By Kristen Hays, Astrid Torres, Chris Liu, Miguel Cambeiro

US-Asia ethylene flows were expected to ramp up in the second half of 2021 as US output returns to normal months after a historic Texas freeze caused weeks-long cracker outages that squeezed supply and pushed prices to record highs.

However, high freight rates could continue supporting a shift in spot flows to Europe, with flows to Asia largely contract cargoes, as post-freeze prices normalize, market sources said.

The Asian ethylene market in H2 2021 is expected to be balanced to stronger despite new cracker start-ups and expansions in China and South Korea increasing supply and an unclear demand outlook as COVID-19 surges prompt shutdowns or increased restrictions that were suppressing downstream demand in some regions, notably India.

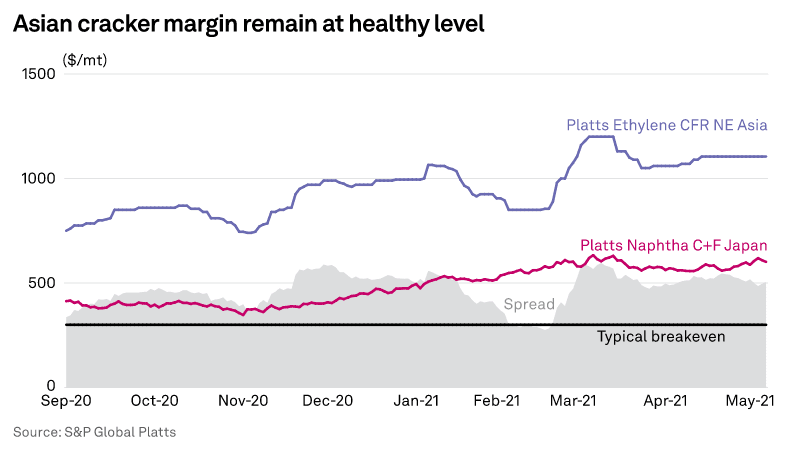

Asian market sources expect high overall operating rates for steam crackers in the region because of healthy petrochemical margins and a wider naphtha/ethylene spread.

“For the naphtha and gas feed steam crackers, the margin would be favorable to the cracker operators,” a market source said. “However, for the CTO (coal-to-olefin) it might be challenging due to environmental concerns.”

Trade sources expect the US-Asia arbitrage window to re-open during the second half of the year as US ethylene prices retreat from six-year highs reached in April. Prices shot up following sustained subfreezing temperatures in the US Gulf Coast and much of the country in mid-February, forcing widespread petrochemical shutdowns that included more than 70% of 40 million mt/year of US ethylene capacity.

In the US, ethylene demand is expected to be strong in the second half of 2021 due to robust downstream demand and a re-opening of the US-Asia arbitrage.

US ethylene output recovered slowly from the mid-winter freeze, as producers gradually ran material through crackers to find cracks, pinhole leaks and other issues. The delays upstream meant downstream restarts had to wait for cracker ramp-ups. Downstream units also had to restock depleted inventories and supply chains as growing demand for ethylene products surged.

The US economy was still recovering but the government’s various stimulus measures supported consumer demand and consequently increased the pull for ethylene and its derivatives.

While producers meet increased demand, they also expect to spend the rest of 2021 playing catch-up from the freeze.

“We expect markets to remain tight through at least the end of this year due to very high demand, low inventories and the capacity that will be lost during planned downtime,” LyondellBasell CEO Bob Patel said during the company’s 1Q earnings call on April 30.

And part of that catch-up is expected to be US ethylene export growth after a retreat from the freeze-induced shutdowns. US ethylene exports more than doubled year-on-year in 2020 to 650,743 mt as Enterprise Products Partners ramped up its export terminal along the Houston Ship Channel. Asian countries received 86% of those volumes, up from 27% in 2019.

Spot and contract export volumes were expected to continue rising through 2021, particularly with the US-Asia arbitrage seen re-opening. When closed, most vessels fixed to Asia were contract rather than spot, and more spot vessels were seen heading to Europe.

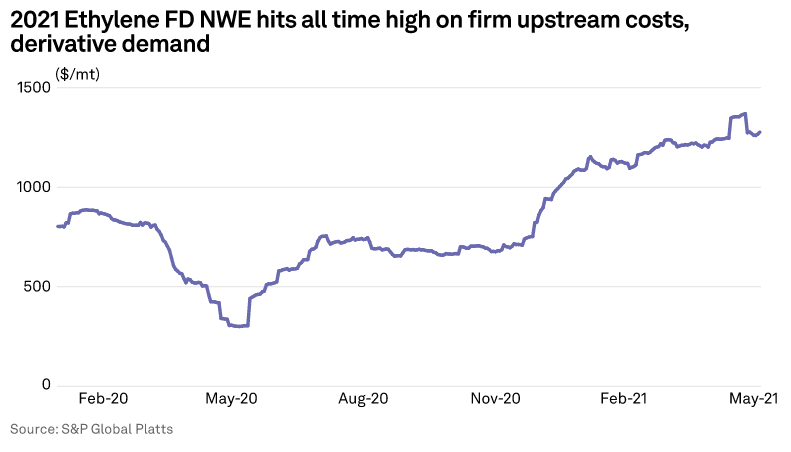

In Europe, ethylene supply was expected to resume normal levels in Q2 2021 as increased supply alleviates tightness that kept differentials against the industry-settled contract price in a range between parity and historically high premiums of up to 10%. European ethylene is typically a net-long market in which spot volumes trade at discount differentials to the industry-settled contract price.

In the second quarter, upstream naphtha costs stabilized amid a pushback against downstream polyethylene and polyvinyl chloride pricing that had reached record highs. COVID-19 surges in Turkey, a major market for European products, and India prompted more lockdowns, suppressing demand.

“Some European derivatives are starting to struggle with the high spot prices,” a European producer said.

The other driver is US ethylene production, which hasn’t been the same since the start of the pandemic in Q2 2020. A resumption in US ethane and ethylene production back to pre-pandemic levels is expected to improve global supply, with imports flowing to Europe as needed, sources said.

“Maybe ethylene will be more available, so we’ll see fewer skyrocketing prices. I’m not expecting to see premiums in Q3,” another source said, noting it would “move to a slight discount. It could even be between a 5%-10% discount come Q3.”