Feb. 04, 2022

Sandeep Chana London +44-20-7176-3923

Marta Stojanova London +44-20-7176-0476

Shane Ryan London +44-20-7176-3461

This report does not constitute a rating action.

European collateral loan obligations (CLOs) typically benefit from portfolio diversification, both from an issuer and sector perspective, with CLO managers maintaining portfolios of leveraged loans that have an average exposure to 156 different corporate issuers operating across 39 different industry categories.

In this publication, we examine the aggregate asset quality held by European CLOs, observed through key credit metrics and consolidated by S&P Global Ratings’ CLO industry sectors. Specifically, this edition of sector average metrics for European CLO assets focuses on loans issued by 687 corporate issuers, which represents over 95% of the assets under management (AUM) held in reinvesting European CLOs rated by S&P Global Ratings as reported at Sept. 30, 2021. We calculated the average metrics for all floating-rate assets with both an S&P Global Ratings' credit rating and an S&P Global Ratings' recovery rating (the S&P Global Ratings-rated CLO assets), weighted by the euro notional exposure to each asset.

Based on our review of third-quarter 2021 data, the average reinvesting European CLO portfolio rated by S&P Global Ratings exhibited the following changes:

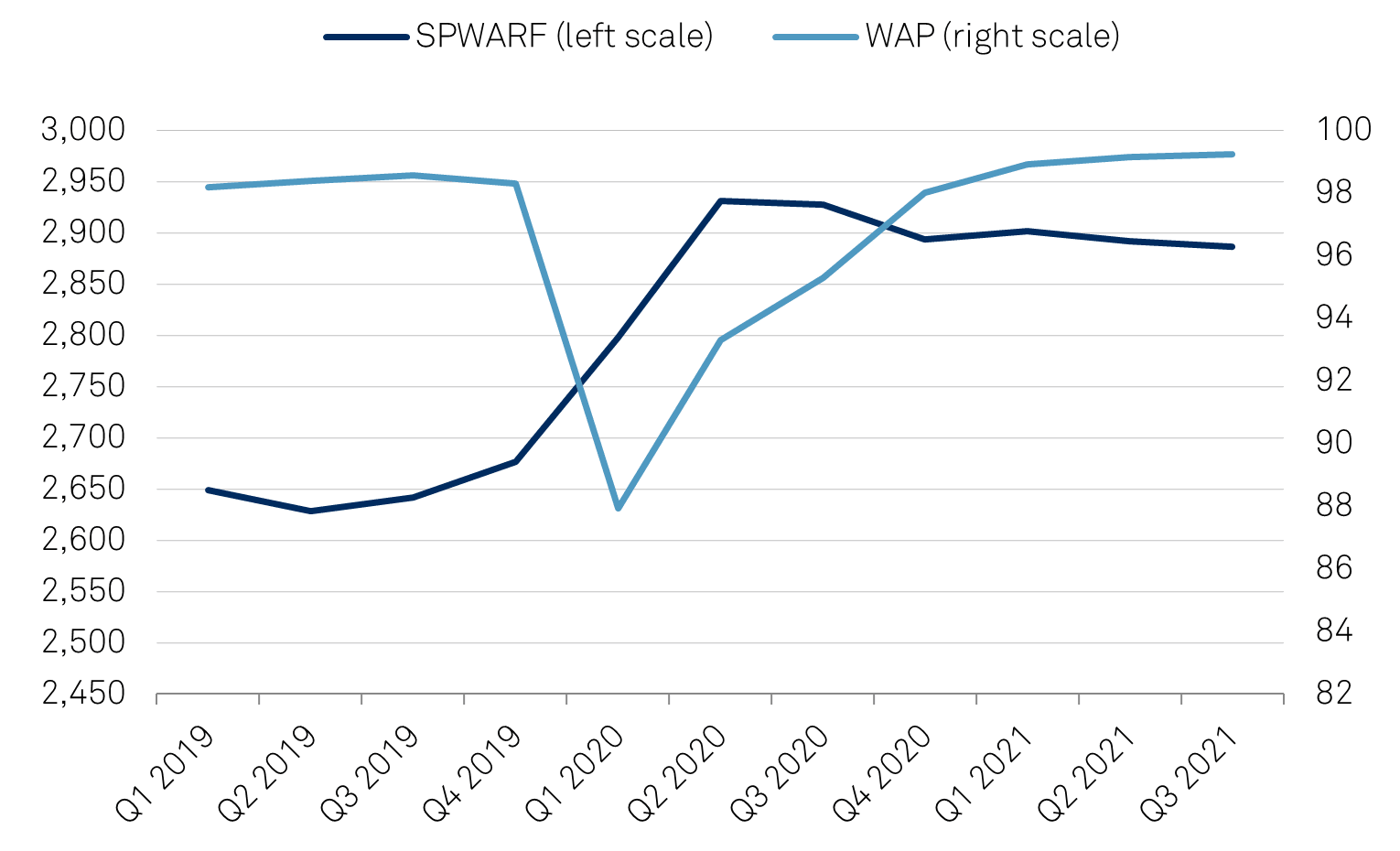

Chart 1 | SPWARF And WAP Movements In European CLO Portfolios

Q--Quater. WAP--Weighted-average price. SPWARF--S&P Global Ratings' weighted-average rating factor.

The third-quarter 2021 median debt-to-EBITDA and interest coverage ratios of issuers present in European CLOs improved to 6.5x and 3.4x, respectively. Over this period, European CLOs added 63 new obligors to the pool of assets compared with year-end 2020. Only 17 obligors had interest cover below 1.0x, including Piolin Bidco S.A.U. (Parques Reunidos), which was upgraded in December to 'B-' from 'CCC+' on improved liquidity and better than expected performance. On the other hand, Invictus Media S.L.U. (subsidiary of Joye Media S.L.) missed its interest payment and has therefore been rated 'D' since late July. Other obligors, like Vue International Bidco PLC (cinema operator), Transportes Aéreos Portugueses, S.A. (airlines), and Vincent Bidco B.V. (Dutch caterer), are still waiting for a more robust recovery in demand for their services to shake off the additional debt and disrupted operations due to COVID-19.

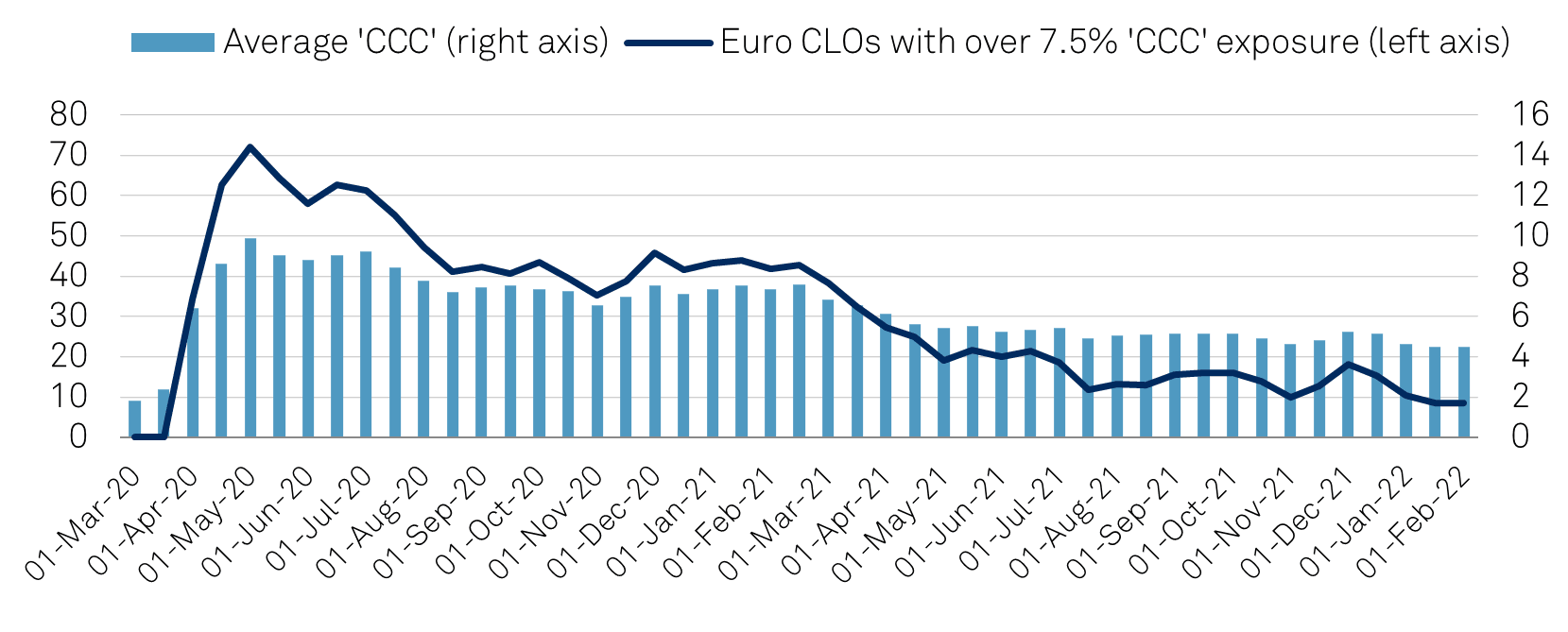

As we end the third quarter of 2021, European CLOs have continued to work through their ‘CCC’ exposures in 2021, with now just over 16% of CLOs comprising on aggregate more than 7.5% exposure in ‘CCC’ rated obligors. As we go past the third quarter of 2021, we now see ‘CCC’ exposure levels at their lowest since the end of the first quarter of 2020 (see chart 2).

Chart 2 | Proportion Of European CLOs With Greater Than 7.5% 'CCC' Exposure And Average 'CCC' Exposure (%)

Source: S&P Global Ratings.

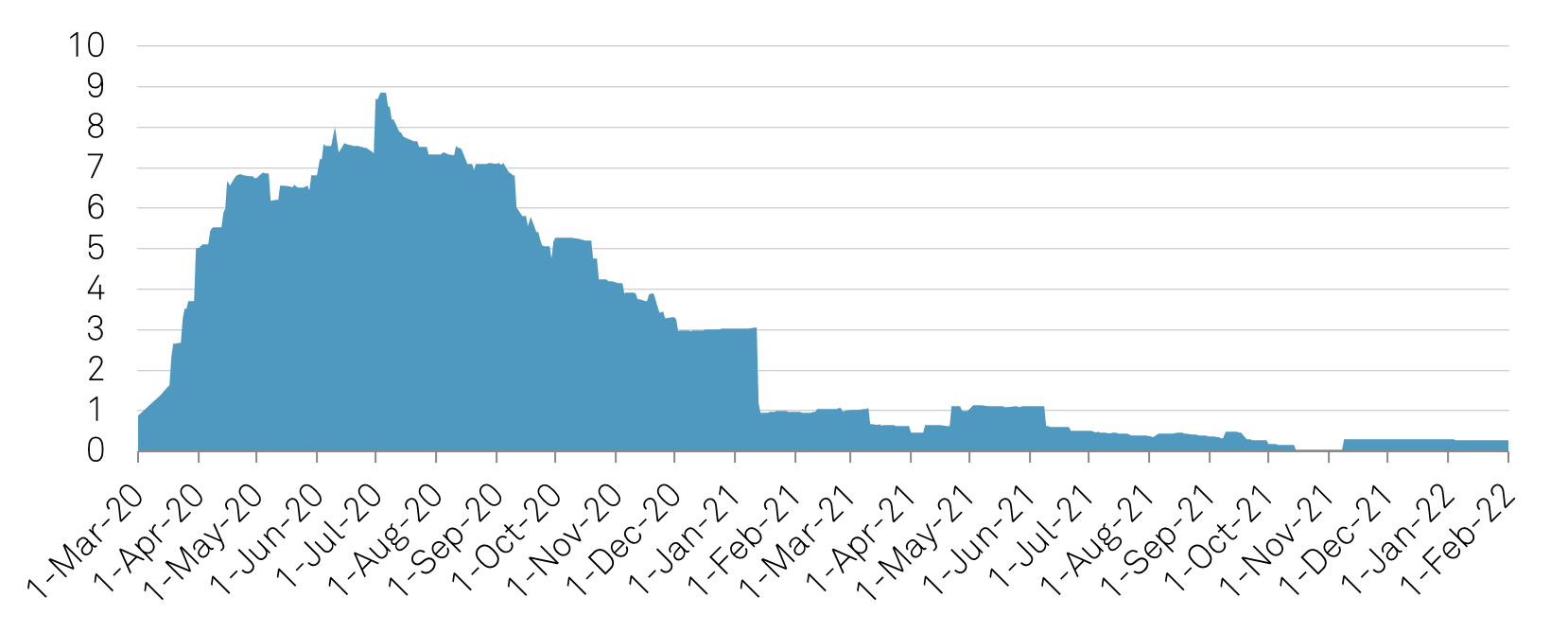

This goes hand-in-hand with CLO portfolio exposure to obligors on CreditWatch negative. For the first time since the start of the pandemic, average European CLO exposure to obligors on CreditWatch negative is below 1%.

Chart 3 | Average CreditWatch Negative Proportion In Euro CLOs (%)

Before diving deeper into the results, it is worth highlighting the following caveats:

We calculated the average metrics for all floating-rate assets with both an S&P Global Ratings' credit rating and an S&P Global Ratings' recovery rating (the S&P Global Ratings-rated CLO assets), weighted by the euro notional exposure to each asset.

Our analysis of reinvesting euro CLO portfolio at the end of each quarter exposure include average values over time for key credit metrics (see table 1, as well as the Appendix for calculation specifics). Those metrics are:

Table 1 | Floating-Rate European CLO Assets With Derived S&P Global Ratings' Credit Rating And Recovery Rating*

*See the appendix for detailed explanations of these metrics. SPWARF--S&P weighted average rating factor. WARR--Weighted average recovery ratio. WAS--Weighted average spread. WAP--Weighted average price.

Our analysis focuses on a pool of loans issued by 687 corporate issuers, representing over 95% of the AUM currently held in reinvesting European CLOs that we rate. For each sector, we calculated the average metrics for all of the assets that we rate, weighted by the euro notional exposure to each asset. These metrics include the SPWARF, WARR, WAS, and WAP (see table 1 and the Appendix).

The corporate issuers operating within various industries have different credit profiles, and the loans they issue also have different characteristics. Using CLO exposures for these CLO assets, we calculated the average metrics described in the Appendix, weighted by par, across the various Global Industry Classification Standard (GICS) sectors.

Table 2 | Floating-Rate European CLO Assets With Derived S&P Global Ratings' Credit And Recovery Ratings

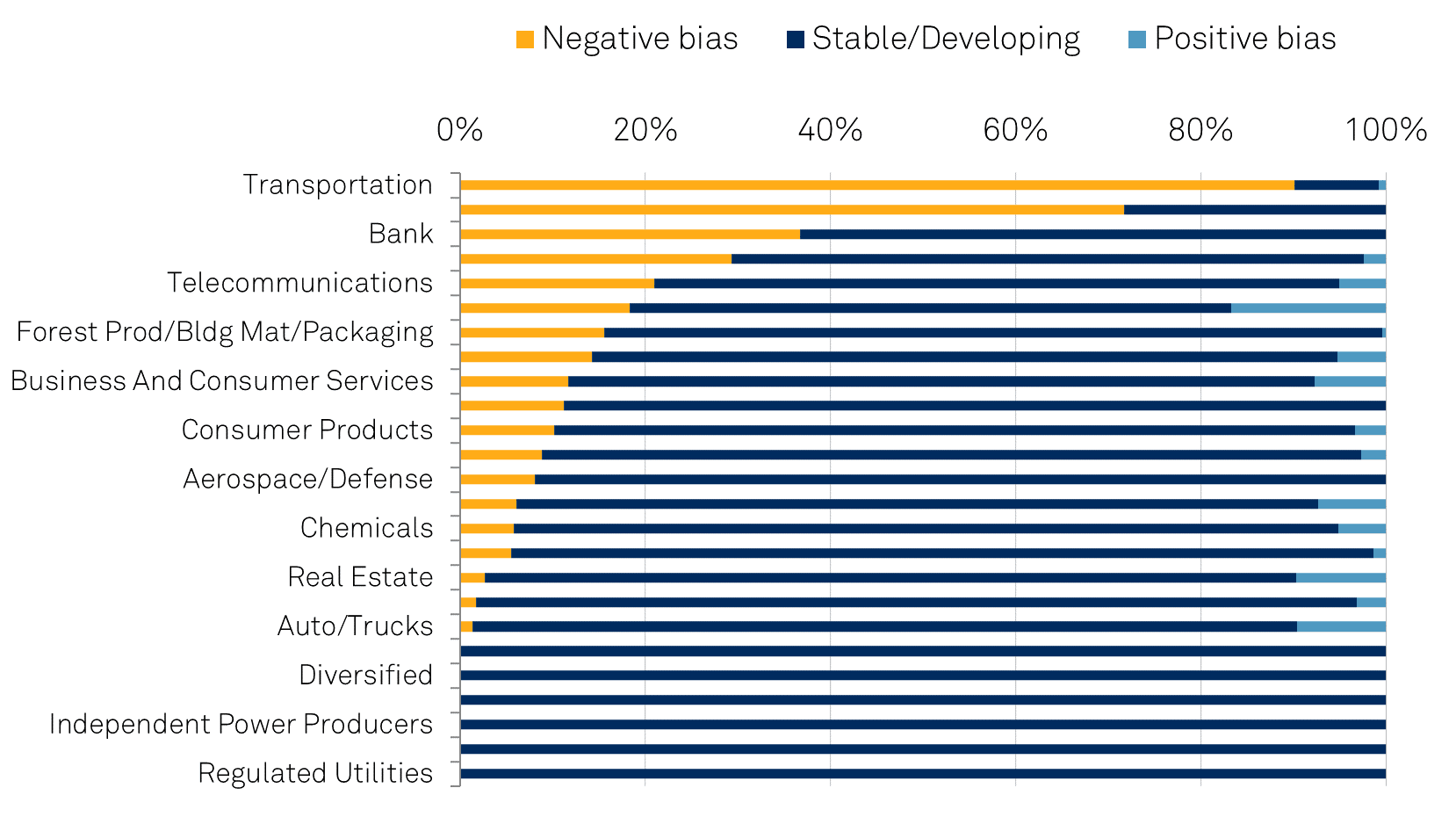

At the end of the third quarter of 2021, 14.81% of S&P Global Ratings-rated CLO assets had a negative rating bias (i.e., ratings from issuers with a negative outlook, or on CreditWatch negative), up from the 21.7% at the start of 2020 and down from 19.65% at the start of the third quarter of 2021. We also examined the breakdown between negative bias, positive bias, and stable for 24 GICS sectors, each weighted by euro notional exposure (see chart 4). The bias breakdown per GICS sector can be sensitive to the rating bias of the issuers with higher CLO exposure, particularly the GICS sectors with fewer obligors.

Chart 4 | Rating Bias Of GICS Sectors Weighted By CLO Exposure

CLO--Collateral loan obligations. GICS--Global Industry Classification Standard. Negative bias--Negative rating outlook or on CreditWatch negative. Stable/Developing bias --Stable and Developing rating outlook along with ratings with no CreditWatch or outlook. Positive bias--Positive rating outlook or on CreditWatch positive. Source: S&P Global Ratings.

In response to investors' growing interest following the COVID-19 pandemic and ongoing credit effects on companies and European CLOs, S&P Global Ratings is publishing a regularly updated list of rating actions we have taken globally on nonfinancial corporations that have had an effect on European CLOs, and a summary of how European CLOs have been affected with key benchmarks.

The report, titled "Weekly European CLO Update," covers all currently S&P Global Ratings' rated European CLOs, including those which are in their reinvestment period. The rating actions and benchmarks will be refreshed weekly to provide an update of the European CLO market.

To compare European CLO data each week, S&P Global Ratings provides you with an EMEA CLO Collateral Managers Dashboard. This dashboard is a single snapshot view of CLO-critical credit risk factors where you can examine, compare, and benchmark individual S&P Global Ratings' rated European CLOs.

https://www.spglobal.com/ratings/en/research-insights/topics/powerbinew

The information is based on the aggregation of CLO exposures to corporate issuers as reported in the third-quarter of 2021 trustee reports of reinvesting European CLOs.

S&P Global Ratings' corporate group issues and maintains credit ratings for the vast majority of companies that issue the loans held in CLOs. As part of our credit rating process, we capture various ratios of the issuer at the time of the rating. We also issue and maintain recovery ratings for most loans held in CLOs.

Almost all of the companies that issue loans held in European CLOs are classified within the GICS. These industry classifications are utilized within the CDO Evaluator credit model, which S&P Global Ratings' structured finance group uses in its rating process for CLOs.

We aggregate CLO exposures reported in trustee reports available as of the end of the third quarter of 2021 and calculate various metrics, weighted by the outstanding par amount of exposures and stratified by the GICS classification of the issuer of the loans. Our analysis focuses on those assets with an S&P Global Ratings' credit rating and an S&P Global Ratings' recovery rating. These S&P Global Ratings-rated CLO assets were issued by 687 corporate issuers operating across various GICS industries and represent over 95% of the total par of the CLOs aggregated in this third-quarter 2021 update. The credit rating, recovery rating, spread, price, and leverage ratio values of these floating S&P Global Ratings-rated CLO assets were used to calculate the averages outlined in tables 1 and 2.

The six metrics we use in our analysis are listed below.

The SPWARF of a CLO portfolio provides an indication of the overall credit rating distribution of the portfolio, weighted by each asset's par balance. The rating factor for each of the portfolio assets is determined by S&P Global Ratings’ credit rating (or implied rating) and the rating factor. (An individual asset's S&P Global Ratings rating factor is the five-year default rate, given the asset's S&P Global Ratings credit rating and the default table in the corporate CDO criteria, multiplied by 10,000.) The SPWARF is calculated by multiplying the par balance of each collateral obligation by the S&P Global Ratings rating factor (including exposures to issuers with a non-performing rating: 'CC', 'SD' and 'D', each with a rating factor of 10,000), then summing the total for the portfolio and dividing this result by the aggregate principal balance of the collateral obligations included in the calculation.

For a subset of assets with an S&P Global Ratings recovery rating, the WARR is the sum product of each asset's recovery rate (the number within parenthesis to the right of the recovery rating) and the asset's par exposure as a percentage of the sum of the par of the subset of assets. For more details on S&P Global Ratings' recovery ratings, see "Recovery Rating Criteria For Speculative-Grade Corporate Issuers," published Dec. 7, 2016.

For a subset of floating-rate assets, the WAS is the sum product of each asset's nominal spread above the base rate and the asset's par exposure as a percentage of the sum of the par of the subset of assets.

For a subset of assets with loan prices, the WAP is the sum product of each asset's price at the end of the quarter and the asset's par exposure as a percentage of the sum of the par of the subset of assets, where we have no loan price we assumed par at 100.

For those assets with a CreditWatch negative rating, the CreditWatch negative percentage is a proportion of the total CLO par amount considered in this analysis. This is also broken down per GICS sector (see table 4) as a total sum of the par of CLO GICS sector assets.

For those assets with a negative outlook, the outlook percentage is a proportion of the total CLO par amount considered in this analysis. This is also broken down per GICS sector (see table 4) as a total sum of the par of CLO GICS sector assets.

The leverage is based on the assumptions we make around debt and EBITDA, as used in our rating analysis:

Beyond that definition, our decision to include or exclude an activity from EBITDA depends on whether we consider that activity to be operating (e.g., acquisition-related or restructuring costs) or nonoperating (e.g., asset impairment or non-recurring items).

We generally calculate a company's credit ratios based on a three-year weighted average: the previous one year's results, our current-year forecast (incorporating any reported year-to-date results and our estimates for the remainder of the fiscal year), and our forecast for the next fiscal year. We apply weights to the core and supplemental ratios for the respective years to get to one final ratio for each metric. The length of the time series applied is dependent on the relative credit risk of the company and other qualitative factors, and the weighting of the time series varies according to transformational events.

For a subset of floating-rate assets, the debt-to-EBITDA ratio is the sum product of each asset's obligor nominal debt-to-EBITDA ratio and the asset's par exposure as a percentage of the sum of the par of the subset of assets.

For entities with weaker leverage assessments, interest coverage ratios can also shed light into the issuer's ability to service its debt.

We use the EBITDA value, as described above, divided by the carrying cost, or interest burden of the issuer's debt.

For a subset of floating-rate assets, the EBITDA interest coverage ratio is the sum product of each asset's obligor nominal EBITDA interest coverage and the asset's par exposure as a percentage of the sum of the par of the subset of assets.

Because we focus only on S&P Global Ratings-rated CLO assets (which represent over 95% of the overall AUM in the sample), by definition, we have full coverage of the data used to calculate the SPWARF, WARR, and WAS in tables 1 and 2. We have credit ratings, recovery ratings, and spread information for all loans issued by the 687 issuers as of Sept. 30, 2021, and each end of quarter in table 1.

Due to limitations within the various data sources, we did not have complete coverage regarding the price and leverage ratios for all the loans issued from all issuers. We were able to source pricing information for 98% of the loans and corporate leverage ratio information for 87% of the loans.