By Emmanuel Gallegos, Astrid Torres, Melvin Yeo, Abdulaziz Ehtaiba

The global propylene outlook for the second half of 2021 holds uncertainty and challenges for market participants as COVID-19 related issues continue to impact both the demand and supply sides.

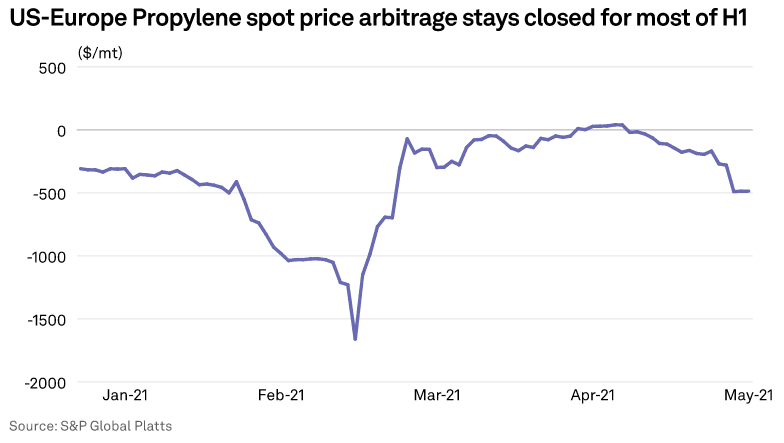

The underlying supply shortage in the European propylene market will likely persist for most of 2021 as upcoming cracker turnarounds in Q3 and an absence of US imports continue to lend support to price levels.

In March, FD NWE polymer-grade propylene prices rallied to levels last seen in 2018, hitting Eur1,120/mt ($1,353/mt) on March 8, as strong demand from derivatives was met with insufficient supply due to a lack of imports and reduced refinery FCC run rates.

Market participants expect firm spot propylene prices to remain for much of the second half of 2021 with at least three cracker turnarounds scheduled to take place on the continent, which will keep supply snug. Fresh regional COVID-19 related lockdowns in H2 could see the availability of chemical-grade propylene tighten as refinery fluidized catalytic crackers adapt to changes in gasoline demand.

Consumption of propylene from downstream derivatives is expected to remain healthy as the positive impacts of stay-at-home orders continue to support the market for the remainder of the year. “I believe prices will be at a premium to the contract price all year long, there is a big demand for products, people continue to purchase online goods,” a trader source said.

Europe remains net short of propylene and relies on imports from the Middle East and the US to supplement domestic supply. The structural flow of US imports into Europe stopped in 2020 and has remained halted throughout the first half of 2021. Participants will be watching the US-Europe arbitrage closely to make use of any import opportunities.

US market participants have a bearish outlook for propylene in the second half of 2021 amid mixed market fundamentals.

The PGP market has faced increased volatility since the start of the pandemic, reaching an 11-year low and an all-time high in the span of a year. PGP quickly recovered throughout last year following the historic low in April 2020 as the market faced many supply issues that culminated in February 2021 when PGP prices reached $2,755/mt FD US Gulf Coast basis, the highest since Platts began assessing the market in 1998, during the US Gulf Coast freeze that shut down or curtailed operations for suppliers.

PGP had already reached an all-time high of $2,160/mt prior the freeze as recovering downstream demand pushed prices higher and Enterprise’s propane dehydrogenation unit went down for a scheduled maintenance on Feb. 1. During the freeze, the two other Gulf Coast PDHs shut down and prices soared by a further $600/mt.

With no upcoming planned maintenance on PDH units, market participants are expecting propylene output to increase and prices to fall in H2 2021. Demand is expected to continue strengthening throughout 2021 as consumers spend more. However, while availability will improve and prices will fall from record highs, the looming semiconductor shortage leaves downstream products with fewer outlets than they would otherwise have -- such as polypropylene for vehicles that cannot be built without chips. Semiconductor production declined in 2020 when COVID-19 shutdowns crushed demand for durable plastics and has not been able to ramp up fast enough to meet the strong rebound in demand.

The Asian propylene market is expected to remain stable in H2 2021, amid the startup of new crackers and PDH plants, fewer planned turnarounds and the expected arrival of deep-sea cargos.

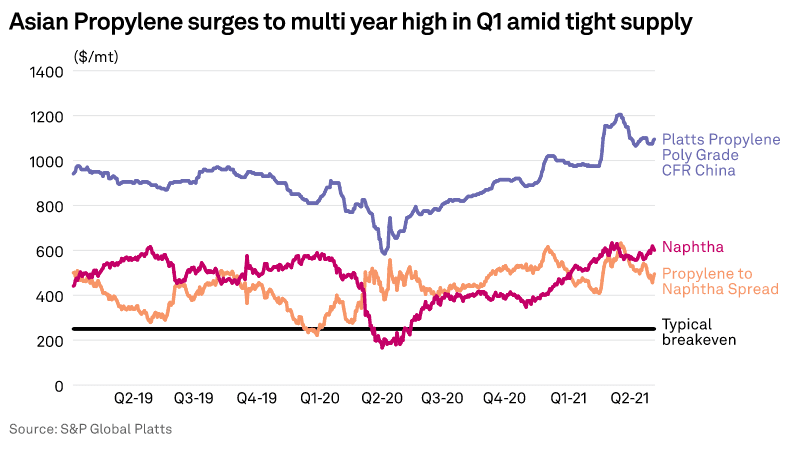

The propylene CFR China marker hit a multi-year high on March 17 at $1,205/mt as a fall in spot supply from Korea, increased demand after the Lunar New Year holidays, and a lack of exports from the US amid adverse weather in February saw a surge in the spot price.

The startup of two crackers owned by GS Caltex and LG Chem by June, with a total propylene capacity of around 900,000 mt/year, is expected to boost overall supply to buyers in Asia.

"Many crackers in NE Asia have completed their turnaround in H1, and more deep-sea shipments from the US are arriving in H2, we can expect more propylene supply," said a regional supplier.

Elsewhere, Jinneng Science and Technology in China is on track to finish building its new 900,000 mt/year PDH plant and 450,000 mt/year polypropylene in Qingdao by Q3, absorbing a portion of the supply.

The propylene market in Southeast Asia is also expected to see stability as Hyosong Vina plans to postpone the startup of its new 600,000 mt/year propane dehydrogenation plant in Vung Tau, Vietnam to August, a delay from June.