By Luke Milner, Fumiko Dobashi, Callum Colford, Astrid Torres

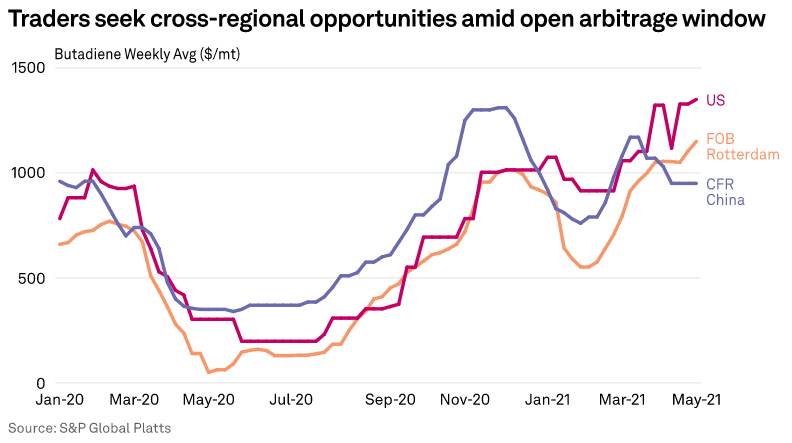

Traders will continue to seek arbitrage opportunities in global butadiene market in the second half of 2021 as plant hiccups and additional capacities globally continue to trigger additional cross-regional spot activities.

Trading sources said the US market maybe a demand spot in H2 amid persisting tight supplies, while Asian suppliers may actively try to export to the Americas in a bid to clear excess supplies after capacity expansions.

Trading sources said a 5,000 mt spot cargo was fixed to the US from South Korea in mid-May for early June loading. The sources also said some traders are seeking opportunities to export ex-China cargoes to the Americas, possibly Mexico. They said it is difficult to sell ex-China cargoes to the US due to an additional 25% tariff.

With 20% of US butadiene production curtailed since TPC Group’s Port Neches explosion and fire in 2019, the US has seen varying extents of supply tightness since. As a result of continued supply constraints, sources anticipate a bullish H2 2021 until TPC Group’s recent operational issues in Houston resolve possibly leading to a mild improvement.

US butadiene exports in 2020 fell more than 13.7% year on year, according to US International Trade Commission data. The US shipped 61,632 mt of butadiene overseas in 2020, down 9,842 mt from 71,475 mt in 2019. US butadiene exports are expected to continue falling throughout 2021 with exports falling 55% in the first quarter of 2021, according to USITC data.

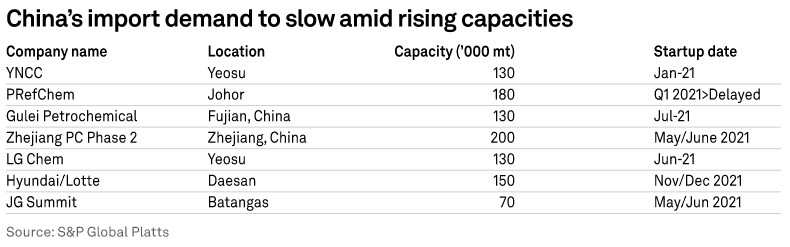

Supplies from South Korea are expected to increase from June in line with a planned startup of new butadiene unit. South Korea’s LG Chem plans to start up its new 130,000 mt/year butadiene plant in Yeosu in the middle of June 2021.

China will continue exporting butadiene in the second half of this year amid rising supplies in line with new plant startups, including China’s Zhejiang Petrochemical, which planned to start up its new 200,000 mt/year butadiene plant in Zhejiang in Q2.

Market sources said China’s butadiene would continue to be supplied to South Korea, which is the nearest outlet for Chinese suppliers to export. According to the Korea Customs, South Korea imported 19,887 mt of butadiene from China for January to March; the equivalent of almost 79% of the 25,232 mt total imports to South Korea from China in 2020.

Amid rising supplies in Asia and expected tightness in the US, European suppliers will likely eye the US market to seek arbitrage opportunities as well.

European exporters are also closely watching the US for any signs of waning demand as production in the region returns to more normal levels following the months of disruption after February’s winter storm that battered the US Gulf.

Butadiene is a key feedstock for synthetic rubber, which is used for tires. As a result, the recovery of automobile sector is a key for the butadiene market.

Global automobile output is seen to be increasing in 2021, when compared with 2020. Toyota, the largest carmaker in the world, forecasts its global vehicle sales for the 2021 fiscal year (April 2021 to March 2022) to increase 14% from a year earlier to 8.7 million units, according to the company’s financial results for 2020.

Market participants expect automobile output to recover in Europe and the US as economic activities are returning normal after COVID-19 cases are coming down.

“European car sales figures are now looking positive, with lockdowns easing this will progressively continue and improve,” a producer said. Styrene-butadiene rubber producers in Europe also anticipating stronger demand, with increased driving levels once lockdown measures are eased expected to increase demand for replacement tires.

The world’s largest tiremaker Bridgestone also expects tire demand in 2021 will recover to 2019 levels, according to the company.

However, there is still a downside risk. In Asia, the surging COVID-19 cases in India and some Southeast Asian countries may slow down automobile production, while globally, a shortage of microchips may pressure automobile output as well.

Market sources said in Asia, the styrene-butadiene-rubber market maybe supported by a firmer natural rubber market. Natural rubber production may be impacted in the beginning H2 due to lower production in Malaysia and India amid surging COVID-19 cases.

The European toluene market is expected to see stable supply conditions in the second half of the year, as well as improving demand from the gasoline blending sector due to summer vacations mixed with easing lockdown conditions across the continent.

Material tightness that raised premiums sharply in early 2021 was driven by a lack of domestic production capacity. Planned and unplanned maintenance turnarounds at major European production sites left material thin on the ground as petrochemical demand for TDI-grade toluene remained steady.

With outages potentially extending into June, availability is not expected to normalize until the second half of the year.

Demand has also been bolstered by strong US interest in European molecules. The export market will remain in strong focus going forward for European sellers.

Much of the bullishness for benzene in Europe has been driven by lost production from a planned maintenance at ExxonMobil’s Botlek refinery during the second quarter, with impact on material availability expected to extend into Q3. As benzene supply normalizes in Europe, this could see supply tightness ease, and demand for disproportionation drop.