By Kevin Allen, Kristen Hays, Hui Heng, Miguel Cambeiro

As the monoethylene glycol industry moves into the second half of 2021, a combination of renewed lockdowns, prolonged recessions and new anti-dumping duties in Europe on US- and Saudi Arabia-origin material presents a bleak picture at a time of limited visibility, market participants said.

xpectations of ample supply from new production facilities in China and US by H2 2021 also pose headwinds to recovery going forward.

Expectations of ample supply from new production facilities in China and US by H2 2021 also pose headwinds to recovery going forward.

However, many Asian market participants were unsure of the new China coal-based capacities starting up in 2021, heard to amount to more than 5 million mt/year and accounting for as much as 20% of current Asian MEG global capacity by year-end. Downstream textile industry demand expansion was lagging Asia's MEG supply growth by more than 1 million mt/year in 2021, mainly that of naphtha-based MEG, amid the global economic recession, a market participant said.

On a brighter note, the potential for a sharp decline in Asian prices was limited as poor margins would prompt less competitive Asian MEG makers to reduce operating rates, they said.

MEG prices generally move with crude. Average Asian integrated MEG margins will still be positive to incentivize producers to continue operations, sources added. China was still expected to import around 10 million mt/year or more by the end of 2021 on economic recovery post COVID-19.

Traders said more US supply was expected to reach Asia in the coming months as plants ramp up output after the deep freeze that hit the US Gulf Coast in mid-February which forced widespread weeks-long petrochemical shutdowns, including more than 4 million mt/year US MEG capacity.

China will continue to dominate trade flows as it accounted for 60%-70% of global demand, market sources said. Nearly 42% of 2.2 million mt of US MEG exported in 2020 went to China, South Korea and India, according to US International Trade Commission data.

Trade flows could see more changes after the European Commission imposes new antidumping duties on US- and Saudi Arabia-origin MEG in June 2021 as expected.

The EU announced May 14 that US companies would face provisional duties ranging from 8.5% to 52%, while Saudi companies would face 11.1% duties. ITC data showed that 16.4% of US MEG exports went to European countries in 2020, including the non-EU UK. Those flows increased during the summer of 2020 when US spot export prices had fallen to what was then an 18-year low of 14 cents/lb FOB USG, largely on oversupply. US market sources said a dropoff in European demand would send volumes looking for other homes, particularly in Asia.

"That's looking more and more to be the case because there are not many other options," a US-based source said. "It will be a fight for Turkey, Brazil, China and India."

US spot export MEG prices was already expected to retreat in H2 2021 if supply availability grows as anticipated, and the antidumping duty news from the EU should add to that downward pressure, market sources said. Overall, US MEG output was expected to return to normal after some turnarounds by the third quarter of 2021 and bring prices down as well, US-based sources said.

US MEG capacity was also expected to climb to 5.75 million mt/year by the end of the year when ExxonMobil and Sabic start their new joint venture petrochemical complex in Texas in the fourth quarter, which includes a 1.1 million mt/year MEG plant.

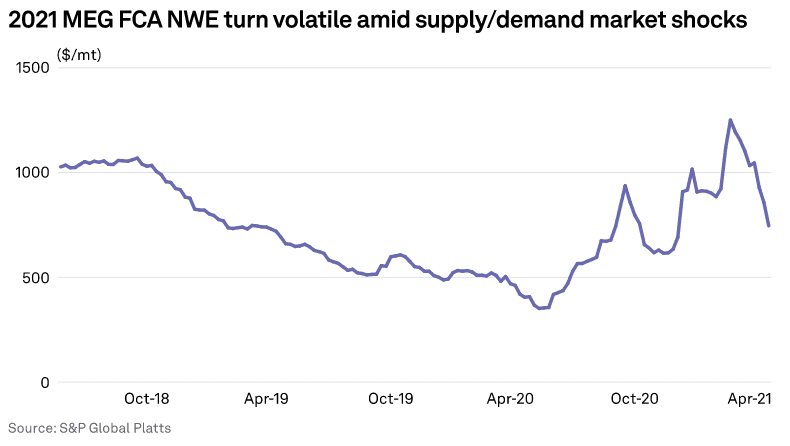

In Europe, after hitting an all-time high truck price of $1,250.45/mt FCA NWE on March 5, MEG prices were expected to continue falling in H2 2021 with supply tightness now no longer a concern as import vessels had started to arrive. In addition, market participants expect demand to weaken as COVID-19 infections rise in some key demand centers such as India, Turkey, and Germany.

A lockdown in Turkey, record-high COVID-19 infections in India and rising infections in Germany were expected to dampen demand, when seasonal demand for plastic bottles should be at its highest.

However, a MEG price decline could be stemmed by a slump in downstream terephthalate demand due to a force majeure declared in March at INEOS' co-feedstock purified terephthalic acid in Geel, Europe's largest, depending on how long the outage lasts.

"It's high season now. There are holidays and people want to get out but it's the total opposite in Germany, where you are not allowed to enter any store without a quick test," a trader said. "That doesn't help PET bottle [demand], and no concerts are allowed. If INEOS starts production then I think that this [price decline] could be reversed."