June 17, 2021

This report does not constitute a rating action

Stephen A Anderberg New York +1-212-438-8991

Daniel Hu, FRM New York + 1-212-438-2206

Jimmy N Kobylinski New York + 1 (212) 438 6314

Dmytro Saykovskyi New York + 1-212-438-1296

Victoria Blaivas New York + 1-212-438-2147

Despite significant downgrades to the ratings on U.S. broadly syndicated loan (BSL) issuers in 2020 due to the pandemic, CLOs backed by these loans showed relatively modest rating changes.

To test the resiliency of U.S. BSL CLO ratings for the next possible downturn, we performed an analysis to see how our CLO ratings might respond a series of hypothetical stresses with different levels of CLO asset defaults and downgrades.

Our analysis shows the fundamentals of the CLO structure protecting senior noteholders, as over 90% of the 'AAA' CLO notes are within a one-notch downgrade even in the harshest of the scenarios where defaults and 'CCC' buckets across CLOs reach 20% and 40%. None of the 'AAA' CLO ratings move below 'A+' under any of the scenarios.

The arrival of the COVID-19 pandemic and related economic shutdowns in early 2020 presented significant challenges to speculative-grade companies with loans in U.S. CLO transactions, and by the middle of 2020, nearly a third of all corporate ratings held within U.S. CLO collateral pools (by par) had experienced a downgrade. In the end, however, ratings on U.S. BSL CLO transactions saw comparatively few downgrades. By year-end 2020, 478 U.S. CLO ratings--about 11% of our total outstanding book at the time--had been lowered. More than 79% of these downgrades were taken on speculative-grade CLO ratings ('BB+' and below), and 64% of the downgrades were a one-notch downgrade. No 'AAA' CLO ratings were placed on CreditWatch negative or downgraded.

Since then, the CLO market has rebounded, with new investors entering the space and record-setting U.S. CLO issuance occurring in first-quarter 2021, due in part to the resilience shown by the asset class during the downturn.

While our U.S. BSL CLO ratings fared well during the pandemic, how resilient will they be during the next downturn? To test the resiliency of U.S. BSL CLO ratings for the next possible downturn, we performed another scenario stress analysis exercise similar to the one from our article, "How Credit Distress Due To COVID-19 Could Affect U.S. CLO Ratings," April 24, 2020, which we published relatively early in the pandemic. In the article, we applied a hypothetical series of stress scenarios to our U.S. BSL CLO transactions to show their rating impacts. Each scenario envisioned a proportion of corporate loans experiencing a payment default, combined with a proportion of the remaining (i.e., non-defaulted) loans experiencing their issuer ratings being lowered into the 'CCC' range. For purposes of this current exercise, we re-ran four of the stresses from the April 2020 article to see what the CLO rating impact could be, and how the results might have changed since the article was published. We also added a fifth scenario not included in the April 2020 article. The sample for our current rating stress scenario exercise includes a total of 530 CLOs, all currently inside their reinvestment period. Of these, 421 were originated before the pandemic and experienced the credit stresses of 2020 (and potentially saw one or more ratings lowered), while the other 109 were originated during and after the pandemic and generally have cleaner portfolios with lower exposure to loans from obligors rated in the 'CCC' range.

Before reviewing the results of the current round of stress scenarios, let's look back at the April 2020 exercise and see how the CLO rating outcomes envisioned in the article line up against the rating changes our CLOs actually experienced during 2020.

During the pandemic and related economic turndown in 2020, the S&P/LSTA Leveraged Loan Index default rate (which tracks the twelve-month trailing payment default rate on loans from speculative-grade obligors) peaked at 4.64% during third-quarter 2020 before ending the year at 4.22%. The 'CCC' exposure within our U.S. BSL CLO collateral pools (which, under our methodology, includes obligors rated 'B-' on CreditWatch negative) peaked in May 2020 at just over 12.3% of total assets before receding to 8.7% by end of 2020. The 4.64% loan default peak and 12.3% 'CCC' exposure peak our BSL CLOs saw in 2020 aren't too far off the "5/10" scenario (5% of loans default and 10% get lowered to 'CCC') we published in our April 2020 rating stress article, and the outcomes from this stress scenario line up pretty closely with the actual CLO rating actions we took in 2020, both in terms of the proportion of CLO ratings lowered and the severity of those downgrades (see table 1).

Table 1 | U.S. CLO Rating Actions in 2020: Actual Downgrades Vs. April 2020 "5/10" Scenario

Source: S&P Global Ratings.

For the purposes of our scenario testing, we generated a quantitative analysis for our sample CLOs using the same tools we use when rating the transactions. Our CDO Evaluator credit model assesses the overall credit quality of a portfolio of assets based on the rating and maturity of each asset, as well as the correlation between assets, and produces expected default rates at different rating levels. Our S&P Cash Flow Evaluator model is used to assess the ability of the tranches in each CLO to withstand loss rates under various interest rate and default timing scenarios. While ratings are assigned by committee and our criteria encompass a variety of qualitative and quantitative components, looking at the output of these two models for a given CLO portfolio and structure should provide an indication of the ratings a surveillance committee might assign following a given stress scenario.

The broad approach to the stress testing has two steps: First, apply the collateral stresses of defaulting and downgrading loans in each CLO portfolio to hit the default and 'CCC' obligor exposure outlined for the stress. The collateral default and downgrade stresses are applied to the CLO portfolios at time zero, so don't consider changes that might occur if they occurred over time (manager actions, coverage test paydowns, etc.) that might mitigate some of the rating impact of the stresses. Then, generate automated quantitative results (CDO Evaluator and Cash Flow Evaluator runs) across the entire sample of CLOs and seeing what ratings the quantitative analysis points to assigning.

Although this excludes qualitative discussions that might occur in the context of a surveillance committee, it gives a good idea for each CLO of what the CDO Evaluator/Cash Flow Evaluator results reviewed by the surveillance committee would look like under a given stress.

Also, it's worth highlighting a few caveats:

Finally, for each of the scenario results tables below, we include a column for the instances where our cash flow results point to a rating below 'CCC-'. In many of these instances, the CLO notes still have overcollateralization greater than 100%, and, in practice, the committee might not lower the ratings to a nonperforming rating, 'CC', based on this. In practice, the quantitative results are only part of the rationale behind assigning a 'CC' rating to a CLO note. In 2020, we only lowered three ratings to 'CC', where the notes were significantly undercollateralized and payment in full on the legal final date of the CLO note is highly unlikely.

To produce our updated rating stress scenarios, we chose a cohort of 530 U.S. BSL CLO transactions rated by S&P Global Ratings that were within their reinvestment periods as of mid-May 2021. We excluded CLO X notes and combo notes from the stress scenarios. Given the volume of resets within the last four years, there is a wide range of vintages across this sample, and some of the CLOs have gone through both the energy/commodities downturn of 2015-16 as well as the 2020 pandemic. A large majority of our sample (421 of the 530 CLOs) had closed before the pandemic arrived, while the remainder (109 CLOs) closed after the pandemic had arrived. Despite the positive credit trends as we head into mid-2021, there are clear differences between the two cohorts, with the CLOs originated after the arrival of the pandemic generally having cleaner portfolios than the pre-pandemic CLOs since they built portfolios with the clarity of hindsight to avoid certain pandemic-affected sectors and issuers.

Across our full sample of 530 reinvesting U.S. BSL CLOs, we see exposure to over 2,300 loans from more than 1,500 obligors. As of mid-May 2021, 243 of these obligors were rated within the 'CCC' category ('CCC+', 'CCC', and 'CCC-'), and 43 obligors had a nonperforming rating ('CC', 'SD', and 'D'). The average 'CCC' bucket across the full sample prior to applying the stresses was 6.3%, while the average exposure to nonperforming assets was 0.1%.

Similar to the process for our April 2020 scenario analysis, we notched the ratings amongst the 1,500+ obligors from the weakest on up (first sorted by rating, and then by loan price) to achieve the target 'CCC' and default exposures for each scenario, on average, across our sample of CLOs. Note that this can produce CLOs with a range of exposures in the stress analysis--for example, in the "5/10" scenario, some CLOs end up with more than 5% exposure to defaulting loans, and others less, but the average ends up at 5% across the entire cohort. Finally, we assume a 45% recovery rate (or par loss given default of 55%) for purposes of the stresses.

Table 2 | Creating The Scenarios

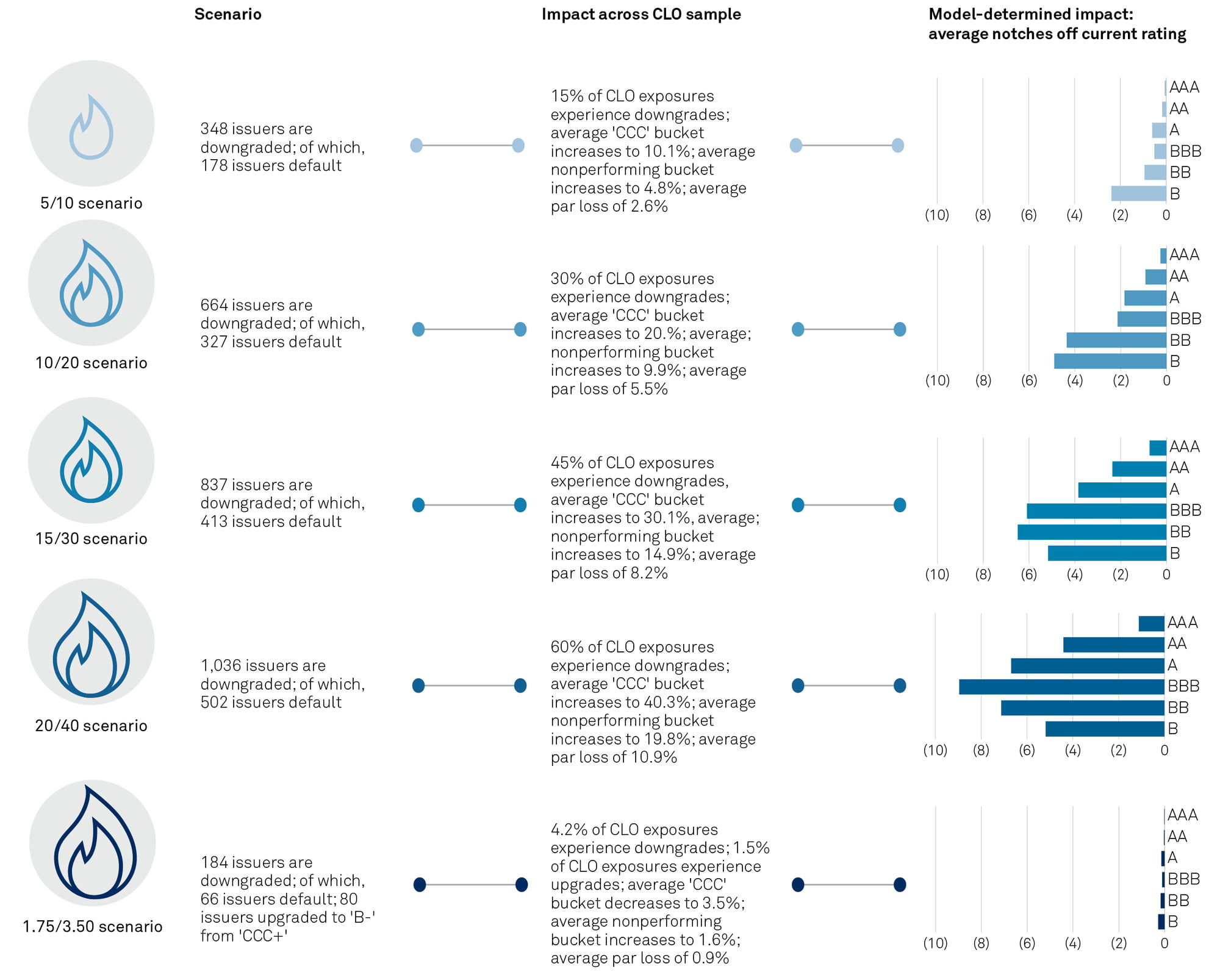

As mentioned above, for purposes of this current exercise, we re-ran four of the stresses from the April 2020 article to see what the CLO rating impact could be, and how the results might have changed since the article was published.

We also added a fifth scenario not included in the April 2020 article:

Chart 1 | Summary Of Scenarios And Ratings Impact

In this scenario, we assume that 178 of the weakest obligors (as determined by rating and loan price) experience a payment default, and that 170 issuers see their ratings lowered into the 'CCC' range.

As a result, the average CLO exposure to defaulted assets and assets from obligors with a rating in the 'CCC' range increases to about 5% and 10%, respectively, from 0.1% and 6.3% as of mid-May 2020.

After modeling this "5/10" scenario within our quantitative process, we captured the rating transitions (see table 3). A majority of the speculative-grade CLO notes experience downgrades.

A majority of each of the investment-grade-rated CLO notes do not experience a downgrade, though about 43% of 'BBB' category CLO notes lose their investment-grade status (mostly from just a one-notch downgrade since most new issue CLO 'BBB' category notes in recent years have been rated 'BBB-' rather than 'BBB').

Table 3 | Cash Flow Results Under "5/10" Scenario

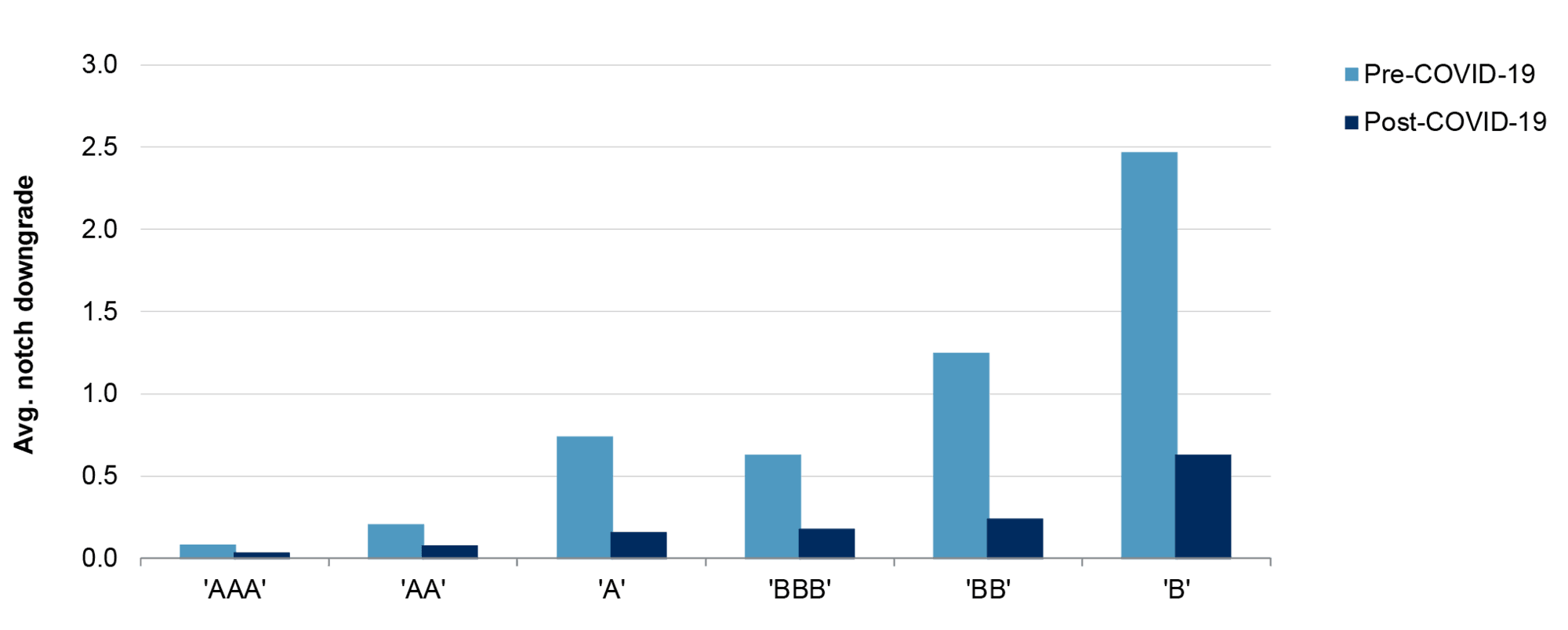

As noted above, CLO vintage has a significant impact on the rating transition outcomes from this "5/10" scenario, as well as the other four scenarios in this study. In table 3 above, we provide average 'CCC' and default buckets as of the starting point in mid-May 2021, as well as for each of the five scenarios for the deals that have closed pre-COVID-19 and for the deals that closed post-COVID-19. The pre-COVID-19 CLOs had weaker credit distribution and, thus, had larger exposure to the 178 weakest obligors we assumed would default in this "5/10" scenario.

As a result, the default bucket for the pre-COVID-19 CLOs increased to 5.5%, on average, while the same bucket for the post-COVID-19 CLOs increased to only 1.5% under this same "5/10" scenario.

Both the pre- and post-COVID-19 CLOs show resilience against the stresses we put them through. However, when we bifurcate the results between the two sets of transactions, we see a difference in the rating outcomes between the two within a given scenario, especially at the lower rating levels. This is because the newer transactions, having not experienced the credit effects of the pandemic, generally have cleaner portfolios and larger rating cushions in place than do the pre-COVID-19 transactions. This theme carries across all five scenarios within this study.

Chart 2 | Comparison Of Pre-COVID19 CLO And Newer CLO Transitions For The "5/10"

In this scenario, we assume that 327 of the weakest obligors (as determined by rating and loan price) experience a payment default, and that 337 issuers see their rating lowered into the 'CCC' range.

As a result, the average CLO exposure to defaulted assets and assets from obligors with a rating in the 'CCC' range increases to about 10% and 20%, respectively, from 0.1% and 6.3% as of mid-May 2020.

In this scenario, all of the obligors currently rated within the 'CCC' category as well as a few 'B-' rated obligors with low loan prices are assumed defaulted.

Some of the pre-COVID-19 CLOs within the sample currently have double-digit 'CCC' buckets, all of which and then some are treated as defaulted. As expected, the outcomes are harsher this time around.

We see a majority of 'AA' and below-rated notes experience downgrades, but only the 'AAA' notes see a majority of their ratings affirmed. All of the 'AAA' and 'AA' notes and just about all of the 'A' notes, maintain investment-grade ratings, while a large majority of the 'BBB' notes now go to speculative-grade ratings.

Table 4 | Cash Flow Results Under "10/20" Scenario

In this scenario, we assume that 413 of the weakest obligors (as determined by rating and loan price) experience a payment default, and that 424 issuers see their rating lowered into the 'CCC' range.

As a result, the average CLO exposure to defaulted assets and assets from obligors with a rating in the 'CCC' range increases to about 15% and 30%, respectively, from 0.1% and 6.3% as of mid-May 2020.

As noted in table 2 above, the pre-COVID-19 CLOs experience par loss of 8.9% on average, while post-COVID-19 CLOs experience 4.8% in this scenario. A majority of the CLO notes rated 'BB' and below do not pass our 'CCC-' rating stresses, meaning they may be at risk of default at some point in their lives.

Table 5 | Cash Flow Results Under "15/30" Scenario

In this scenario, we assume that 502 of the weakest obligors (as determined by rating and loan price) experience a payment default, and that 534 issuers see their rating lowered into the 'CCC' range. As a result, the average CLO exposure to defaulted assets and assets from obligors with a rating in the 'CCC' range increases to about 20% and 40%, respectively, from 0.1% and 6.3% as of mid-May 2020.

It is no surprise that the average notch movement increases as we dial up the stress in this "20/40" scenario. A majority of the CLO notes rated 'BBB' and below do not pass our 'CCC-' rating stresses, meaning they may be at risk of default at some point in their lives. None of the 'AAA' CLO ratings move below 'A+', and a majority only get downgraded one notch.

Table 6 | Cash Flow Results Under "20/40" Scenario

In addition to re-running four of the scenarios we published in our April 2020 article, we included this last scenario where we set the base-case projected S&P/LSTA Leverage Loan Index default rate of 1.75% (see "The S&P/LSTA Leveraged Loan Index Default Rate Is Expected To Fall To 1.75% By March 2022," published June 15, 2021) to the target average default exposure across our sample of CLOs, and double that same figure for our target average 'CCC' exposure of 3.50%. To achieve this, we assume that 66 of the weakest obligors (as determined by rating and loan price) experience a payment default, and that 118 issuers end up with a rating in the 'CCC' range. Given that the 'CCC' exposure in the scenario is lower than the current value across our sample, to achieve this scenario, we downgraded ratings from 184 issuers and upgraded ratings from 80 'CCC+' issuers to 'B-'.

Table 7 | Cash Flow Results Under "1.75/3.50" Scenario

Historically, average CLO portfolio exposure to defaults obligors have mostly been lower than the one-year lagging default rate (by count), perhaps partially due to asset selection and manager intervention. By setting the average default exposure to the lagging default rate, although small relative to the prior four stresses, the impact of this scenario where the average default exposure increases toward 1.75% by defaulting another 66 issuers can still be significant for some CLO that currently have larger exposures to these weaker issuers.

There are a few handful of 'AAA' and 'AA' CLO notes within our sample that experience downgrades within this scenario, almost all from pre-COVID-19 CLOs. Many of the pre-COVID-19 CLO ratings that have not been downgraded in 2020 have experienced rating cushion erosion, so it's not surprising that a small stress (on top of what they have been through already) can still result in transitions in our quantitative analysis.

We note that the reduction of the 'CCC' bucket to 3.5% through the upgrades of 80 'CCC+' rated issuers to 'B-' have an offsetting positive effect for some deals. In particular, some deals that have been downgraded in 2020 have benefitted from issuer upgrades out of the 'CCC' category and into 'B-'. We note in this "1.75/3.50" scenario, not all of the CLO notes currently rated within the 'BB' category within our sample remain speculative grade (96.2%). The difference of 3.8% are from CLO notes that have been downgraded from 'BBB-' in 2020, that now pass at an investment-grade rating under this scenario.

Our analysis shows the fundamentals of the CLO structure protecting senior noteholders, as over 90% of the 'AAA' CLO notes are within a one-notch downgrade even in the harshest of the scenarios where defaults and 'CCC' buckets across CLOs reach 20% and 40%.