Feb. 08, 2022

This report does not constitute a rating action

Primary Credit Analyst

Olen Honeyman New York + 1-212-438-4031

Secondary Credit Analysts

Steve H Wilkinson, CFA New York + 1-212-438-5093

Minesh Patel, CFA New York + 1 -212-438-6410

Analytical Manager

Ramki Muthukrishnan New York +1-212-438-1384

Research Assistant

Salvatore Gummo New York

Media Contact

Jeff Sexton New York + 1-212-438-3448

EBITDA addbacks remain on an upward trend, with addbacks for deals originated in 2020 representing 31% of management projected EBITDA, and over 66% of last-12-month reported EBITDA in our sample of large mergers and acquisitions and leveraged buyout transactions.

Our analysis continues to confirm that marketing EBITDA (including addbacks) generally does not provide a realistic indication of future EBITDA and that companies also consistently overestimate debt repayment.

Together, these effects meaningfully understate actual future leverage and credit risk, and contribute to incremental event risk, as many covenant baskets are tied to EBITDA.

Actual leverage continues to fall significantly short of management projections (from deal inception). The 2018 cohort of deals, added in this report, on average, reported actual net leverage of 4.6 turns and 3.5 turns higher than that forecasted for 2019 and 2020, respectively.

Aggressive earnings projections were the principal culprit in the large leverage misses, with reported EBITDA coming in at 36% below marketing EBITDA in 2019 and below 39% in 2020.

S&P Global Ratings' fourth annual analysis of EBITDA addbacks finds most U.S. speculative-grade corporate issuers continuing to be unable to achieve the earnings, debt, and leverage projections presented in their marketing materials at deal inception. Of particular interest was whether EBITDA adjustments were an accurate picture of future earnings, with the answer remaining a resounding no. (Our recent analysis of EBITDA addbacks is also the subject of episode 19 of The Upgrades podcast, on spglobal.com.)

Our updated analysis consists of two main components:

While the findings herein are reminder of the perils of "buying in" to overly optimistic management forecasts, our ratings are based on our projections of a company's expected earnings, their capacity and appetite for debt repayment, and our view of issues like management projected synergies or cost efficiencies.

Over the past six years, most U.S. issuers that were assigned a speculative-grade rating were initially rated in the 'B' category (B+/B/B-). If we took the marketing leverage presented to us and rated to pro forma addbacks, projected earnings, and debt reduction, our initial issuer credit ratings would undoubtedly be higher, forcing us to lower our ratings as actual results are reported. All told, marketing leverage and the language around addbacks--as defined in debt agreements--are not determinants of our view of credit risk (other than in assessing covenant headroom when reviewing debt instruments containing financial maintenance covenants).

S&P Global Ratings defines EBITDA as revenue minus operating expenses plus depreciation and amortization (including noncurrent asset impairment and impairment reversals). This definition generally adheres to what EBITDA stands for: earnings before interest, taxes, depreciation, and amortization. However, it excludes other income-statement activities that we view as nonoperating. We exclude adjustments for items like management fees and restructuring costs. We include cash dividends received from investments accounted for under the equity method and exclude the company's share of these investees' profits.

We often give some credit to addbacks or synergies that we view as achievable, especially when a company--or a particular sponsor--has demonstrated such ability in past comparable transactions. Even then, we allocate this credit only during periods when we expect the benefits to be achieved, rather than baking these factors into pro forma metrics as is the convention with marketing EBITDA. Further, we are almost always considerably less optimistic than management regarding some aspects of future growth, such as realizable revenue and cost synergies, and our projections reflect that. Our analysis goes much deeper than EBITDA and examines issuers' true cash-flow characteristics.

Do addbacks present a more realistic picture of future profitability and risk, and do companies typically hit their forecast?

Deal arrangers, sponsors, and management teams continue to raise the aspirational bar in selling what qualifies as an addback. This increases the number, types, and ultimately the magnitude of adjustments. In many of these cases, S&P Global Ratings views the ever-expanding definition of management-adjusted EBITDA as an artificial deflation of leverage and an inflation of profitability that contributes to understated valuation multiples.

For example, what is the true leverage of a company with last-12-month (LTM) reported EBITDA of $50 million, management-adjusted EBITDA of $200 million, and pro forma debt of $1 billion? The absence of a standardized definition of EBITDA is the critical issue here. In practice, it is and has always been a negotiated definition, varying from agreement to agreement.

Summary of findings

In this study, we found yet again that both anticipated EBITDA and deleveraging efforts fell materially short of issuer projections for the two years that we tracked companies' performance after transaction origination (see Table 1).

We repeated the performance gap analysis for M&A and LBO transactions originated in 2015, 2016, and 2017, along with 2018 that we reviewed this year. Our analysis of the 2018 cohort showed that the magnitude of the misses increased significantly vs. the 2017 cohort on an average and median basis.

For the 2018 cohort of deals, about 70% of the companies missed their EBITDA targets by at least 25% in the following two years (significantly worse than the prior year, where misses greater than 25% were about 55% in the two years following origination). The median miss on earnings over years one and two were 38% and 39%, respectively, the highest miss in the four years of our study. We chose median metrics for comparison because we observed a fair amount of variation within in each cohort and across the four sets of cohorts.

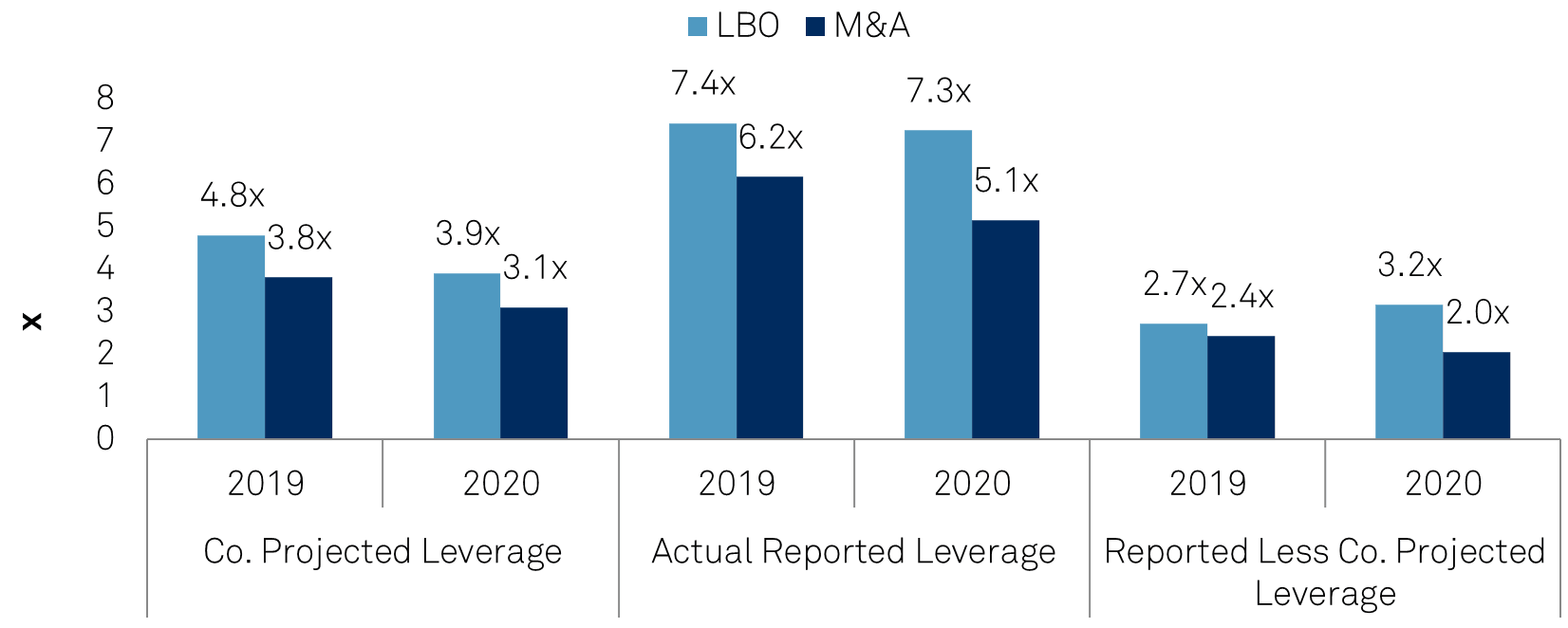

Table 1 | Transactions Originated In 2018 Company Projected Vs. Net Reported

*Company's projections are adjusted EBITDA. **Leverage calculation based on average of debt to EBITDA of each company in sample.

Table 2 | Transactions Originated In 2017 Company Projected Vs. Net Reported

Table 3 | Transactions Originated In 2016 Company Projected Vs. Net Reported

Table 4 | Transactions Originated In 2015 Company Projected Vs. Net Reported

To assess the validity and achievability of addbacks, we compared marketing EBITDA presented at deal inception with the actual reported EBTIDA. We compared the aggregate level, given the difficulty in evaluating the various individual components of addbacks. For example, a company often does not disclose the actual achievement of a particular type of cost savings in its financials. Further, in the current predominantly covenant-lite loan environment, we do not benefit from compliance certificates that can provide detail on addback realization. We include two years of actual performance data--allowing time to gauge whether the company could achieve anticipated synergies--to permit certain addbacks to roll off.

Further, just like our earlier three reviews, we eliminated companies that underwent a material M&A or LBO transaction after the initial transaction (for example, a subsequent sponsor-to-sponsor LBO in Year T+2). This enabled us to remove distortion following transformative events (new debt issuance, earnings colored by subsequent acquisitions, etc.), rendering initial projections irrelevant. It also lets us cleanly track the reported EBITDA, debt, and leverage versus what was projected by these companies.

Because management projections are confidential, we cannot disclose any company names.

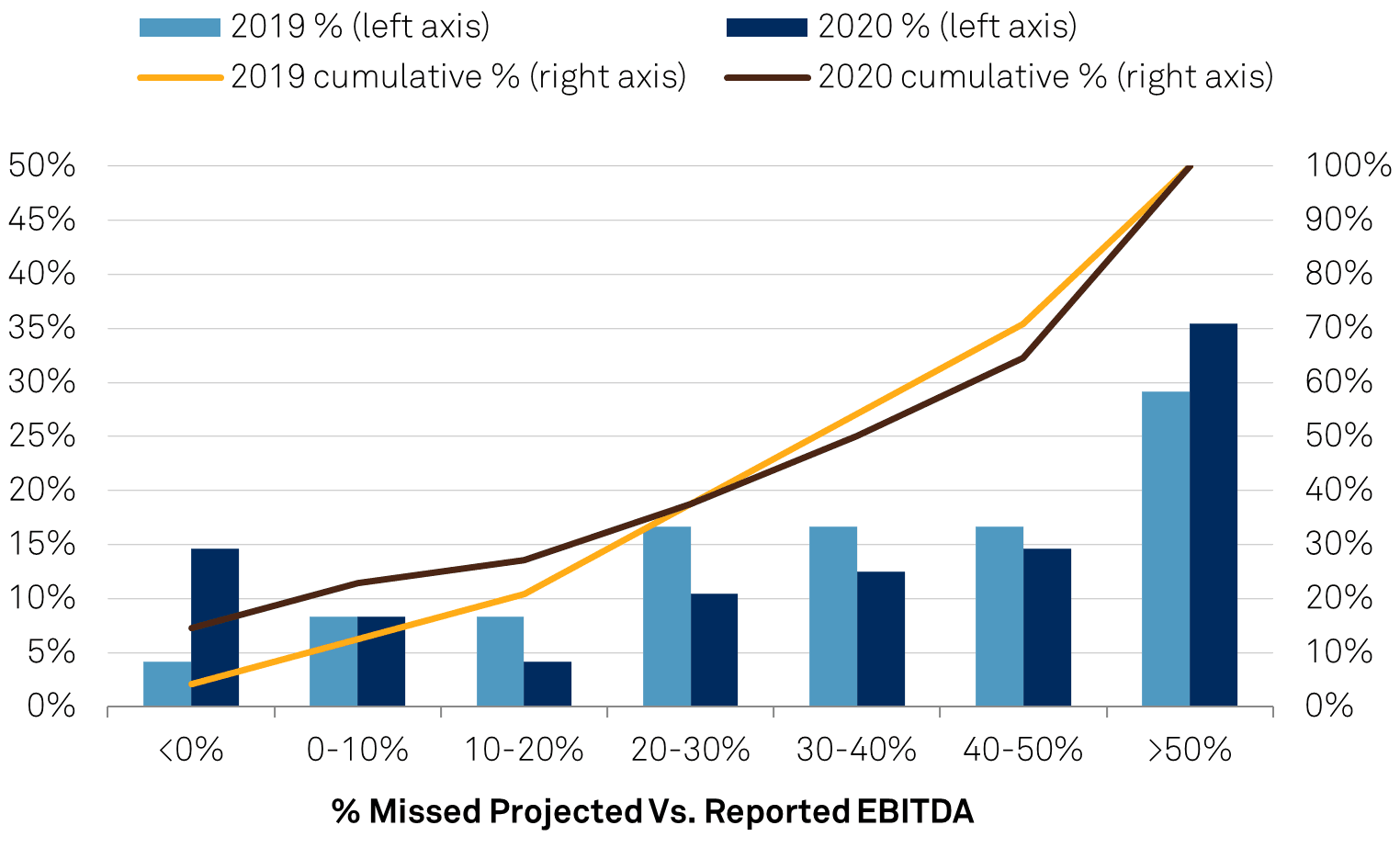

As opposed to seeing a convergence between management's projected and reported EBITDA, which one would expect to see if companies realize their anticipated earnings and one-time items fall away and synergies were achieved, we saw a material divergence. Moreover, this divergence grew between years one and two in all cohorts except for 2017, when the median miss improved to 30% in year two from 32% in year one. The deviation indicates unmaterialized growth projections, operating challenges, and unrealized synergies or unattained cost savings. The 2018 cohort had the highest median miss in year two (2020) since the 2015 cohort at 39%. The pandemic-induced recession was undoubtedly a contributing factor in the magnitude of the miss in 2020.

Chart 1 | EBITDA Divergence

S&P Global Ratings.

Table 5 | Company Projected Versus Actual Reported EBITDA

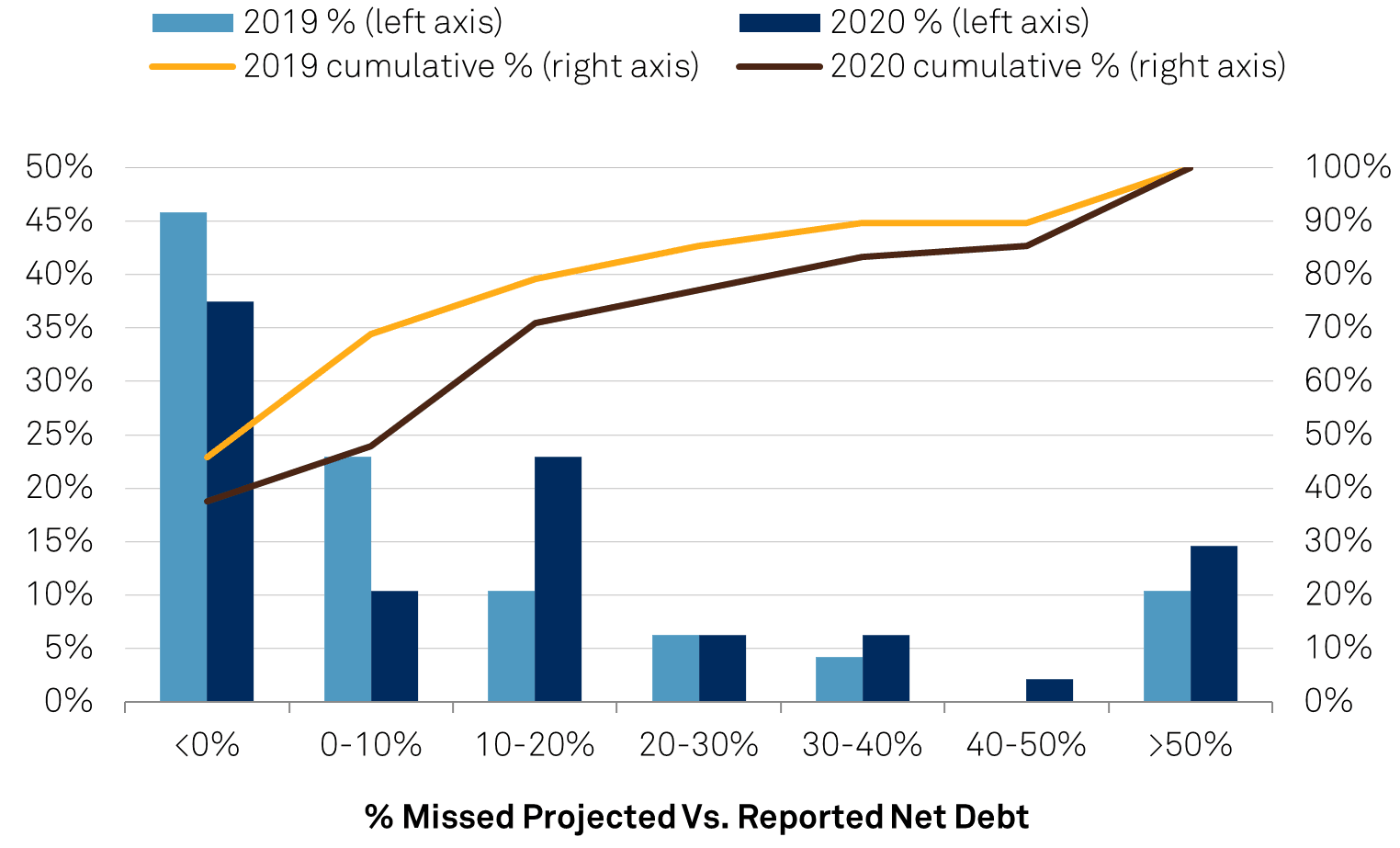

Failure to meet projected debt levels also contributed to the significant miss of managements' projected leverage, but to a much lesser extent than EBITDA misses. Virtually all issuers present a deleveraging story to the market at deal inception, stating intentions to sweep surplus cash to reduce debt in management projections.

Ironically, most issuers contend that their forecasts are conservative during management presentations before deal launch. However, the 2018 cohort did a lot better and showed significant improvement over the prior two years with a median miss of 2% in year one, growing to 11% in year two following origination (see Table 5). This compares to 11% and 25%, respectively, for the 2017 cohort, 3% and 11% for the 2016 cohort, and 1% and 12% for deals printed in 2015.

In short, companies' intentions to apply surplus cash to pay down debt appear to be infrequently executed. Indeed, companies rarely, if ever, pay down debt to the extent indicated. All four vintages displayed a similar pattern: roughly two-thirds of companies kept debt levels in check (exceeded or within 10% of their targets for projected debt) in the first year following origination.

That share quickly deteriorated to an average of 45% by the end of the second year across all cohorts. We netted reported cash balances against reported debt to compute both debt and leverage divergence for comparability.

Chart 2 | Net Debt Divergence

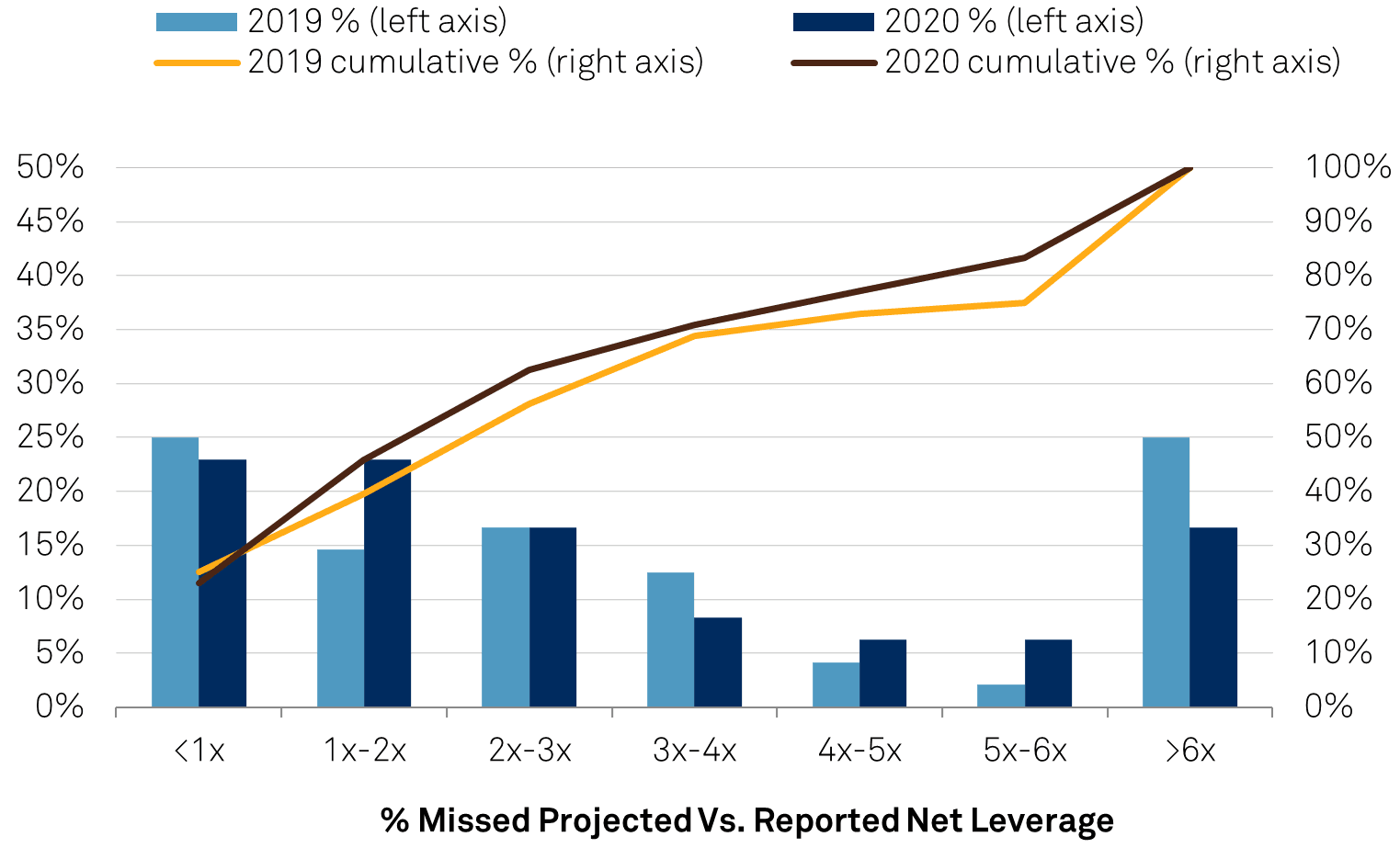

As a result, there is a material discrepancy between projected and reported leverage across the aggregate data set. We see a company's projections become increasingly aspirational on both ends, building a significant leverage cushion and presenting a case that does not necessarily represent credit realities.

By averaging the median gap across the four vintages, companies under-projected leverage by

an average of over two turns (2.3x) in the first year, increasing to 2.9 turns by the end of year two (see Table 6).

Table 6 | Company Projected Versus Actual Reported Net Debt

Chart 3 | Leverage Divergence

Table 7 | Company Projected Versus Actual Reported Net Leverage

While the table above shows improvement year over year (YOY) for the 2018 cohort with the leverage miss improving in 2020, our leverage calculations are based on net debt. When looking at reported (gross) debt figures for the 2018 cohort, the average projected debt miss went from 17% in 2019 to 73% in 2020 compared to 19% and 35% for the 2017 cohort. We believe this is due partly to COVID-related cash hoarding during the last the three quarters of 2020.

The data set for this part of our review is larger, encompassing 449 M&A and LBO transactions originated between 2015 and 2020 with deal sizes exceeding $50 million. It includes S&P Global Ratings-rated transactions and is limited to those where management provided us with a detailed bridge from reported EBITDA to marketing EBITDA (as is typically the case).

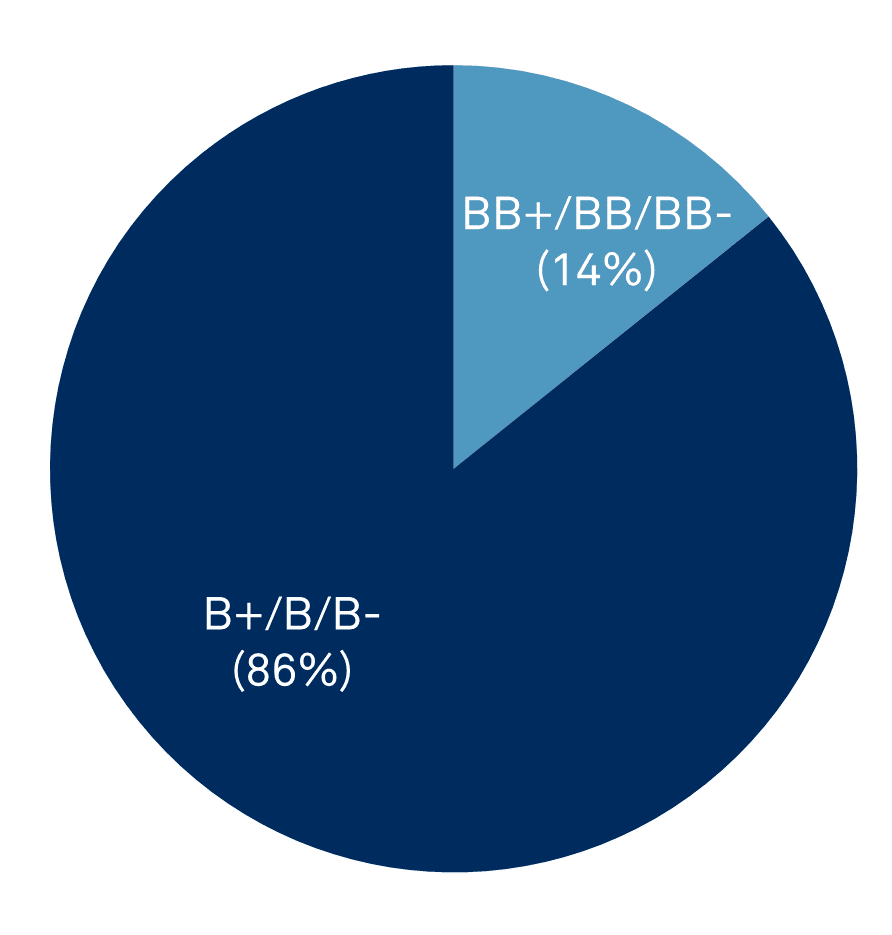

The breakdown of this sample contains 261 M&A transactions and 188 LBO transactions; of the total, 86% by deal count were rated in the 'B' category at inception, with the remaining 14% in the 'BB' rating category.

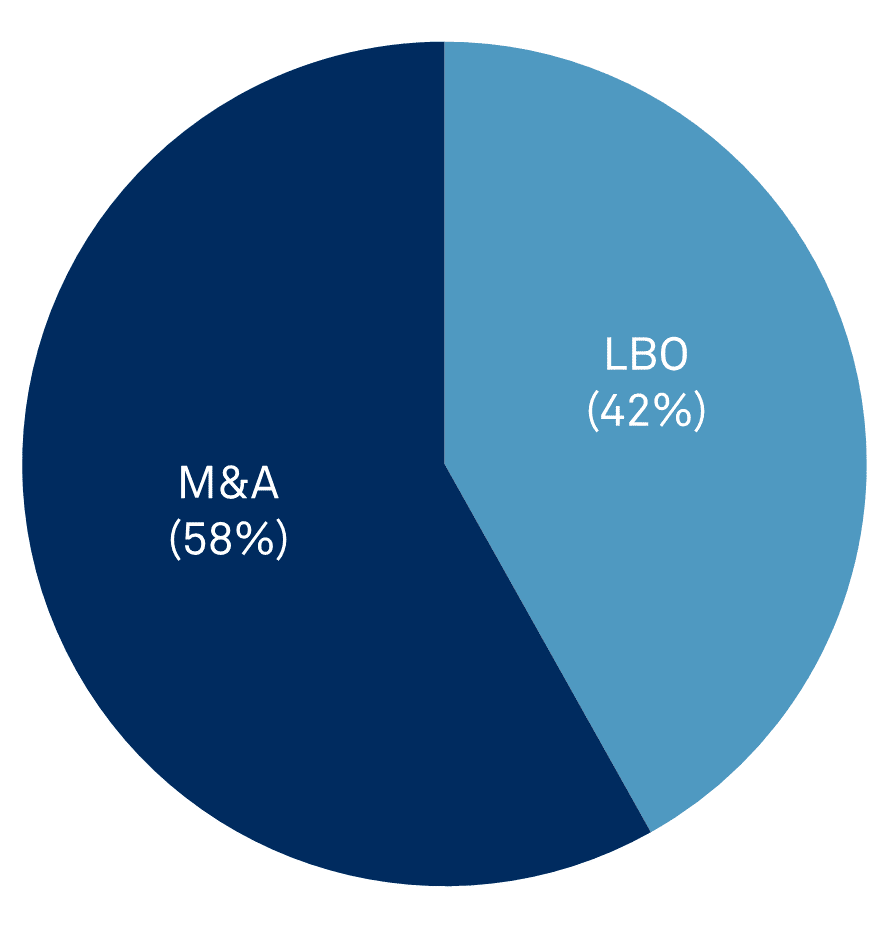

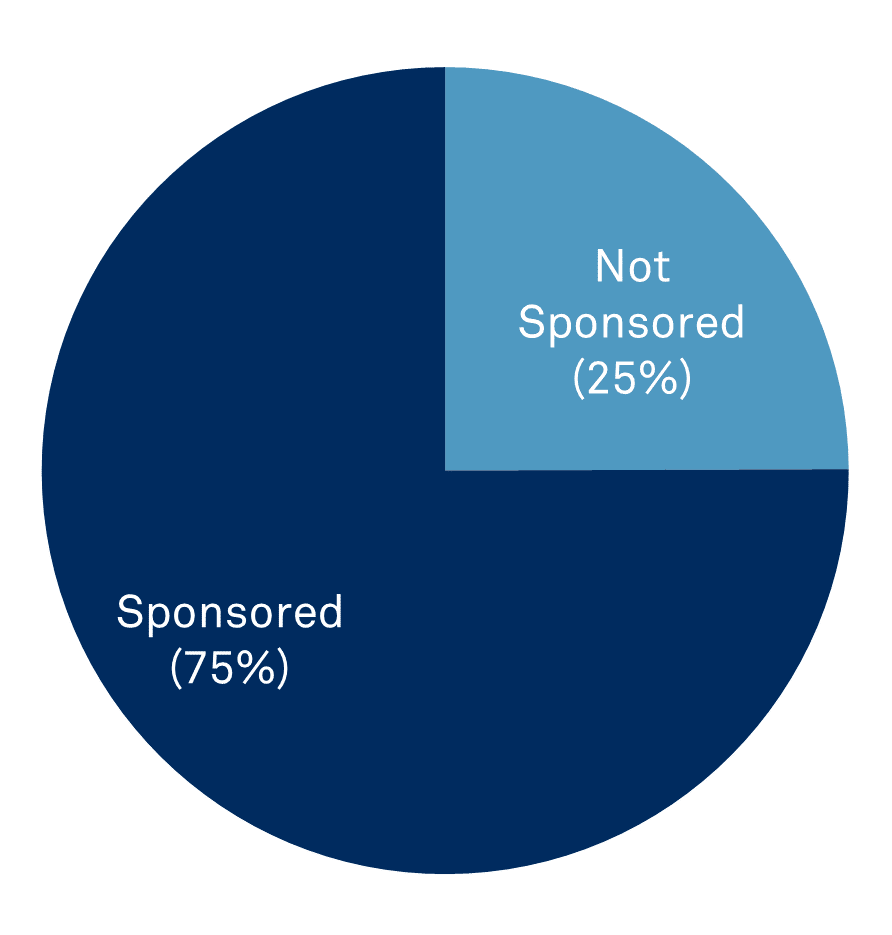

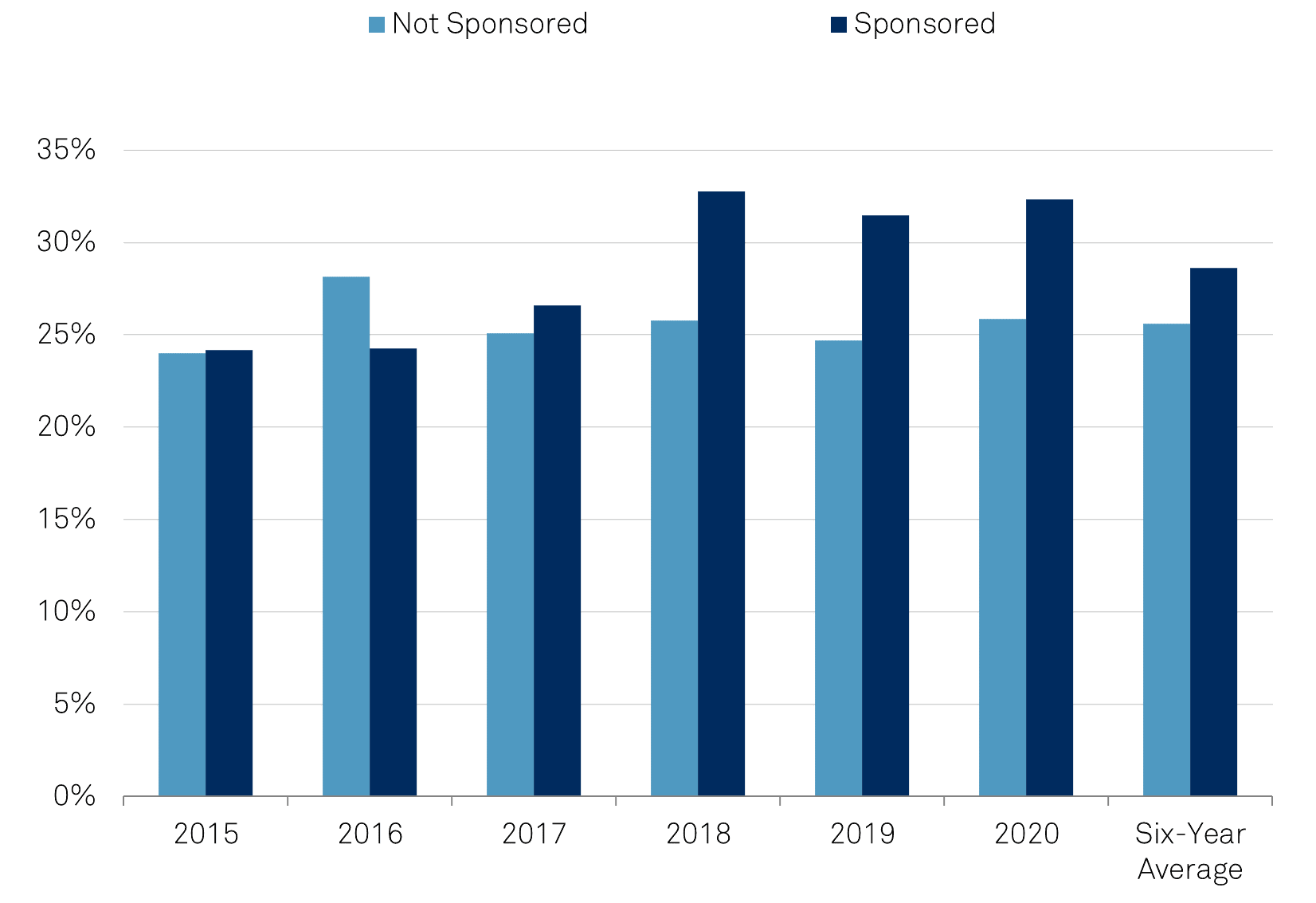

With the expansion of the data set to include a new cohort, the proportionate share of 'B' category ratings continues to grow, reflecting the erosion of credit quality in the broader leveraged finance market. Three-quarters of the transactions in the sample were sponsored, and the breakdown between LBO and M&A transactions is 42% and 58%, respectively.

Chart 4A | Breakdown Of Data Sample By Transaction Type

Chart 4B | Breakdown Of Data Sample By Initial Issuer Credit Rating

Chart 4C | Breakdown Of Data Sample By Sponsorship Status

We measured the magnitude of addbacks both as a percentage of management's marketing EBITDA and pro forma LTM EBITDA excluding any addbacks, both as presented at transaction inception.

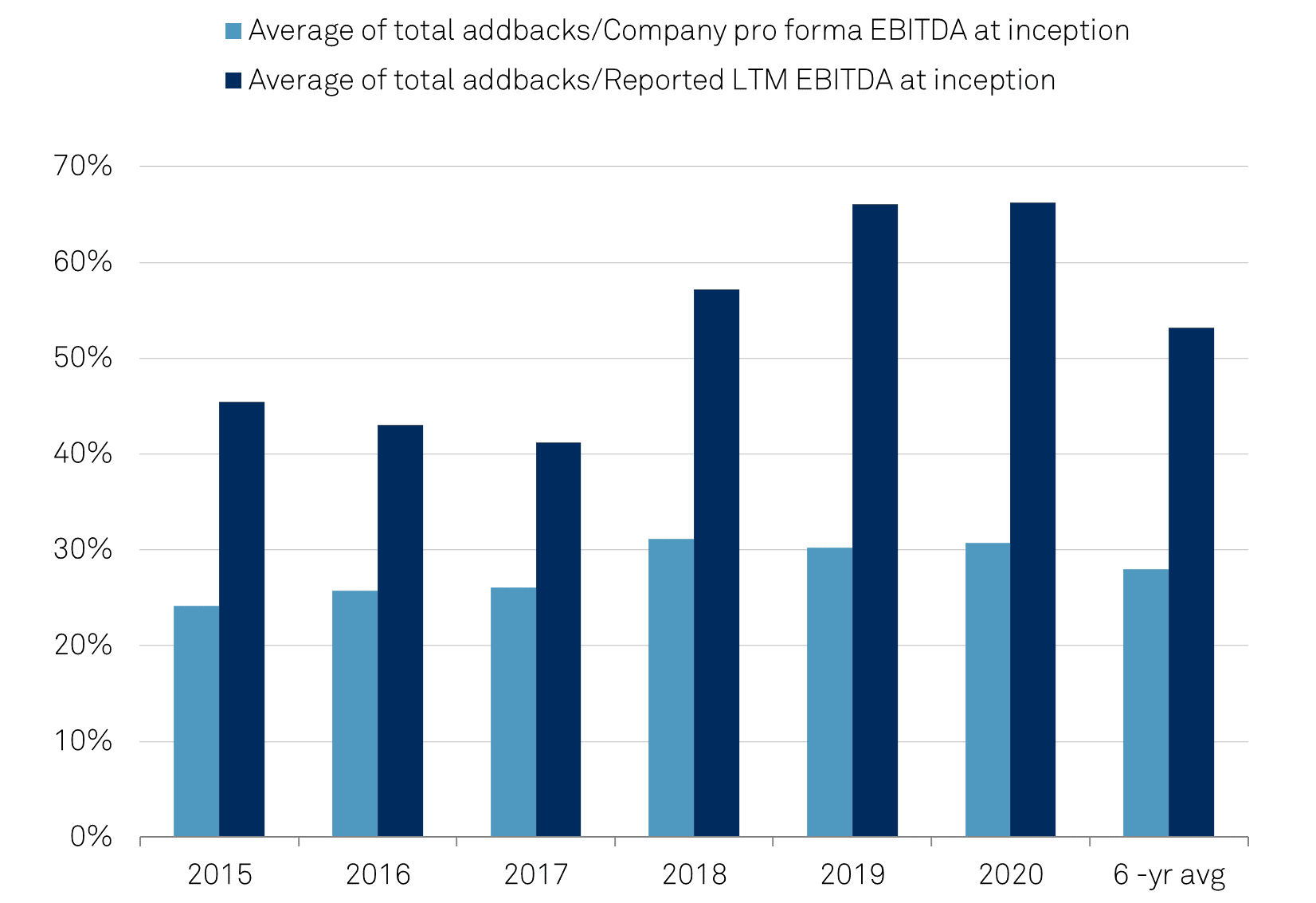

On average over the past six years, addbacks made up over 28% of marketing EBITDA and over 53% of LTM reported EBITDA (see Chart 5). Over the period, the forward-looking measure (addbacks as a percent of marketing EBITDA) has grown each year marginally, exceeding 30% in 2018 and beyond from 24% in 2015.

Meanwhile, average addbacks as a share of LTM EBITDA declined steadily between 2015 and 2017 before jumping to 57% in 2018 and 66% for both 2019 and 2020. The 2015 average is inflated by its unusually high concentration of small health care and tech companies, which have displayed tendencies toward more aggressive adjustments. In 2015, over half of these companies marketed addbacks outsized to their LTM EBITDA. Excluding these deals, the average addback would have dropped to 29% in 2015.

The surge over the past two years is somewhat expected given the increase in M&A activity, which skewed the backward-looking LTM measures upward and made them out of sync with the post-acquisition business.

Across the six-year sample, a large percentage of the average is weighted toward 'B' rated issuers and has been steadily increasing. We found that regardless of transaction type, 'B' category credits led their higher-rated 'BB' counterparts in the average adjustment amount.

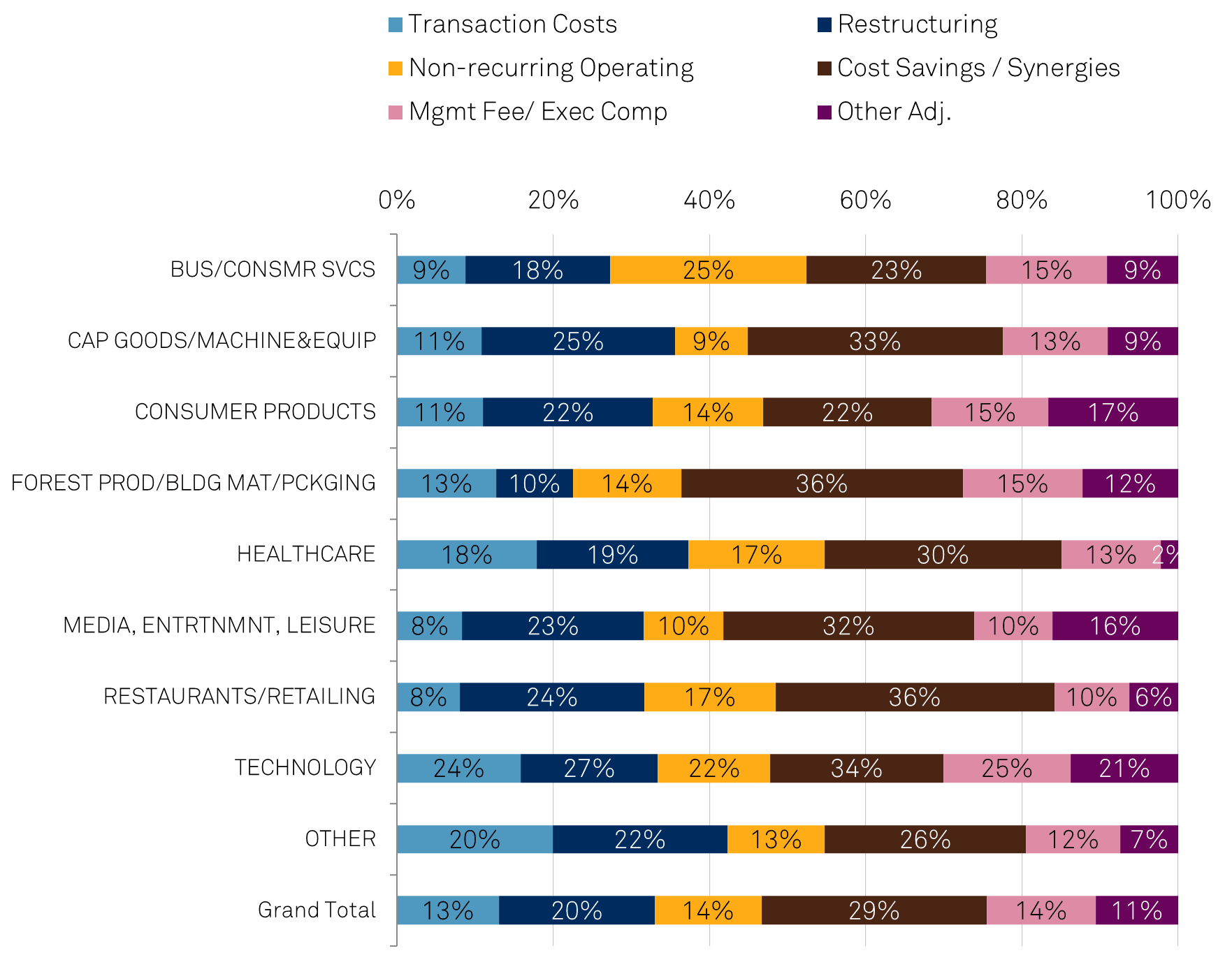

Chart 5 | EBITDA Addback Trends (2015-2020)

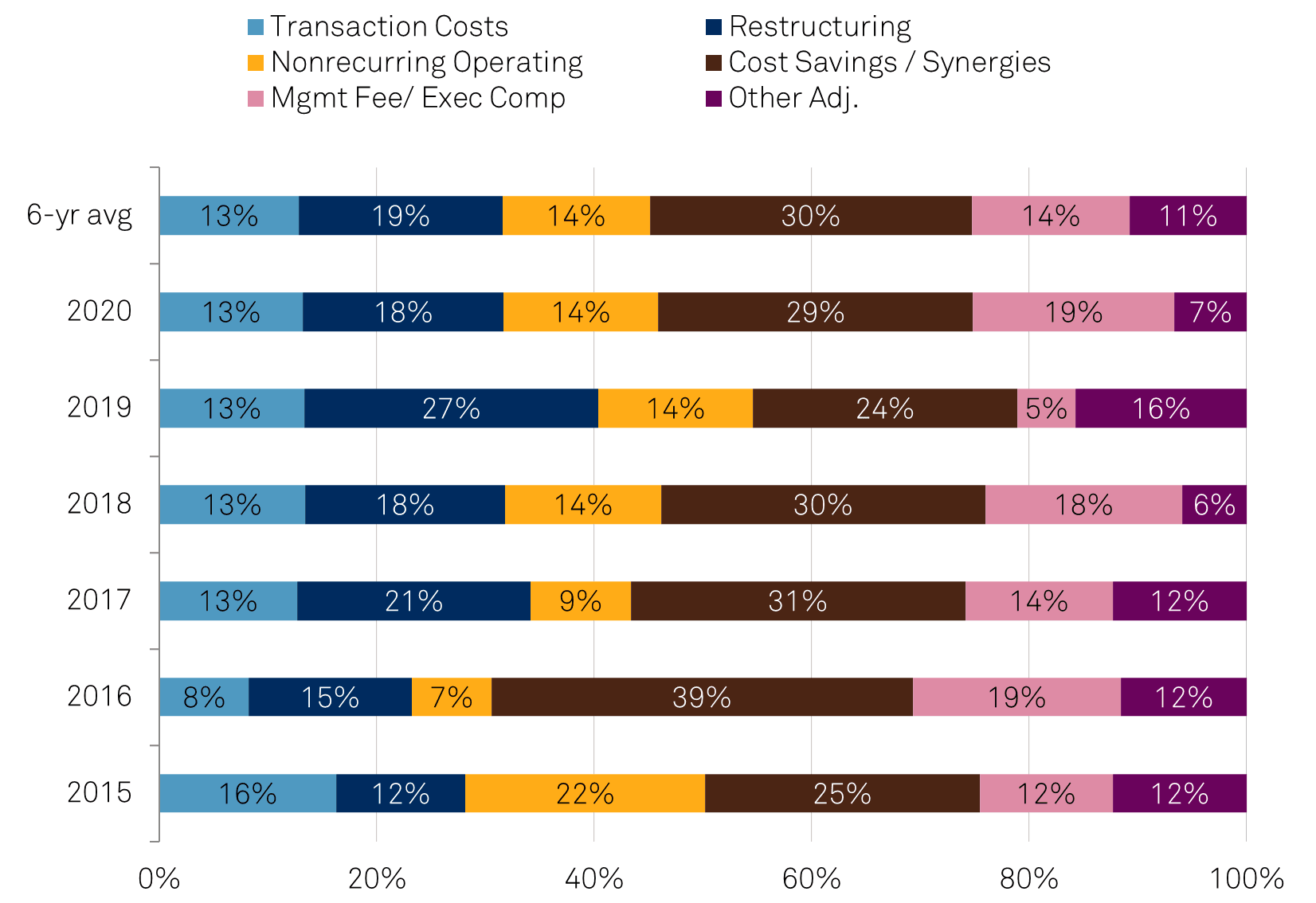

Expected synergies and cost savings continue to be the largest components of add-backs. Chart 7 sorts the general addback adjustments into six broad categories. On average and each year, synergies/cost savings led over other adjustment types. It peaked in 2016 at close to 39%, with a six-year average of 30%. Synergies are often the most difficult of the common addbacks to project accurately.

We rarely factor the full amount of management-anticipated synergies into our projections as mentioned earlier. Instead, we have detailed discussions with management teams and their advisors regarding expected synergies and assess what we believe to be achievable, and when such achievement is likely. It often depends on the source of synergy and, when relevant, whether a company or sponsor has a demonstrated track record in realizing similar synergies or cost savings from past transactions. While some are easier to execute--such as eliminating overlapping corporate overhead to achieve labor savings--others fall outside management's control. Pro forma saving on procurement offers one example: it takes contract negotiations with various third-party vendors. Lastly, some synergies are costly to implement, requiring an upfront expense, such as severance pay.

Restructuring costs are another area of disparity in treatment. We generally treat restructuring charges as operating costs because most companies need to restructure their operations to adapt to changing environments and remain competitive and viable. Similarly, as stated in our approach to EBITDA, management fees constitute a cash operating cost and are treated as such in our analysis. For this reason, we do not add back restructuring costs or management fees in our calculation of adjusted EBITDA. In addition, the consistent body of data demonstrates how far off companies' original assumptions tend to be about the future realization of addbacks.

Chart 6 | Breakdown By Type Of Addback (2015-2020) Avg. % share of total addbacks

Criteria Categorization: Count of less than 19 was categorized in the "Other" sector. S&P Global Ratings.

The telecom, technology, and media/entertainment/leisure sectors had the most addback-inflated EBITDA when comparing the six-year average of total addbacks to company marketing EBITDA at deal inception at 38%, 37%, and 36%, respectively. At the other end of the spectrum, business and consumer (19%), and forest products (18%) had addbacks well below the aggregate sample average of 29%.

Table 8 | Average Addbacks By Sector

Chart 7 | Addback Types By Sector

Table 9 | Addback Types By Transaction Type, Issuer Credit Rating, And Ownership Type

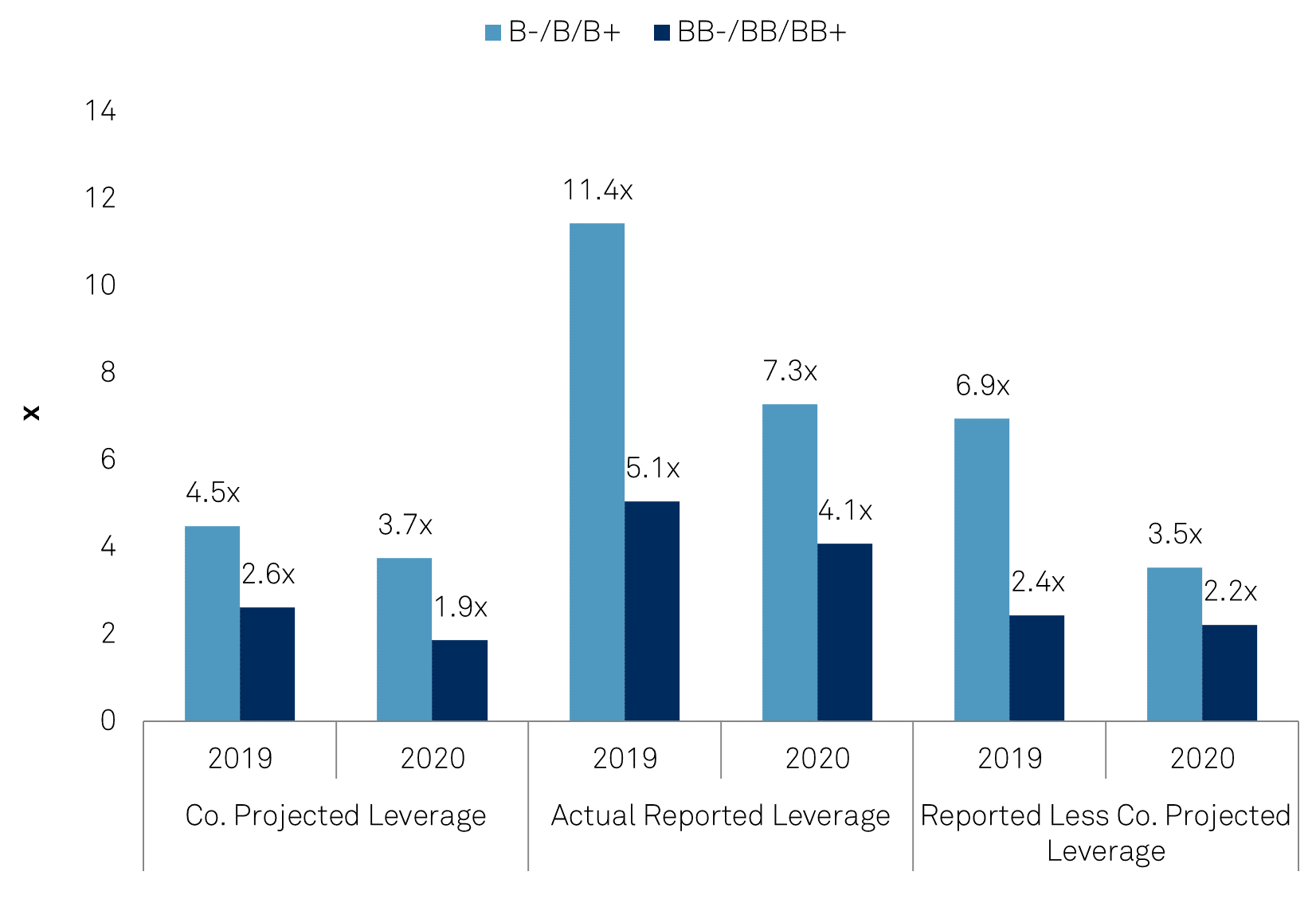

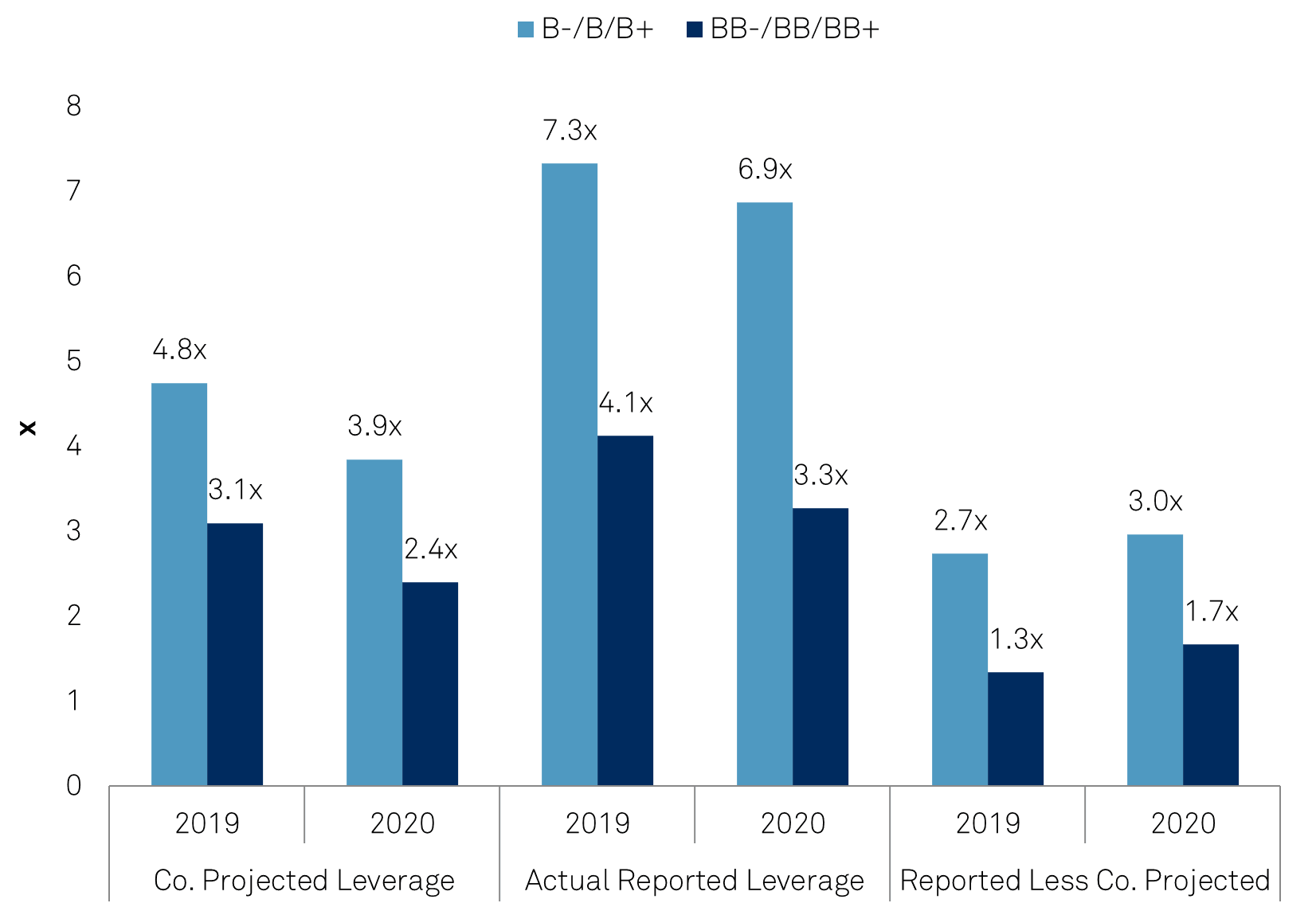

The number of companies rated in the 'B' category continues to increase. These companies have consistently underperformed 'BB' category credits in projecting earnings.

The need for addbacks to make a deal appear attractive to the market is likely lower for 'BB' rated companies because their pro forma leverage is typically lower, so it is possible that the addbacks were less aggressive or aspirational.

In addition, an intuitive view could be that lower-rated credits tend to be smaller and have higher earnings volatility, making projections more difficult. Also, financial sponsor ownership is more common among lower-rated entities than those in the 'BB' category.

Comparing on a median basis 'B' category credits, the reported leverage is 2.7 turns higher than projected in 2019, with the gap widening to 3.0 turns in 2020. 'BB' category credits performed significantly better than 'B' category credits, missing by 1.3 turns in 2019, increasing to 1.7 turns in 2020 This analysis further reinforces the significant credit disparity between 'B' and 'BB' credits.

Table 10 | Average Addbacks By Issuer Credit Rating

Addback/reported

Chart 8 | Average Leverage Divergence ('B' Category Versus 'BB' Category)

Chart 9 | Median Leverage Divergence ('B' Category Versus 'BB' Category)

Consistent with our prior studies, LBO and M&A transactions are comparable in the amount of addbacks as a percentage of marketing EBITDA, at 27% and 30%, respectively. However, the distribution of addbacks differs. As one would expect, M&A transactions showed above-average addbacks for synergies and cost savings as these are often a selling point of the transaction, accounting for about 30% of addbacks versus 27% for LBOs.

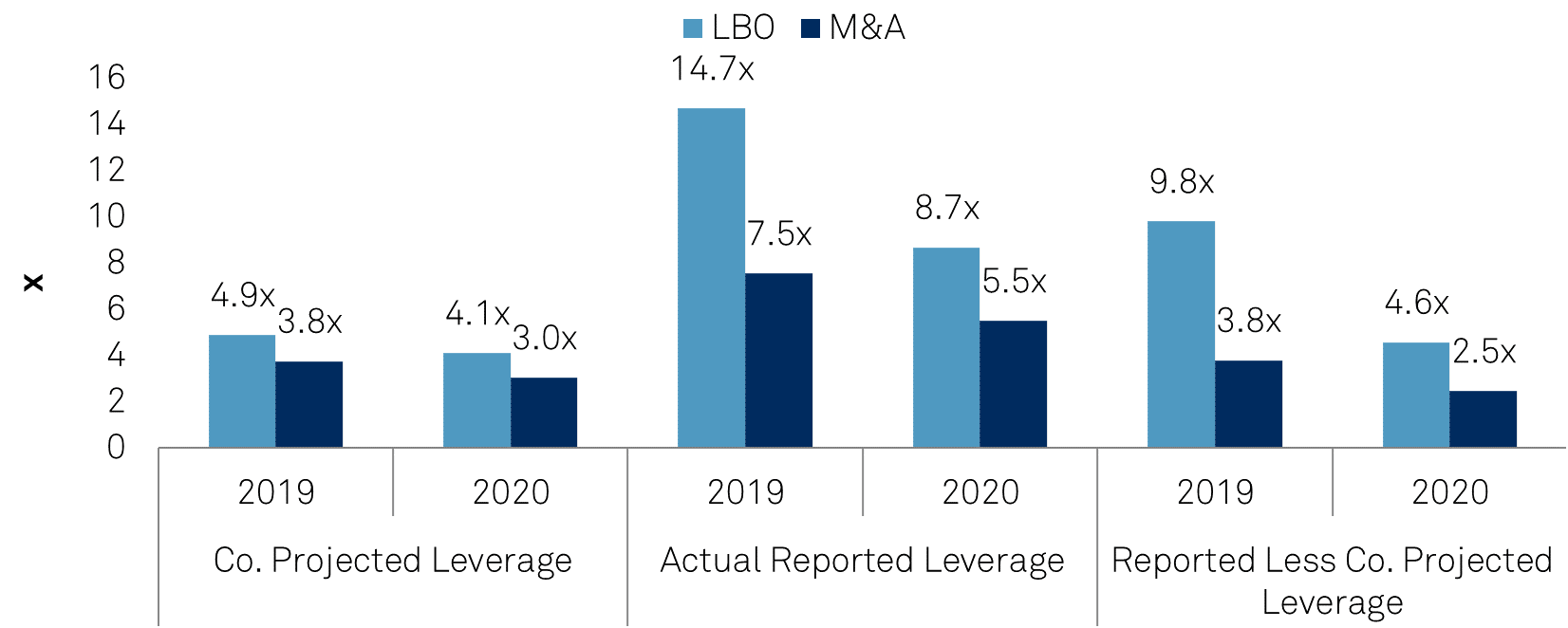

Again reverting to the performance data in part 1 of the study, LBO transactions have consistently underperformed M&A deals in terms of projecting leverage. For the 2016 cohort, there was no pronounced difference in the quality of management projections; both proved unreliable, with the discrepancy between management projected and reported ranging between 2.7-3.6 turns of leverage across both universes.

However, the gap widened materially in the 2017 cohort, with M&A deals missing leverage targets by 2.3 turns in 2018 and 2.6 turns in 2019 compared with LBO deals missing by 3.5 and 4.1 turns, respectively. In our latest cohort, M&A missed by 2.4 turns in 2019, improving to 2.0x in 2020, while LBOs missed by 2.7 turns in 2019, growing to 3.1 turns in 2020.

For comparison, within our financial risk categories, the difference between the mid-points of two different categories (significant and aggressive, for example) is 1.0 turn of leverage.

Table 11 | Average Addbacks By Transaction Type

Chart 10 | Average Leverage Divergence By Transaction Type

Chart 11 | Median Leverage Divergence ('B' Category Versus 'BB' Category)

Our six-year study on the magnitude and composition of addbacks show that sponsored transactions tend to be more aggressive with addbacks versus nonsponsored deals--but not by a significant margin. The six-year average for sponsored deals was 29% versus 26% for nonsponsored. Nonsponsored deals were generally about 25% each year with limited fluctuations.

On the other hand, sponsors padded marketing EBITDA with more adjustments in years 2018 through 2020, all three years in excess of 30%, likely driven by the increase in lower-rated deals given accommodative capital markets. Of the 449 transactions in our data set, 337 were sponsored, 112 were not.

We also noted a large variation by sponsor in terms of their aggressiveness in the use of addbacks. We looked at the 32 sponsors with at least 4 transactions in our data set.

Of those, the 10 most "aggressive" firms accounting for 64 transactions had addbacks averaging 43% of marketing EBITDA. Conversely, the 10 least aggressive sponsors accounting for 68 of the transactions averaged 19%.

Chart 12 | Addback/Marketing EBITDA

Tables 11 and 12 show that sponsored transactions significantly underperformed nonsponsored in the accuracy of their projections at deal inception. For the 2018 cohort, the median leverage miss for sponsored deals in 2019 was 3.0 turns, improving to 2.3 turns in 2020. For nonsponsored deals the median miss was 1.8 turns in 2019 and 1.7 turns in 2020.

Table 12 | Company-Projected Versus Actual Reported Net Leverage (Sponsor-Owned)

Table 13 | Company-Projected Versus Actual Reported Net Leverage (No Sponsor)

Our four cohorts of projection performance data show that EBITDA addbacks at deal inception continue to be substantial and overstated, resulting in understated leverage and purchase price multiples.

Our study led us to several conclusions consistent with our previous studies: