Source: S&P Global Ratings.

The global macro effects of the Russia-Ukraine conflict will likely push government borrowings above our baseline projections. The extent of the global fallout from the conflict is difficult to quantify at this point. That said, we have revised our GDP growth forecast in most regions, expecting it to be weaker globally, and particularly so in Europe. Commodity prices and knock-on inflationary pressures are also expected to be higher than our previous projections (see "Global Economic Outlook Q2 2022: No Cause For Complacency As The Russia-Ukraine Conflict Modestly Dents Growth," published March 31, 2022). These factors will almost certainly make governments adjust their funding plans upward for this year. Even before the conflict, high energy and food prices had prompted many governments to extend some fiscal measures established during the pandemic or replace them by new ones, rather than phase them out.

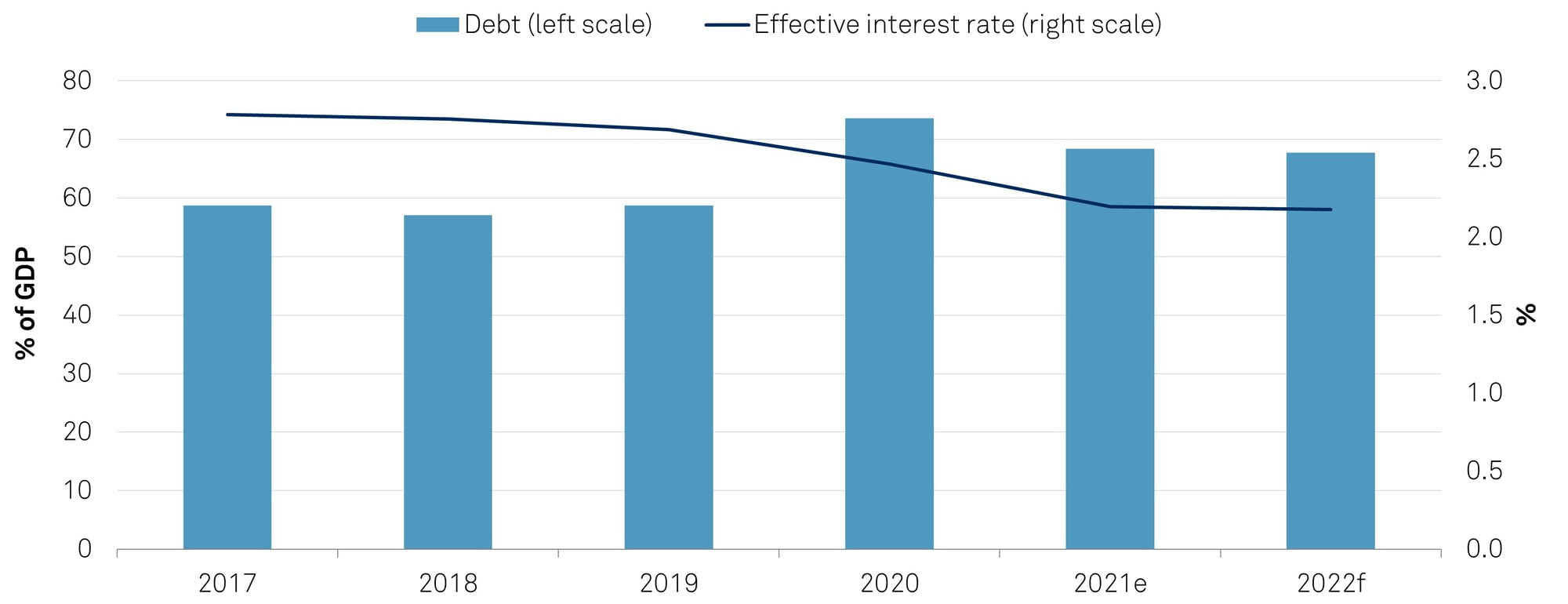

Nevertheless, we expect nominal GDP growth to remain relatively high, enabling the global sovereign debt burden to broadly stabilize in 2022. By our estimate, sovereign commercial debt as a proportion of GDP will stay at around 68% in 2022--about the same as in 2021 but lower than the peak of 74% in 2020 (see chart 3). The implied interest rate on the existing sovereign debt stock will also remain flat, reflecting governments' efforts to lock in exceptionally low interest rates brought about by monetary loosening in 2020.

Chart 3 | Commercial Debt Stock Declined In 2021 And Will Stabilize In 2022, After A Pandemic Spike Central government stock and cost of debt

Note: All figures denote to central government commercial debt, budget revenue and interest expenditures. Effective interest rate denote to interest expenditures divided by outstanding debt stock. e--Estimate. f--Forecast. Source: S&P Global Ratings.

Global averages mask substantial differences across sovereigns, with some likely to face credit stress in 2022, including from higher funding costs. Economies that are unable to kick-start growth or consolidate their fiscal positions will experience debt on an upward path (for more details, see our regional borrowing reports listed in "Related Research" below). Furthermore, larger debt burdens will go hand in hand with higher borrowing costs as central banks across the world continue to normalize or tighten their policies.

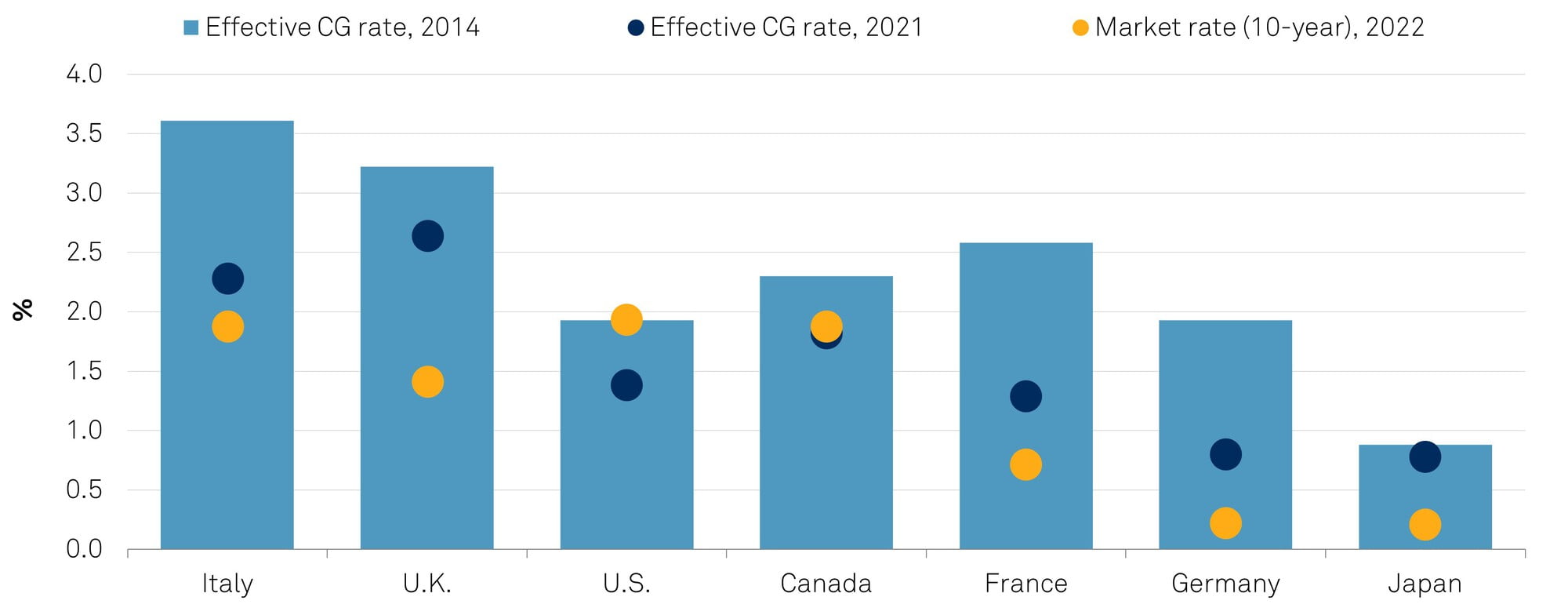

So far, the current market borrowing costs are still favorable for advanced sovereigns. In most G-7 countries, except the U.S., cost of debt in early 2022 remained below the effective interest rate of the existing debt stock. In these economies, the government interest bill will likely increase only moderately, even if monetary normalization comes sooner and faster than we currently expect (see chart 4a).

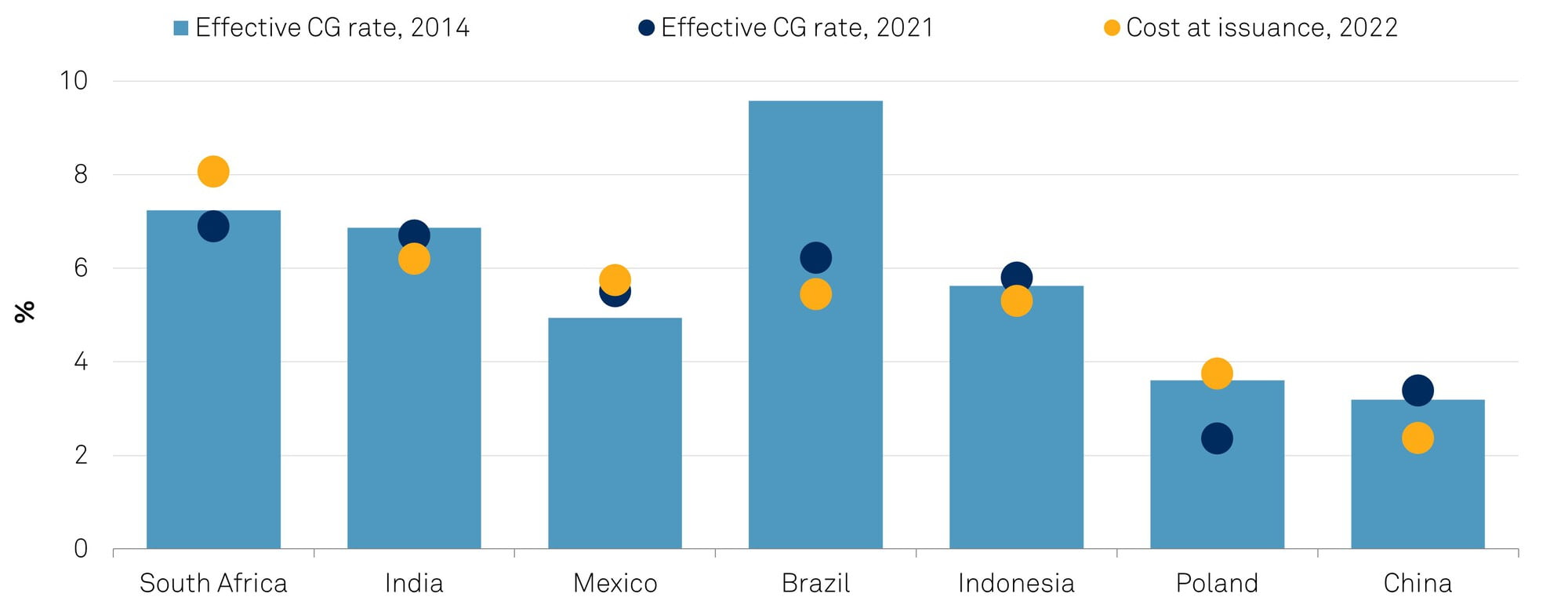

However, the cost of borrowing for emerging market economies has picked up more substantially. Many EM central banks have brought forward or accelerated policy tightening, resulting in the current issuance cost approaching multiyear historical levels (see chart 4b). For those sovereigns with weaker policy credibility, vulnerable budgetary positions, and reliance on foreign currency borrowings, higher borrowing costs will represent a credit risk.

Chart 4a | Market Cost Of Issuance Is Still Below Effective Interest Rates On Existing Debt For Most Developed Market Sovereigns...

Note: GC denotes to central government; market rate refers to 10-year bond yield in early 2022. Effective interest rate = interest expenditures divided by outstanding debt stock. Source: S&P Global Ratings.

Chart 4b | …But Have Already Approached Or Exceeded Effective Interest Rates For Some Emerging Market Economies

Note: GC denotes to central government; cost of issuance refers to average coupon rate of 3 to 5-year local-currency bond issuance in early 2022; effective interest rate = interest expenditures divided by outstanding debt stock. Source: S&P Global Ratings.

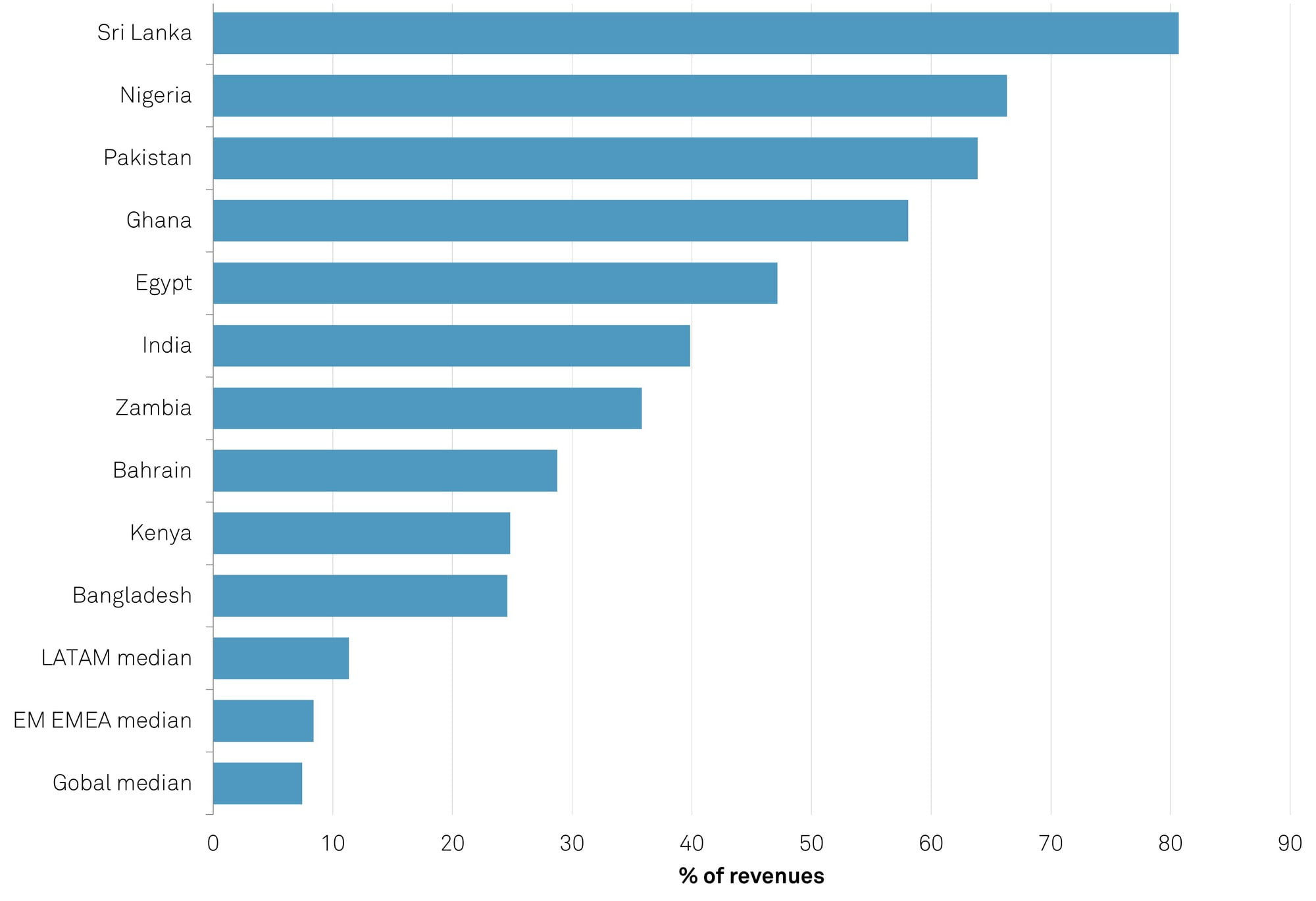

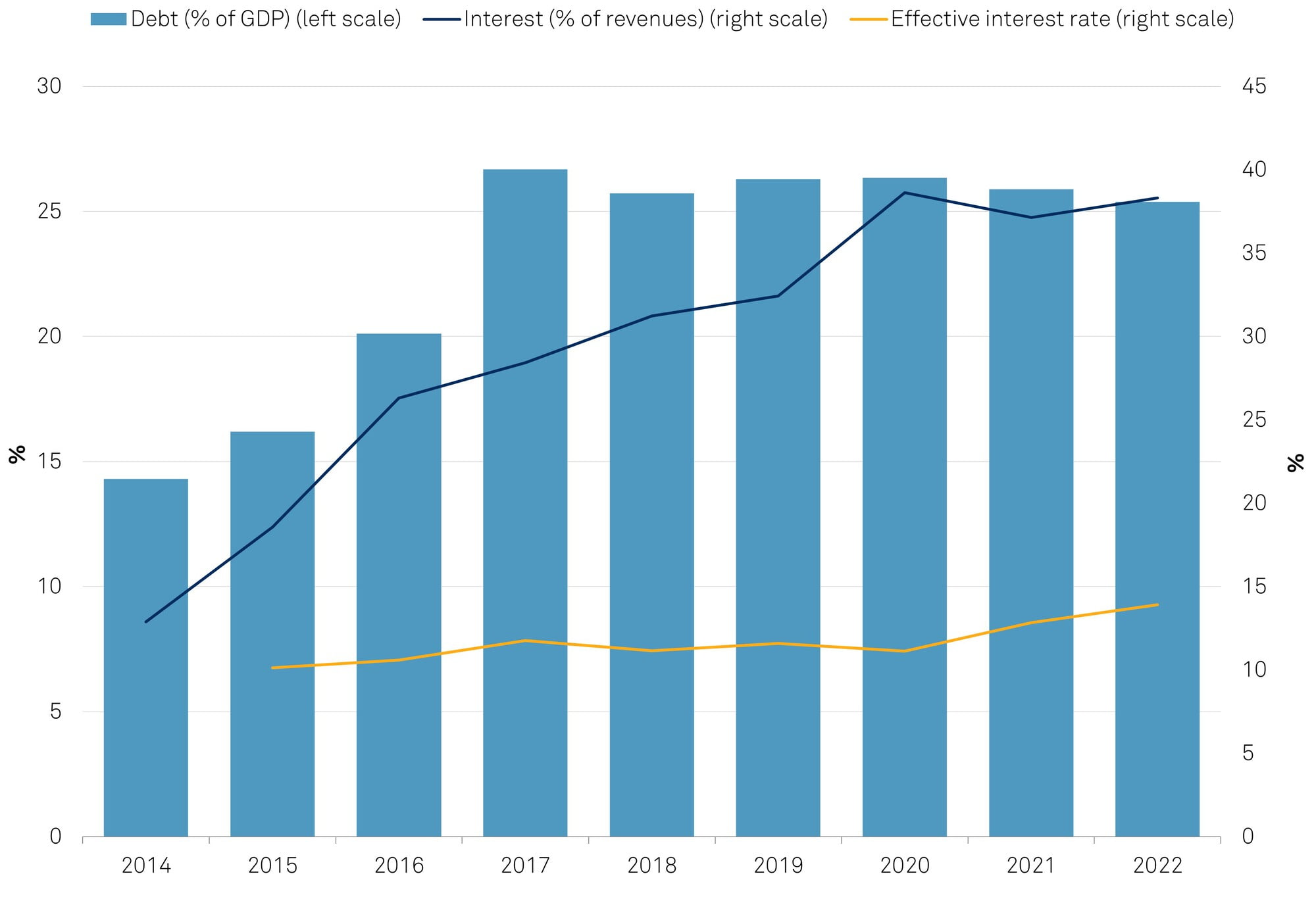

The effect of tighter borrowing conditions is even more nuanced for frontier market sovereigns with weak tax generation capacity. Some governments in EMEA and APAC are facing exceptionally high interest burdens, sometimes exceeding two-thirds of their total fiscal revenues (see chart 5a). For many, this can be attributed to longstanding fiscal challenges, including weak tax administration rather than higher cost of debt per se. One telling example is sub-Saharan Africa, where tax revenue to GDP rarely exceeds 20%, or is even lower. As a result, interest expenditures of the four largest commercial issuers--Angola, Ghana, Nigeria, and Kenya--account on average for a substantial 40% of fiscal revenues, even though they have only a moderate stock of debt (see chart 5b).

Chart 5a | Interest Payments Consume Over Half Of Budget Revenues In Some EM Sovereigns Government interest expenditure, 2022

EM--Emerging market. Source: S&P Global Ratings.

Chart 5b | Interest Spending Will Go Up For Many Sub-Saharan Africa Sovereigns Despite Stabilizing Debt Weighted averages for Angola, Ghana, Kenya, and Nigeria

Note: Data refers to the averages for Angola, Ghana, Kenya and Nigeria taken together. Figures refer to central government commercial debt, budget revenue and interest expenditures. Effective interest rate refers to interest expenditures divided by outstanding debt stock. Averages are weighted by annual nominal GDP converted to $ at period-average exchange rates. Source: S&P Global Ratings.

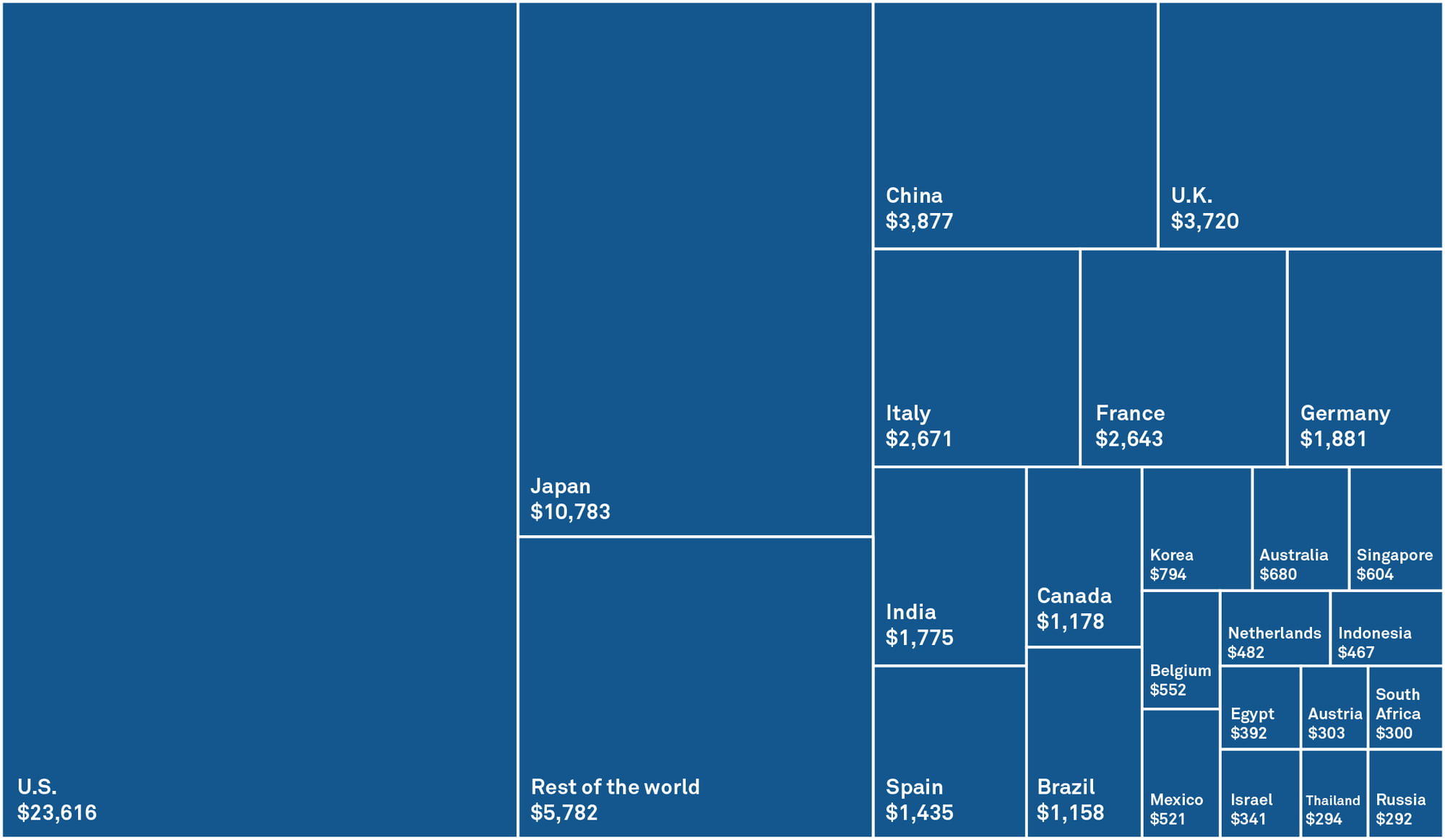

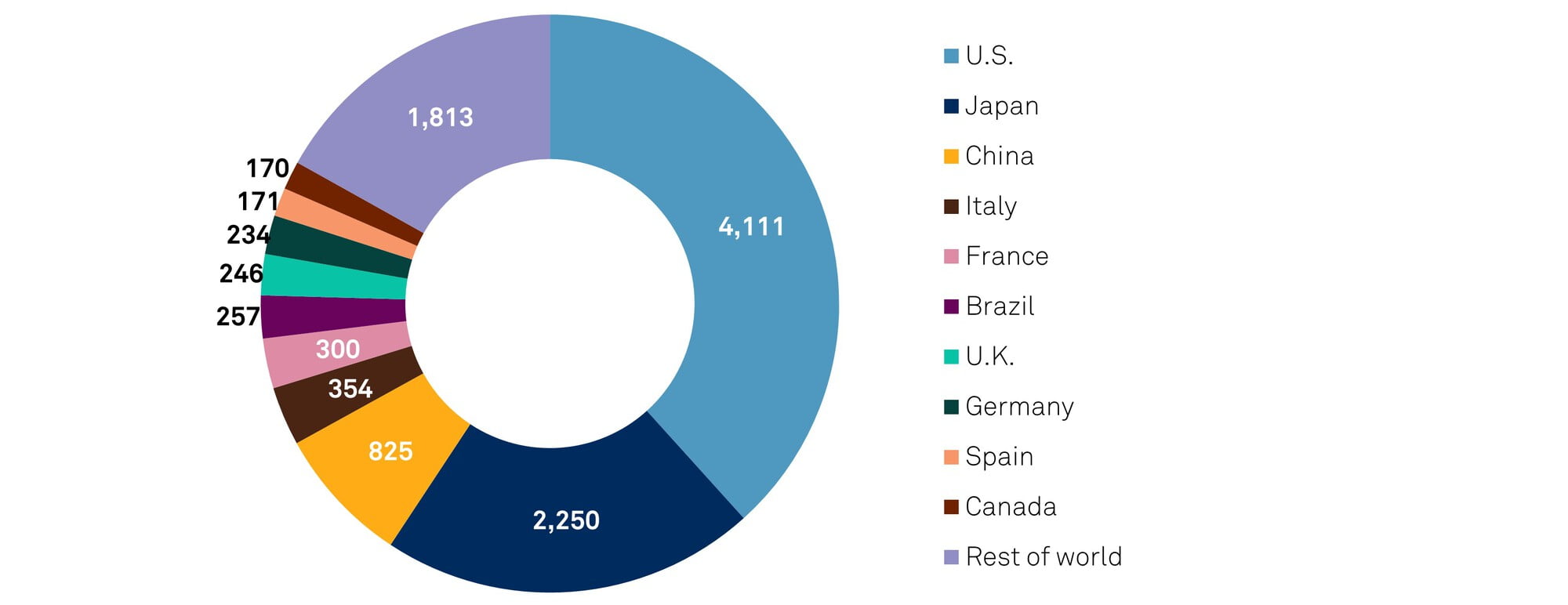

By end-2022, we project that the commercial sovereign debt stock will reach a record of $66.5 trillion, with the U.S. and Japan accounting for over one-half of it. The G-7 group of nations will continue to contribute 70% of the total commercial debt stock of all rated sovereigns (see chart 6). The U.S. and Japan are by far the largest sovereign issuers. We estimate they will account for about 60% of total global sovereign borrowing in 2022, with the U.S. alone accounting for around 38% of the global total (see chart 7). They are followed by China, which we forecast will issue around $825 billion in 2022, and Italy, France, Brazil, the U.K., and Germany, each of which we believe will raise about $250 billion-$350 billion in 2022.

Chart 6 | 2022 Commercial Debt Stock By Issuer: Total $66.5 Trillion Bil. $

Source: S&P Global Ratings.

Chart 7 | The U.S. And Japan Are The Largest Sovereign Issuers Sovereign long-term borrowing 2022 (Bil. $)

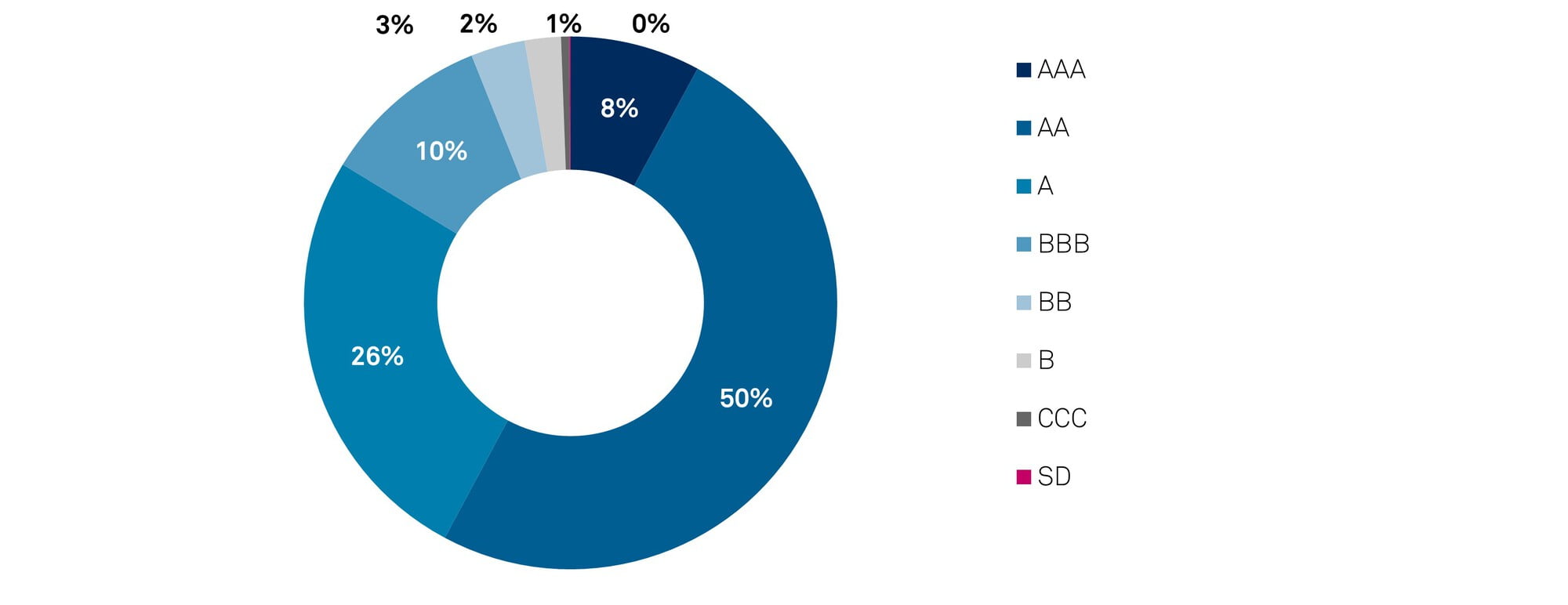

Investment-grade sovereign borrowing will account for the majority of total issuance. We project that, during 2022, the share of commercial sovereign debt rated 'AAA' (foreign currency rating) will account for a modest 7.9% of the total estimated commercial debt stock and 5.9% of total long-term commercial borrowing. Similar to recent years, about one-half of all commercial borrowing and the total debt stock will fall into the 'AA' category because three of the top six sovereign debtors fall into this rating category (the U.S., U.K., and France; see chart 8).

The share of the debt stock and long-term commercial borrowing by sovereign issuers rated in the 'BB' category or below (speculative grade) accounts for around 7% of the global total. Brazil, accounting for around $257 billion (or 2.4%) of global sovereign commercial borrowing, remains by far the largest speculative-grade borrower this year. Among all sovereign borrowers it ranks at No. 6 globally (see table 2). Other big speculative-grade sovereign borrowers in the top 20 sovereigns by absolute borrowing volumes in 2022 include Egypt and Argentina, accounting for a combined 1.5% of the global total.

Chart 8 | Investment-Grade Sovereigns Will Account For Most Of Debt Stock In 2022 Sovereign commercial debt (foreign-currency ratings)

The nominal stock of sovereign debt across all rating categories has increased steadily over the past decade, but debt profiles vary significantly by region. Excluding the G-7 countries (which distort average trends due to their size), we expect that about 70% of the debt stock of Asia-Pacific and 90% of developed Europe, Middle East, and Africa (EMEA) is in local currency, while above 70% is at fixed interest rates in 2022. By contrast, about 40% and 60% of emerging EMEA and Latin America's debt stock, respectively, are estimated to be denominated in foreign currency, while approximately 70% and 80%, respectively, will be issued at fixed interest rates.

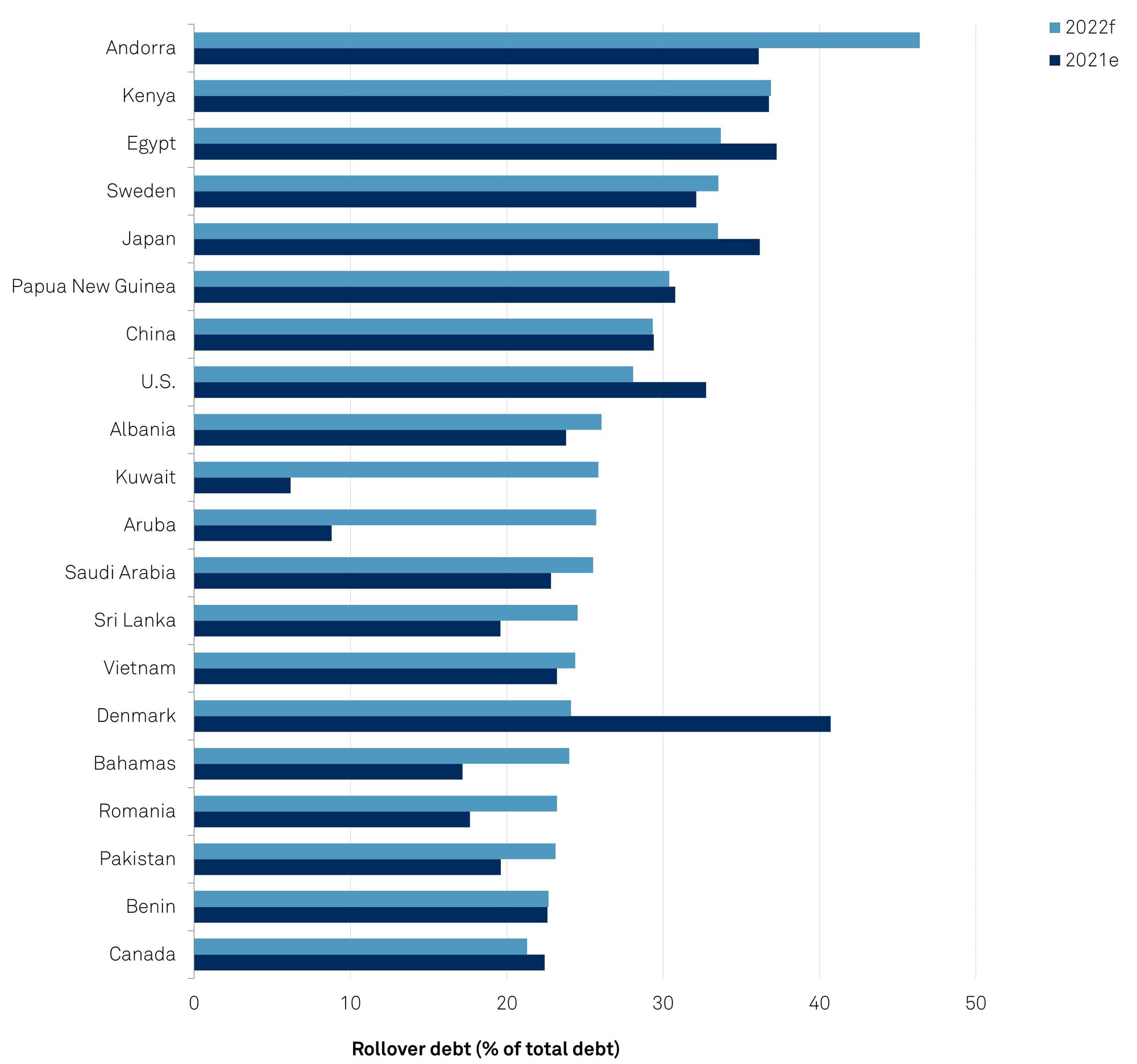

According to our calculations, among the bigger sovereigns, Kenya, Egypt, and Japan will face the highest rollover ratios in 2022 (see chart 9). This is a function of an elevated share of short-term debt, which constitutes about 26% of total debt for Egypt and 30% for Kenya, for example.

Chart 9 | Sovereigns With The Highest Debt Rollover Ratios

f--Forecast. e--Estimate. Source: S&P Global Ratings.

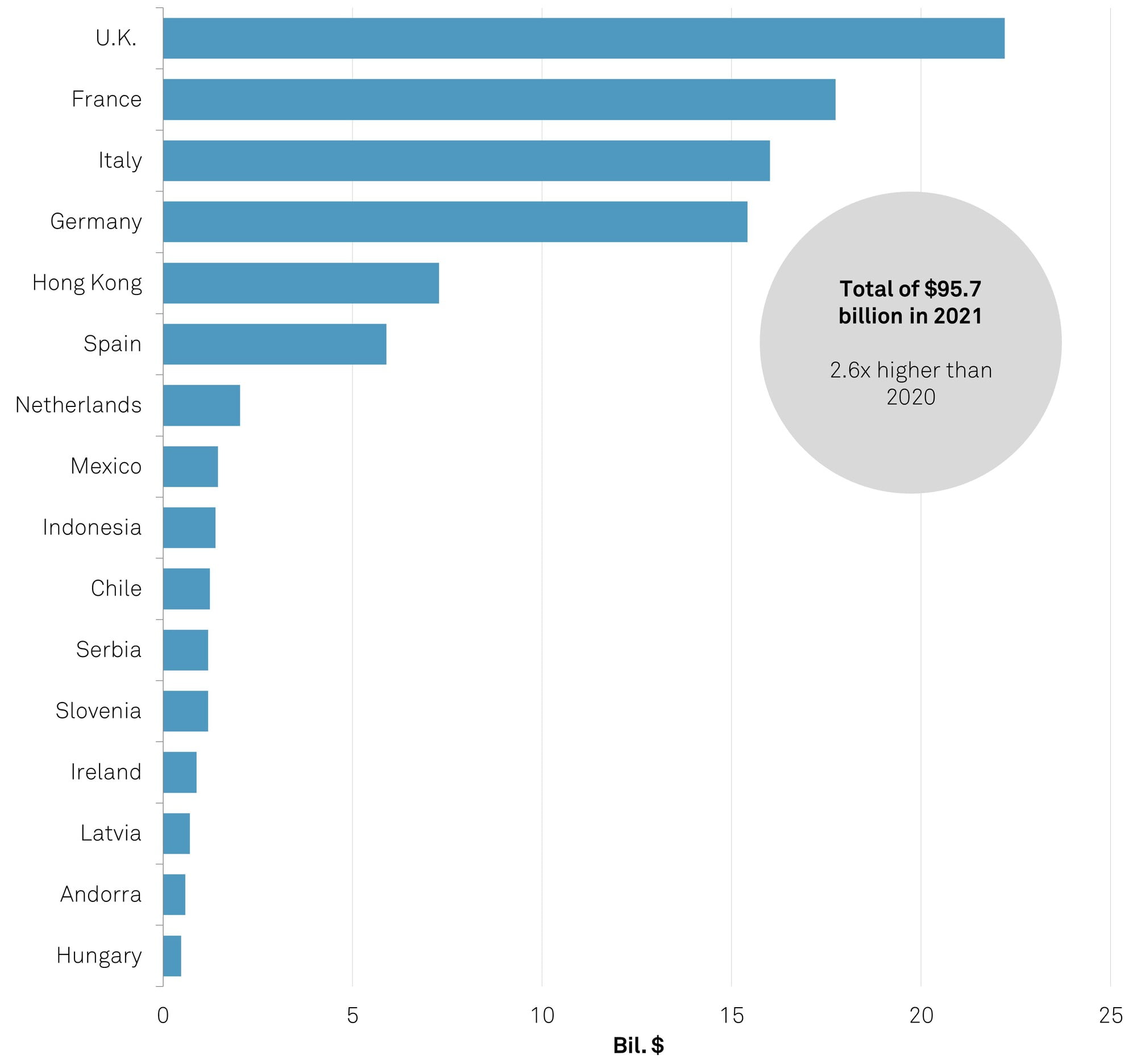

The sovereign green bond market has been growing at a fast pace, more than doubling over the past year. In 2021 alone, green issuance expanded more than 2.6x that of 2020, rising to $96 billion (see charts 10 and 11). The number of governments that issued green debt for the first time last year increased and included the U.K., Italy, Spain, Serbia, Slovenia, and Andorra.

We expect that at least 11 sovereigns will tap the green bond market in 2022. Even though rated sovereigns expect to issue a lower amount of green bonds ($46 billion) this year, we note that in the past years actual issuance substantially exceeded initial plans. We estimate the global green debt stock of 22 sovereigns that have by now issued such bonds will amount to around $171.1 billion in 2022.

Chart 10 | Green Sovereign Issuance Has Accelerated In 2021, But Total Amount Remains Small

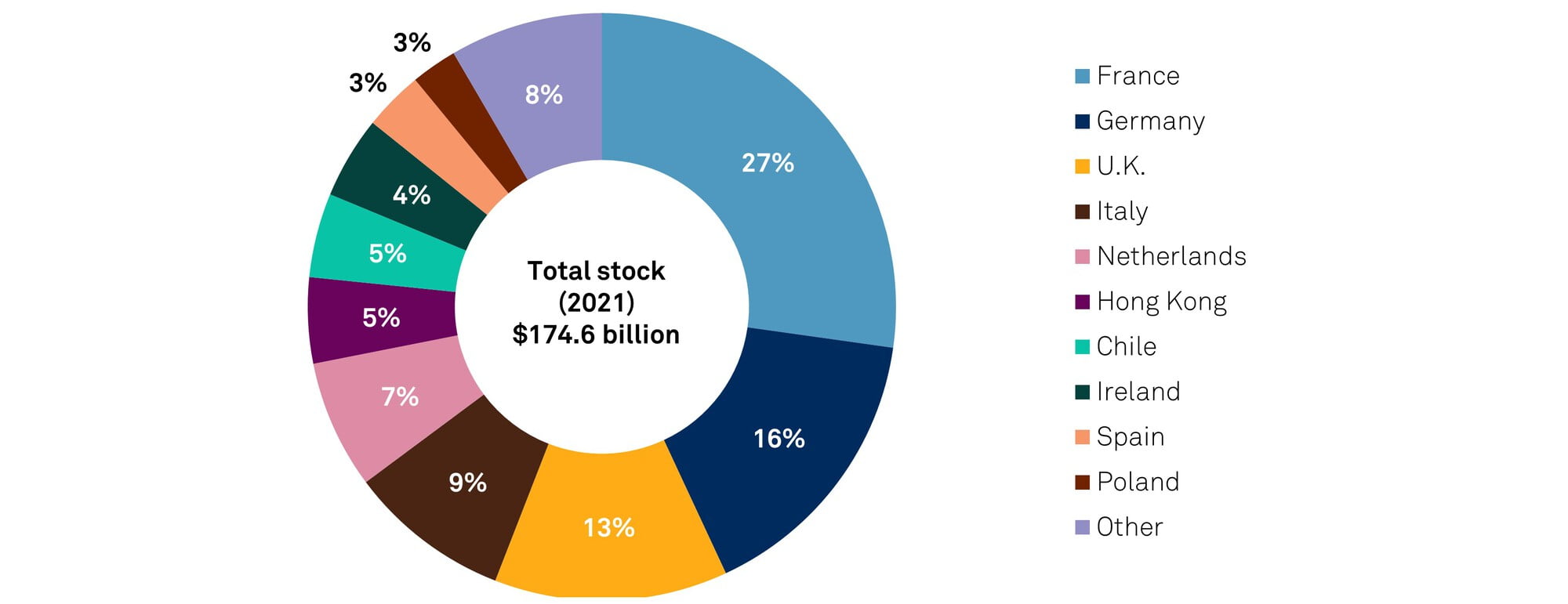

Chart 11 | France, Germany, And The U.K Are The Three Largest Green Borrowers

Estimates in this report do not take into account sovereigns not rated by S&P Global Ratings. Since few sizable sovereigns remain unrated, however, we see our data as a reliable reflection of global developments in sovereign debt and borrowing. Our estimates focus on debt issued by a central government in its own name. We exclude local government and social security debt, as well as debt issued by other public bodies and government-guaranteed obligations. In terms of commercial debt instruments, our estimates for borrowing include bonds, issued either on publicly listed markets or sold as private placements, as well as commercial bank loans. We do not include government debt that some central banks may issue for monetary policy purposes. All reported forecast figures are our own estimates and do not necessarily reflect the issuers' projections. Our estimates are informed by our expectations regarding central government deficits, our assessment of governments' potential extra budgetary funding needs, and our estimates of debt maturities in 2022. Estimates that we express in U.S. dollars are subject to exchange-rate variations.

This global report summarizes a series of simultaneously released regional sovereign borrowing and debt reports. We have produced detailed reports for developed EMEA, emerging EMEA, Asia-Pacific, and Latin America.

Table 2 | Gross Commercial Long-Term Borrowing

Table 3 | Total Commercial Debt At Year-End (Long- And Short-Term)

Table 4 | Central Government Rollover Ratios And Debt Structure (% Of Total Debt, Including Bi-/Multilateral)

Secondary Contacts

Michelle Keferstein Frankfurt +49-693-399-9104

Constanza Maria Chamas Mexico City

Research Contributor

Hari Krishan Mumbai CRISIL Global Analytical Center, an S&P affiliate