Aug. 26, 2021

This report does not constitute a rating action.

Ramki Muthukrishnan New York +1-212-438-1384

Robert E Schulz, CFA New York +1-212-438 7808

Hanna Zhang New York +1-212-438-8288

Yucheng Zheng New York +1-212-438-4436

Joe Maguire New York +212-438-7507

Pawel Dzielski New York

In terms of both the cause and duration, the credit and financial crisis of 2020 was unlike any other. The pace at which the pandemic-related social and business restrictions hurt the U.S. economy and financial markets was almost matched by the speed at which capital markets rebounded. For example, the weighted average bid of the S&P/LSTA Leveraged Loan Index--an indicator of loan prices--fell to a low of 76.23 in March 2020 from 97.35 in January, but then it rallied back to 91.24 by June 2020 and 97.59 in January 2021, which was the highest since November 2018. Equity markets rallied even faster: The benchmark S&P 500 index regained all of its lost ground by June of last year, finishing 2020 at an all-time high, and it has continued to surge since then.

Against this backdrop, private equity (PE) firms wasted no time ramping up their transactions (LBOs, M&A, refinancings, etc.).

The number of new issue transactions by PE-owned North American companies dropped to 34 in the second quarter of 2020, less than one-third of the 109 a year earlier, according to S&P Global Leveraged Commentary & Data (LCD). But by fourth-quarter 2020, the number of PE-backed transactions had rebounded to 105, a large portion of which was driven by resurgent M&A.

There were 44 North American sponsor-backed M&A transactions (including LBOs) in the first quarter of 2020, according to LCD. By March, when the pandemic was in full swing, deals were shelved or abandoned altogether, and PE firms focused on preserving their portfolio companies’ liquidity.

Companies in consumer-facing sectors--such as restaurants, retail, and travel and hospitality--were hit the hardest, and efforts were directed to keep these entities afloat, including negotiating covenant amendments and injecting funding (see “Changing Times Have Led To New Trends In Amendments To U.S. Middle-Market Credit Agreements," Aug. 24, 2020).

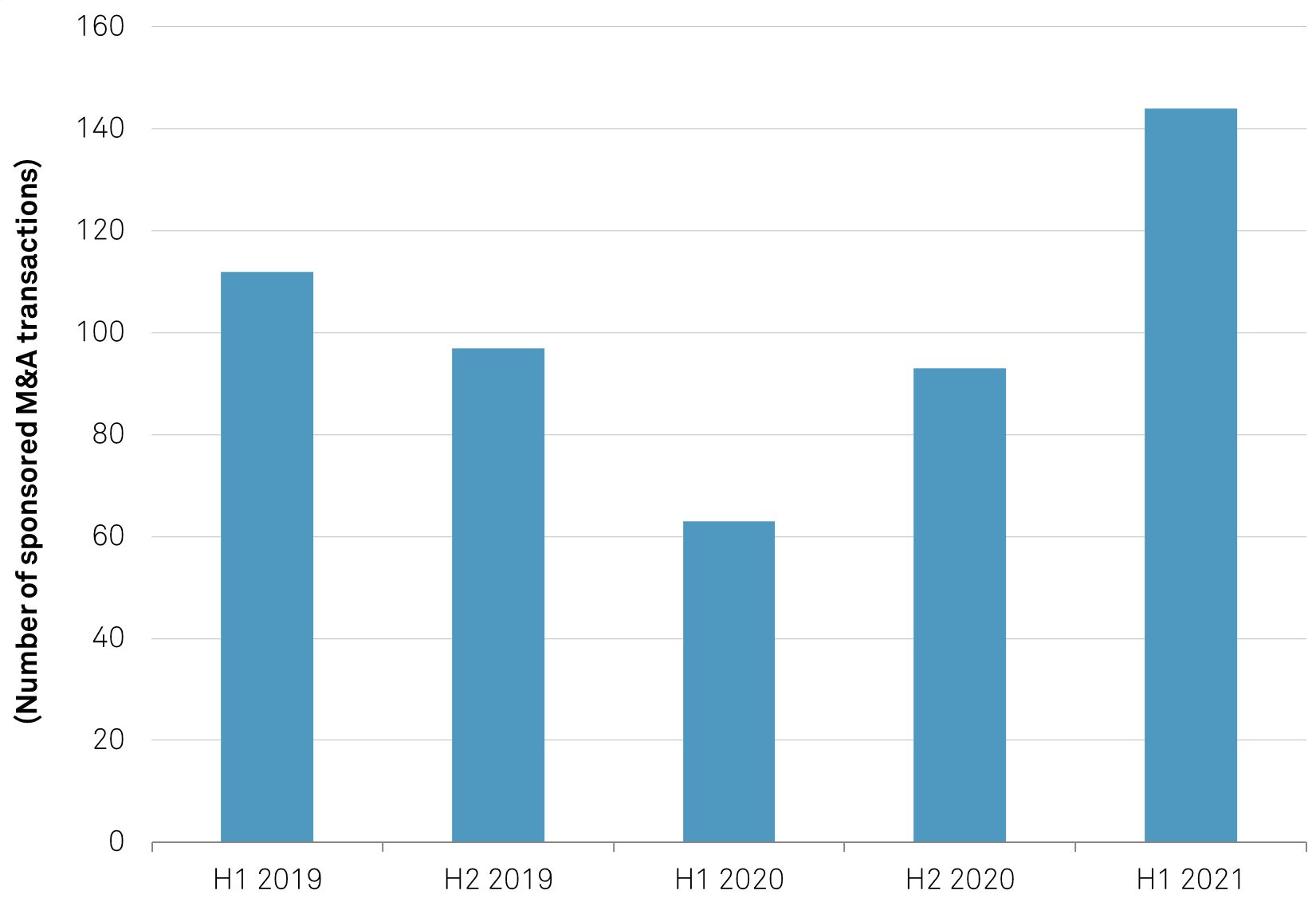

In the second quarter, as markets were navigating the uncertainty, 19 M&A deals were completed. This brought the number of sponsor-backed M&A issuances in the first half of 2020 to 63, down from 112 for the same period in 2019. However, in the second half of last year, after Federal Reserve’s massive intervention via a variety of programs to bolster liquidity, the markets opened with renewed vigor. A total of 93 sponsor-backed M&A transactions were done in the second half, pushing the 2020 total to 156. And there were a record 144 in the first half of 2021.

Chart 1 | M&A Activity Reached A Record High In The First Half Of 2021

Source: S&P Global Ratings, and LCD, an offering of S&P Capital IQ Pro.

In our view, the soaring popularity of M&A transactions stemmed from three related factors:

The historically low interest rates that have persisted for several years have attracted new investors into the private equity and private credit markets, and they’ve also enticed existing investors to significantly expand their footprints, all in pursuit of higher returns. On the PE side, low rates and reduced costs of funding incentivized financial sponsors to borrow aggressively and add leverage to the balance sheets of their portfolio companies. Current conditions are even more favorable given that the decline in benchmark rates during the pandemic has pushed the cost of funding even lower. Many loans tend to have a floor that sets a lower limit for floating-rate loans, but based on recent research by LCD, the total borrowing cost among leveraged buyout deals (LBOs) this year is the lowest it has been since the Great Financial Crisis (even after incorporating the effect of LIBOR floors).

Record-tight credit spreads have fostered cash hoarding, and there's been a buildup in cash through the pandemic. When tracking a representative sample of 1,326 speculative-grade companies in the U.S. and Canada, we found the median size of cash reserves (including cash equivalents and short-term investments) are running about 175% above the year-end 2019 level. Median cash reserves to gross debt has reached 12% since mid-2020 and has stayed elevated at 12% since, a significant increase from 8% at year-end 2019.

The rise in the cash reserves indicates that there's now excess cash being held beyond what's needed for operations and debt-servicing. Given the record amount of cash on hand, companies--no longer in survival mode--have reverted to strategies focusing on growth and shareholder payouts. This has fueled M&A and LBOs in recent quarters. Decisions around financial policy influence credit quality and the potential direction of rating actions, particularly for borrowers on the cusp between two ratings. Currently favorable funding rates could continue to make more-aggressive financial strategies--such as shareholder distributions and debt-financed acquisitions--appealing, and they might also limit improvements to credit statistics and ratings.

Prospects for economic recovery have varied across sectors. For some, the shifts in consumer and corporate behavior triggered--or accelerated--by the pandemic will likely have sustained effects that require a repositioning of business models. The Fed’s signal that it will stay the course of low policy rates has provided favorable conditions for companies looking to consolidate their positions or grow in the near future. We expect most U.S. nonfinancial corporate sectors to see some consolidation this year, building on the 144 PE-sponsored M&A transactions in the first half.

The technology sector, which was perhaps hurt least by the pandemic, has had the largest M&A volumes in the past 12 months. The pandemic only reinforced the attractiveness of tech companies, and PE shops raised funds to target this sector. Looking ahead, we expect more M&A in the hardware and software subsectors than in the semiconductors industry. Although it’s compelling for semiconductor companies to pursue acquisitions to gain efficiencies of scale and broaden product portfolios in ways that would otherwise be difficult to achieve, we believe large transactions will be limited given regulatory scrutiny (see "Credit FAQ: Latest Views On Hot Tech Topics--Semiconductor Supply Shortage, Inflation, And Big Tech Regulation,” July 9, 2021).

Consolidation in the health care sector has also accelerated as industry players seek to grow, with the goal of mitigating competitive and disruptive pressures. Makers of consumer staples, which focused on shoring up liquidity during the peak of the pandemic, have also restarted M&A and shareholder returns. In the media and entertainment sector, pending transactions include Discovery/WarnerMedia, Amazon/MGM, and Univision/Televisa’s media assets (see “Industry Top Trends Midyear 2021: Resilience, Recovery, Risks,” July 20, 2021).

Conversely, companies in some industries are following more conservative financial policies. Faced with severe headwinds related to environmental, social, and governance (ESG) and climate regulation, North American oil and gas producers have remained disciplined in their capital spending and maintained healthy balance sheets while balancing shareholder initiatives. The midstream-energy sector could be ripe for consolidation, given declining organic growth prospects, but large mergers have yet to materialize. Metals and mining companies are also showing sustained financial moderation and prudence. In light of relatively high valuations--and despite improving operating performance--the higher leverage as a result of M&A deals could translate into pressure on ratings.

Some of the frenzy in the use of special purpose acquisition companies (SPACs) to access public equity markets seems to have slowed. An April statement from the Securities and Exchange Commission on the accounting and reporting treatment related to SPAC warrants likely contributed to the slowdown. According to S&P Global Market Intelligence, SPAC IPOs dropped sharply in the second quarter. Nevertheless, they still accounted for $16 billion in capital from over 110 IPOs, and we expect the use of SPACs in M&A to continue.

From a credit perspective, we’ve seen examples of how SPAC transactions have been favorable for rated entities that reduced debt. Successful transactions can be credit positive, but unintended consequences merit watching. For example, SPAC-driven liquidity for acquisitions could lead to upward pressure on private-entity valuations.

In the sample of M&A deals we reviewed for studying SPACs, there was one entity that involved a SPAC transaction. More broadly, competition for acquisition targets by SPAC money might be a factor in purchase-price multiples of other transactions in the sample. The sole deal involved Advantage Sales & Marketing Inc., which completed its merger with the Conyers Park II Acquisition Corp. SPAC in October of last year. At that time, we raised the credit rating to ‘B’ from ‘CCC+’ and assigned a stable outlook. The company was able to successfully refinance its upcoming maturities, and leverage dropped to 4.9x, from 7.3x, following the merger. We expect the company to operate at lower leverage levels as a public company than it had in recent years (historically well above 6x). Nevertheless, financial sponsors still own more than 60% of the company, and we believe they will continue to aggressively pursue M&A.

We have also seen some asset managers use SPACS to raise capital. Alternative asset managers we rate--including Apollo Global Management Inc., Ares Management Corp., and Oaktree Capital Management--have issued SPACs to offer investments that might be far longer-term than the typical life of PE funds. As these managers source and close on targets, our analysis will focus on deployment and performance of the SPAC, governance of potential conflicts (such as regarding deal flow priority), and the ultimate revenues generated for the asset manager, among other factors.

In the following section, we compare the credit ratings, first-lien recovery expectations, and leverage levels of PE-sponsored M&A transactions with those of the broader speculative-grade universe. Our list of transactions builds from M&A deals tracked by LCD and includes only North American companies that tapped the U.S. leveraged loan market from July 2020 to June 2021. We chose this period because the second half of 2020 signaled widespread market recovery and a change in financing conditions, as demonstrated by the surge in high yield issuance and an acceleration in leveraged loan issuance. Of the 237 M&A transactions from July 2020-June 2021, we rated 212 companies (some of which executed multiple transactions).

The cohort of ‘B-’ borrowers expanded steadily in the years leading up to the pandemic, whether it was among first-time borrowers or those that had previously been rated higher. In addition to being highly leveraged, many of these companies are comparatively small and operate in fragmented markets or have niche offerings.

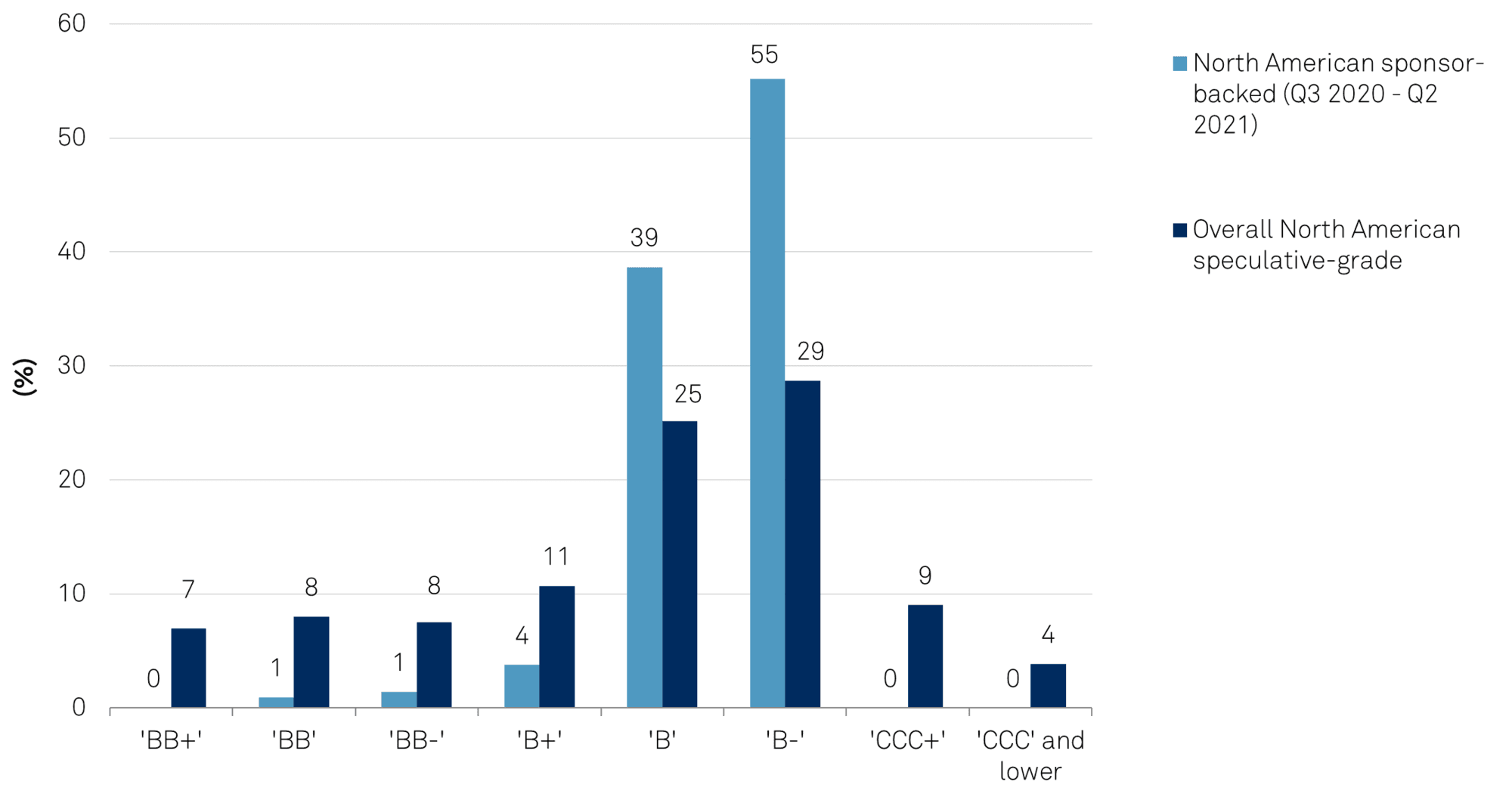

All these factors contribute to the low ratings. Sponsor-backed M&As are also concentrated among ‘B’ and ‘B-’ entities (see chart 2).

Chart 2 | Ratings Distribution Of Sponsor-Backed M&As Versus Overall Speculative-Grade

Source: S&P Global Ratings.

The most represented rating for both sponsor-backed M&A deals and overall speculative-grade borrowers is ‘B-’, with about 55% of the sponsor-backed companies and 29% of all North American speculative-grade borrowers having that rating.

However, before the pandemic, the modal rating for the North American speculative-grade companies was ‘B’. The combination of ratings actions and new issuance, 68% of which was sponsor-backed, has swelled the ‘B-’ cohort.

The roughly 55% of sponsor-owned M&A at the ‘B-’ level isn’t surprising given that in our ratings methodology, we generally view PE-owned companies as having a financial risk profile consistent with that of highly leveraged companies. We also found that regardless of the financial profile, PE-owned companies in the data we analyzed are more likely to have a weak or vulnerable business risk profile. This mostly reflects the relative shortcomings in such a company’s competitive position, such as a limited ability to pass along increases in input costs or heavy reliance on a small group of suppliers that can’t be replaced without high switching costs. A less-favorable business risk profile means there’s less financial risk that a company can bear at a given rating.

The ‘B-’ dominance is mostly evidenced in the sectors with the most M&A. The top three rated sectors in this regard during the period--technology, health care, and business services--accounted for close to half of all transactions. Of the companies in the tech sectors, about 80% were rated ‘B-’. This figure was about 64% for health care and 66% for business and consumer services. In the speculative-grade universe, 41% of the companies in the tech sector have a ‘B-’ rating, 38% in consumer services, and 35% in health care.

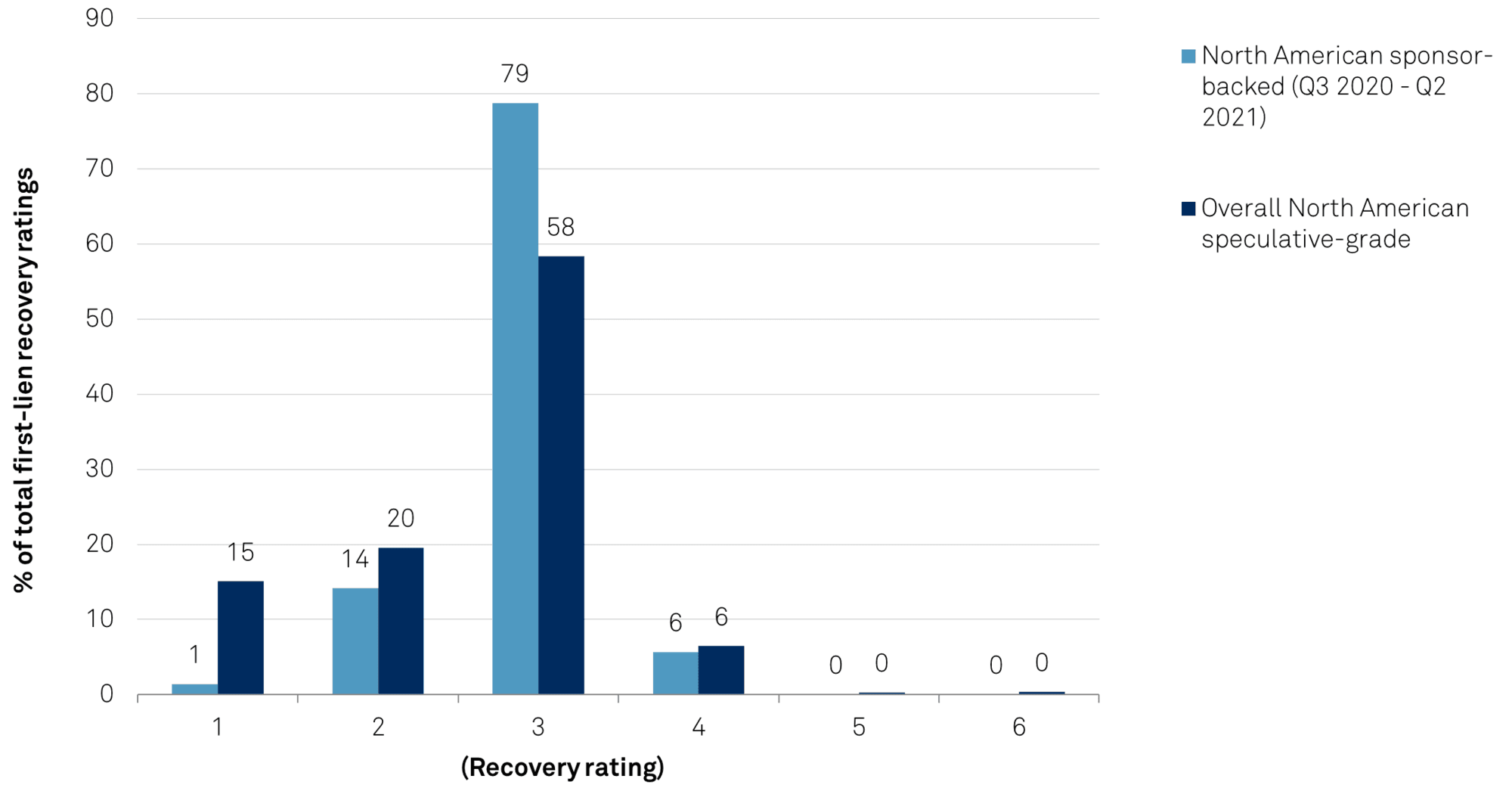

Similar to the trend in credit ratings, there has been a gradual decline in the recovery ratings of senior secured first-lien instruments issued by North American speculative-grade corporates.

In 2016, new issues with recovery ratings of ‘1’ (90%-100% estimated recovery) and ‘2’ (70%-90%) accounted for 52% of the total, while new issues with a recovery rating of ‘3’ accounted for 43%. In 2020, the new issues with recovery ratings of ‘1’ and ‘2’ accounted for 32% of the total, while ‘3’ (50%-70%) made up 59% (see chart 3). The buildup of leverage--along with a steady erosion of the junior debt cushion and, to some extent, the lack of maintenance covenants--have contributed to this decline.

Chart 3 | First-Lien Recovery Rating Distribution Of Sponsor-Backed M&A Versus All Speculative-Grade

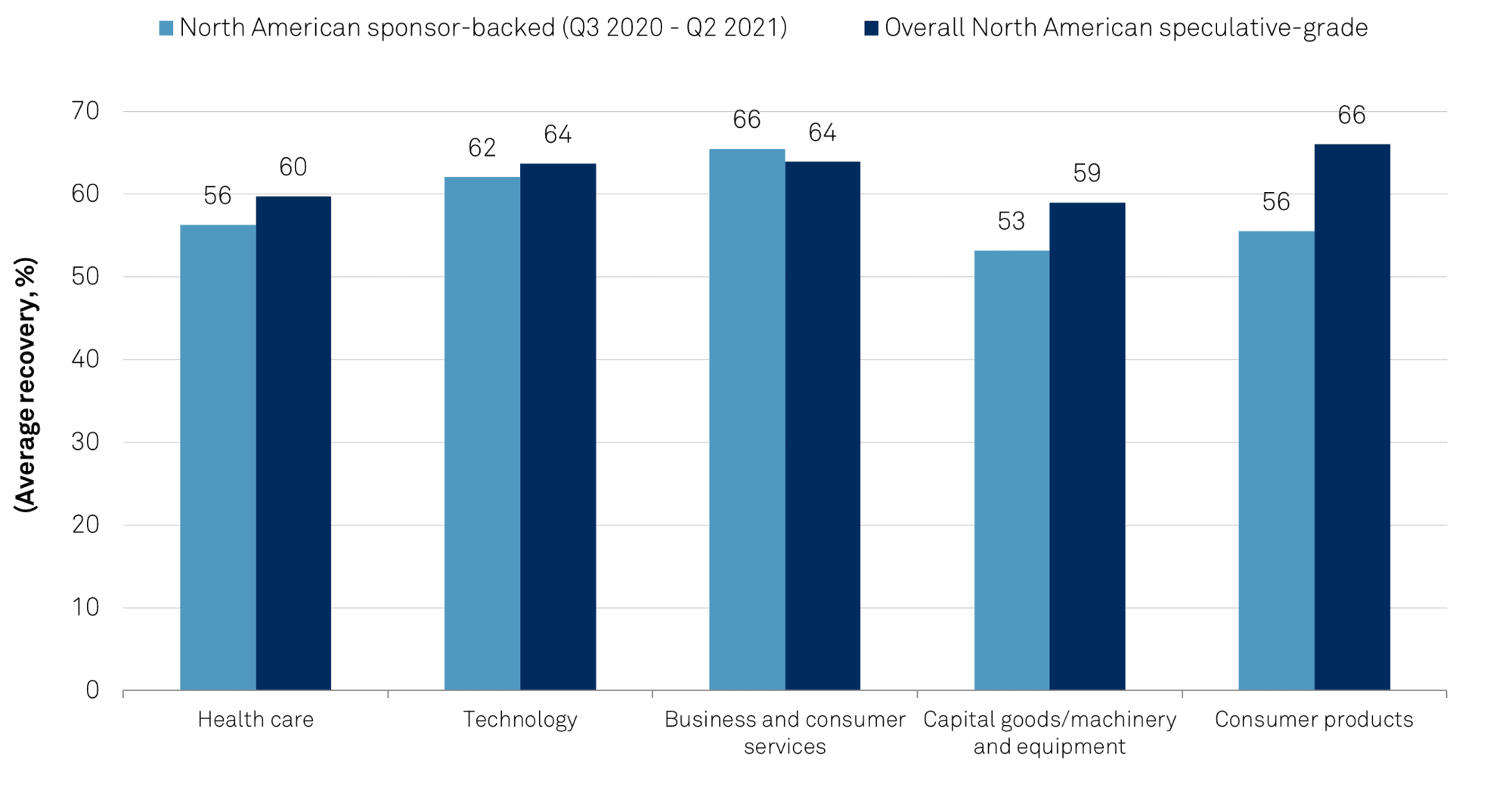

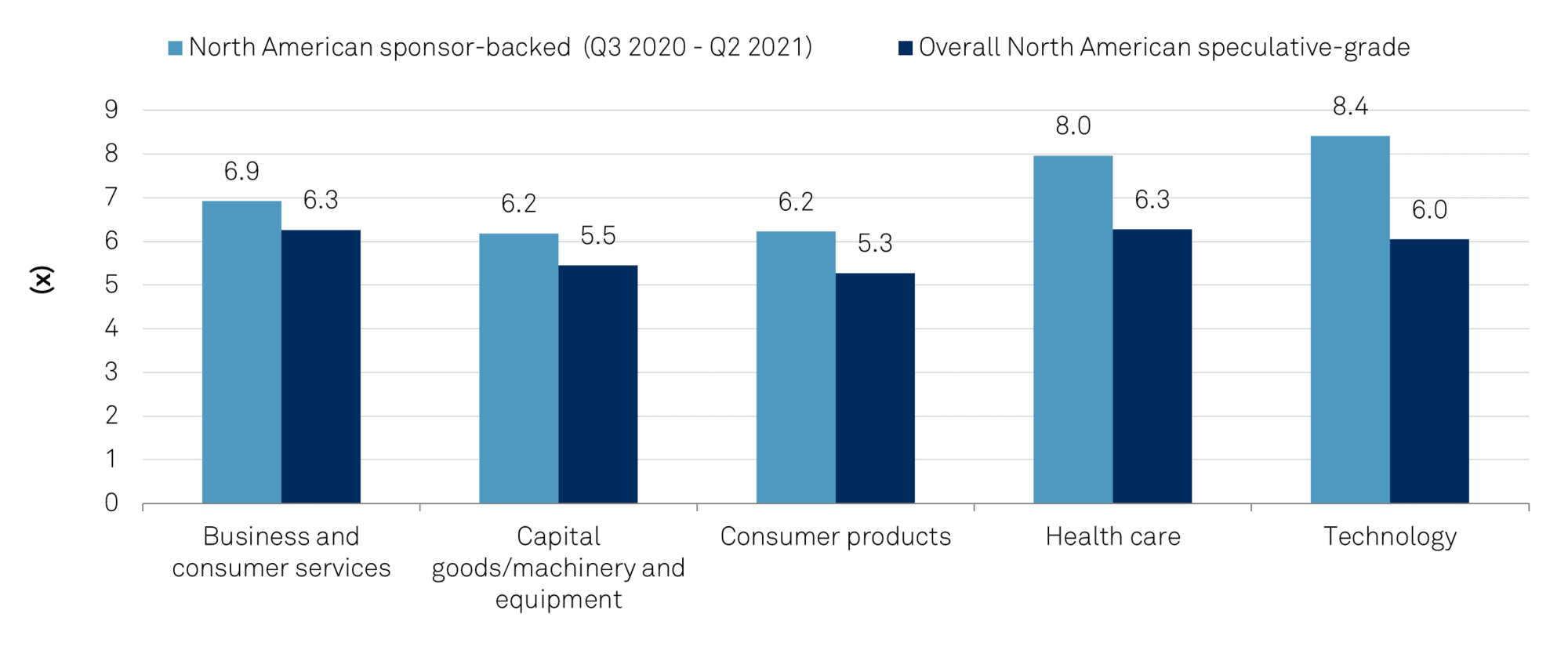

On average, the recovery point estimate for senior secured first-lien debt in the North American speculative-grade universe is 6 percentage points higher than that for sponsor-backed M&A transactions, at 65% versus 59%. A recovery rating of ‘3’ continues to be the most dominant in both categories. More than one-third of issues in the speculative-grade universe have a senior secured recovery rating of ‘1’ or ‘2’ compared to roughly 15% of sponsor-backed M&A transactions. For companies in consumer products and forest products/building material, there was a 10 percentage-point difference in recovery point estimates between the sets. By contrast, health care and technology had a difference of just 2-3 percentage points (see chart 4).

Chart 4 | Average First-Lien Recovery Estimates: Top Five Sectors Show A Gap Version

One of the contributing factors to the general downward trend in corporate credit ratings in the past few years is the gradual buildup of leverage. Competition among PEs has driven up purchase-valuation multiples among M&A deals, meaning companies today need to borrow more without the help of a higher equity contribution. We believe frothy valuations and accompanying aggressive leverage will persist as long as there is demand from investors for increased yield.

On average, the difference in leverage, as calculated by S&P Global Ratings and used in our rating analysis, between sponsor-backed and speculative-grade companies is almost 1.7 turns, while on a median basis, the difference is about 1.4 turns (see the table and charts 5 and 6).

(The earnings used in our calculations of leverage are based on our projection of earnings and are often more conservative than how EBITDA is defined in credit agreements for covenant calculations and other purposes. Our calculated leverage takes into account both a historical and a forward-looking component of earnings and debt.)

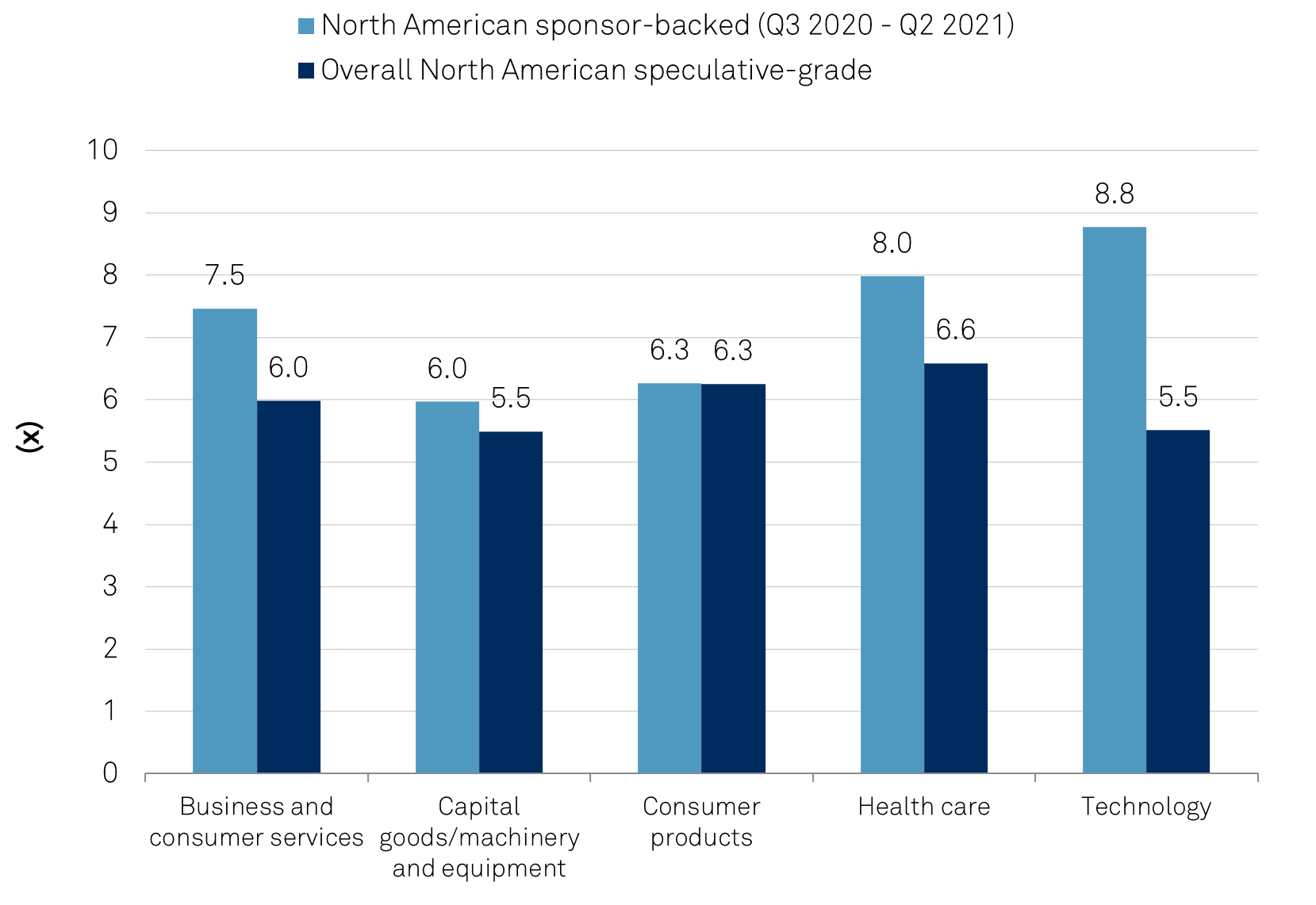

Median leverage is highest for sponsor-backed technology companies (8.4x) and is more than two turns higher than leverage for rated technology companies in North America (6.0x). Many of the tech companies offer predictable recurring revenue streams, giving sponsors and investors the comfort for piling on excessive debt. In fact, the 2.4x gap between sponsored and all speculative grade is the largest among major sectors. Similar enthusiasm for the potential growth and its non-cyclical nature propelled the health care sector to second place, with median leverage as high as eight turns.

Chart 5 | Leverage Comparison

(x)

North American sponsor-backed (Q3 2020 - Q2 2021)

Overall North American speculative-grade

Average

7.32

5.64

Median

6.85

5.48

Chart 6 | Median Leverage Gap Among Top Five Sectors

Chart 7 | Average Leverage Gap Among The Top Five Sectors

Credit quality is one of the biggest concerns among leveraged finance investors, and the onslaught of M&A deals has come amid both easy access to capital and a greater inclination of PE-owned companies to take on more risk.

Our analysis reveals the fragility of these companies that took on excessive debt (where median leverage is 1.4x higher than the broader speculative-grade universe) and are expected to recover less on first-lien debt in a default scenario (with recovery expectations 6 percentage points lower than that of an average speculative-grade company).

Overwhelming demand has led to lofty valuation and ever-increasing leverage in sponsor-backed M&A deals. Looking ahead, the credit quality for these companies will largely rely on a positive trajectory out of the pandemic. This means they could face downgrades if an optimistic scenario--accelerating EBITDA growth and continued favorable credit markets--does not pan out.

Global Capital Markets & SPAC Activity – H1 2021, Aug. 3, 2021

U.S. Leveraged Finance Q2 2021 Update: Credit Metric Recovery Shows Sector, Rating, And Capital Structure Mix Disparities, July 20, 2021

COVID-19 Heat Map: Pent-Up Demand And Supply Shortages Further Improve Recovery Prospects For Credit Quality, June 8, 2021

Credit FAQ: SPAC Warrants Reclass And Their Ratings Implications, June 2, 2021

Credit FAQ: SPACs And Credit Quality: S&P Global Ratings' Recent Ratings Experience, March 12, 2021