Feb. 07, 2022

First-lien recoveries improved in the first half of 2021 from the post-lockdown lows of the second half of 2020.

The oil and gas and restaurant/retail sectors had more defaults than other sectors over the past year and a half.

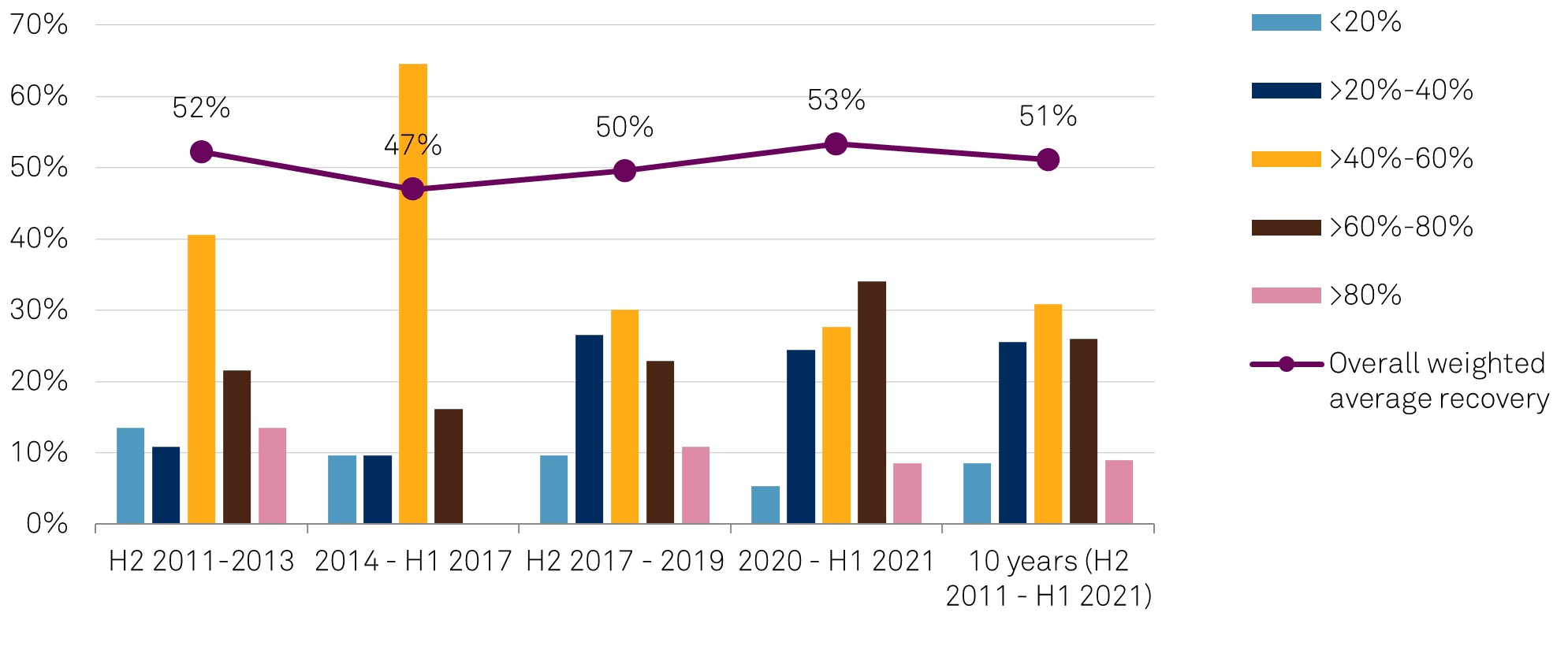

Overall weighted average recoveries have remained consistently in the high-40% to low-50% range over the past 10 years, though for the six quarters through the first half of 2021, they fluctuated between the low-40% area and the high-50% area.

This report does not constitute a rating action.

Kenny K Tang New York +1-212-438-3338

Steve H Wilkinson, CFA New York +1-212-438-5093

Ramki Muthukrishnan New York + 1-212-438-1384

Jessica Templeton-Lynch Centennial +1-303-721-4842

There's no doubt the COVID-19 pandemic has had an adverse impact on all facets of society, and corporations are no exception. Amid the widespread lockdowns of the initial outbreak, most companies' ability to operate and remain solvent was constrained. This was apparent from the sharp spike in distress and defaults. In 2020, 62 companies rated by S&P Global Ratings filed for U.S. bankruptcy protection, and another nine did so in 2021 through Nov. 28.

Debtors and creditors alike worried about the prospects of lengthy bankruptcy proceedings because there was so much uncertainty as to how the pandemic would play out, amplifying the risks for debtors and creditors. In response, many debtors and creditors clamored to pre-negotiate restructuring plans prior to filing to expedite proceedings and exit bankruptcy as soon as possible. Thus, many creditors consented to restructuring plans that resulted in lower-than-average recoveries as they aimed to limit the time and cost spent in bankruptcy and mitigate further losses given the dire and uncertain circumstances during this period. However, optimism and market liquidity were buoyed by the Federal Reserves’ fiscal and monetary stimulus programs and liquidity measures enacted in 2020, which were intended to counteract the fallout from the pandemic and support the economy. And, along with the eventual rollout of COVID-19 vaccines and easing of restrictions in 2021, companies that emerged in the first half of 2021 had better business prospects and creditor recovery rates. The contrast in recoveries between these two relatively short time periods further supports S&P Global Ratings’ view that the timing of a company’s exit from bankruptcy can significantly affect lender recoveries.

Three key factors affected the large number of defaults during this period:

This report is an update of "From Crisis To Crisis: A Lookback At Actual Recoveries And Recovery Ratings From The Great Recession To The Pandemic," which was published on Oct. 8, 2020. Here, we focus on corporate debt recovery trends for North American companies that defaulted and emerged during the six quarters through the second quarter of 2021. We compare these trends to long-term historical recovery trends going as far back as 2008, when we rolled out unsecured debt recovery ratings to accompany our existing secured debt recovery ratings. We also break down recovery trends by sector and weighted-average recovery.

The recovery trends discussed in this report evolved from a dataset consisting of North American companies rated by S&P Global Ratings that filed for bankruptcy (excluding distressed exchanges and out-of-court restructurings) and exited bankruptcy over the past 13 and a half years (from 2008 through the second quarter of 2021). We included only companies for which we could obtain reliable and clear recovery data, primarily from the reorganization plans and disclosure statements that debtors filed when they prepared to exit bankruptcy.

This update adds another 52 companies that exited bankruptcy in 2020 and 19 that did so in the first half of 2021, thus increasing the sample size by 352 debt issues and nearly $158 billion in aggregate debt.

The total size of the dataset going back to 2008 stands at 358 companies with over 1,600 debt issues and $655 billion in total debt.

Table 1 | Prepetition Debt (Mil. $)

Source: S&P Global Ratings.

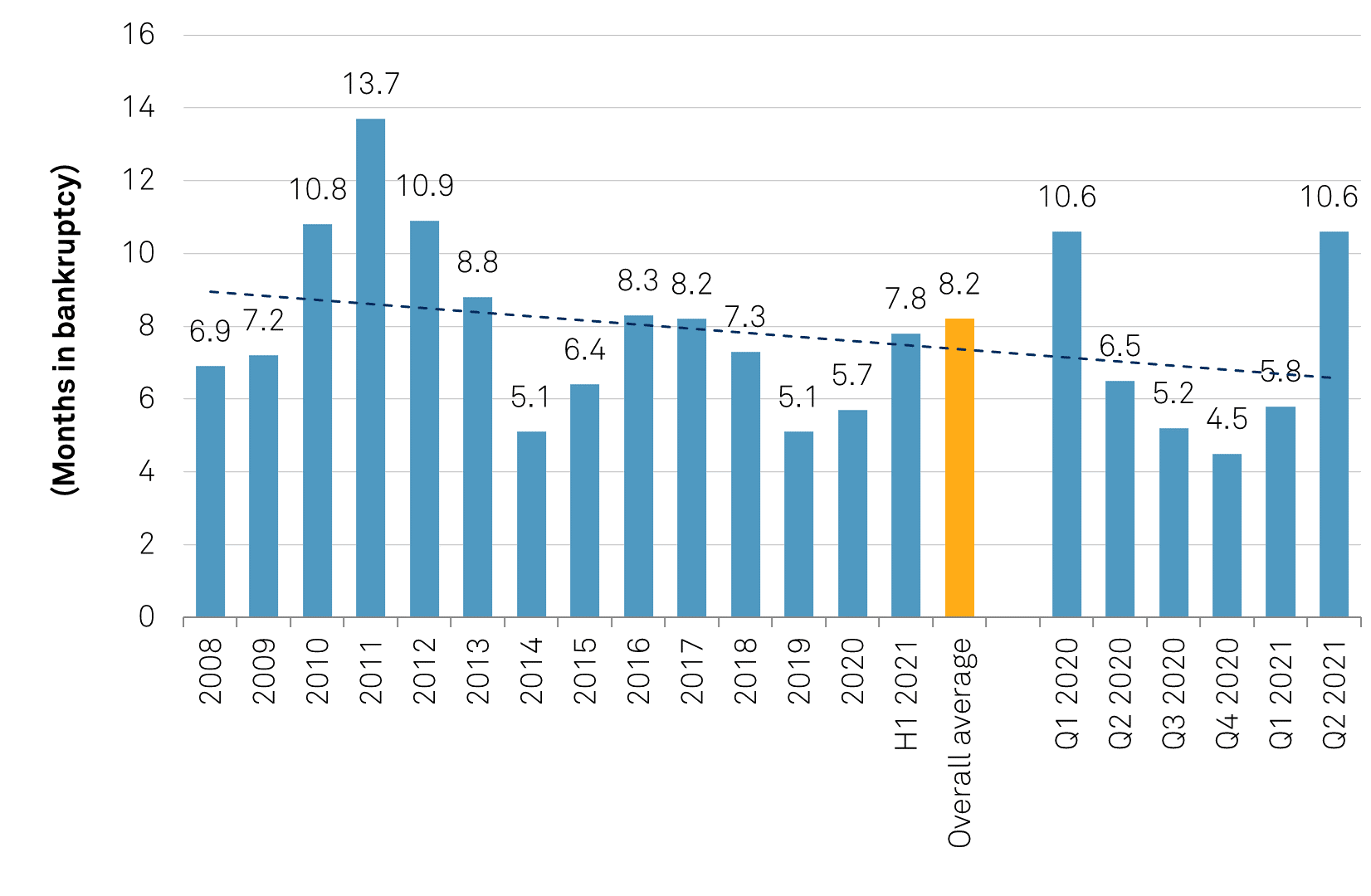

Companies seeking bankruptcy protection have tended to spend less time in bankruptcy administration by negotiating with creditors and agreeing to a restructuring plan before filing.

This was demonstrated in the six quarters through second-quarter 2021, as the lion’s share of corporate bankruptcies spent an average of only four to seven months in administration before exiting.

However, not all companies could emerge in expedited fashion, particularly those that were larger with more complex organizational structures and those that were unable to negotiate a restructuring plan beforehand. For example, some companies that emerged in the second quarter of 2021 spent an average 11 months in bankruptcy. This cohort includes several large corporations that defaulted within two months of the lockdown, such as Hertz Global Holdings Inc., Frontier Communications Corp., and Diamond Offshore Drilling Inc. Southern Foods Group LLC also emerged in the second quarter of 2021 after spending almost 19 months in bankruptcy (it filed in November 2019); it exited via a 363-asset sale transaction. In addition, FirstEnergy Solutions Corp. and Pacific Gas & Electric Co. (PG&E), given their large size and relatively complicated debt structures and restructuring considerations, spent 23 months and 17 months, respectively, in bankruptcy before exiting in the first half of 2020.

Chart 1 - Average Time In Bankruptcy (Months)

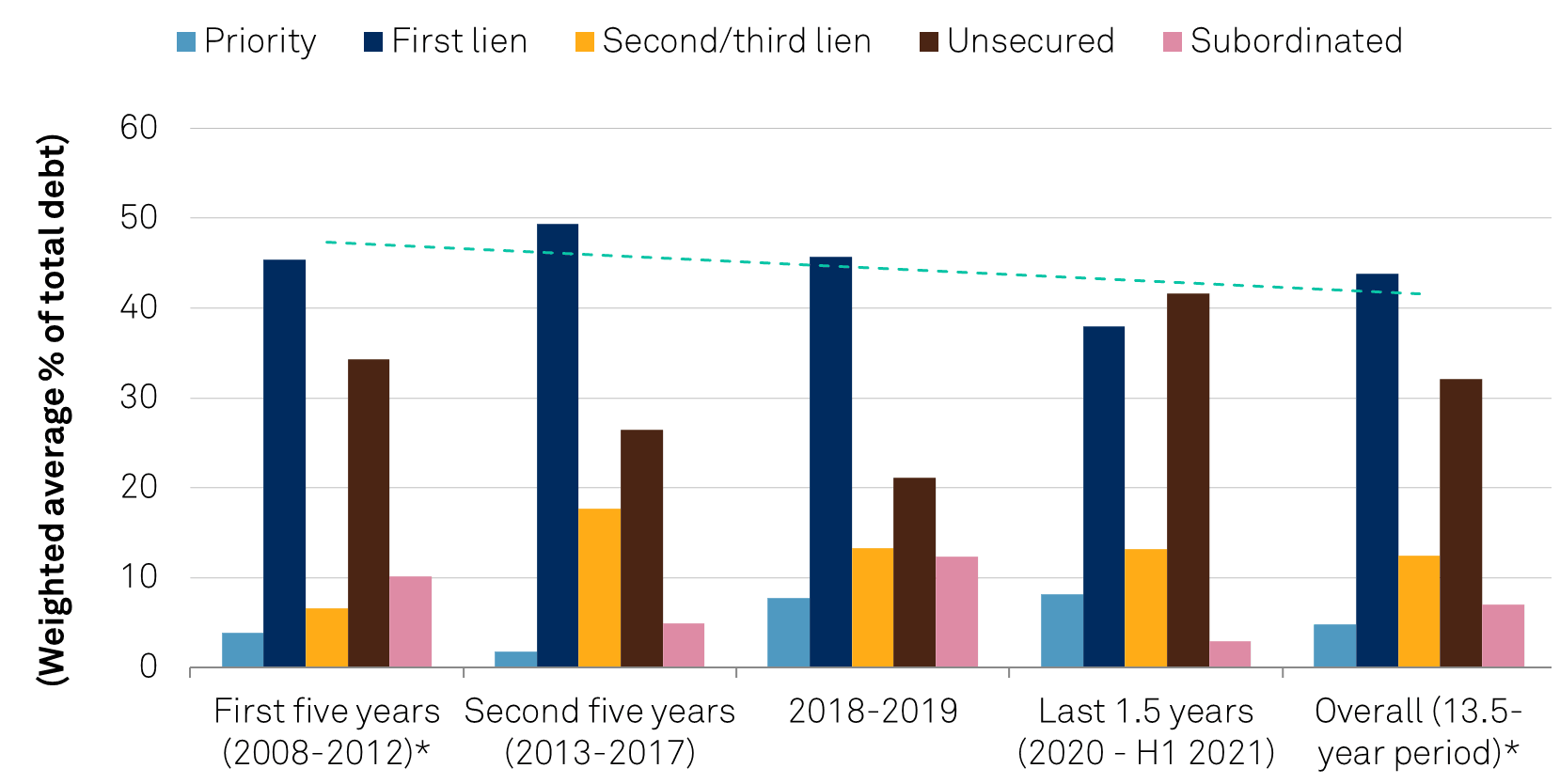

The debt mix, the relative proportions of debt classes in a company’s capital structure, has shifted for companies that emerged from bankruptcy in recent years. Our dataset from the past 1.5 years shows changes in weighted average debt structures compared to earlier periods, with an increase in priority debt for each of the more recent periods and a substantial increase in unsecured debt (see Chart 2). For example, the mix of first-lien debt declined 7 percentage points to 38% from 45% (five-year average of 2008 to 2012) in the 1.5-year period.

The key drivers of this shift is largely the high proportion of companies in the oil and gas and restaurant and retail sectors that have been in the cohort over the past 3.5 years. These sectors typically had asset- or reserve-based revolvers with priority liens on key assets that we usually treat as priority debt. In addition, oil and gas company debt stacks typically include a large proportion of unsecured debt (such as Valaris PLC’s, Diamond Offshore Drilling Inc.’s, and Whiting Petroleum Corp.’s), with an average of 41% of the sector’s debt structure being unsecured debt. Furthermore, several large companies had thick layers of unsecured debt, which skewed the past 3.5-year debt mix toward the unsecured debt class. Examples include PG&E, with $15 billion in unsecured debt (82% of the total) and Frontier Communications Corp. ($11 billion; 66%).

Chart 2 - Weighted Average Debt Mix (%)

*Excludes $21.3 billion in General Growth Properties property-level debt (emerged in 2010), which would have significantly skewed the average toward the priority debt class.

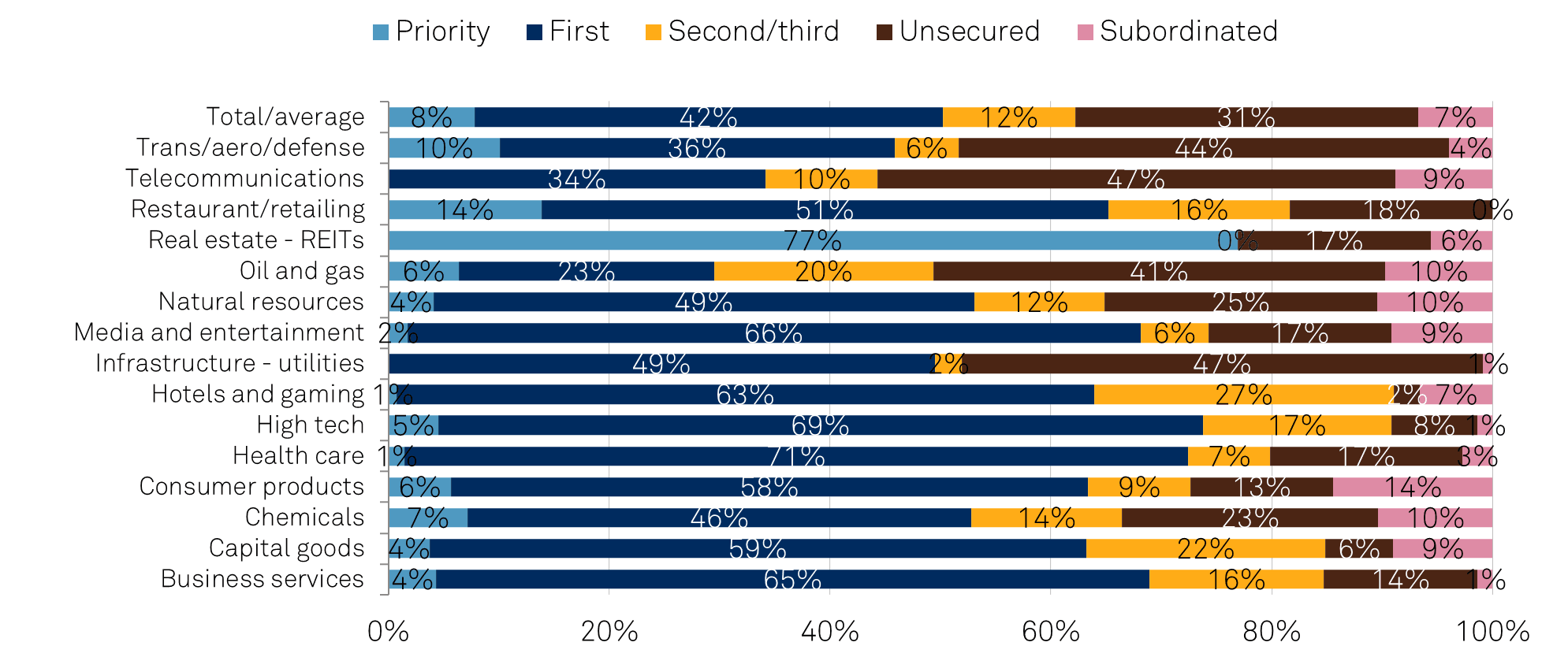

Different sectors (and business types) often have inherently varying debt structures that are specific to the particular sector (or business type) and its asset base. As already mentioned, oil and gas companies (exploration and production ones in particular) typically had stacked debt structures with priority RBL (reserve-based revolving facilities). By contrast, retail had a higher proportion of working capital-based financing via asset-based lending (ABL) facilities. Real estate also has a distinguishable debt structure, with a significant portion of its debt in the form of property-specific mortgage debt plus a layer of corporate-level debt. (In Chart 3, the data for that category is from just one company, General Growth Properties (GGP), which emerged from bankruptcy in 2010). While GGP had been the only REIT in our dataset over the past 13.5 years, two mall REITs--CB&L Associates and Washington Prime Group Inc.--recently emerged from bankruptcy, and we’ll include them in our next update.

Chart 3 - Debt Mix (% Of Total Debt)

Actual recoveries in the six quarters through June 30, 2021, were affected first by the significant economic stress and uncertainty caused by the COVID-19 pandemic and related mitigation measures, and then by the improving economic conditions over 2021.

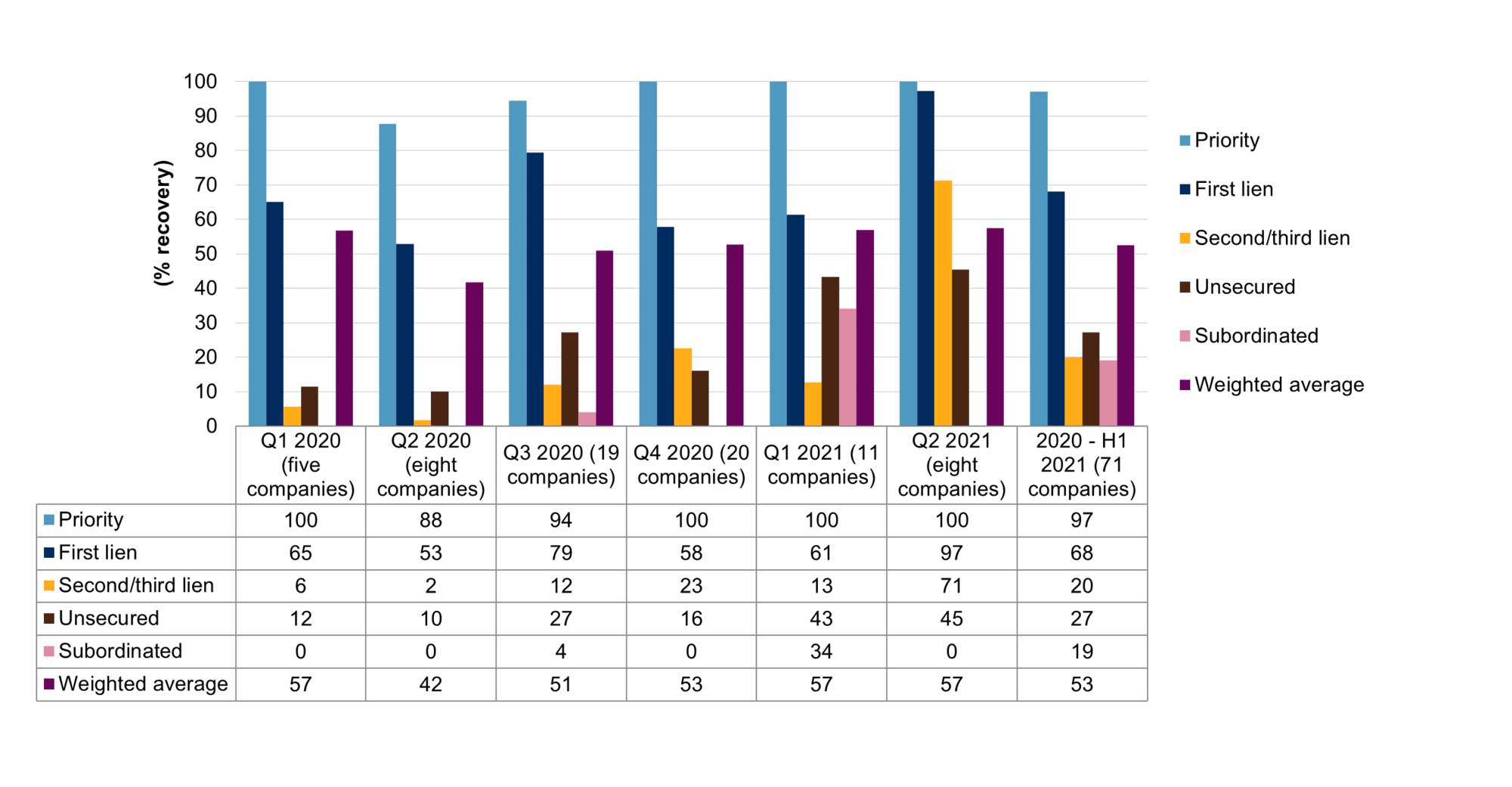

In particular, there was a notable dip in weighted average recovery rates by company in the second quarter of 2020 that didn’t abate until 2021, when economic conditions and expectations improved significantly.

There was a similar drop in average actual first-lien debt recoveries during this time. The exception was a brief rebound in third-quarter 2020, which stemmed from a combination of debt mix and above-average recoveries for several companies; weighted average recoveries improved to slightly above the 50% mark. The uptick in first-lien recoveries in third-quarter 2020 was bolstered by strong (100%) recoveries from PG&E, Whiting Petroleum, Denbury Resources, and Quorum Health Corp. However, these figures were partially offset by poor recoveries for senior lenders to retailers Neiman Marcus Group (32% recovery) and Chinos Holdings Inc. (J Crew; 54%).

First-lien recoveries declined again to an average of 58% in fourth-quarter 2020 before inching up a bit to 61% in the first quarter of 2021. Recoveries picked up substantially in Q2 2021 as vaccines were rolled out and economic prospects were bolstered by the perception that a return to normalcy was on the horizon. Low recoveries hampered creditors including those of EP Energy LLC (39% first-lien recovery), California Resource Corp. (21%), Libbey Inc. (22%), 24-Hour Fitness Worldwide Inc. (29%), JC Penney Co. Inc. (25%), Ascena Retail Group Inc. (19%), and LSC Communications Inc. (15%). However, they were offset by 100% recoveries for Noble Corp., SPR Holdings LLC, Guitar Center Inc., and Akorn Inc.

Of course, these quarterly average recoveries are invariably skewed because the set of emerged companies in each quarter is small, and it shows large swings in recovery rates.

But when looked at over a one-year period or longer with a larger sample set, a smoother transition of recovery between periods is evident. Overall, first-lien recoveries over the past six quarters averaged 68%, which was weighed down by the fourth quarter of 2020, when 20 companies emerged from bankruptcy.

Chart 4 - Average Actual Recoveries By Debt Class (Last Six Quarters Ended Q2 2021)

Average recoveries have trended downward, not just in the past six quarters but during pre-pandemic years 2018 and 2019, as our last update indicated (see " ," Oct. 8, 2020). The predominant sectors from which companies emerged from bankruptcy in the past 3.5 years were oil and gas and retail--both of which experienced extreme stress. The oil and gas sector dealt with volatility, while the retail industry faced the secular decline of physical stores. These factors hindered overall plan valuations, debt recovery rates, and resulting in exit capital structures, with low recoveries for creditors.

Companies that exited with low recoveries since 2018 include Vanguard Natural Resources LLC, Checkout Holding Corp., Charming Charlie LLC, FULLBEAUTY Brands Holdings Corp., and FR Dixie Acquisition Corp. However, not all retail bankruptcies resulted in low recoveries, as demonstrated recently by Guitar Center Inc., which had 100% and 90% recoveries for its first- and second-lien debtholders, respectively, despite ABL priority facilities. In addition, GNC Holdings Inc.’s first-lien lenders attained 75% recovery despite the presence of higher-priority ABL debt.

Companies in both of these sectors generally have asset-based revolver facilities that we treat as senior over non-working capital asset-based first-lien debt with respect to the ABL or RBL collateral, which usually makes up the brunt of a company’s asset value.

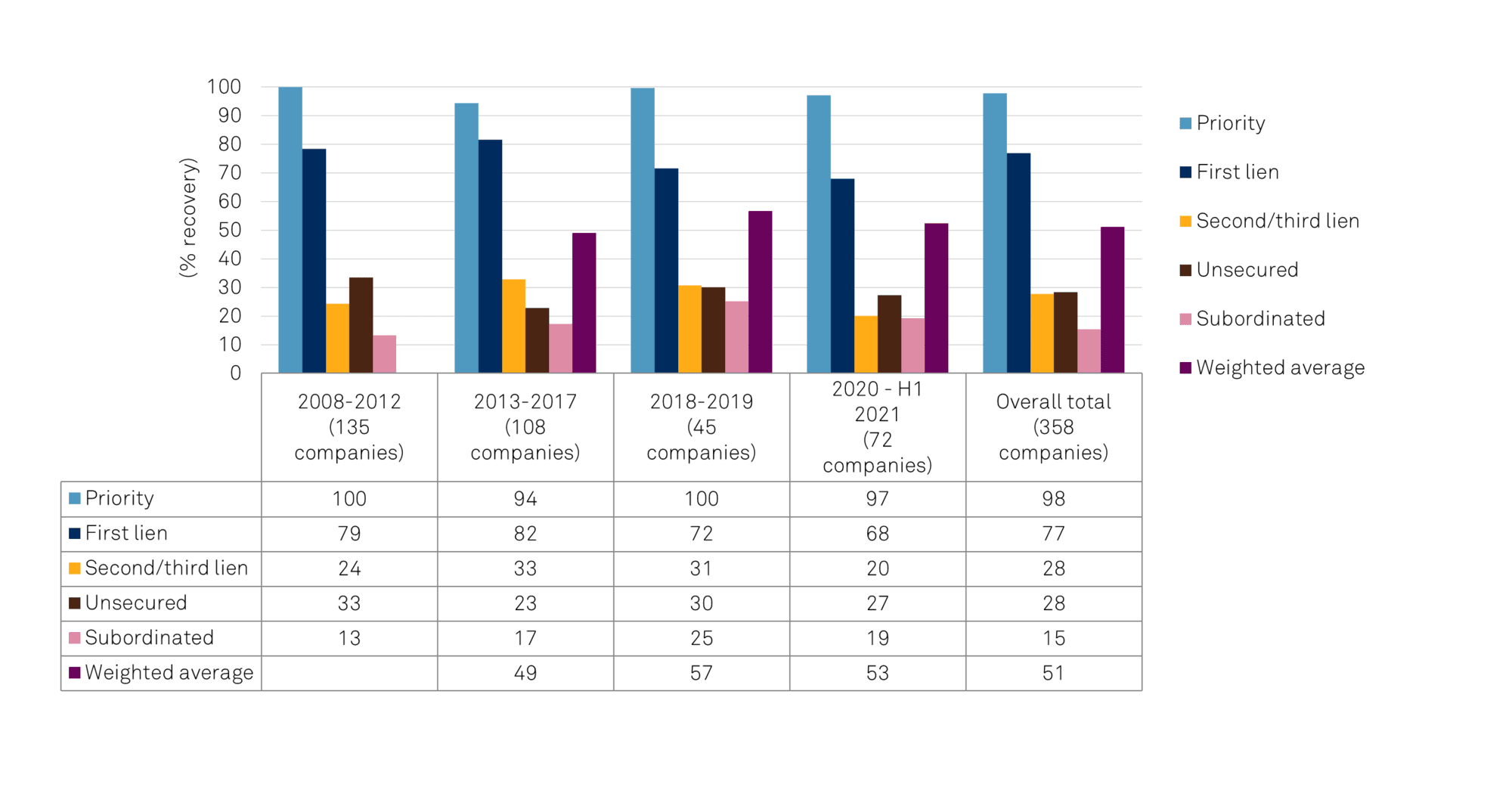

Average recoveries for first-lien debt declined to 72% for 2018-2019 and further to 68% in the six quarters through June 30, 2021, from 79%-82% in 2008-2017 (see Chart 5). While the last 3.5-year period endured a steeper decline in average recovery, it only brought the overall average first-lien recovery to 77% because our dataset is now much larger, with 358 companies holding $655 billion in aggregate debt.

Chart 5 - Average Actual Recoveries By Debt Class (2008 - Q2 2021)

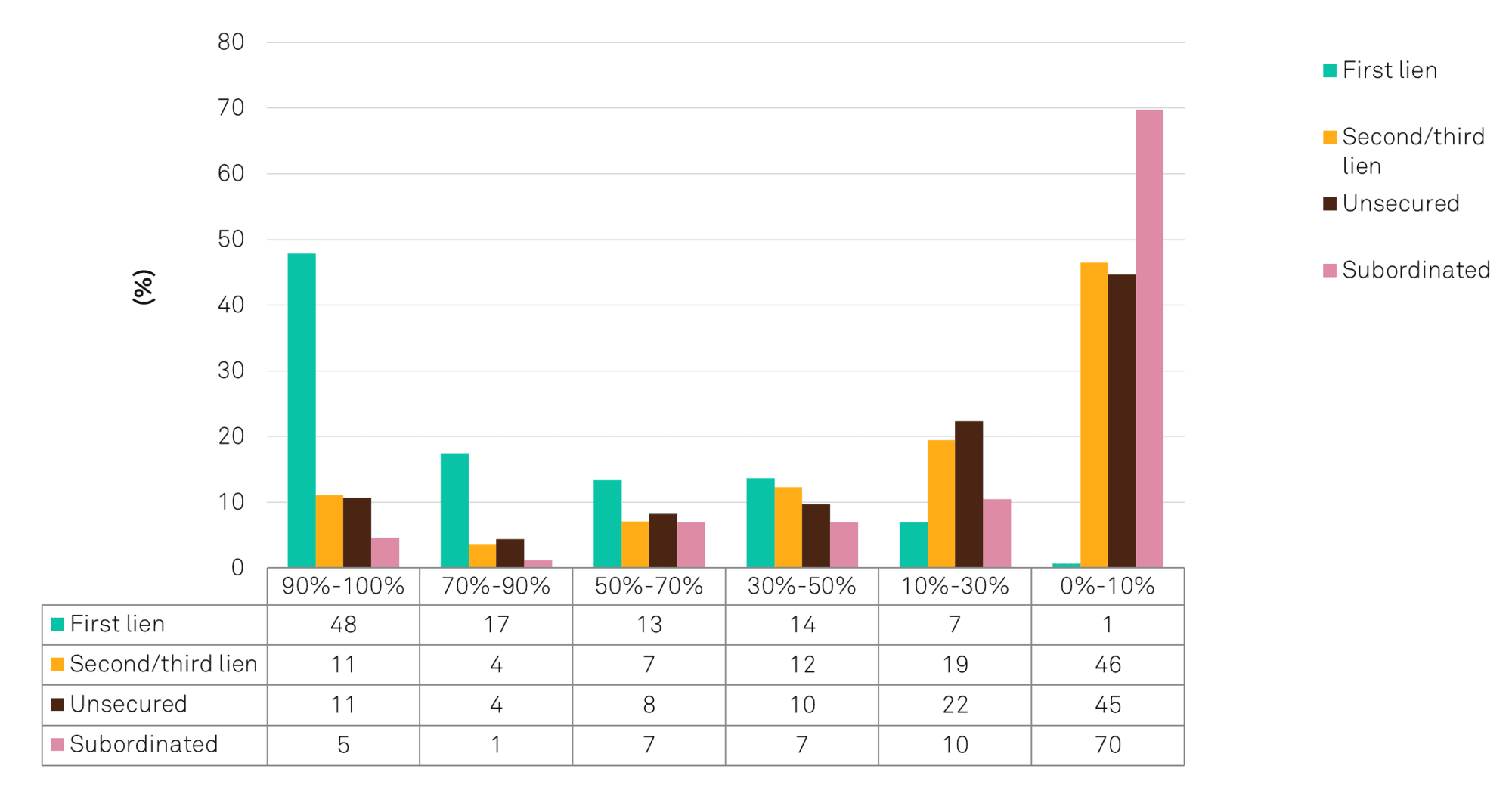

Another way of looking at the underlying data is to ascertain the number of recoveries within the ranges that correspond to our recovery ratings.

For example, 48% of all first-lien debt classes achieved at least 90% recovery and 17% achieved recoveries in the 70%-90% range (see Chart 6). Similarly, if we look at unsecured debt and its junior position in the capital structure, unsecured creditors achieved 0%-10% recoveries 45% of the time.

Chart 6 - Percent Of Actual Recoveries Within A Recovery Range By Debt Class (2008 - H1 2021)

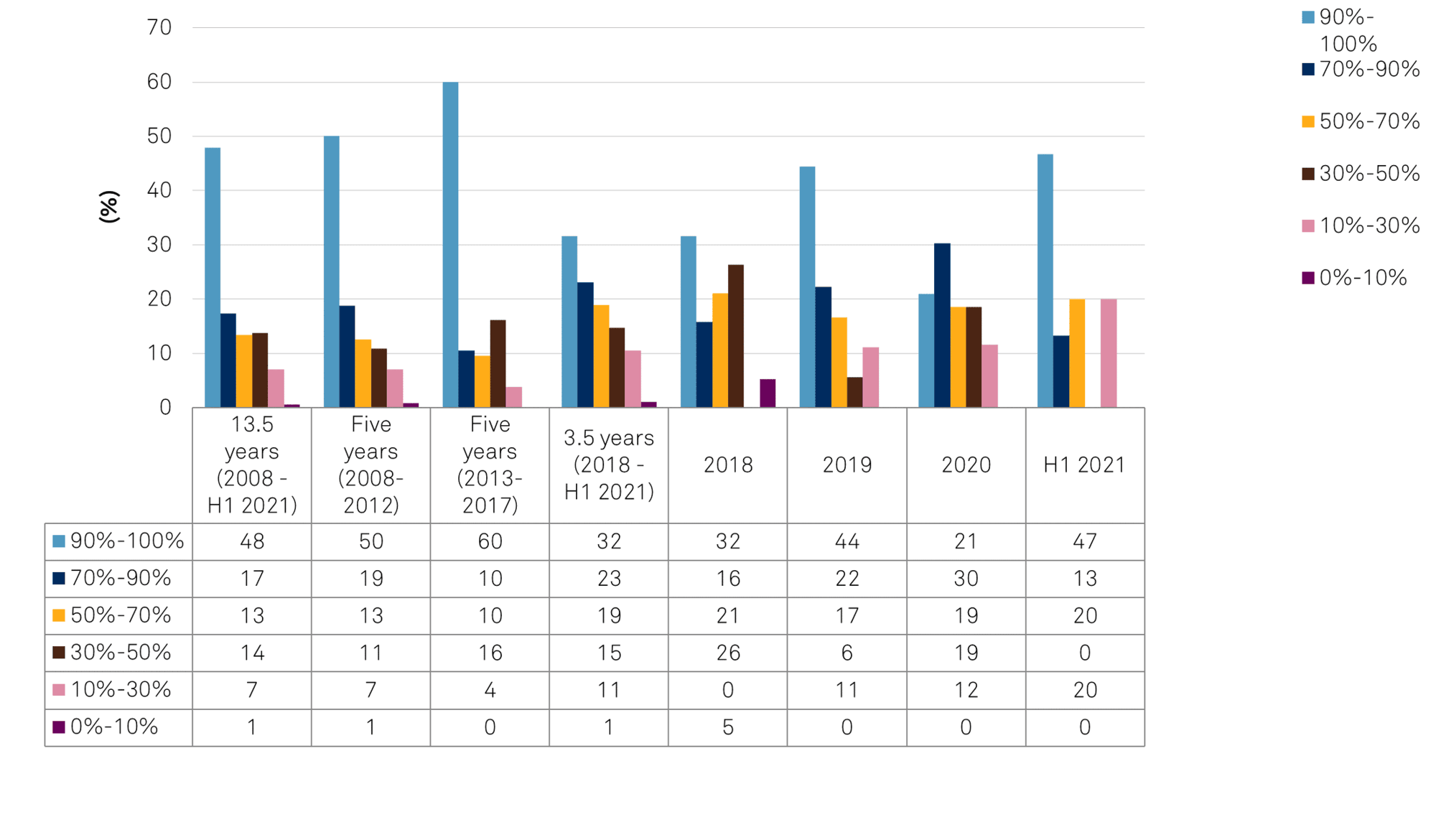

If we look at the data at different times, we notice that recovery trends have shifted downward.

For instance, in the past 3.5 years, 32% of first-lien debt class recovered at least 90%, and 23% recovered 70%-90%. Underlying factors include a prevalence of retail and oil and gas companies (which had ABL/RBL structures that depressed recovery for first-lien creditors) and high demand for leveraged loan paper, which allowed companies to operate with for higher-leveraged debt structures.

Chart 7 - Percent Of First-Lien Debt Recoveries Within A Recovery Range

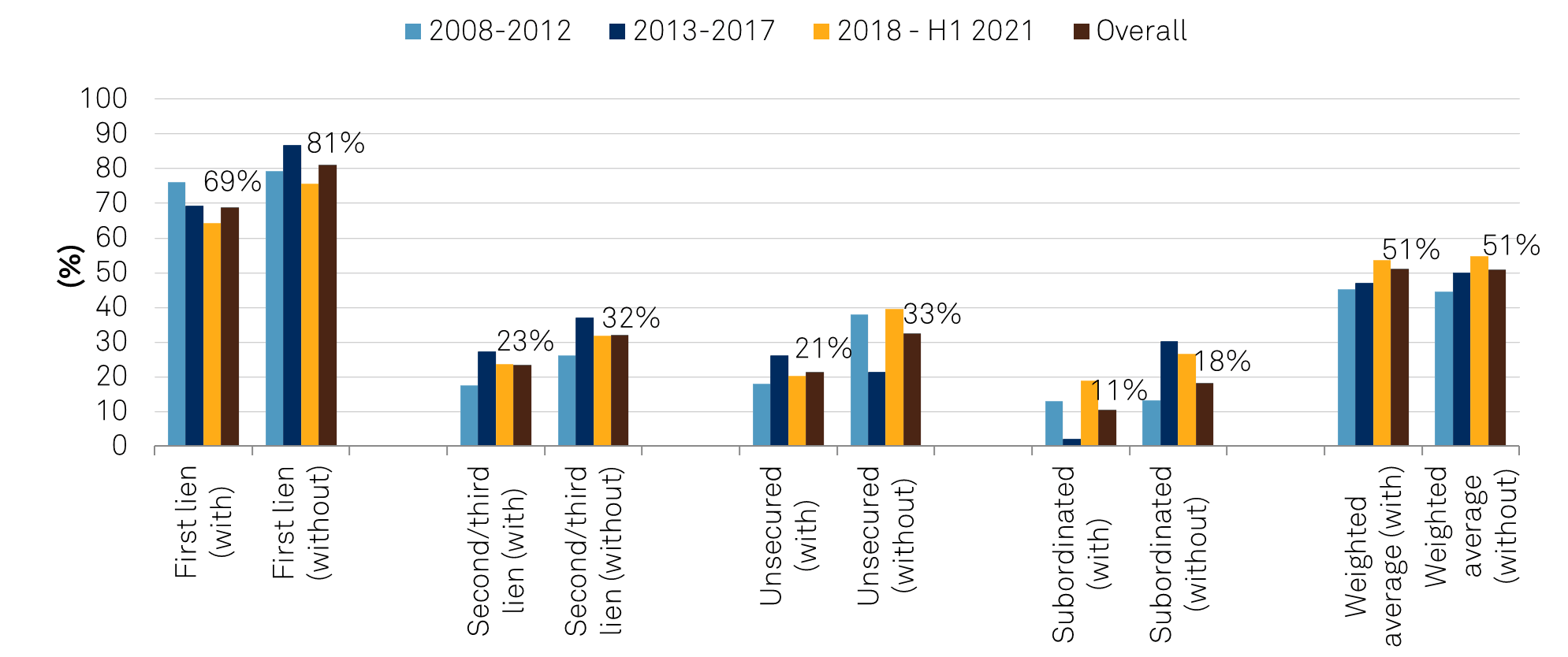

Given that recent bankruptcies were concentrated in the oil and gas and retail sectors, which meant that recoveries were disproportionately skewed by the number of issuers that had priority debt within the debt structures, we decided to take a look at how average recoveries compared if we excluded those companies.

Chart 8 demonstrates that the average recovery is 12 percentage points better in the overall 13.5-year period at 81% for first-lien debt when there is no priority debt compared to 69% for those that had priority debt.

The 81% average recovery for first-lien debt without priority debt is skewed toward the overall average of 79%. This is because while the oil and gas sector and retail sector made up most of the recent defaults in the overall 358-company dataset, the majority (60%) of companies didn't have priority debt ahead of the first-lien debt in their debt structures.

Specifically, for unsecured debt, the difference in recovery over the past 3.5 years was 20 percentage points better for debt structures without an ABL or RBL facility. This was because unsecured creditors of larger companies had higher-than-average recoveries, including those of PG&E (100% unsecured recovery), Hertz Global Holdings Inc. (100%) Superior Energy Services Inc. (70%), and Noble Corp. (86%). While recoveries are better for creditors when the debt structure doesn't have priority debt, the overall weighted-average recovery is about the same at 51% overall, which indicates that recovery valuations might not be so different but rather the distribution of it by priority of rights of claim made a difference.

Chart 8 - Average Recoveries Comparisons (With And Without Priority Debt)

While overall weighted-average recoveries have hovered in the 47%-53% range for the past 10 years, the actual weighted-average recovery by company has moved toward a more normal distribution (see Chart 9).

In other words, the company-specific weighted-average recoveries are more evenly spread out on both sides of the 40%-60% weighted-average recovery range. Weighted-average recoveries were concentrated within the 40%-60% bucket from 2011 to 2016; however, the distribution moved to either side of this bucket during the past five years, with 24%-27% of companies within the 20%-40% bucket, 28%-30% within the midpoint 40%-60% bucket, and 23%-34% within the 60%-80% bucket. Overall, the 10-year distribution is essentially a normal distribution. This shift to the 20%-40% bucket highlights the recent low weighted-average recoveries from the oil and gas sector (particularly in 2020, when commodity prices were at record lows) in addition to local news firm The McClatchy Co. (33%) as well as retailers JC Penney (34%) and 24 Hour Fitness (19%). However this was similarly offset by shifts toward the higher 60%-80% bucket, with higher overall weighted-average recoveries such as Hertz (100% weighted average recovery), PG&E (100%), Ferrellgas Partners L.P. (95%), SPR Holdings (97%), and Akorn Inc. 100%). Some retailers also achieved relatively high levels of weighted-average recoveries in the 61%-66% range, including Guitar Centers, Chinos Holdings Inc., and Bluestem Brands Inc. (see Table 2).

Chart 9 - Distribution Of Weighted Average Analysis

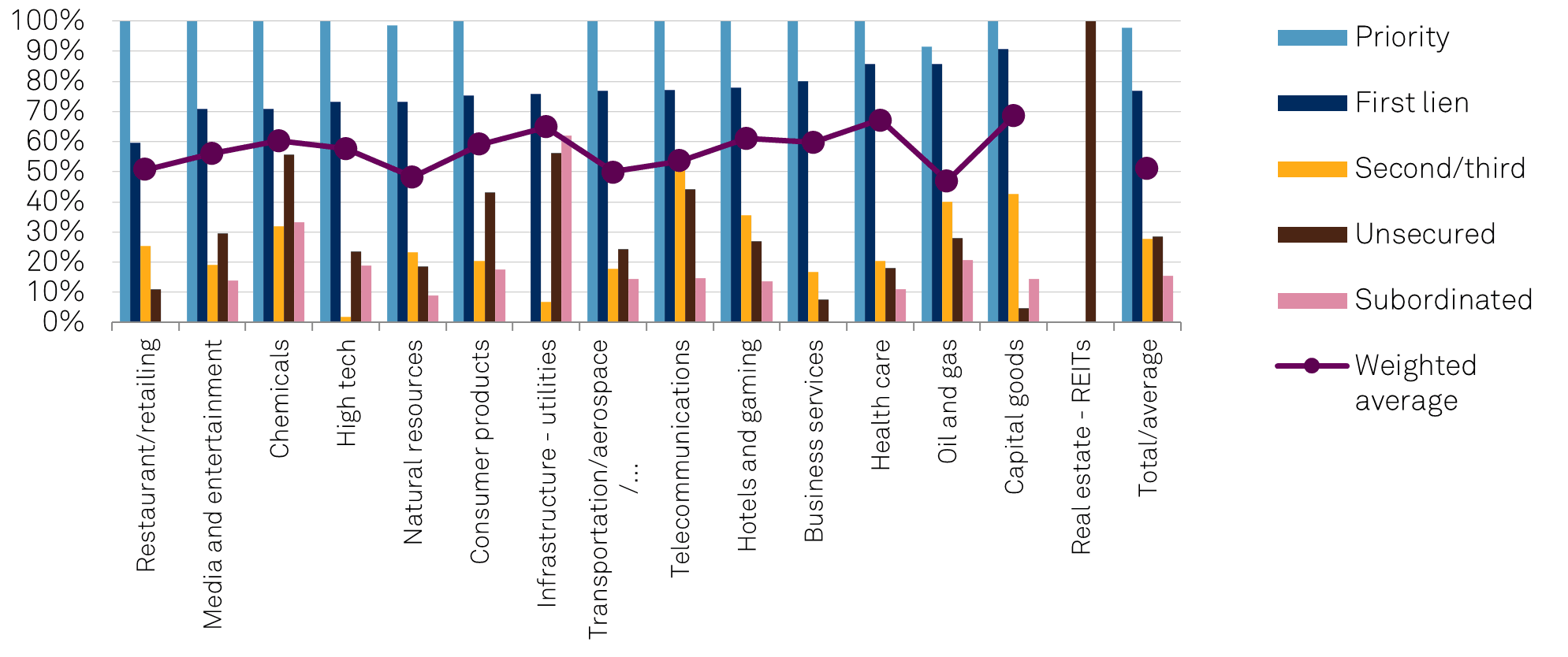

Over the past 13.5 years, recoveries for the companies we rate often differed by sector, by debt type, and in terms of weighted average recoveries (or average debt recovery rates for the entire company on a dollar weighted basis). These differences often reflect differences in debt structures by sector. An example is the first-lien debt recoveries in the oil and gas sector, which is the largest sector overall, with 91 companies in our 358-company dataset over the past seven years). This sector shows above-average recoveries of 86%, despite exploration and production companies typically having RBL facilities ahead of first-lien debt. This is because these companies also typically have a sizable cushion from large layers of unsecured and more junior debt (see Chart 3). These structural factors support first-lien recoveries in the sector notwithstanding it having the lowest proportion of first-lien debt.

Notably, current debt stacks in the sector have shifted away from multi-stacked structures to heavily unsecured debt, especially as lenders have reallocated holdings to meet environmental, social, and governance targets or socially responsible investment goals.

Other sectors had high average first-lien recoveries, including capital goods (91%) and health care (86%); together, these sectors had 29 companies in our dataset. In these cases, strong emergence valuations resulted in relatively high first-lien recoveries and weighted average recoveries despite a lighter debt cushion of junior and unsecured debt. The laggard in terms of first-lien recoveries was the retail sector, with an average 60% recovery rate due to secular pressures and high debt loads, including large priority ABL claims pushing down first-lien recovery rates. The impact of debt structure and mix is further illustrated by carving out nine restaurant companies from the larger retail group. These companies did not have any ABL facilities (except for three that had small priming revolvers in place), and they exhibited much higher average first-lien recoveries of 67%. From a weighted-average recovery perspective, the retail sector was in line with the 51% overall weighted average recovery rate. The key factor here is that ABL lenders benefitted from high recoveries due to top-heavy debt structures. The sectors with the highest weighted-average recoveries included capital goods (69%, with 15 companies) health care (67%, 14), and infrastructure (65%, 11).

Chart 10 - Average Actual Sector Recovery By Asset Class

As we’ve seen, the timing of a company’s exit from bankruptcy could significantly influence recovery expectations for lenders across the capital stack. And the pandemic highlighted how recoveries can vary during unprecedented economic turmoil. At the inception of the COVID-19 lockdown worldwide, with tremendous uncertainty and zero visibility plaguing companies and creditors alike, creditors settled for lower recoveries to mitigate further losses. Meanwhile, companies that emerged after the vaccinations rolled out to the general population benefitted from better recoveries overall.

This is because prospects were brighter as economic activity transitioned back closer to historical levels when people felt safer to venture out and travel. As with the Great Recession of 2007-2009 and the oil and gas downturn in 2014-2016, the pandemic has further reinforced S&P Global Ratings’ view that the timing of exits from bankruptcies have a significant impact on recovery levels. Just in the last six quarters, there’ve been exceedingly large swings in recoveries, as demonstrated by the low 42% weighted average recovery in the second quarter 2020 and the high of 57% in the second quarter of 2021.

Table 2 - Average Actual Recoveries By Sector

Of course, other factors affect recovery prospects as well, including changing trends in debt cushions over time and debt leverage and creditor terms thresholds that the leveraged loan market establishes will invariably impact recovery rates. With the pandemic continuing into 2022, and with the rapid spread of the Omicron variant globally, the return to normal will depend on several factors. These include threats of other pandemics and COVID-19 variants, inflation, additional global supply-chain disruptions, climate change-related disturbances, and domestic and foreign political shifts in power. While a new normal is being established, the timing of when and if these issues play out could have an unsettling effect on credit, distress, and default levels as well as on resulting recovery expectations.