Feb. 26, 2021

This report does not constitute a rating action.

Stephen A Anderberg New York +1-212-438-8991

Daniel Hu, FRM New York + 1-212-438-2206

Victoria Blaivas New York + 1-212-438-2147

Dmytro Saykovskyi New York + 1-212-438-1296

Jimmy N Kobylinski New York +1-212-438-6314 Brian O'Keefe New York +1-212-438-1513

There has been strong market interest in private credit and middle-market (MM) collateralized loan obligations (CLOs) in recent years, and discussion of the asset class has increased as CLO investors search for yield and look at the relatively strong performance of MM CLOs during the COVID-19 pandemic. According to Leveraged Commentary Data (LCD), in 2020, there were 27 MM CLOs issued, despite a first half with light CLO issuance due to the pandemic-driven uncertainty about the direction of the credit markets (see table 1).

Table 1 | U.S. CLO New Issuance

MM--Middle market. BSL--Broadly syndicated loan.

The arrival of COVID-19 and the resulting pandemic-related shutdowns presented significant challenges to many of the companies whose loans were held in U.S. CLO transactions. With some companies in consumer-facing sectors facing the prospect of a second quarter with severely impacted business and earnings, negative actions on corporate ratings came swiftly amongst rated broadly syndicated loan (BSL) issuers in the second quarter of 2020. Many of the same pressures faced the credit-estimated companies within S&P Global Ratings-rated MM CLO transactions as well (see "Credit Estimates For Entities Backing U.S. Middle-Market CLOs Took A Hit From COVID-19," published Dec. 1, 2020), and it wasn't long before the effects of lowered credit estimates were felt within MM CLO portfolios. However, when our CLO reviews were complete, MM CLOs had experienced only a fraction of the downgrades seen on BSL CLOs: about 1.3% of MM CLO ratings were lowered compared with 12.4% of BSL CLO ratings (see "How COVID-19 Affected U.S. Middle-Market And BSL CLO Performance In 2020," published Feb. 4, 2021).

MM and BSL CLOs differ in some significant ways. MM CLOs are a segment of the U.S. CLO market backed by senior secured loans to smaller companies, typically those with EBITDA of $100 million or lower (and often much lower); they represent around 14% of total outstanding U.S. CLOs by both transaction count and volume. Unlike BSL CLOs, where we rate more than 95% of the companies issuing the loans held within the CLO collateral pools, most MM CLOs contain a significant proportion of loans from smaller companies that aren't rated. We typically use credit estimates to assess these unrated companies for the purpose of our MM CLO analysis (see "Anatomy of a Credit Estimate: What It Means and How We Do It," published Jan. 14, 2021).

The proportion of loans from credit-estimated versus rated companies varies significantly from one MM CLO to another (see table 2 below), but all of them have a much higher proportion than comparable BSL CLOs.

Table 2 | Proportion Of Credit Estimates At The Start Of 2021

Because companies in the MM CLOs are smaller than those in BSL CLOs, and because credit estimates are a point-in-time credit view based on an abbreviated analysis, MM CLOs have far more exposure to loans from 'B-' and 'CCC' rated companies than BSL CLOs.

As of January 2021, the average U.S. BSL CLO exposure to loans from companies rated 'B-' and 'CCC' was about 25% and 8% of total assets, respectively; the proportion for MM CLOs was about 66% and 23% of total assets. In addition to having a lower-quality credit profile, most MM CLO portfolios tend to have lower diversity, shorter average tenor of the loan collateral, and higher spread relative to BSL CLO portfolios.

However, while there is less diversification within MM CLO collateral pools, there is greater diversification across CLOs issued by different managers, as MM CLO loans are often unique to a single collateral manager and BSL CLO portfolios have some level of overlap between managers.

As a result of the lower credit profiles of their portfolios, and because they tend to be more concentrated, MM CLOs also tend to have considerably more par subordination for their senior tranches than BSL CLO transactions. Additionally, unlike most BSL CLO transactions, which are originated with a 'BB' (and sometimes 'B') rated tranche in the structure at origination, many MM CLO transactions are originated with only investment-grade-rated ('AAA' through 'BBB') tranches. Often, the junior-most tranche in the CLO capital structure is rated 'BBB' (and in a few cases 'A') with a correspondingly larger unrated CLO equity class beneath it. In our 65 CLO sample we used for the rating stress scenarios in this article, fewer than half had a 'BB' or lower-rated tranche within the capital structure at time of issuance (see table 3 below).

Table 3 | Subordination Per Rating Category At Start Of 2021

As a result of strong interest in the asset class, and from conversations we've had with MM CLO investors in the U.S. and Japan, we decided to generate and publish stress scenarios for MM CLOs that are analogous to the rating stress scenarios we published in April 2020 for our BSL CLO transactions (see "How Credit Distress Due to COVID-19 Could Affect U.S. CLO Ratings," published April 24, 2020). The MM CLO rating stress scenarios we produced are similar to the ones in April 2020 article, although the specific stresses we applied are different given the differences between the two sets of CLOs.

Despite the differences in the portfolios, MM and BSL CLO exposures to non-performing issuers were similar in 2020, both peaking at about 1.6% on average in mid-2020. However, MM CLOs on average did not experience par loss in 2020, while BSL CLOs, on average lost about 1% in par as BSL CLO managers tried to de-risk portfolios by selling loans at discounts to par. MM CLOs are entering 2021 with a relatively weaker credit profile; with higher portfolio concentrations (lower diversity) and higher 'CCC' buckets relative to BSL CLOs. With that in mind, we turn our attention toward the possibility of heightened levels of default across MM issuers. What would happen to a MM CLO rating under different default levels?

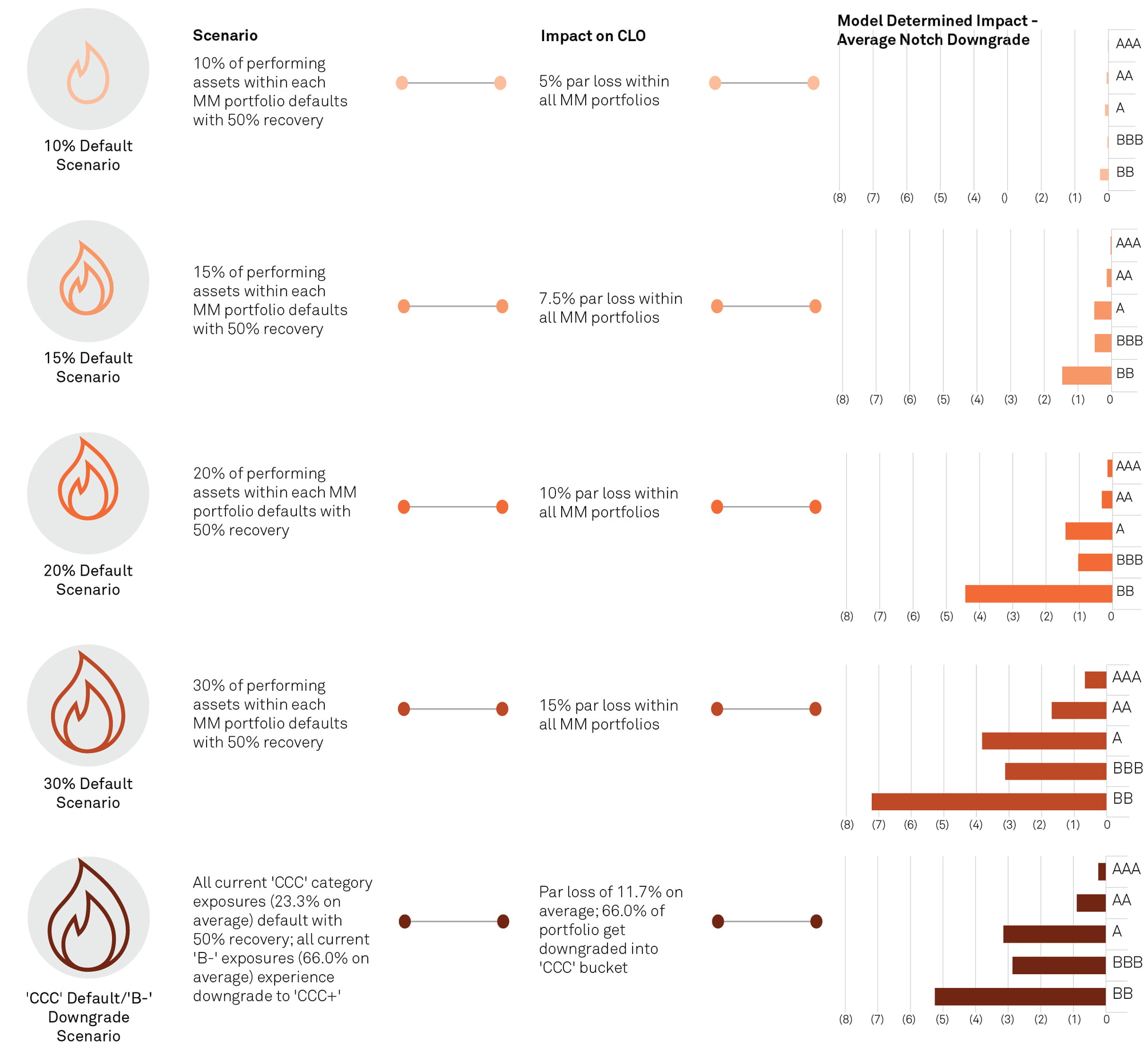

The default rate across MM CLO portfolios in a significant downturn would potentially be correlated by the manager, in our view, as a majority of loans within MM CLO portfolios are specific to a single manager. For our stress runs, to maintain consistency across the sample for our first four scenarios, we assumed each portfolio experiences the same default level, which are applied with increasing levels of asset default stress to see how the CLO ratings would respond. In the fifth and final scenario, the stress is dependent on the current credit profile of the companies within each portfolio. For all runs, we excluded CLO combo notes and X notes from the analysis.

Our sample included 65 MM CLOs that are scheduled to reinvest for all of 2021. There was a wide range of structures as well as portfolios, with some of the portfolios being something of a hybrid of both MM and BSL assets (see chart). Our specific stress assumptions were:

Sharp-eyed readers will note some differences between these stresses and the ones we used for our April 2020 BSL CLO rating stress article. The default rate assumptions here are more punitive (10%, 15%, 20%, and 30% of CLO assets defaulted for this exercise, versus 5%, 10%, 15%, and 20% for the BSL CLO rating stress article) due to the differences in rating/credit estimate profiles for MM and BSL CLO transactions. Note that the 30% collateral default scenario for this article, like the 20% default scenario in the BSL CLO rating stress article, was well outside the range of default forecasts even at the depth of the 2020 pandemic-driven downturn, but we include it as an interesting hypothetical.

Another difference is that for the first four scenarios in this article, unlike the April 2020 article, we did not assume any rating transition on the non-defaulting loans in the CLO collateral pools because, for most MM CLOs, so much of the collateral is already rated (or credit-estimated) at 'B-' or lower. Finally, for purposes of this exercise, we assume a 50% recovery rate for the loans we're defaulting, versus a 45% assumption for the April 2020 BSL CLO rating stress article.

This may at seem counterintuitive at first—one might expect lower recovery prospects from loans to smaller companies - however it makes sense when we consider the fact that loans in MM CLOs are generally not covenant lite, and they tend to have notably more constrictive loan documents than loans held in BSL CLOs.

None of the above scenarios are meant to be predictive of any specific outcome for the collateral within CLO transactions, or for the most stressful scenarios even be particularly plausible. But we think the hypothetical scenarios provide insight into how MM CLO ratings might respond to varying stress levels. By setting up the first four scenarios in the way we have, with a simple progression of increasingly severe assumptions, we hope to allow CLO investors and others to make their own view amongst the four scenarios and gauge the potential CLO rating outcome. The "Additional Scenario" stresses were added to address questions we've gotten from market participants, and to test a simple benchmark level of stress and provide comparisons to future scenario analysis.

CLO--Collateralized loan obligation. MM--middle market. Source: S&P Global Ratings.

Chart 1 | Summary Of Scenarios And Ratings Impact

For purposes of our scenario testing, we generated a quantitative analysis for our sample CLOs using the same tools we use when rating the transactions. Our CDO Evaluator credit model assesses the overall credit quality of a portfolio of assets based on the rating and maturity of each asset, as well as the correlation between assets, and produces expected default rates at stresses we associate with our various rating levels. Our S&P Cash Flow Evaluator model, on the other hand, is used to assess the ability of the tranches in a given CLO to withstand loss rates under various interest rate and default timing scenarios (see "S&P Global Ratings' CLO Primer," published Sept. 21, 2018). While ratings are assigned by committee and our criteria encompass a variety of qualitative and quantitative components, looking at the output of these two models for a given CLO portfolio and structure should provide an indication of the ratings a surveillance committee might assign following a given stress scenario.

Also, a few caveats worth highlighting:

Additionally, as noted above, many MM CLOs do not include a 'BB' rated tranche. In our 65 CLO sample we used for the rating stress scenarios in this article, only 26 had one or more tranches rated within the 'BB' category by S&P Global Ratings. We report results for 'BB' tranches in our stress analysis below, but note that the sample size for the 'BB' rating category is substantially smaller than for the more senior (investment-grade) rating categories.

In this scenario, we assume all of the MM CLO portfolios within our sample experience a 10% default rate, resulting in a 5% par loss.

As of the start of 2021, MM CLOs across this sample had average junior O/C of about 120.9%, where the average junior O/C trigger was 115.6% (average junior O/C cushion of over 5%). If 10% of all the portfolios within our sample defaulted with 50% recovery (resulting in 5% par loss for all deals), over half of the deals within our sample would experience an O/C test failure (assuming no additional O/C haircuts).

Within the table below, we see a large majority of all the MM CLO notes show rating stability under this stress. Over 90% of the investment-grade-rated notes continue to pass our quantitative results at their current rating levels, while just over 80% of the 'BB' rated notes pass at their current rating levels.

Table 4 | Stress 1: Cash Flow Results Under 10% Default Scenario

Source: S&P Global Ratings.

In this scenario, we assume all of the MM CLO portfolios within our sample experience a 15% default rate, resulting in a 7.5% par loss.

Under this stress, just about all the MM CLOs will wind up failing one or more of their O/C tests.

A majority of the MM CLO 'BB' tranche ratings experience downgrades under this stress, and more than 10% of these would see multi-notch downgrades into either the 'CCC' or non-performing categories. About half of the 'BBB' tranches see downgrades (43% of the 'BBB' tranches dip into speculative grade under this scenario). A majority of investment-grade-rated notes continue to pass our quantitative results at their current rating levels; over 90% of the 'AAA' and 'AA' notes continue to pass; and just under two thirds of 'A' tranches continue to pass.

Table 5 | Stress 2: Cash Flow Results Under 15% Default Scenario

In this scenario, we assume all the MM CLO portfolios within our sample experience a 20% default rate, resulting in a 10% par loss. Just about all the CLOs will be failing one or more of the O/C tests.

All of 'BB' rated notes experience downgrades (some of the 'BB' notes are underwater as average subordination of 'BB' notes was 12.54%). As a result, 21% of 'BB' notes see quantitative results that point to a non-performing rating, while 43% see downgrades into the 'CCC' category. 87% of the 'BBB' notes lose their investment-grade status, though none see downgrades into the CCC or non-performing categories. Even under this stress, a majority of the 'AAA' and 'AA' rated MM CLO tranches continue to pass at their current rating level.

Table 6 | Stress 3: Cash Flow Results Under 20% Default Scenario

In this scenario, we assume all of the MM CLO portfolios within our sample experience a 30% default rate, resulting in a 15% par loss.

All of the 'BB' notes experience downgrades to non-performing. All of the 'BBB' notes experience downgrades into speculative grade, though most continue to maintain a performing rating as almost all remain above water (average subordination of 'BBB' notes was 19.09%).

Almost all of the 'A' notes see downgrades; over one third are lowered into a speculative-grade rating. A majority of 'AAA' and 'AA' notes now experience downgrades as well, though none lose their investment-grade rating.

Table 7 | Stress 4: Cash Flow Results Under 30% Default Scenario

In this scenario, we assume that all 'C'CC' category rated issuers default and recover 50%, while all 'B-' rated issuers get downgraded to 'CCC+'.

This scenario is different from Stress One through Four above in that this stress is based on the current credit profile of each portfolio, and will produce an asset default rate (and downgrade to 'CCC' rate) that is specific to each CLO portfolio. Across the sample, the average exposure to 'CCC' category rated assets was 23.34%, while exposure to 'B-' rated assets was 66%. On average, the par loss of this scenario is slightly higher than that of the 20% default scenario in Stress Three above, with the added stress of credit downgrades to 'B-' rated issuers.

All of the 'BB' notes experience downgrades; just over half see their ratings lowered to non-performing. Just about all of the 'BBB' notes experience downgrades into speculative grade, while some are lowered into the 'CCC' and non-performing categories. Most of the 'A' notes see downgrades; about one third see downgrades into speculative grade. Most of the 'AAA' and 'AA' notes continue to pass at their current rating.

Table 8 | Stress 5: Cash Flow Results Under 'CCC' Category Default And 'B-' Downgrade Scenario

Most MM CLOs showed strong performance during the 2020 downturn, with no par loss on average during the year and a lower downgrade rate of the CLO tranche ratings compared to the ratings on their BSL CLO siblings. In addition to the lack of par loss, we think the strong 2020 performance is also due to MM CLO structures typically having lower leverage than BSL CLO structures, with a larger equity classes and higher par subordination for the rated tranches.

As with the BSL CLO rating stress analysis we published in April 2020, our MM here analysis outlined in this article shows the fundamentals of the MM CLO structure protecting senior noteholders, with more than 97% of CLO 'AAA' tranche ratings either experiencing an affirmation or one-notch downgrade to 'AA+' even under our most punitive scenario where 30% of the obligors are immediately defaulted.

Outcomes for tranches further down the CLO capital stack depend upon the severity of the assumptions applied, but no tranche rated 'A' or higher defaulted under any of our scenarios. We note that the 'AAA' CLO tranche downgrade rate in the real world would likely be lower than indicated in the stress test transition tables above. This is because rating committees sometimes take into account qualitative considerations, our expectations for future senior tranche pay downs, and other factors beyond the results of the quantitative analysis done for this article.