Feb. 09, 2022

This report does not constitute a rating action

Ramki Muthukrishnan New York +1-212-438-1384

Daniel Hu, FRM New York + 1-212-438-2206

Patrick Drury Byrne Dublin 0035-31-568-0605

Evangelos Savaides New York + 1 212-438-2251

Evan M Gunter Montgomery + 1-212-438-6412

Joe M Maguire New York + 1-212-438-7507

While direct lending continues to provide positives such as better yield, speed of execution, and is relationship-driven, the resilience of this market hasn't been truly tested in a deep, protracted credit crisis.

Improved earnings and better balance sheets in 2021 made many middle-market companies' candidates for upgrades. Just as was the case with the rating actions in the U.S. speculative-grade universe, there were more upgrades than downgrades of credit estimates in middle markets in 2021.

A slowdown in economic growth coupled with inflation pressures and rising interest rates--and the consequent pressure on margins--could weigh heavily on some weaker companies with low coverage ratios.

The U.S. market for private debt has enjoyed a boom in recent years and it seems clear why: It is relationship-based lending, the deal execution is relatively swift, there is better documentation, and periods of distress can be relatively painless and quick to work through--as we saw during the pandemic. Still, it remains difficult to assess just how much long-term risk exists and how vulnerable the borrowers would be in the event of a credit crisis. A slowdown in economic growth coupled with inflation pressures and rising interest rates--and the consequent pressure on margins--could weigh heavily on some weaker companies with low coverage ratios. In this report we look through the portfolio companies that middle market (MM) collateralized loan obligations (CLOs) lend to as a representative sample of borrowers in the larger private debt universe. We look at the credit profile and performance of these companies to take the temperature of the underlying private debt market.

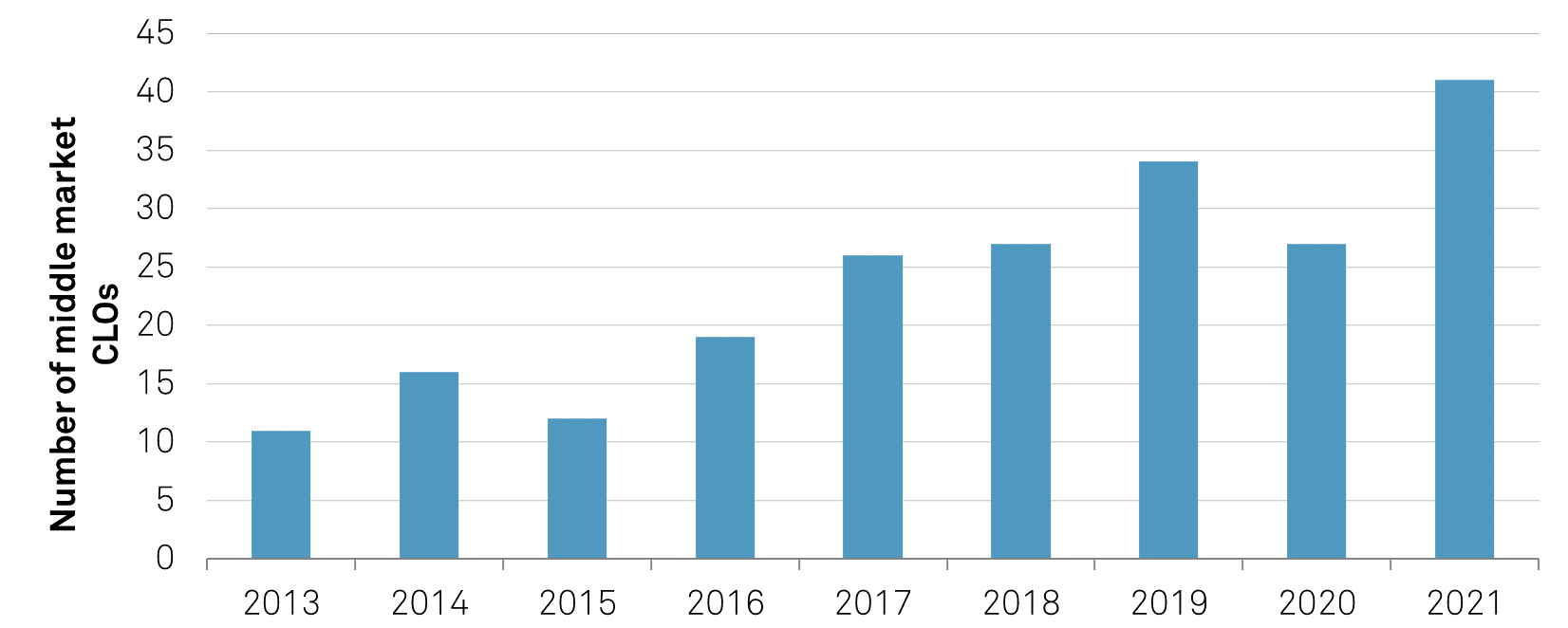

Chart 1 | Growth of Middle Market CLOs 2012-2021

Following the 2007-2008 Great Financial Crisis (GFC), the U.S. economy has enjoyed a long credit cycle, with benign credit conditions enabled by low inflation and rock-bottom interest rates--all leading to diminished levels of defaults. Capital flowed into private equity (PE) and private debt, including securitization markets, including CLOs. The lure of richer spreads and the track record of positive credit performance also contributed to increased interest in the broadly syndicated loan (BSL) and middle-market (MM) CLO markets.

Although CLOs as an asset class weathered the GFC, the pace and popularity of MM CLOs accelerated only in 2017. Based on Leveraged Commentary & Data (LCD) data, there have been about 155 MM CLOs since the start of 2017, compared to 69 in the five years before that.

Source: LCD.

After a pandemic-induced hiccup, 2021 was a landmark year for U.S. CLOs and leveraged loans, both of which saw a record issuance. Institutional leveraged loan volume surpassed $615 billion, with high-yield bond issuance at about $465 billion, based on data from LCD. Issuance in both asset classes bested previous records and pushed annual spec-grade bond and loans volume past $1 trillion. Meanwhile, U.S. CLOs recorded the highest issuance, about $187 billion. It was also a record year for MM CLOs, both in terms of issuance and number of deals priced; LCD data show 41 new transactions totaling about $22 billion for the year. And S&P Global Ratings reviewed more than 1,500 companies for the purpose of assigning credit estimates. (For unrated companies whose loans are in S&P Global Ratings-rated MM CLOs, we provide a credit estimate score as an indication of their credit quality; some companies were reviewed multiple times, given the timing of review during the year.)

MM CLOs are for the most part backed by smaller companies with narrower product or service lines that primarily serve local and regional markets. Given that the companies are private and unrated, there is less publicly known information available on them compared to that of the BSL market.

When the pandemic led to business closures, several smaller companies, especially those that were consumer-facing, faced liquidity issues and made efforts to preserve liquidity, such as reducing the payment of cash interest and swapping that portion for payment in kind (PIK), complete deferral of cash interest for some quarters, pushing back scheduled amortization payments to the final maturity date, and extending maturities. Lenders were often willing to waive covenants for one or multiple quarters.

MM companies generally have close relationships with their lenders--more so than in the BSL market. This made it easier during the pandemic to get the relevant parties to the negotiating table to work on executing amendments to loan agreements as a way to preserve liquidity and generally avert a conventional default. However, this resulted in some MM CLO managers getting less than promised of their original security without adequate and offsetting compensation, which we considered to be selective defaults, and lowered the credit estimate score to 'sd'.

The resurgence of credit markets that started in late-2020 has continued. On the business side, just like their larger counterparts, MM companies have benefited from pent-up consumer demand, high levels of savings, and better cost controls. On the financial side, easy credit conditions evidenced by high liquidity and favorable lending terms have paved the way for more refinancings, mergers and acquisitions (M&A), and leveraged dividends/leveraged buyouts (LBOs). Of the MM companies we reviewed in 2021, more than one-third saw M&A and LBOs and a good portion of the estimates were issued following those transactions. The uptick in these transactions was driven by factors including decline in cost of funding and the desire of companies to reposition their offerings in a post-pandemic world.

Based on Global Industry Classification Standard Sector (GICS) that we use for CLO sector categorization, sectors that saw high levels of consolidation included IT and software, and health care. For the latter, mergers were driven by companies' desire to expand their presence regionally, to expand the range of services offered and diversify the customer base and delivery mix. In the IT and software sectors, companies did takeovers to enhance product or service offerings, access new customers, or create opportunities to cross-sell, as well as to reposition their business models given the focus on digitization. The forms of financing that funded LBOs and M&A also returned capital to sponsors through leveraged dividends (although the number was relatively low compared to BSL markets).

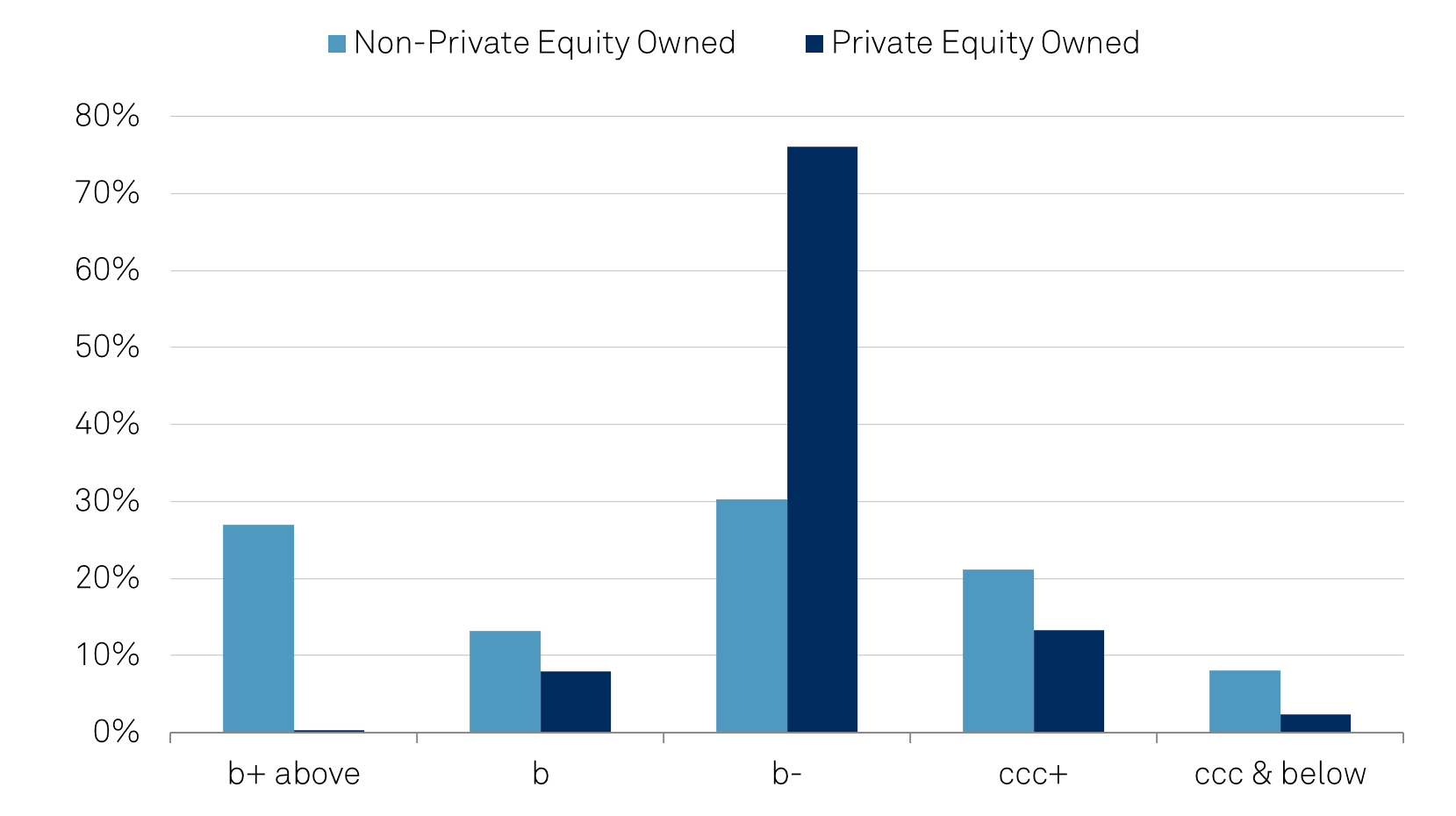

About 94% of the companies that we provided credit estimates on were owned by PE firms.

The ownership was somewhat dispersed across PE, with close to 350 PE firms owning these companies. More specifically, the top five PE firms accounted only for 7% of the entities reviewed.

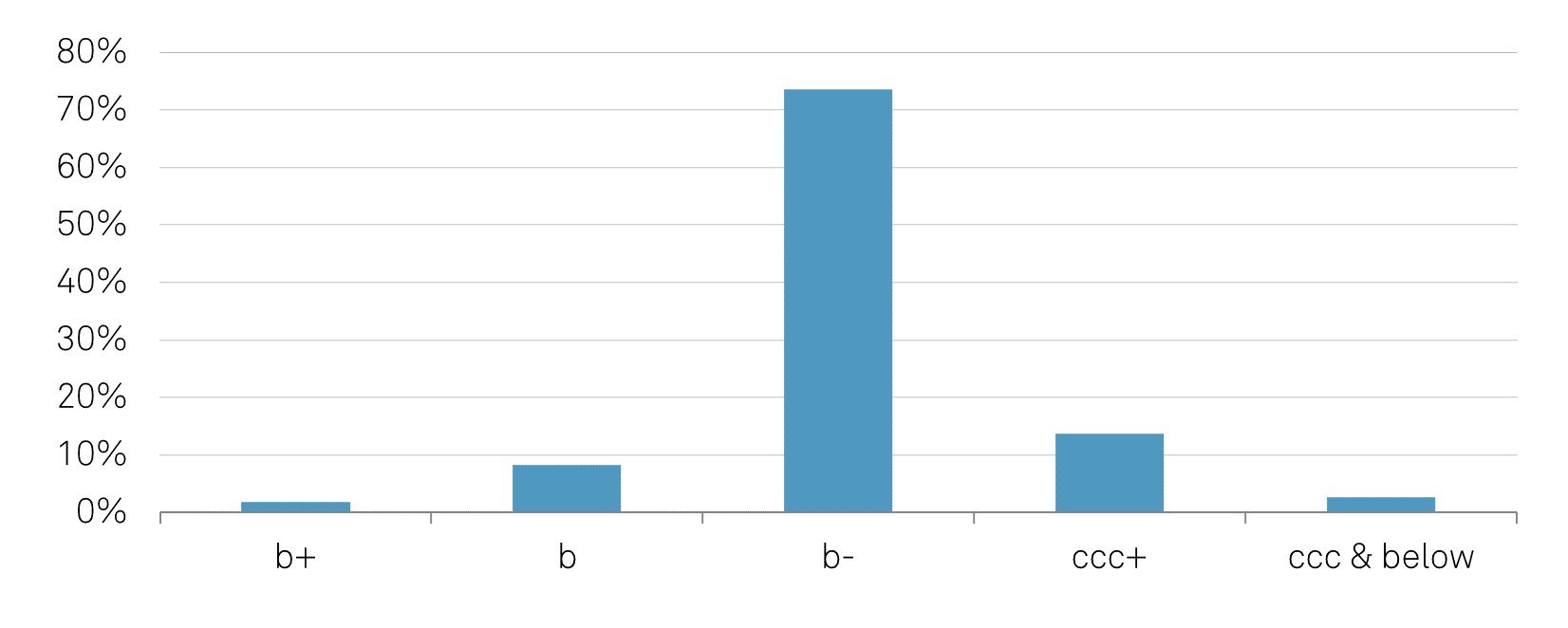

Almost three-fourths of the middle-market entities we reviewed last year got a credit estimate score of 'b-' (see chart 2). This isn't surprising given the high degree of PE ownership. In our methodology, we assume financial sponsors generally look to maximize returns by extracting cash from their portfolio companies by issuing debt. Accordingly, in our view, the financial risk profile for PE owned companies is commensurate with those of highly leveraged companies.

Chart 2 | Credit Estimate Scores

Source: S&P Global Ratings.

Chart 3 | Credit Estimate Rating Distribution

Most of the companies we reviewed have a weak or a vulnerable business risk profile given their small size. The median EBITDA for the MM companies reviewed based on our calculation was $24 million, and the median adjusted debt was about $175 million. The combination of highly leveraged financial risk and weak or vulnerable business risk resulted in credit estimate scores falling at the lower end of the credit spectrum. This was generally the case even before the pandemic; from 2017-2019, companies with a score of 'b-' constituted around 75% of all credit estimates we issued. In fact, 'b-' rated entities were the most represented cohort among middle market CLOs since 2014 and their share has only continued to grow since.

For 2021, the most represented subsector was health care providers, followed by software and commercial services--with the three sectors together accounting for 30% of the middle-market companies reviewed. Along with professional services and IT services (ranked fourth and fifth, respectively), these five sectors account for nearly 40% of the companies we reviewed. Among the top five, companies in the software sector had the highest leverage, with an S&P Global Ratings-calculated median leverage of 8.94; commercial services followed, at 8.15 turns. Four of the five sectors had an S&P Global Ratings-calculated leverage of 7 turns or higher, with IT services also coming close, at 6.9 turns.

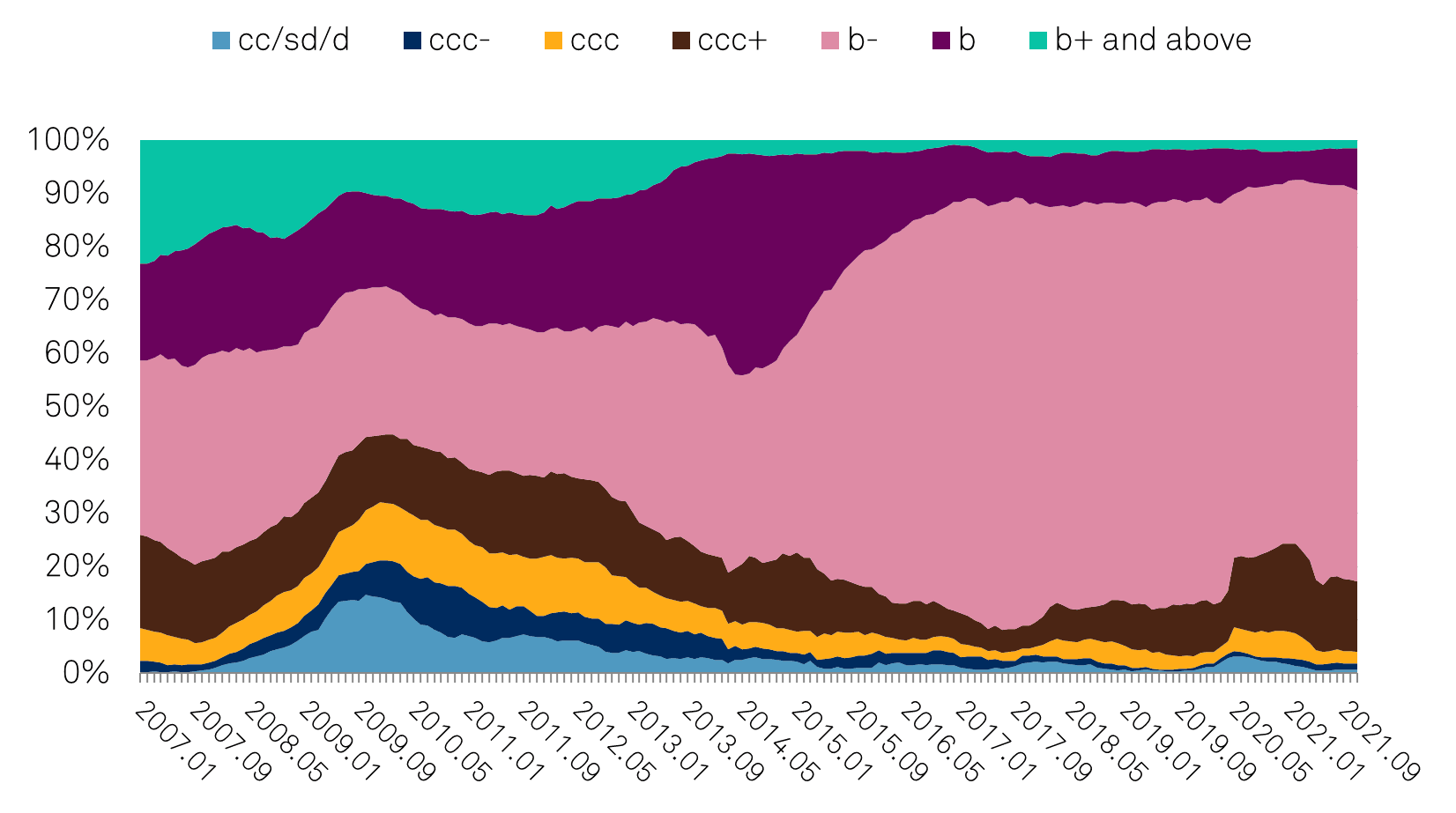

Chart 4 | Credit Estimate Scores Over Time

(S&P-calculated leverage contemplates EBITDA on what we consider to be truly operating in nature. Accordingly, expenses such as acquisition- and restructuring-related costs aren't added back in our analysis. In our view, restructuring and acquisition costs are part of companies' growth strategies and generally not added back in our EBITDA analysis. Our view of debt also includes sponsors' non-common equity unless certain conditions are met; for these reasons, our calculation of leverage is more conservative than what is reported by the companies.)

Just like the larger U.S. corporates landscape, middle-market companies in many sectors enjoyed improved performance arising from pent-up consumer demand, as well as optimism around business conditions. Improved earnings and better balance sheets in 2021 made many MM companies candidates for upgrades. Unsurprisingly, as was the case with the ratings actions in the BSL market, there were more upgrades than downgrades of credit estimate in middle markets. For the year, there were 142 upgrades compared to 108 downgrades.

A slew of factors drove upgrades, including growth in EBITDA, improved interest coverage, deleveraging, better operational performance, labor efficiencies and cost controls, and shifting or expanding product mix to address growing markets. The upgrades crossed all sectors, reflecting a general sense of overall improvement in market conditions with the rising business tide lifting a lot of boats.

Almost half of the upgrades were to a score of 'b-', bringing companies out of the 'ccc' range--and the ability of companies to refinance was a big contributing factor. The 'ccc' category companies in middle market CLOs were north of 22% at the start of 2021. They have since come down to about 16% at the end of 2021, on account of the upgrades.

Upgrades out of 'ccc' have consequences for CLOs because the 'ccc' holdings in a CLO over a certain threshold (as defined in their CLO indenture) are carried at a haircut for overcollateralization test purposes.

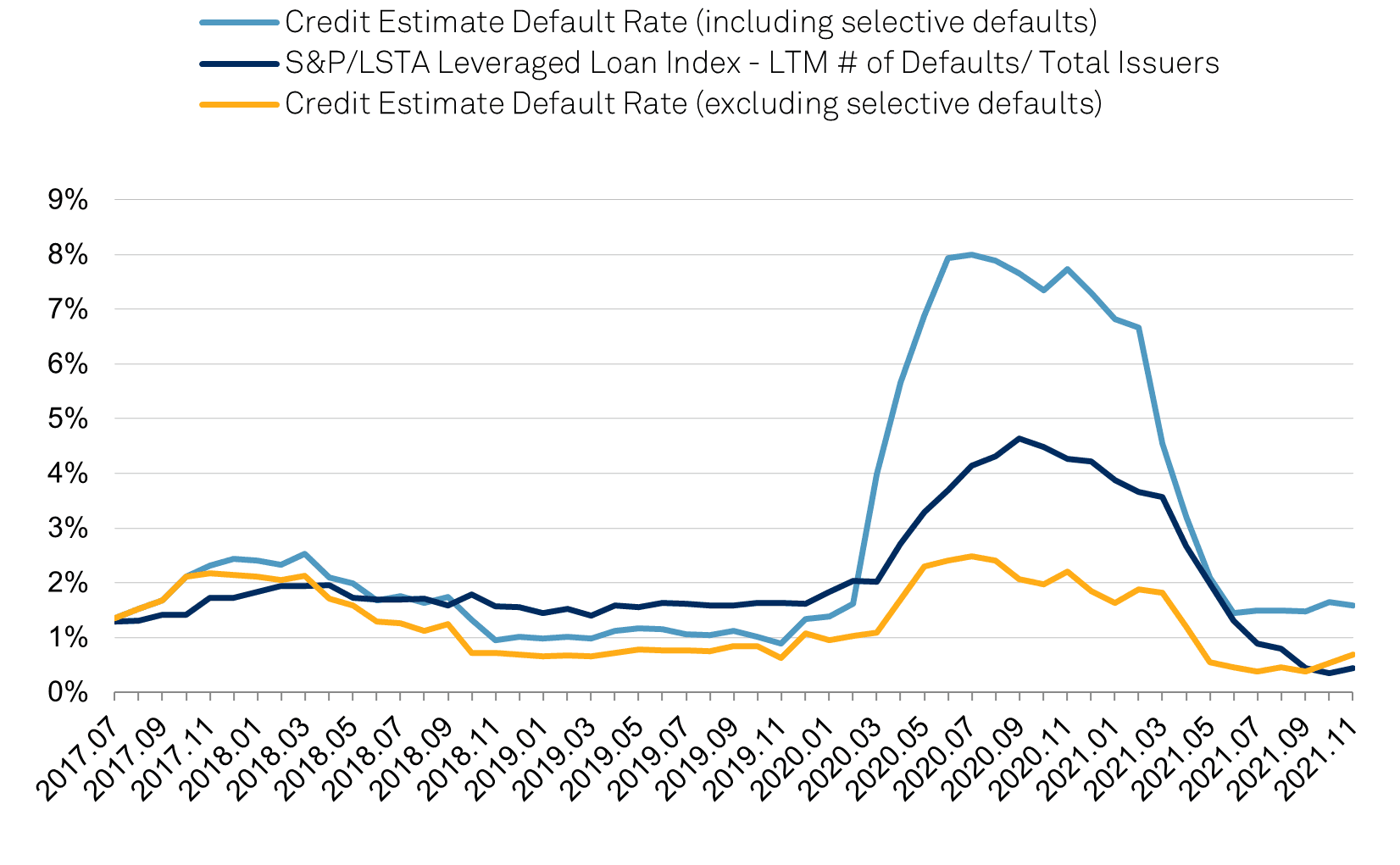

Chart 5 | One Year Lagging Default Rate: Credit Estimates vs. LCD Index

For middle-market entities, the overall default rate (credit estimates with a score of 'd', 'sd', or 'cc')--which had jumped to 8% when the pandemic hit--was around 6% through the first quarter of 2021. The jump in overall defaults was driven by the increase in the number of entities that were issued an 'sd' scores during the pandemic (for reasons cited earlier).

However, starting the second quarter of 2021, the number quickly came down as defaults in 2020 dropped out of the trailing 12-month figures. The middle market default rate is now trending under 2% as we continue to see the occasional selective defaults. Meanwhile, the leveraged loan default rates for the BSL market has trended even lower at under 0.5%

In the past several years, banks have moved to address the needs of larger borrowers, leaving a gap for direct lenders to meet the needs of the smaller and middle-market players. While direct lending continues to be a growing market that provides strong yields, relationship-driven lending (with better documentation and controls), speed of execution, and more efficient forms of workout, the resilience of this market hasn't been truly tested in a protracted credit crisis. Further, a lot depends on the asset managers, their underwriting and portfolio management, and restructuring capabilities. And finally, one of the risks in the overall private debt market is nobody is quite sure how big it is or who ultimately holds the risk given how the risk is distributed. Its growth in recent years suggests it has attracted new crossover investors in search of yield. Consequently, problems in the private markets could ripple through to the more transparent and much-larger syndicated market.