Tough times ahead as recycled plastics struggle with sustainability shifts

US, Europe coronavirus supply impact to be felt through H2 2020

Planned Asia recycling plants delayed amid economic uncertainty

The repercussions of the coronavirus pandemic look set to test recycled plastics markets across the globe in the second half of the year, with tight supply and poor economics the key hurdles for both sellers and buyers.

Sustainability commitments tested as US R-PET economics pose challenges Prior to the coronavirus outbreak, the US recycled plastics industry had already been plagued by extremely cheap virgin PET, high fixed-processing costs and export restrictions, leading to calls for systemic and policy reform initiatives across the supply chain. In 2019, Congress saw an historic influx of recycling-related legislation.

However, in the first half of the year, most sustainability legislation took a back seat as the US focused on containing the coronavirus.

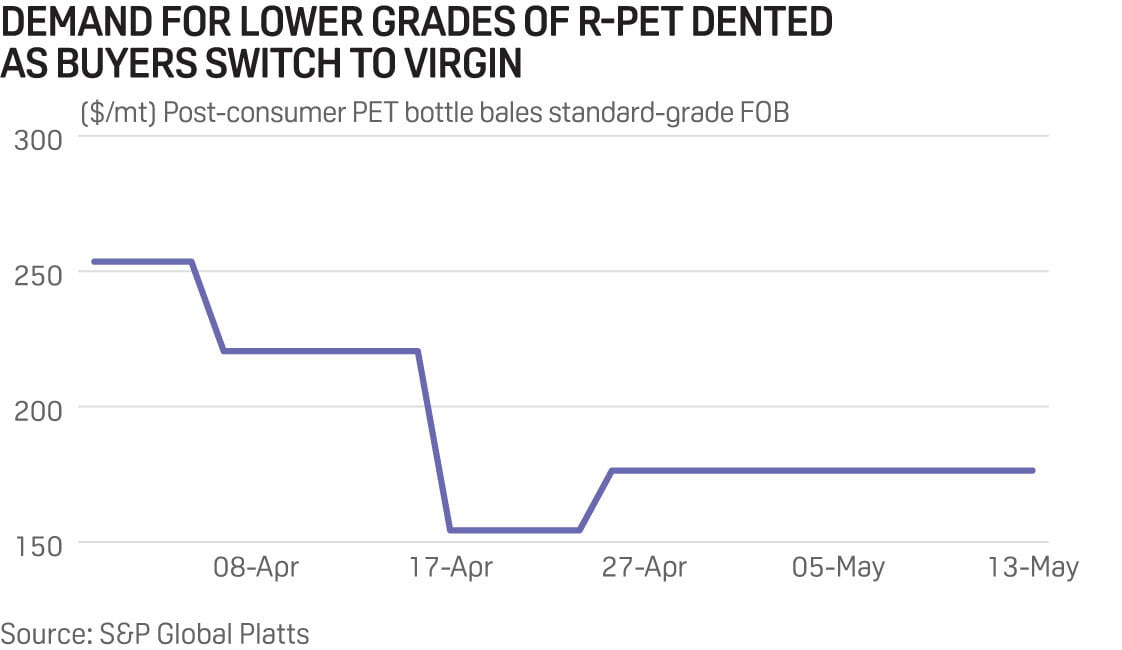

Without government mandates, R-PET demand is expected to remain weak as cost-sensitive bottle manufacturers increasingly reject recycled material for low-cost virgin resin, which saw historic lows in April.

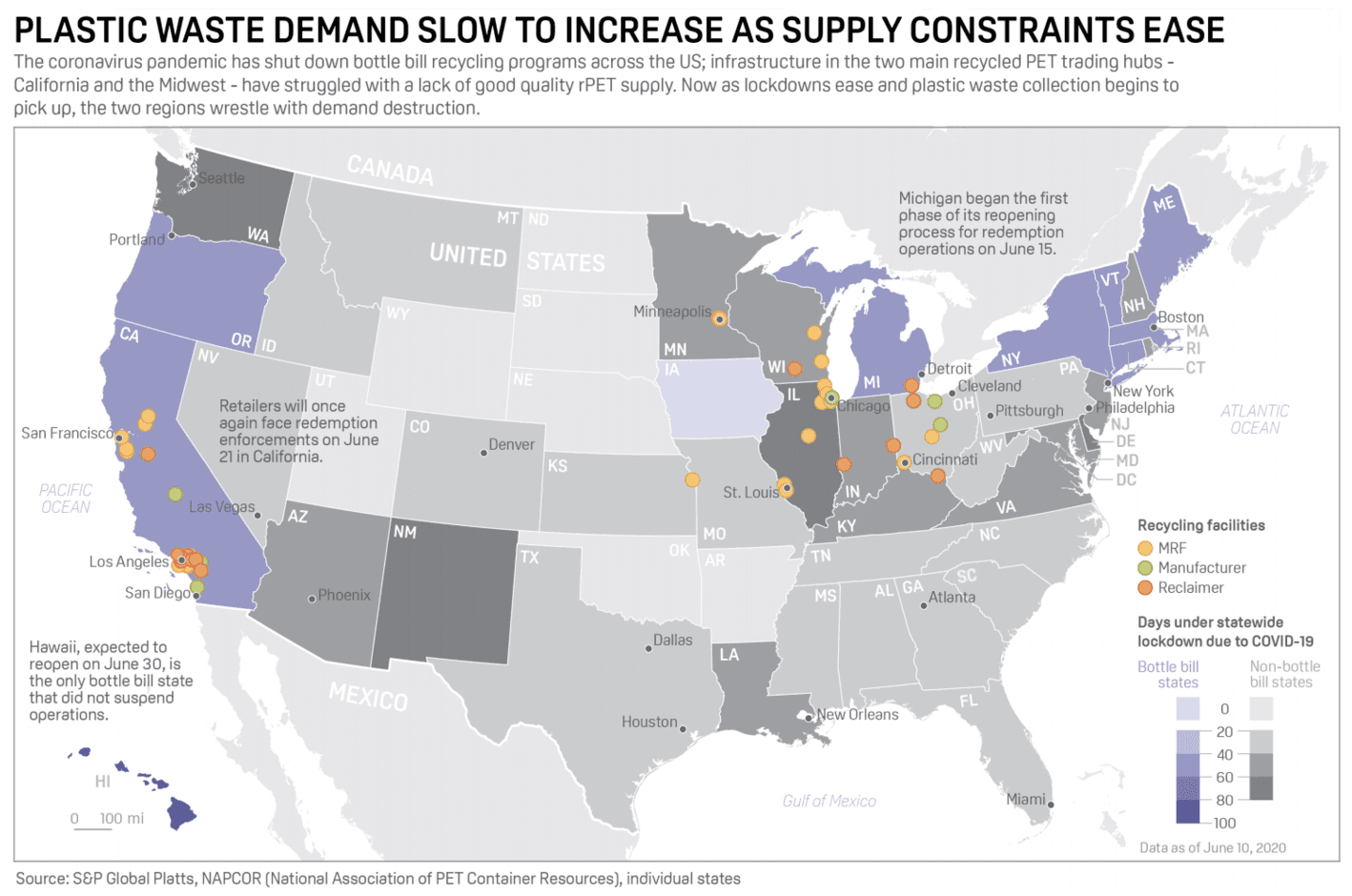

Supply of post-consumer bottle bales has been severely limited during the pandemic due to labor shortages, collection cuts and bottle bill suspensions, prompting PET bale prices to surge and recycled flake/pellet output to decline.

Therefore, given low-cost virgin PET prices and R-PET supply constraints, many end users in the flake to packaging sector struck 6-12 month contractual agreements with resin producers to secure reliable PET supply.

The recycled PET fiber market will likely bear more of the brunt of the imbalance between virgin and recycled PET. Demand will remain weak in the near term as the textile, carpeting and automotive industries continue to face global manufacturing slowdowns and are forced to curtail operations amid financial constraints.

Even if supply volumes and demand levels begin to normalize in H2 2020, some market participants fear the full PET reclamation chain will be unable to survive. Overall, market sources expect R-PET buying and selling to shift away from contracts towards the spot market this year as the future relationship between virgin and recycled PET remains uncertain.

European sustainability commitments endure downturn; supply still key concern The European virgin and recycled PET markets have been decoupling since mid-2019, but H2 2020 will bring fresh concerns for participants looking to secure supply.

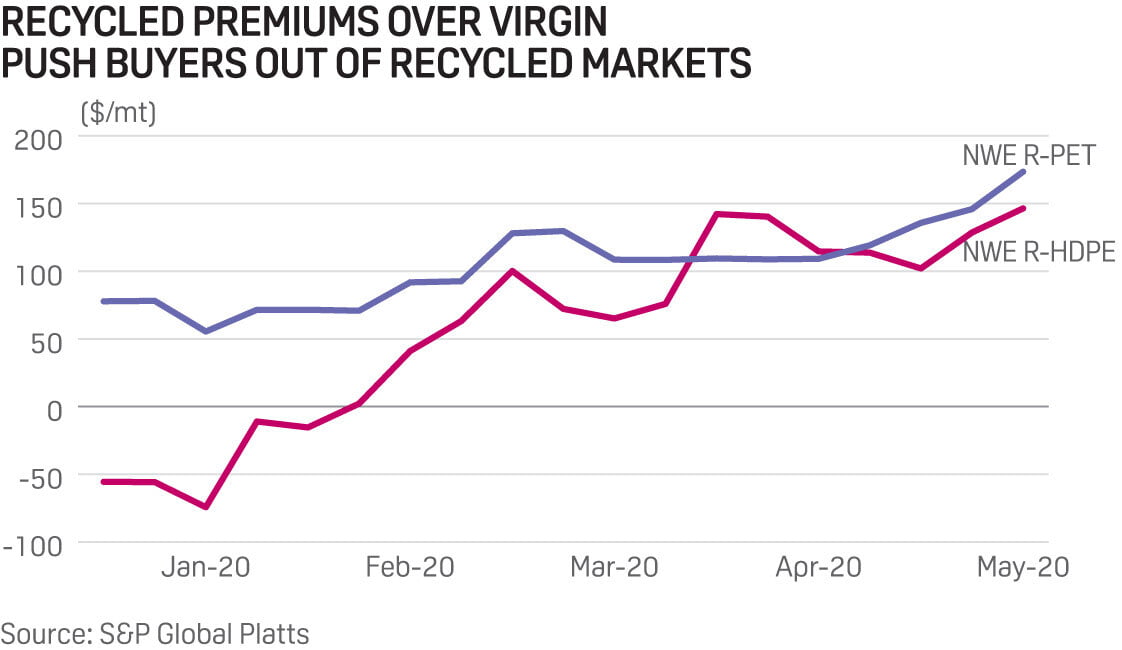

Recycled HDPE and PET premiums over virgin equivalents have increased during the coronavirus pandemic, partly due to more stable demand than virgin but also to high-cost bales and squeezed margins for recyclers. This primarily caused fragmentation in the recycled markets, with demand for higher grade material robust and lower-grade suffering the full effects of the economic slowdown.

As in the US, more economically sensitive buyers — such as those purchasing construction and automotive grades of R-HDPE or tray and sheet participants in the R-PET market — switched further volumes to the virgin market. By mid-May pricing was lower than during the 2008-09 global financial crisis.

At the top end of the market, however, dwindling supply is being consolidated by a small proportion of larger buyers, who remain committed to publicly announced sustainability initiatives.

Across the board, supply was, and will remain, hampered by the coronavirus. Cancellation of large sporting events and mass gatherings over the summer will dampen demand, with far less post-consumer material entering the recycling supply chain moving into the third quarter.

Recyclers may remain reluctant to purchase post-consumer material if margins do not recover.

With pressure from the low-priced virgin market on recycled PET flakes, margins are under pressure; this will lead to lower volumes and even the halting of production of lower grades of R-PET and R-HDPE.

Instead, recyclers will try to offset lower volumes by producing higher quality grades such as R-PET food-grade pellets and R-HDPE natural pellets, where ready buyers remain.

Asian recycling business growth slows Asian recycling businesses are expected to continue expanding, though at a slower rate due to the coronavirus.

Major projects to increase recycling capacity remain in the pipeline, expected to be brought online in the coming six to 18 months, including but not limited to new capacity of 50,000 mt/year of R-PET and R-HDPE from PTT Global Chemical and Alpha Packaging in Thailand, 25,000 mt/year of R-PET from Veolia Services Indonesia, 16,000 mt/year of R-PET from PETValue in the Philippines and 30,000 mt/year of R-PE film from Suez in Thailand.

Nevertheless, the current economy is particularly challenging for small and medium-sized enterprises. Countries lacking infrastructure for both waste collection and reprocessing will see scant government support, with other sectors of their economies the more immediate priority, observers said. Some recyclers are likely to remain closed even after lockdowns due to scant waste and sorting collection supply, and concerns of virus exposure from handling materials, sources said.

The pandemic has also delayed the transition to higher-end applications by at least six to 18 months, a source said.

— Benjamin Brooks, Sarah Schneider, Miranda Zhang

Platts European Recycled HDPE

Platts Asian Recycled PET

Platts European Recycled PET

Platts US Recycled PET