Aug. 31, 2021

This report does not constitute a rating action

Sandeep Chana London +44-20-7176-3923

Nefeli Economidou Foka London +44-20-7176-0643

European CLO 2.0 equity has demonstrated resilience, achieving annualized equity returns (AER) similar to those of previous years, even when considering the severe market disruptions stemming from the COVID-19 pandemic.

CLO equity returns continue to be affected by key factors such as asset selection and funding costs, and we have identified new relationships demonstrating trend patterns against equity returns.

Individually, some variables are more effective than others in driving CLO equity performance, though these features come with associated risks.

Collateralized loan obligation (CLO) equity tranches--classified as those that receive excess cash flows after coupon and/or principal payments to the CLO debt tranches--comprise the highest risk and generate the highest return potential in CLO structures.

Considered as the first-loss piece in any CLO structure, their relative rate of return offers market participants unique insights not only into overall CLO performance, but also its relationship to effective CLO structures, portfolio construction, and CLO management strategies.

To date, European CLO equity returns have remained robust, even under current market headwinds. In this article, S&P Global Ratings examines several unique underlying relationship trends between CLO variables and equity returns, and focuses on how and why particular features in CLO structures and portfolio construction have been crucial in influencing CLO equity performance.

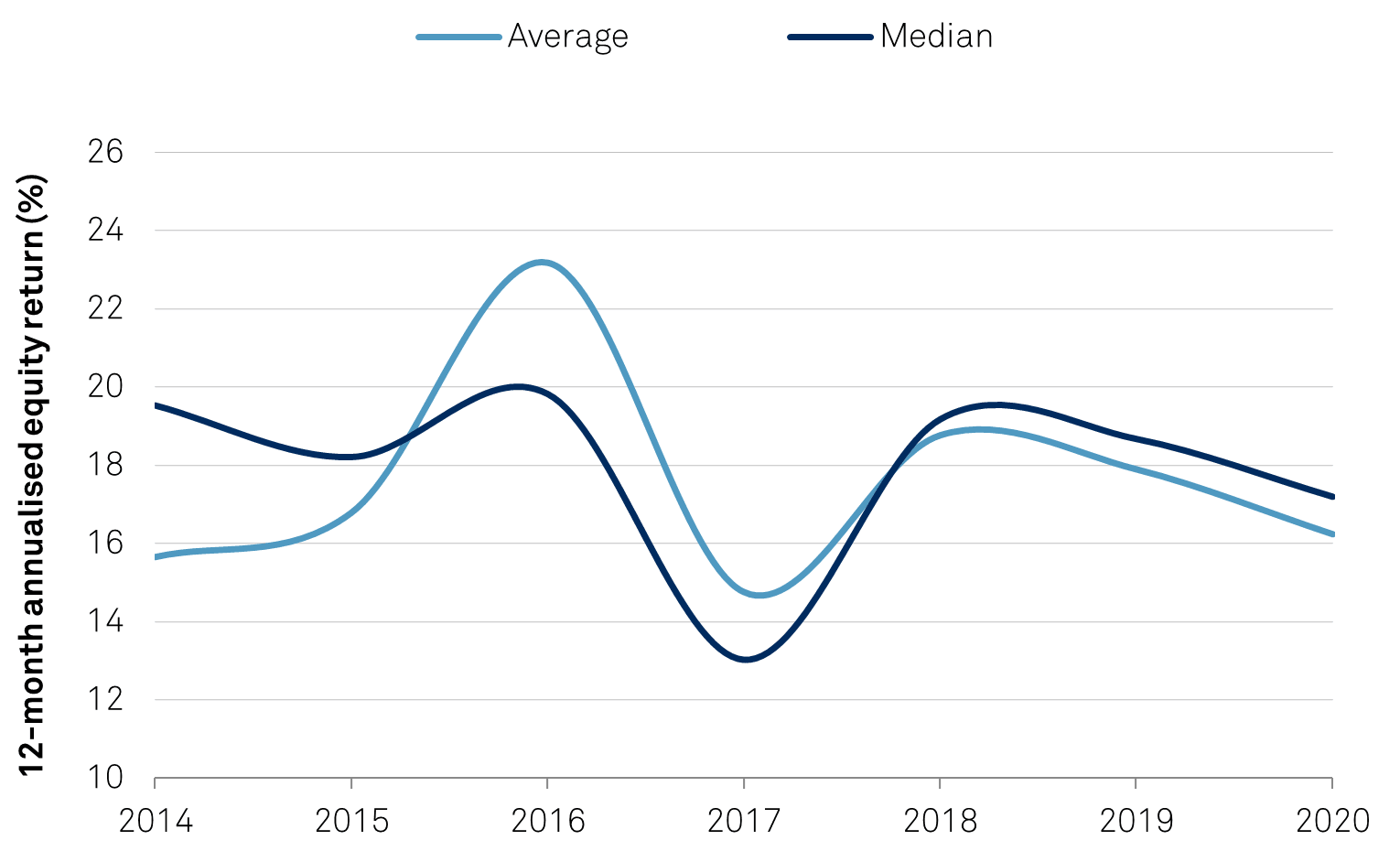

Based on our dataset, which contains all European CLO 2.0 transactions we currently rate, CLO equity cash flow distributions in the past 12 months have averaged 14.04%.

Considering that it averaged 12.69% over the previous 12 months, the distribution highlights a strong and steady CLO performance in spite of the pandemic’s effect on the global macroeconomy and wider markets (see chart 1).

On a median basis, equity distributions across our CLO dataset have returned 12.69% compared with 13.69% in the previous 12 months--lower, but still robust returns considering concurrent headwinds. Additionally, we note a wide range in trailing 12-month annualized equity distributions, between 2.65% and 40.12% (the maximum being driven by a 2020 vintage CLO. At the same time, the average and median 12-month trailing annualized equity distributions are 16.24% and 17.20%, respectively.

In our view, this is predominantly driven by portfolio composition, transaction structures, and multiple equity distributions relative to a CLO’s average annualized distributions on the first payment date.

Chart 1 | 12-Month Annualized Equity Returns Based on CLOs which have incurred 3 or more IPDs

Source: S&P Global Ratings.

Before we dive into the analysis, it's important to note that 2020 vintage CLO structures and their respective underlying portfolios were arranged very differently from most of the traditional arbitrage CLOs that make part of this dataset, namely with significantly less leverage, more defensive structures, and with shorter non-call and reinvestment periods (see "CLO Spotlight: Redesigning The CLO Blueprint After COVID-19," published on April 21, 2020). This has resulted in a number of outliers in the trends we explore, and therefore weaker relationships arising in some cases when consolidating 2020 vintage equity returns with all other vintages. This is unsurprising, in our view, as these CLO structures were purposely structured to be more defensive against the then market headwinds rather than being issued as traditional arbitrage transactions as originally intended. Therefore, in some instances during our analysis we explore relationships with and without 2020 CLO vintage results, and in some cases pay particular attention to the performance of 2020 CLO vintage data only.

So, how were CLOs able to generate such robust returns?

As we observed in our publication, “Examining Equity: What Drives Returns In European CLO 2.0 Transactions?,” a combination of long first periods, the ability for CLOs to transfer ramp-up excess principal proceeds to interest, first-period interest reserve accounts, ramp-up speed and warehousing terms, and in some cases, the utilization of liquidity facilities, have all significantly contributed to most CLOs generating above-average equity distributions on their first payment date (see chart 2).

These sources and uses of proceeds also consider the purchase price paid for the underlying pool of assets, which during the course of the pandemic were trading at relatively lower prices, helping contribute more proceeds toward first-period equity distributions. High front-loaded cash flows is a distinctive feature of CLO equity, making it a moderate duration investment and therefore appealing to equity investors, in our view.

From our dataset, CLO managers such as PGIM (with several CLOs), Blackrock, GSO, and Invesco have yielded some of the highest first-period returns to investors. PGIM, for example, has consistently yielded some of the highest first-period returns over consecutive years.

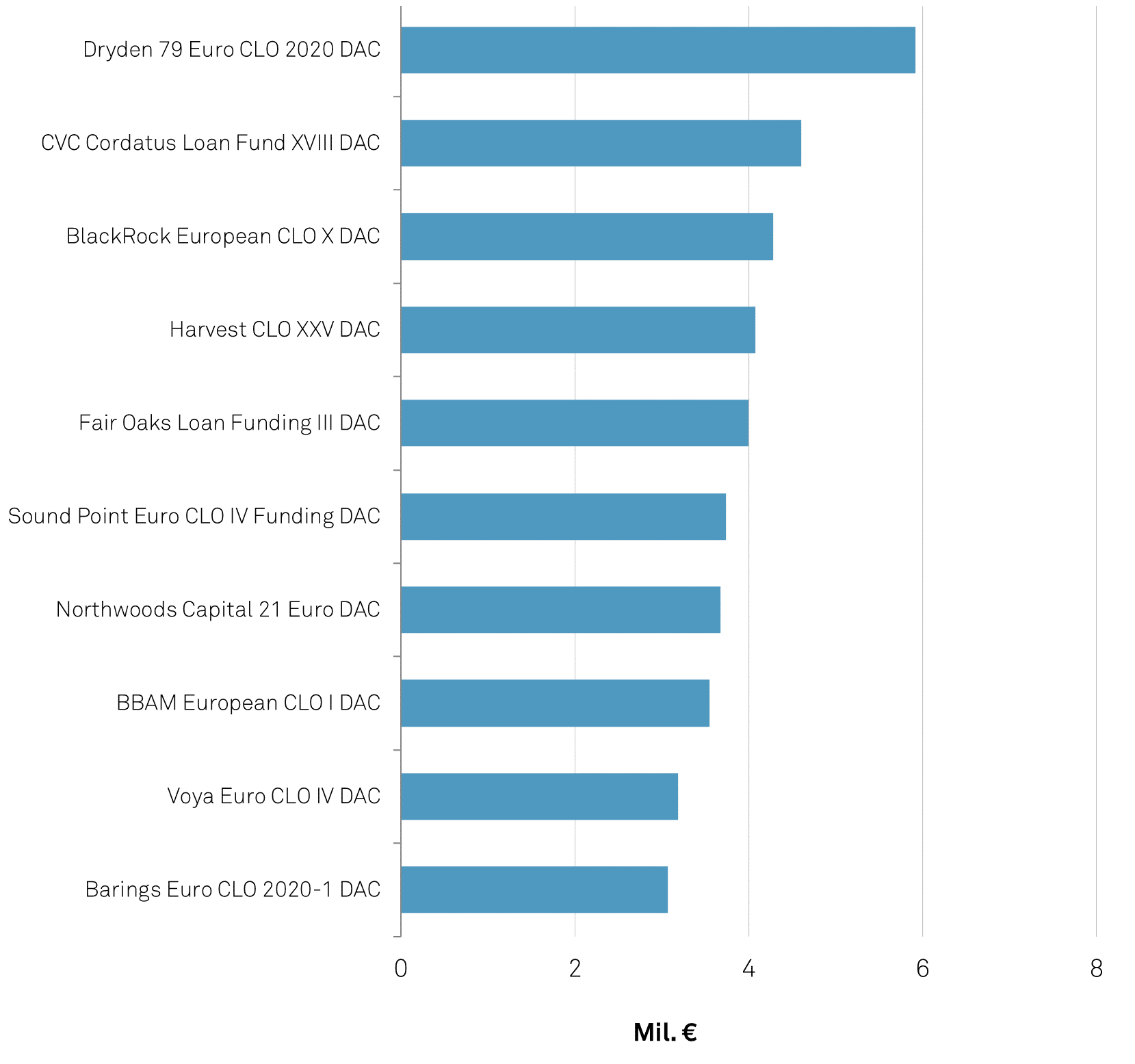

Chart 2 | Initial CLO Equity Distributions As A Multiple Of Average Equity Distributions By CLO Vintage

Source: S&P Global Ratings, trustee reports.

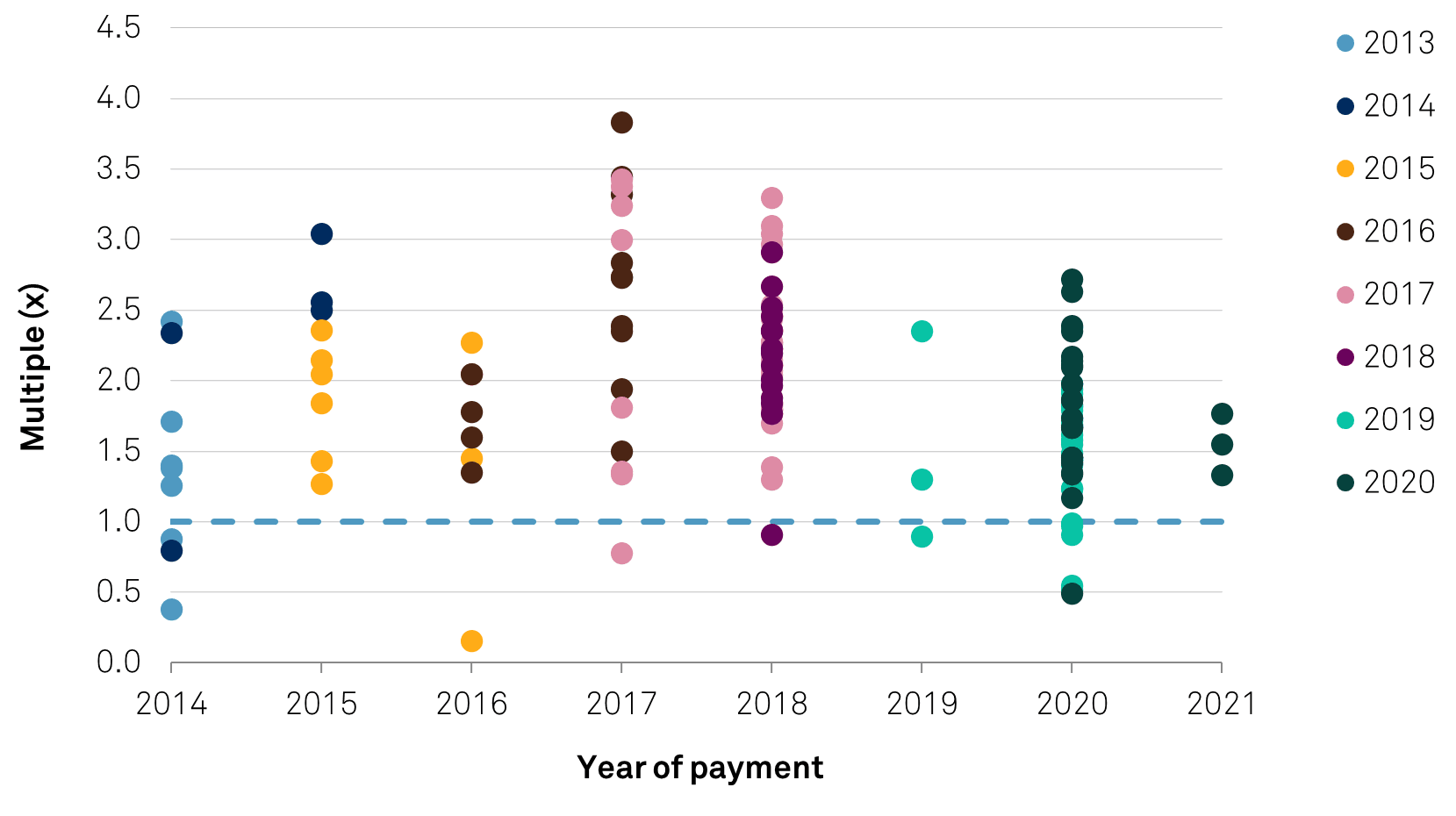

We have deliberately excluded from chart 2 any 2020 and 2021 vintage CLOs that have so far made less than three equity distributions, due to the limited number of distributions when calculating the average equity payment benchmark.

Instead, we have charted these results separately in chart 3. Here, we draw on total nominal return to equity.

Chart 3 | CLO Initial Equity Distributions (Top 10 Distributions) With less than three payment dates

First payment date equity distributions are just one of several key factors that affect equity performance, and represent only one source of cash flow distribution to equity investors. Below, we take a closer look at other factors and relationships that may have contributed toward CLO equity performance.

Note: The analysis presented hereon only includes those CLOs that have incurred more than two payment dates when comparing trends against annualized equity distributions. Our analysis also takes a simplified view that debt and equity is issued at par.

Our analysis here begins with the liability side of CLO economics: CLO structures and the formation of their rated debt.

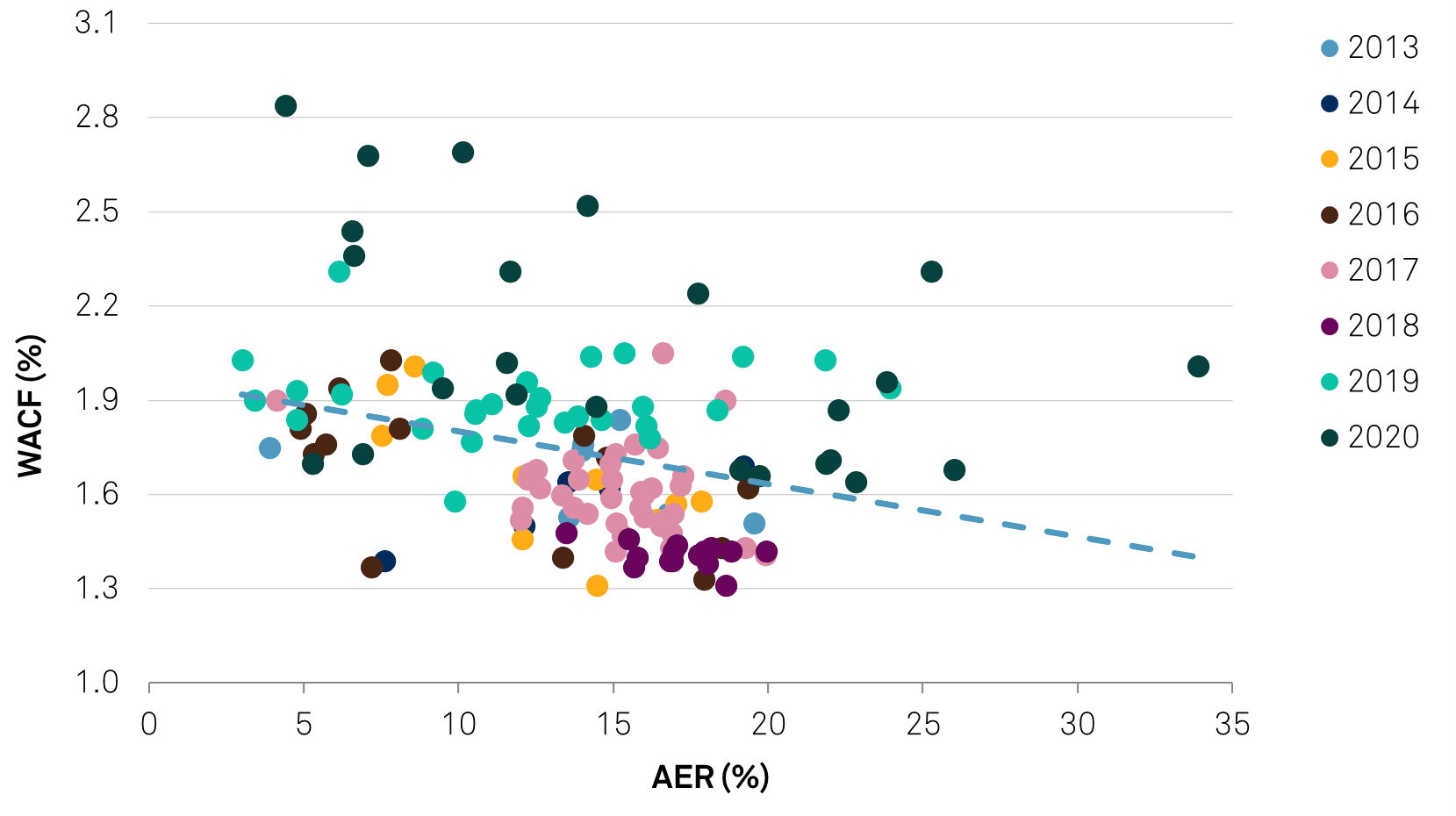

Specifically, the weighted-average cost of funding (WACF) a CLO, which is the average cost of servicing its liabilities before equity investors receive any distributions, is a key driver of CLO equity performance, in our view.

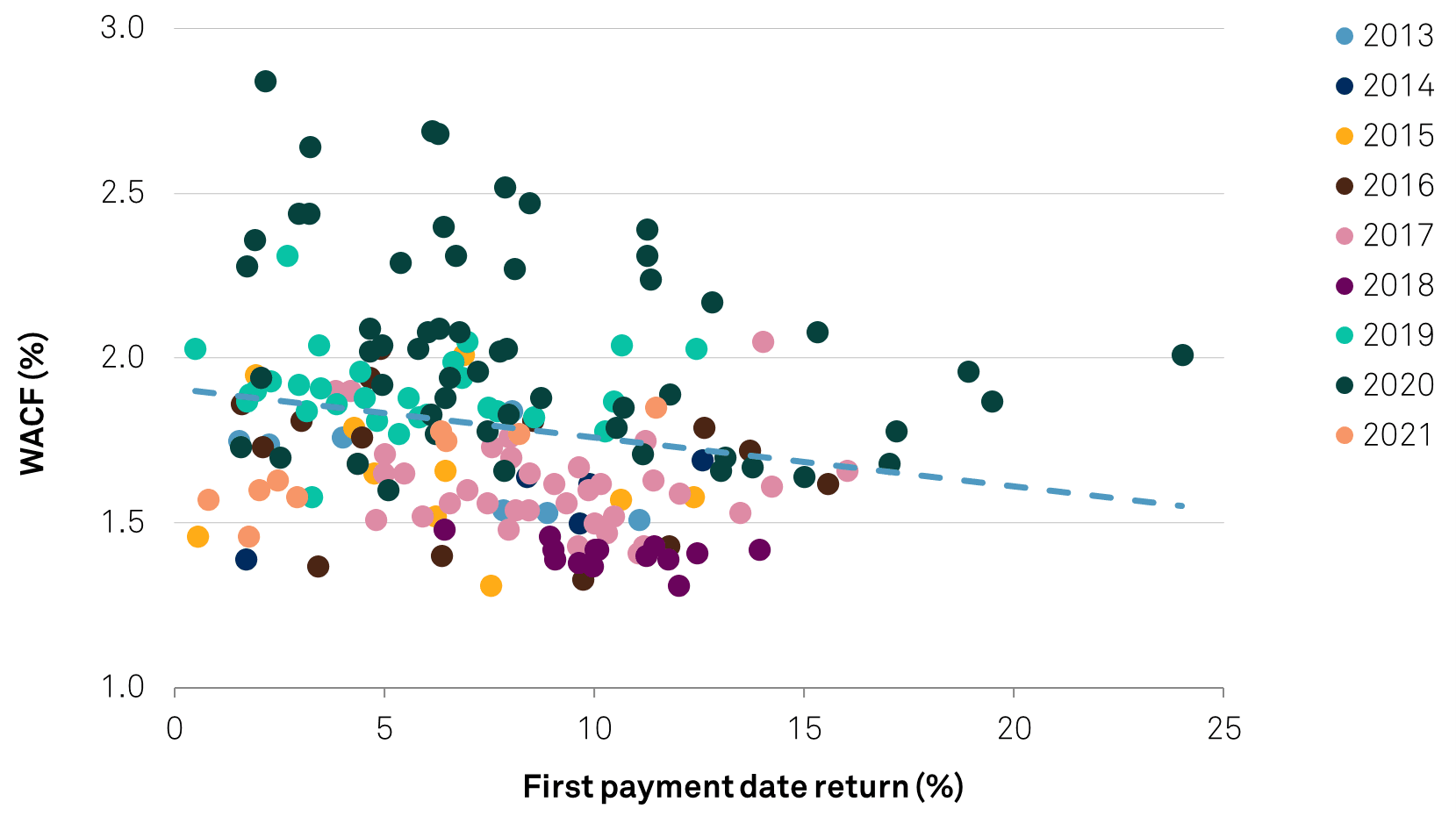

Our dataset demonstrates a strong negative relationship between annualized equity returns and the average cost of funding a CLO, implying that a relatively cheaper or less costly CLO structure would likely result in higher excess/residual income toward CLO equity, all else being equal (see chart 4). Perhaps unsurprisingly, this relationship also holds true when comparing CLO funding costs with first payment date returns to CLO equity (see chart 5).

In both cases, these relationships strengthen considerably when excluding 2020 vintage CLOs, which are synonymous with higher WACF structures as a result of the pandemic. So much so that nearly all of these are being refinanced, as their current funding rates are considerably higher than current market rates, and are therefore in-the-money for refinancing opportunity.

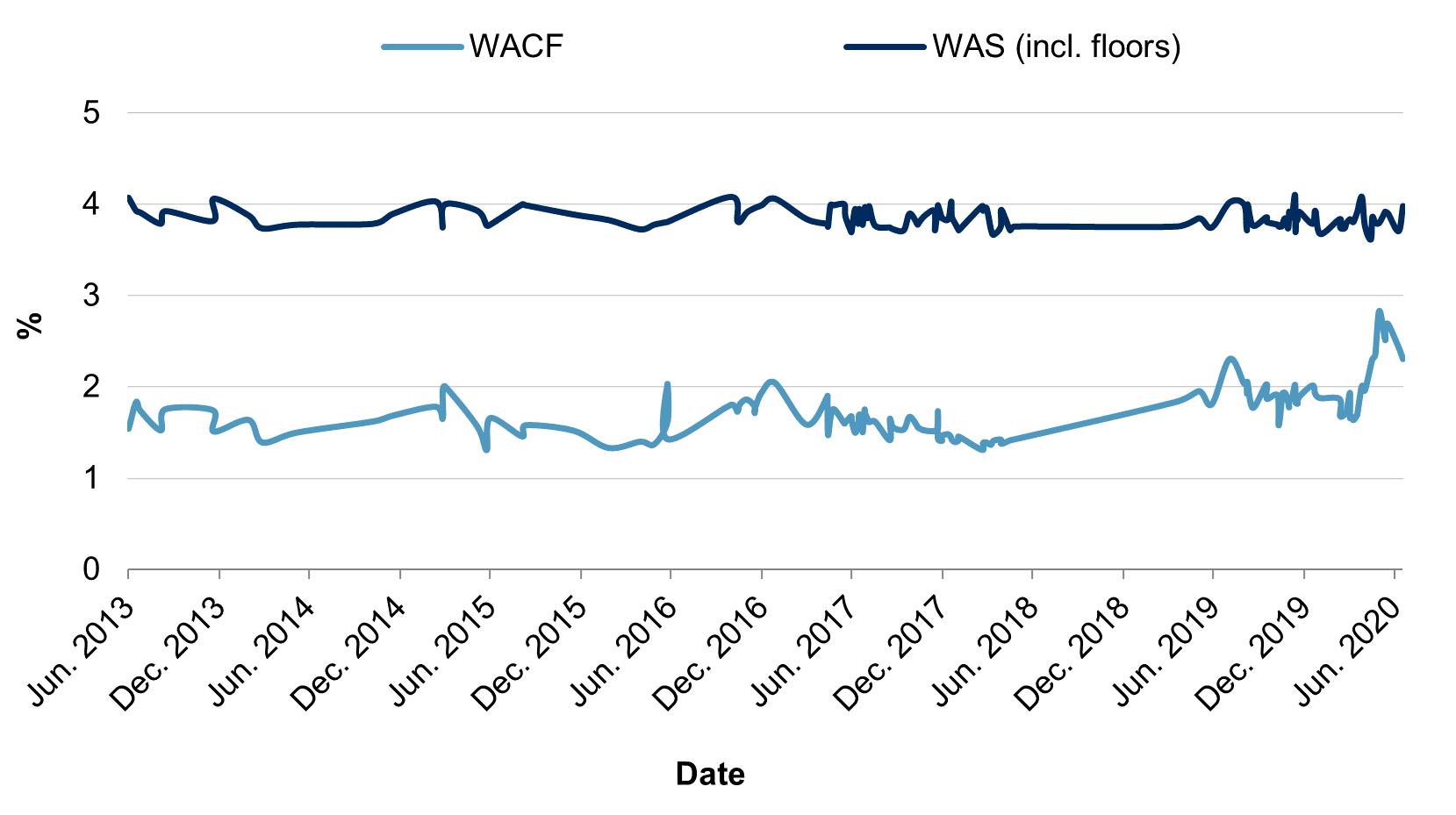

The relationship flattens for 2019 vintage CLOs, which may be partly explained by rising CLO funding costs over time relative to underlying asset spreads (see chart 6).

Chart 4 | AER Versus WACF By CLO Vintage

AER--Annualized equity return. WACF--Weighted average cost of funding. Source: S&P Global Ratings.

Chart 5 | WACF Versus First Payment Date Equity Returns By CLO Vintage

WACF--Weight average cost of funding. Source: S&P Global Ratings, trustee reports.

Chart 6 | Explaining CLO Arbitrage: The Difference Between Underlying Loan Spreads And CLO Funding Costs

WACF--Weighted average cost of funding. WAS--Weighted average spread. Source: S&P Global Ratings, trustee reports.

By the very nature of its calculation, the WACF for CLO liabilities is directly affected by the notional amount or size of each debt tranche that is issued by a CLO.

For instance, all else being equal, the more investment-grade (and therefore relatively cheaper) debt a CLO is able to issue relative to non-investment grade, then the lower the WACF. This would, at the same time, imply lower credit enhancement at senior rating levels, which would be the payoff for generating higher equity returns.

This is a simplified example, however, as several other assumptions are factored into debt tranching, including (but not limited to) the positioning of CLO par value test cushions (for example, the highest par value test in euro-denominated CLOs, which overcollateralizes the ‘AAA’ and ‘AA’ rated tranches, typically includes a 9%-10% cushion on its par value test), the headroom available under CLO collateral quality tests, manager tiering, rating agency methodology stresses, the demand for rated-debt in a CLO’s capital structure, and/or minimum credit enhancement levels required by CLO investors.

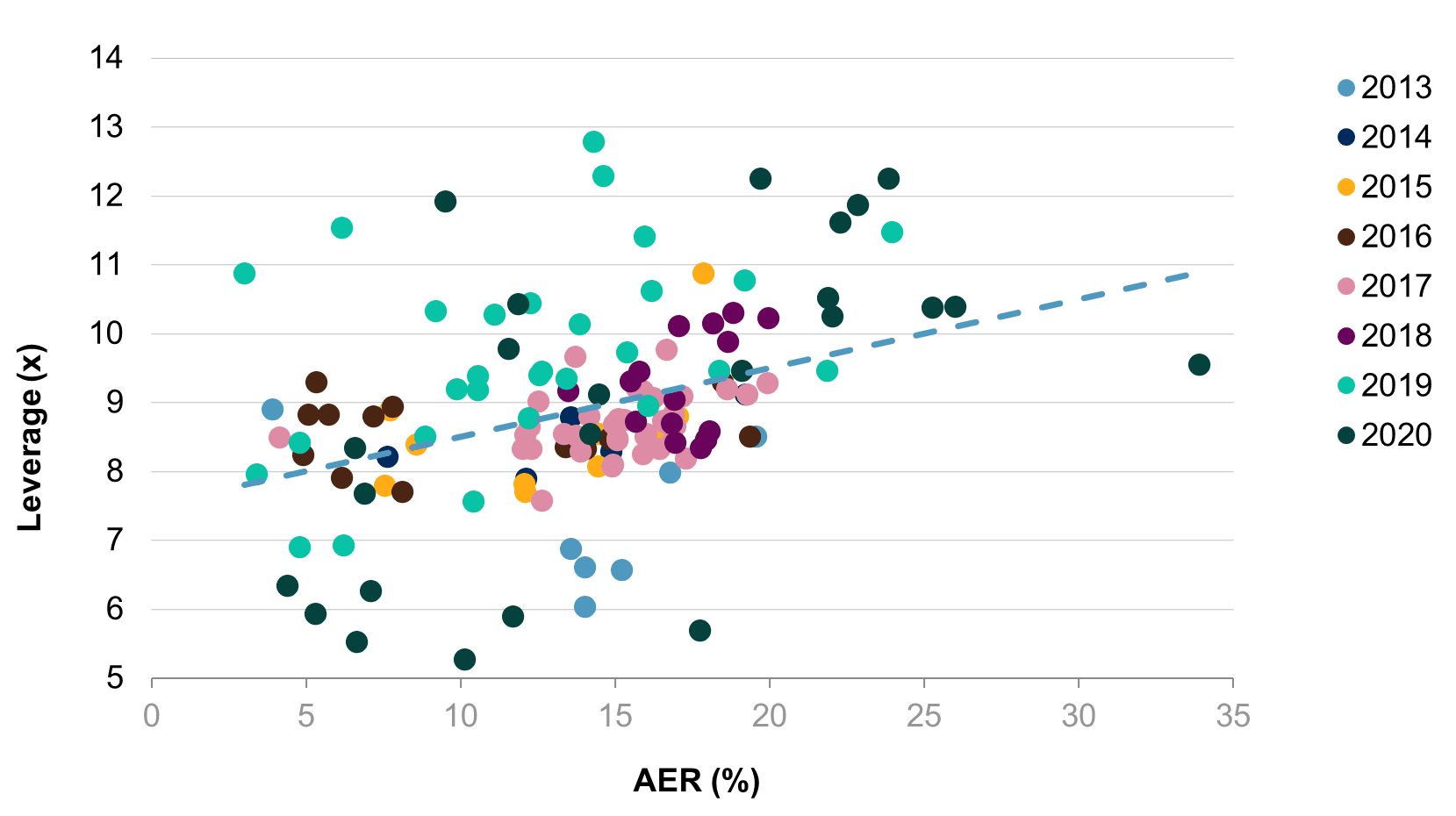

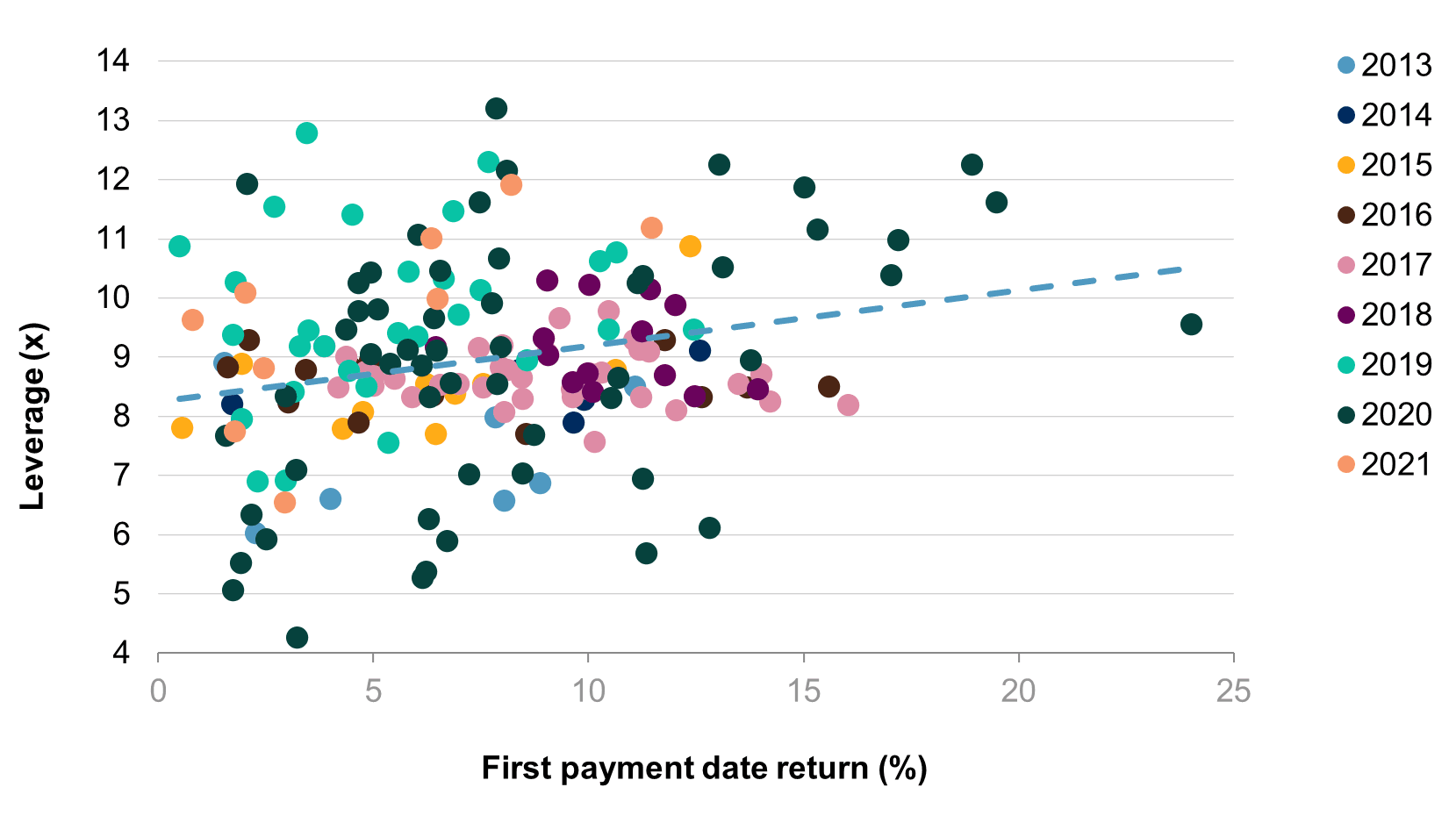

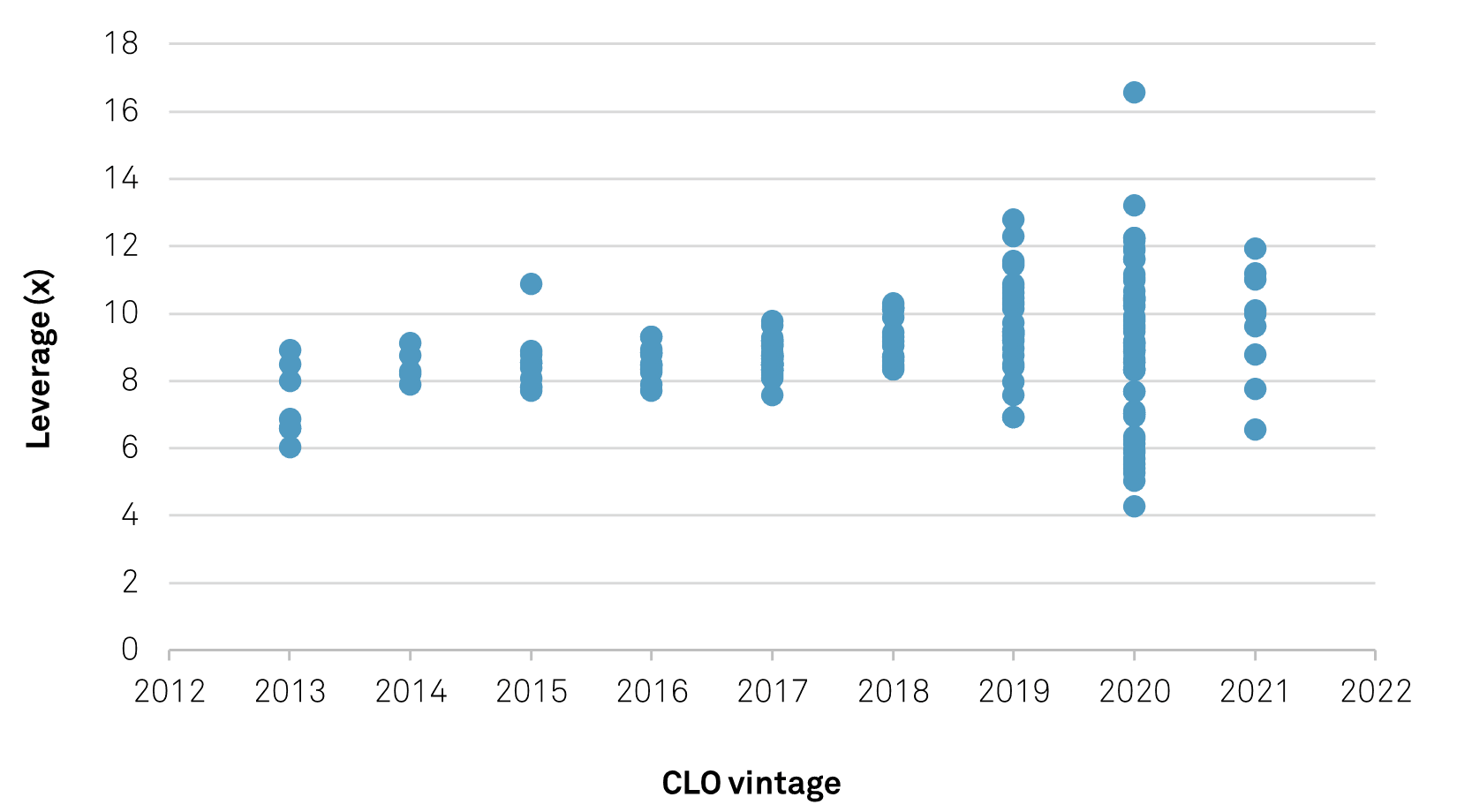

Leverage, defined here as the aggregate of notional rated debt over notional equity, is also a key factor in constructing CLO-arbitrage. However, this relationship is more subtle in our view, because leverage numbers disguise the effectiveness of debt tranching and funding costs to achieve optimal CLO arbitrage. There are more outliers and therefore a weaker correlation in the dataset when drawing the relationship between CLO equity return performance and leverage levels than when comparing against the WACF (see charts 7 and 8). Overall, 2020 vintage CLOs generate the widest range of results, as leverage across these CLOs varied considerably during the year--the widest variance seen across any vintage.

Chart 9 displays a widening range in leverage across CLOs over time, which explains why there are greater outliers the more recent the vintage (i.e., a greater standard deviation).

Chart 7 | AER Versus Leverage By Vintage

AER--Annualized equity return. Source: S&P Global Ratings, trustee reports.

Chart 8 | Leverage Versus First Payment Date Returns By CLO Vintage

Chart 9 | CLO Leverage, By Vintage

Our analysis now takes us to the asset side equation of CLO economics: portfolio composition.

Asset selection affects equity returns. And as such, CLO managers carefully construct CLO portfolios to balance the trade-off between investing in high quality leveraged companies and the benefit this provides to debt investors, while also generating competitive returns for CLO equity investors.

Crucial to portfolio selection, therefore, is the rate of flexibility provided to CLOs in asset concentration levels, collateral quality and coverage tests, in so far as they do not adversely affect the benefits embedded in the formation of CLO structures discussed in the previous section.

To generate higher periodic returns, CLO managers are likely to take more risk in their credit-selection and management of a CLO on a relative basis.

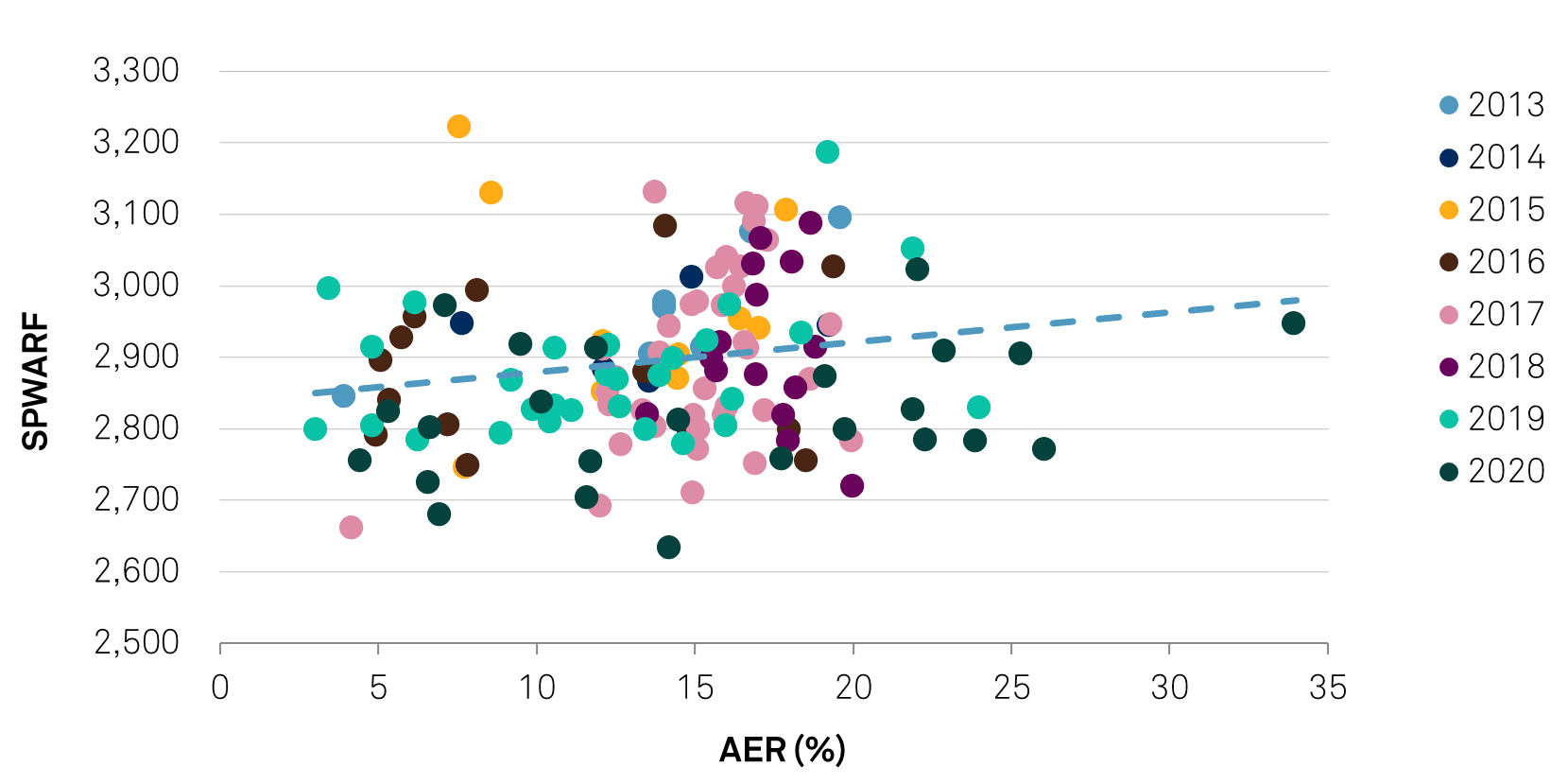

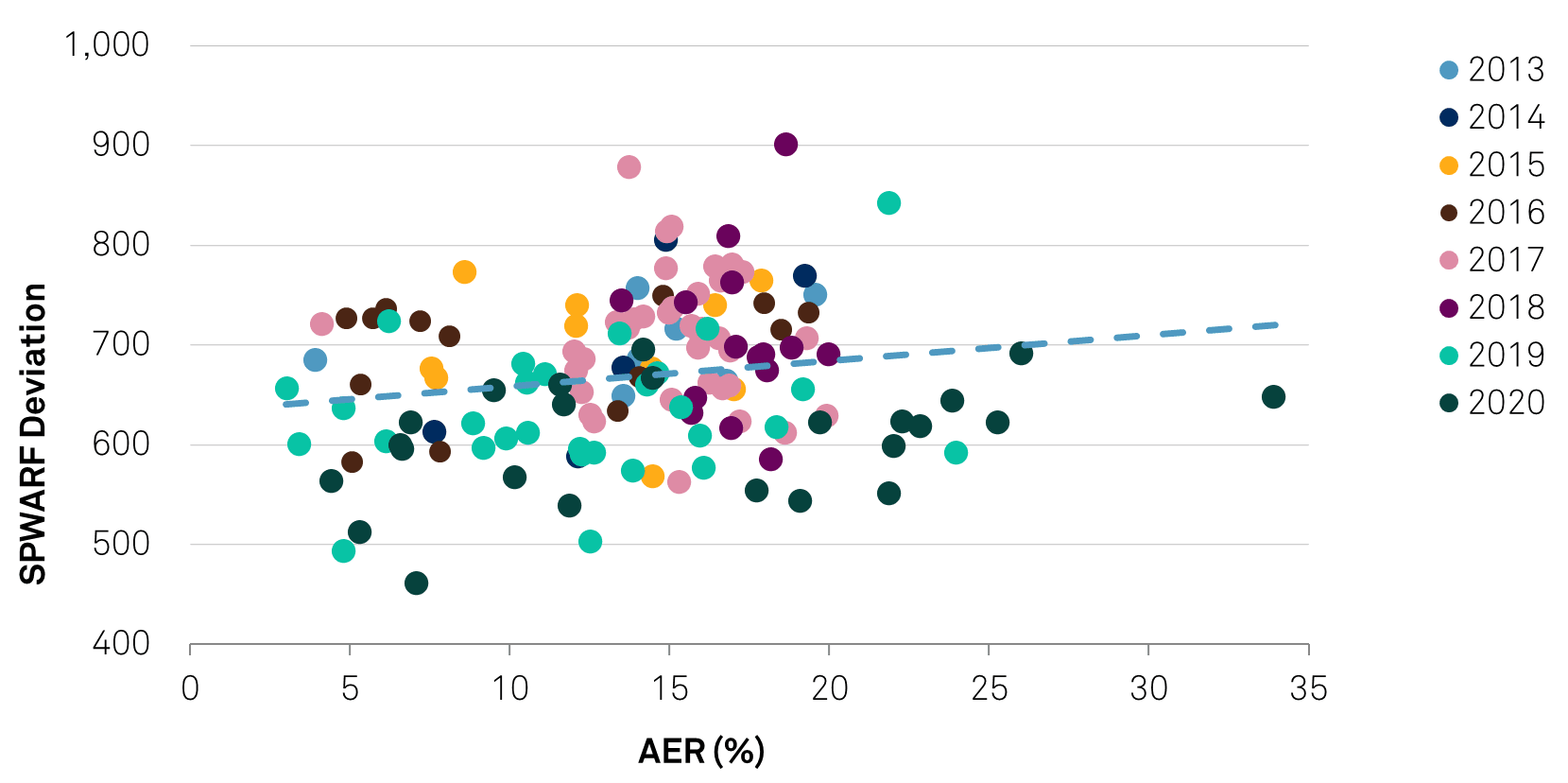

Chart 10 provides one example in supporting this theory, plotting annualized equity returns against each CLO’s S&P weighted-average rating factor (SPWARF; a measure of a CLO’s overall credit quality). Here, we notice a broadly positive relationship between the two variables, whose trend is strengthened when excluding 2020 vintage CLOs. The SPWARF provides a blended average of overall credit quality in an underlying CLO portfolio, and so a closer look at a CLO portfolio’s deviation from SPWARF highlights how a more extreme (or less homogenous) constructed portfolio delivers higher returns to equity investors (see chart 11). Therefore, it seems that particular managers who are able to build a CLO portfolio that suits their unique management style are able to generate relatively higher equity income, balancing the payoff between portfolio risk management against healthy equity returns.

Furthermore, nearly all 2020 vintage CLOs in both charts 10 and 11 remain below the established trend line, highlighting not only that these vintage CLOs were constructed to be relatively more defensive during the pandemic in order to protect portfolio credit quality, but also how their portfolios were more homogenous relative to other vintages, presumably investing in similar credits and industries that are less sensitive to the effect of the pandemic at the time.

Of note, a higher SPWARF is generally associated with a lower credit quality portfolio.

Chart 10 | AER Versus SPWARF, By CLO Vintage

Chart 11 | AER Versus Deviation From SPWARF, By CLO Vintage

AER--Annualized equity return. SPWARF--S&P Global Ratings weighted average rating factor. Source: S&P Global Ratings, trustee reports.

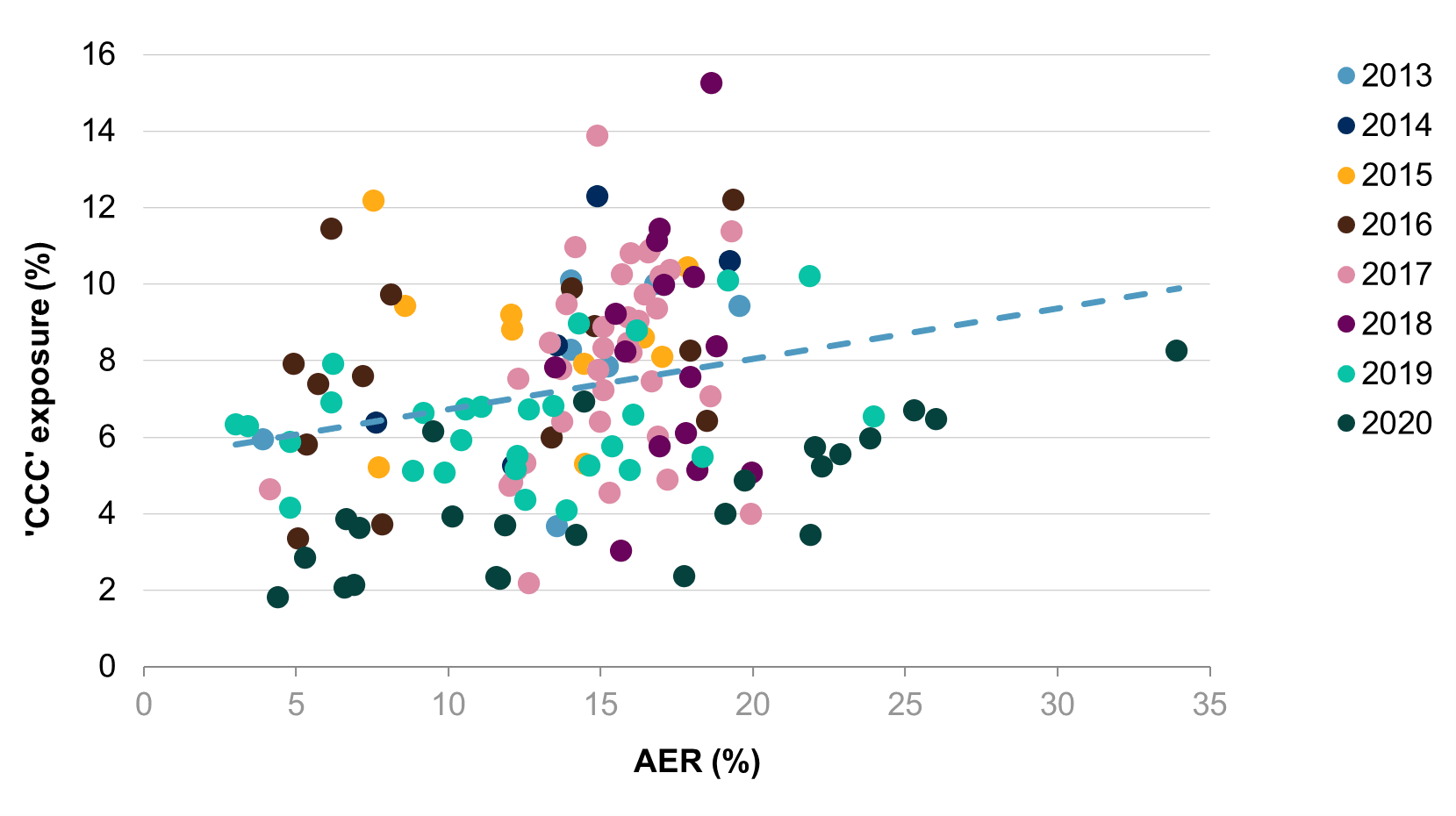

We narrow the above variables further in our dataset and identify strong-positive relationships between asset-rating percentages and equity returns, reaffirming the risk-reward relationship between higher credit risk assets and equity performance (see chart 12, which compares the level of ‘CCC’ rated asset exposure against annualized equity returns).

Chart 12 | AER Versus 'CCC' Exposure, By CLO Vintage

Here again, we note how 2020 vintage CLOs stand out against their counterpart vintages, with nearly all these CLOs marking below the trend line.

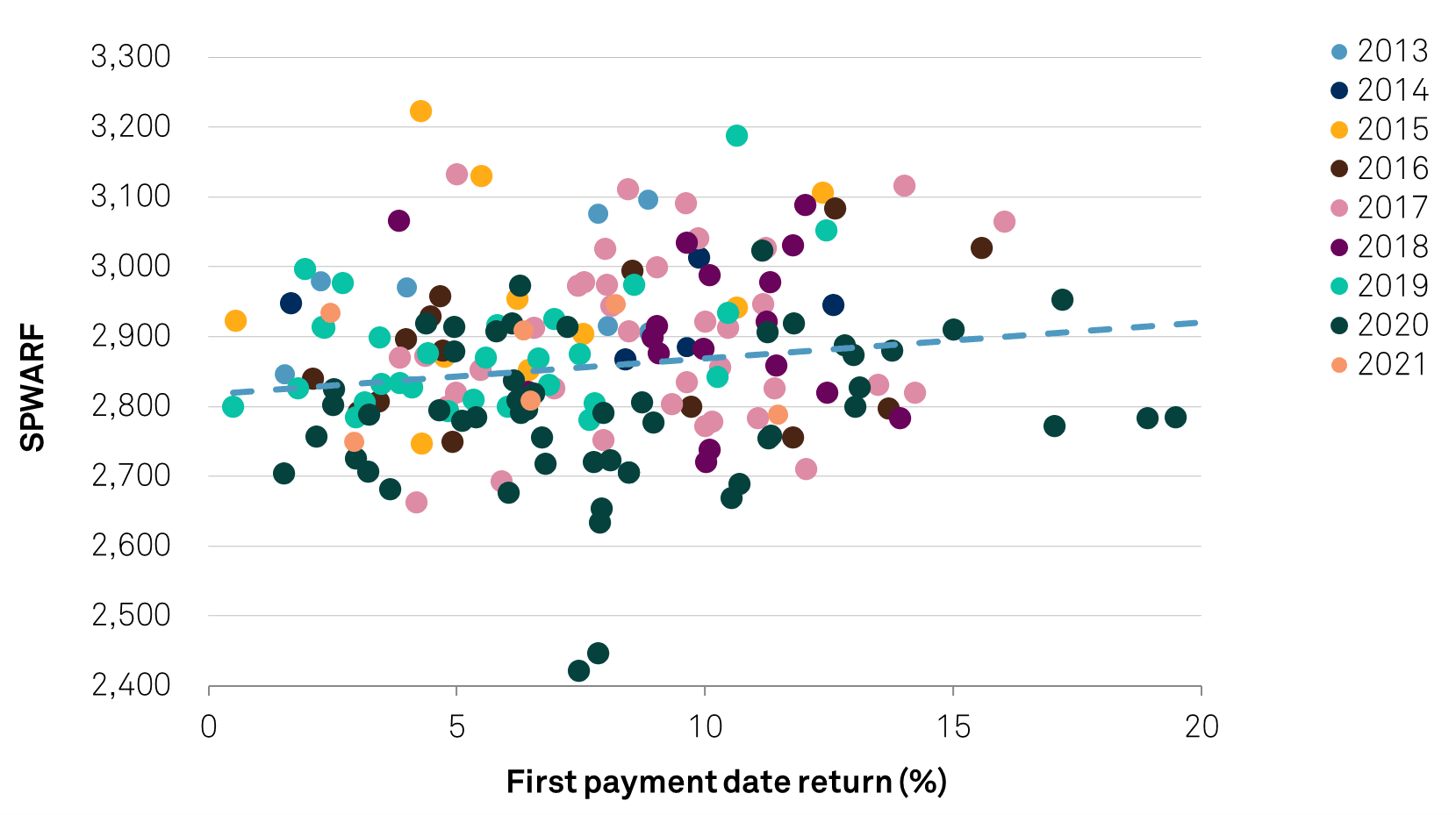

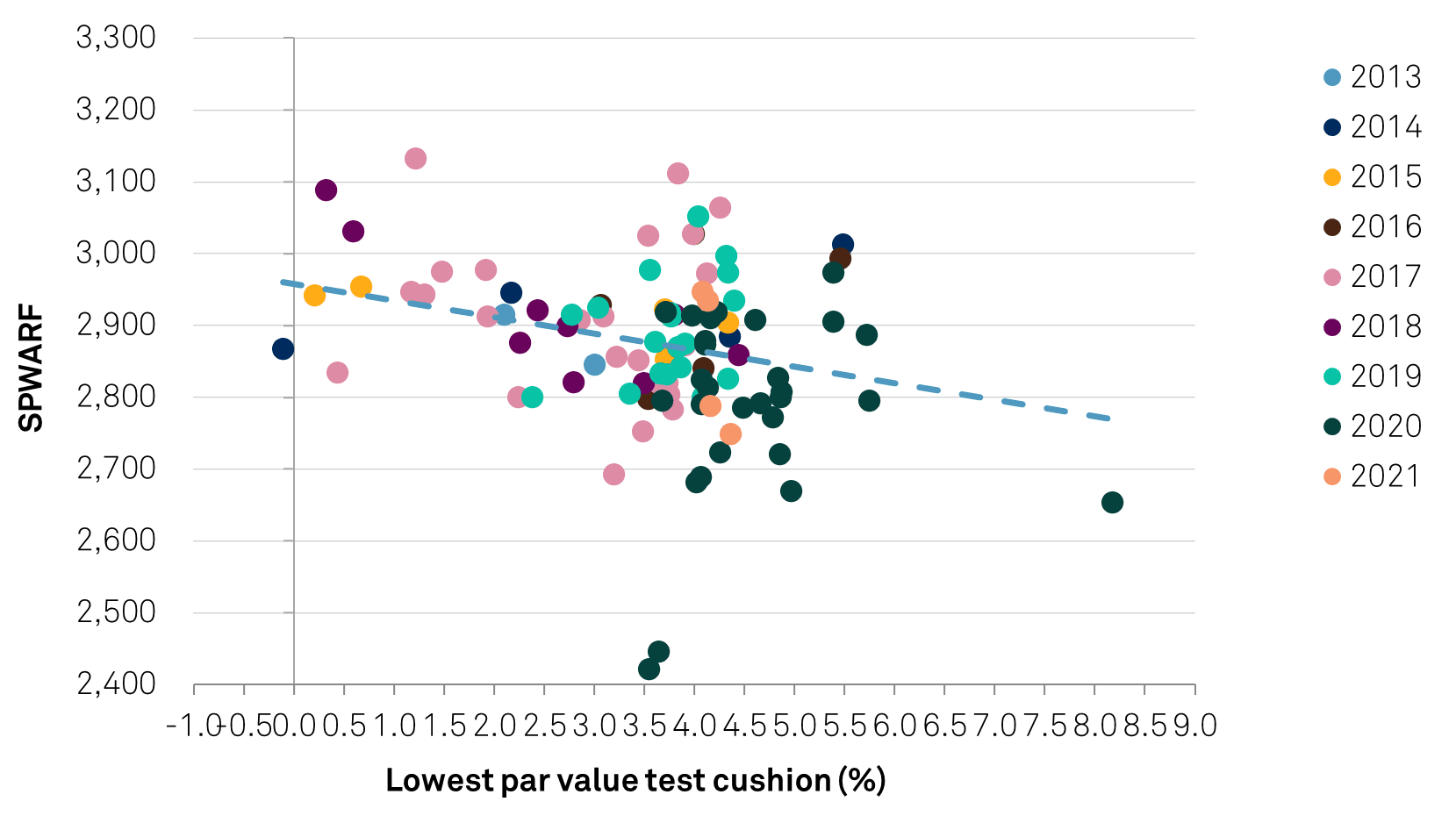

Similarly, SPWARF scores and first payment date returns to CLO equity are strongly related, which highlights the importance placed on generating the most competitive returns on a CLO’s inaugural payment date, more so when removing 2020 vintages (see chart 13). This may raise concerns from debt investors regarding how CLOs are ramping portfolios and potentially triggering effective date events. While this concern may be justified, there are many other factors that drive first payment date equity returns as we analyzed earlier--both credit and non-credit related--such that CLO managers continue to balance portfolio risk management with healthy equity performance. One of the key balancing acts is ensuring that the credit risk of a CLO portfolio is adequately managed against the tests and covenants that may have an adverse effect on equity income. For example, SPWARF scores against the lowest par value test cushion in CLOs exhibit a strong-negative correlation, implying that higher SPWARFs are likely to lead to a breach in one or more par value tests, resulting in less or zero equity income over a given period (see chart 14).

Chart 13 | First Payment Date Returns Versus SPWARF, By CLO Vintage

SPWARF--S&P Global Ratings weighted average rating factor. Source: S&P Global Ratings, trustee reports.

Chart 14 | SPWARF Versus Lowest Par Value Test Cushion, By CLO Vintage

Note: Where class F OC test is applicable. SPWARF--S&P Global Ratings weighted average rating factor. Source: S&P Global Ratings, trustee reports.

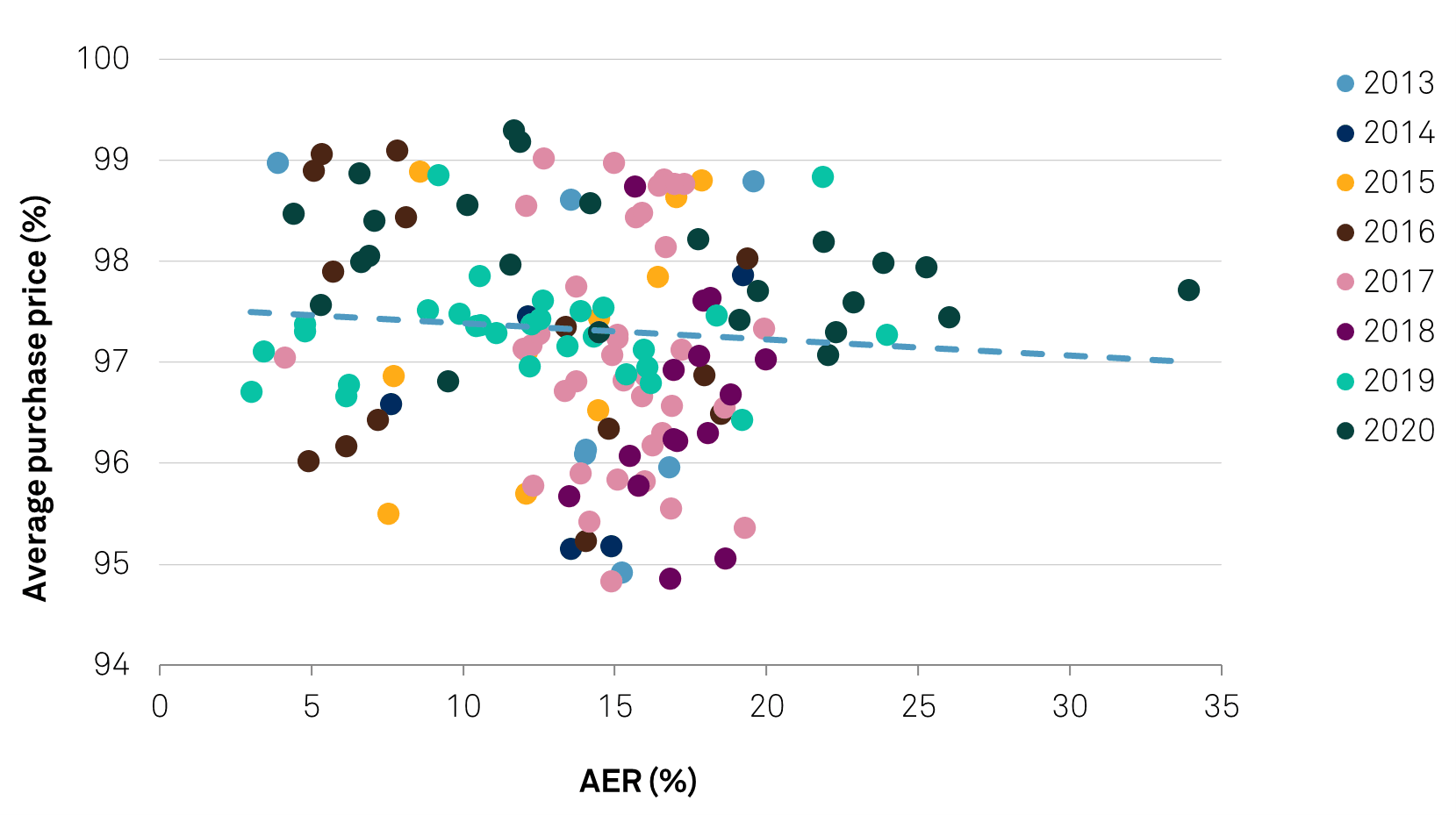

Setting aside rating-relationships, the average purchase price of CLO pools and their annualized returns are distinctly related (see chart 15).

The supposition here is that assets with lower prices are generally associated with exhibiting weaker credit profiles, and therefore are more likely to default than those that trade at higher prices.

The upside is that these assets are higher yielding and therefore present higher return potential to CLO equity.

Additionally, CLO documentation allows for further value-add from discount asset purchases, typically in the form of trading gain language. A trading gain mechanism allows CLO managers, at any time, to recharacterize principal proceeds as interest proceeds when an asset’s sale and/or pre/repayment receipts are above the purchase price paid for the asset or its par balance, subject to certain conditions being satisfied. A lower purchase price therefore provides a several-fold benefit to CLO economics and its arbitrage: these assets may be carried at par in the calculation of par value tests provided they are not classified as discount obligations, they are likely to be higher yielding, and they may be earmarked for future trading gains to bolster equity returns.

Chart 15 | AER Versus Average Purchase Price, By CLO Vintage

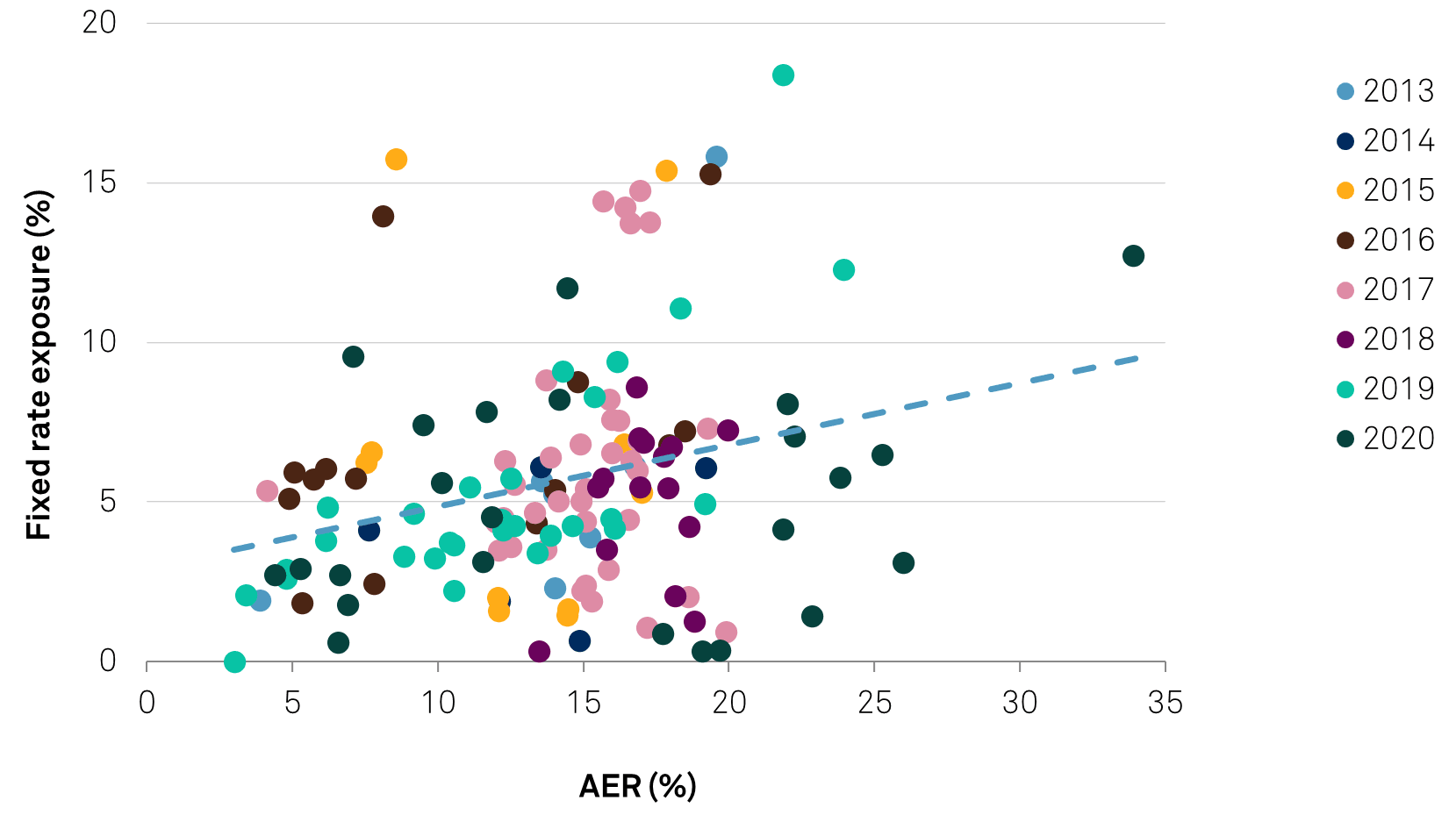

A higher proportion of fixed-rate-paying loans and bonds underlying CLO portfolios strongly correlates with higher annualized equity returns, according to our dataset (see chart 16).

Yields on fixed rate loans and bonds typically exceed those of their floating rate counterparts, since they carry interest rate risk, which may be considered a risk factor if interest rates rise and floating rate CLO liabilities are not adequately hedged. CLOs therefore typically include a maximum limit for fixed rate asset purchases, usually around 10% of the pool balance, though there are several CLO manager platforms that allow for twice as much exposure. Fixed-rate asset exposure in CLOs are typically hedged with fixed-rate tranches, interest rate caps, and/or where floating rate CLO liabilities are structured with a cap on their margins, noting that the relative sizing of the former (and the pricing impact on the latter to some extent) may adversely affect equity returns as a result of its effect on the WACF, as discussed earlier.

As chart 16 additionally highlights, not all CLO managers fully utilize their fixed rate buckets.

Chart 16 | AER Versus Fixed Rate Exposure, By CLO Vintage

The relationships we identify underlying the formation of CLO structures and portfolios are key factors behind the robust performance of European CLO equity returns to date, in our view. While these factors are associated with increased levels of risk on a relative basis, their prime objective in optimizing CLO arbitrage has been tested during both benign economic scenarios and periods of severe stress--such as the COVID-19 pandemic--to ensure competitive returns to equity investors.

Going forward, the challenges, therefore, in ensuring consistently strong equity performance will be navigating away from troubled assets and minimizing losses where defaults do occur, especially in periods of severe economic stress

In large part, we view the role of the CLO manager, their asset selection strategy and trading capabilities as central in balancing the interests of all CLO investors in the ultimate pursuit of competitive equity returns.

For now, European CLO managers appear to have this balance well in check.

CLO Spotlight: Redesigning The CLO Blueprint After COVID-19, April 21, 2020

Examining Equity: What Drives Returns In European CLO 2.0 Transactions?, April 4, 2017