Sept. 01, 2021

This report does not constitute a rating action

Abhijit A Pawar London +44-20-7176-3774

Emanuele Tamburrano London +44-20-7176-3825

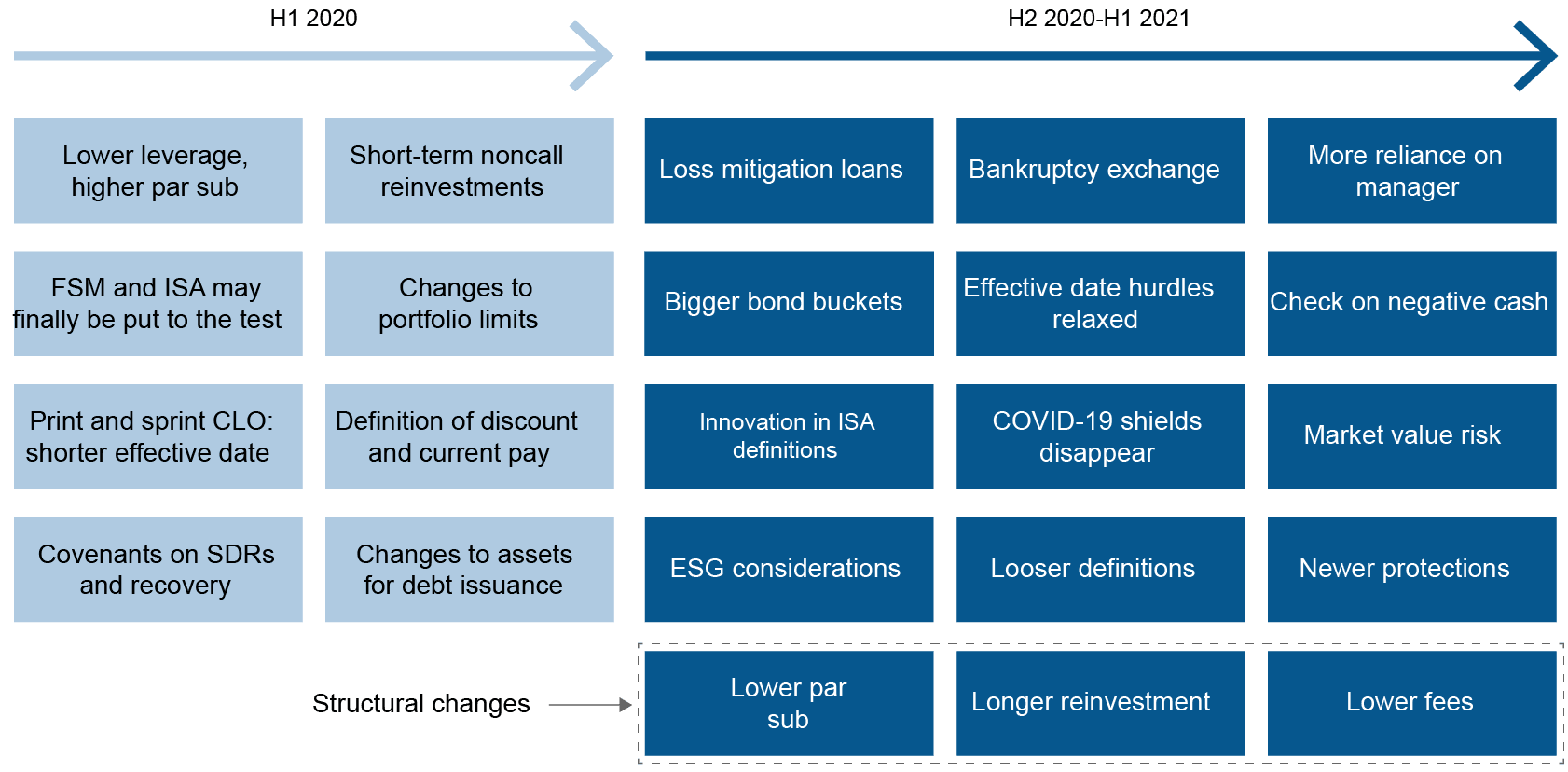

Chart 1 | The European CLO Redesign Is Gathering Pace

FSM--Frequency switch mechanism. ISA--Interest smoothing amount. SDR--Scenario default rate. Par sub--Par subordination. Source: S&P Global Ratings.

Collateralized loan obligations (CLOs) issued in Europe this year have started to again resemble prepandemic deals.

Par subordination (the buffer to par that needs to default before a loss occurs) has moved back to the 38%-40% range compared with 42%-44% for CLOs issued last year.

Documentation continues to evolve, adding further flexibility for effective management of CLO portfolios.

Issuance of CLOs in Europe rose from the beginning of 2021, buoyed by positive news of rollouts of multiple COVID-19 vaccines across the globe and brighter economic prospects. As performance concerns that clouded most of 2020 subsided, margins strengthened as well, fuelling CLO issuance momentum further. The European CLO issuance tally stood at €21.50 billion as of Aug. 24, 2021, from 53 deals; compared with €13.21 billion from 40 deals at the same time last year.

S&P Global Ratings' last CLO Spotlight, "Redesigning The CLO Blueprint After COVID-19," published April 21, 2020, highlighted changes in the financial markets and CLO landscape resulting from the COVID-19 pandemic. Last year, new CLO concepts emerged as the pandemic pushed market participants to consider changes to issuance structures and CLO documentation (such as leverage, par subordination, and reinvestment periods).

With new challenges on the horizon (like lower asset spreads, increasing the weighted-average cost of debt), we anticipate CLO documentation will continue to evolve for the rest of year as CLO managers and arrangers aim to create a niche for themselves.

At the start of the pandemic, CLOs typically had shorter reinvestment periods and higher credit enhancement than in previous years. However, as the economy began to recover from the pandemic's impact, such features began to disappear. By the end of 2020, CLOs again started to resemble their prepandemic structures, with ‘AAA’ credit enhancement shifting to the 38%-40% range and one-year reinvestment periods replaced by four- to five-year terms.

In 2021, with CLO liability spreads tightening, we've seen a resurgence of issuance of 'B-' rated notes after a brief lull in 2020. CLO arrangers have also been discussing the introduction of 'CCC’ rated tranches.

As new CLOs underwent a redesign after the pandemic began in 2020, CLO documents saw key changes, particularly relating to concentration limits. Often, changes in CLOs issued last year were to speed up the issuance process, mainly to mitigate the risk of portfolio assets being downgraded, which would make it difficult for the CLO to meet effective-date requirements as per the transaction documents (see "S&P Adds Transparency To Its Effective Date Process For CLOs," published April 20, 2015).

Traditionally, for a CLO to become effective, the transaction documents stipulated several tests, among them the extent of exposure to assets rated in the ‘CCC’ category. Some of the recent CLO transaction documents do not include such requirements or tests. In a nutshell, this means that a CLO can become effective irrespective of the exposure to ‘CCC’ rated assets in the pool.

Since several corporate entities were downgraded or had ratings placed on CreditWatch negative in 2020, this increased the possibility of an effective-date rating event. Removing this requirement from the documentation was a way for transactions to become effective even if they would have failed the ‘CCC’ test. These features were more common with resets than new issues. From a rating perspective, the 'CCC' exposure is already captured in our CDO Monitor (see "All You Need To Know About CDO Monitor," published March 24, 2020); hence there is less reliance on whether such a test is applicable or not.

Various portfolio tests/buckets required to be met by the portfolio manager serve as a speed bump for CLOs. A failing test/bucket could signify deteriorating health of the CLO, forcing portfolio managers to typically divert excess interest income to principal investments or pay down the notes to cure a failed test. Traditionally, these tests looked at various risk parameters independent of rating agency inputs. For example, if an asset was rated ‘D’ (default) but another agency gave it a higher rating, the portfolio manager would be required to check whether this asset was indeed in default (irrespective of the rating agency outcome), which is not the case for some recent CLOs.

Recently, CLO managers have proposed the removal of the minimum loan bucket requirement, which is typically 70% of the CLO pool. This could allow CLOs to hold larger bond buckets than was previously the case.

Although European CLOs have some exposure to bonds already, it is possible that the removal of this requirement could benefit the high-yield market. At the same time, it may result in CLOs more closely resembling a collateralized bond obligation.

Since last year, we have also seen larger ‘CCC’ buckets proposed in CLOs, and changes to current pay buckets. Additionally, we note that some CLOs have featured higher exposure to obligor and industry concentration. In some instances, CLO documents have also proposed having no concentration limits at all for industries, meaning that a CLO portfolio could, for example, have high exposure to certain industries.

Arrangers have also proposed new ways to calculate these portfolio limits, such as excluding some loans in the pool when exceeding the target par of the CLO, or carrying defaults at par, which could make this test less effective from a ratings perspective.

One of the most significant changes introduced to European CLO documentation in 2020 is the flexibility to buy distressed assets. We believe portfolio managers were preparing transactions with the ability to respond to more challenging conditions and adapt to the changing marketplace.

Historically, CLO documentation limited CLOs' ability to participate in loan restructurings involving the injection of new money. This restriction allowed non-CLO, distressed-debt investors to extract value from CLOs through certain restructuring practices (see "Acosta Inc.'s Modern Day Bankruptcy: A CLO-Distressed Funds Clash," published May 7, 2020). The introduction of loss mitigation obligations (LMOs) aimed to lessen this risk and help CLOs maximize recoveries on distressed credits (please watch the webcast "CLOs Simplified - Episode 4: Loss Mitigation Obligations and Distressed Asset Flexibility In CLOs" posted March 10, 2021).

While the overall objective of LMOs appears positive, it can also erode a portfolio's par value, since additional funds will be placed with an entity that is already under distress or in default. In addition, using funds to purchase LMOs, rather than to deleverage, would increase the share of nonperforming assets in the portfolio and the weighted-average life of the CLO notes.

The concept of LMOs in CLOs has been changing since they started appearing in European CLO documents, leading to a new scenario that raises potential concerns. In certain instances, for example, it is now possible for an LMO (once it is a non-defaulted asset) to be sold to a CLO at the fair market price, subject to certain conditions being met. In the first transactions where such a feature was available, the portfolio manager could not self-mark the asset. However, in more recent transactions, that restriction has been removed.

Unlike CLOs issued before the pandemic, new CLOs now have two additional concepts for exchanging assets in their portfolios, without formally meeting the traditional reinvestment criteria. A defaulted asset can be exchanged for another debt obligation, which could be either a defaulted asset or a performing asset, as long as--based on the portfolio manager’s judgment--it is better for the CLO (either in terms of credit quality or recovery). Similarly, the portfolio manager can exchange a distressed asset for another performing asset.

If the portfolio manager makes the correct selection, the CLO will benefit from a higher par, meaning better protection for noteholders. On the flipside, this could postpone the risk of crystalizing losses in a scenario where the portfolio manager makes the wrong decision. Because the market value of CLOs may change over time, other anomalies associated with such reinvestments may also arise, since there could be a delay in receiving the ultimate principal on the notes.

Via these types of reinvestments, a CLO could continue reinvesting defaulted assets, especially in the instrument's amortization phase. This could increase the ultimate payment on the rated debt because, traditionally, this money could only be used to redeem notes.

The portfolio manager may continue to receive fees for managing these assets, which may or may not have been factored into the ultimate recovery value of the CLO notes.

CLO documents now allow portfolio managers to reclassify assets (to which we give full par credit in our ratings analysis) as a collateral enhancement obligation, typically carried at zero value. Such reclassification is typically made when the asset no longer satisfies the eligibility criteria in CLO documentation.

Historically, the satisfaction of eligibility criteria was only tested when the asset is first introduced to the CLO portfolio. Some CLO documents now allow this test to be carried out at any time during the CLO’s life, as long as the CLO has exposure to that asset.

The CLO documents also allow the portfolio manager to use money in collateral enhancement or supplemental reserve accounts to pay the market value of the asset to the CLO, and keep this ineligible collateral within the CLO for the benefit of junior subordinated notes. This could benefit the CLO because exposure to an ineligible collateral instrument is excluded from various tests the CLO has to manage, such as the collateral quality, portfolio profile, and coverage tests. However, the CLO only receives the market value of that asset instead of the principal balance, which erodes its par value.

Interest on all CLO notes we currently rate in Europe is paid quarterly; that is, until a frequency switch event (FSE) occurs. If a significant portion of assets start paying interest semi-annually or annually, there may be insufficient interest income to make quarterly interest payments on the notes.

To mitigate the effects of any such timing mismatch, before an FSE, the issuer is typically required to hold back a portion of the interest received on assets that pay interest less frequently than quarterly, so as to make quarterly payments of interest on the notes (so-called interest smoothing).

Traditionally, CLO documents typically had a free 5% allowance above which the portfolio manager was required to trap 50% of interest received from semi-annual or annual assets into the interest-smoothing accounts for the next payment date. Recent CLOs have amended these requirements. In some CLOs, as long as interest coverage of the most-junior rated tranche exceeds 140%, and the CLO passes the par coverage tests, then the portfolio manager does not need to hold back any interest for upcoming payment dates. This decision would rely on the portfolio manager’s judgment on how the asset pool is behaving in terms of default expectations, trading, and interest payments from other assets. These limits continue to evolve where some CLO documents propose to reduce the trapped amount to 40% from 50%.

Through their experienced teams and active management of portfolios, CLO managers have over the past two decades contributed toward the success of this asset class, with less than 0.5% of tranches defaulting.

More recent CLO issuance documents show increasing reliance on portfolio managers’ ability to make the right call, at the right time, and avoid losses for CLOs. Determining bankruptcy exchange, distress exchange, the use of LMOs, default definitions, current pay, and using money from the interest-smoothing accounts are some of the areas where the portfolio manager’s judgment is relied upon.

More recently, we have also seen proposals relying on portfolio managers’ judgment for using cash in accounts for various purchases, as long as the portfolio manager deems that the CLO can generate sufficient money to pay all of the transaction expenses (including interest on the rated debt) at the end of the quarter.

As innovative proposals emerge in CLO documents that could be seen as more equity friendly, newer measures are also being introduced to protect CLO debt investors.

For rated debtholders, preserving the principal in CLO assets has always been of paramount importance. However, to please equity investors, CLOs have traditionally allowed a small percentage of principal to be leaked to equity (typically restricted to 1%). Recently, CLOs have also allowed trading gains to go to equity investors, without the money flowing through the waterfall. This may also add a dimension of incentives misalignment, since the equity holder may receive payments earlier, irrespective of the CLO's ultimate performance.

To address this risk, some CLOs require the portfolio manager to also measure credit risk before transferring principal out of the CLO pool. Some CLOs also require the release or sale of all LMOs that were bought using principal proceeds, and only then is the excess gain allowed to be moved out. Some CLO documentation also restricts the transfer of any value from the principal account if the cash balance in the principal account is negative (for example, due to unsettled trades).

Recent CLOs feature reduced portfolio manager fees (senior and junior), which may be viewed as positive for the CLO in terms of excess spread.

Nevertheless, with portfolio managers facing increasing responsibilities and reduced contractual fees, they are likely to rely on incentive fees based on active CLO trading.

More CLO managers are looking at how to incorporate environmental, social, and governance (ESG) factors into their leveraged loan portfolio decisions. However, there is a long way to go.

Leveraged loans from ESG sectors are scarce and there is no standard measure to assess whether a loan belongs to an ESG sector or not. There are no buckets requiring CLO portfolios to include assets from ESG sectors.

Hence, currently, European CLOs are only confined to having a requirement in CLO documents that restricts CLO managers from buying assets relating to any industries that do not comply with ESG requirements.

This appears to be the motto of CLO participants in Europe. Since the beginning of the pandemic, structural features have continued to evolve in response to the challenging environment. We've also seen substantial innovation on the document side, in particular a focus on nonperforming assets, and we expect this will continue.

The resilience of financial markets remains a concern, with real corporate bond yields at record lows and late-cycle behavior apparent in leveraged finance. But with limited signs of inflationary pressures altering the policy calculus, central bank support remains potent and pivotal.

In our view, the trend of more-leveraged structures and pursuit of further flexibility in European CLOs will endure. We foresee investors and other market participants increasingly taking steps to ensure they are fully aware of the evolution of CLO structures.

CLO Spotlight: Redesigning The CLO Blueprint After COVID-19, April 21, 2020

All You Need To Know About CDO Monitor, March 24, 2020

S&P Adds Transparency To Its Effective Date Process For CLOs, April 20, 2015