Jan. 13, 2021

This report does not constitute a rating action.

David W Gillmor London +44-20-7176-3673

Maulik Shah CRISIL Global Analytical Center an S&P affiliate Mumbai

As a choppy economic recovery dominated by COVID-19-related considerations starts to develop, many private equity owners seem to be looking past immediate liquidity concerns. After the pandemic, they are considering whether their capital structures are sustainable, and moving to address weaknesses sooner, rather than later. S&P Global Ratings saw a high volume of distressed exchanges in the third quarter, in sharp contrast to the missed interest payments that dominated defaults in the second quarter of the year.

Although volumes are low, and so our conclusions are tentative, we would argue that owners may be exercising more control over the timing of distressed exchanges, making this a very different type of default.

This plays into a theme we have seen developing since 2019, where owners and management teams have become far more willing to actively restructure their financial obligations well in advance of any obvious liquidity issues. They seem to be addressing the issue as soon as they identify a chance that the capital structure could be unsustainable in the long term.

Given that the pandemic had a detrimental effect on many companies' capital structures, this trend could accelerate. During the downturn, we saw falling revenue, earnings, and cash flows at many leveraged companies, leaving them even more burdened with debt. In some cases, debt also rose to build liquidity.

Based on what we observed in the nine months to September 2020, we expect to see an increasing number of early defaults as owners and management teams move to address the impact of the pandemic on their capital structures.

The line between distressed and opportunistic restructurings can be difficult to see. To help stakeholders understand the difference, we contrast two recent situations, only one of which we view as a default.

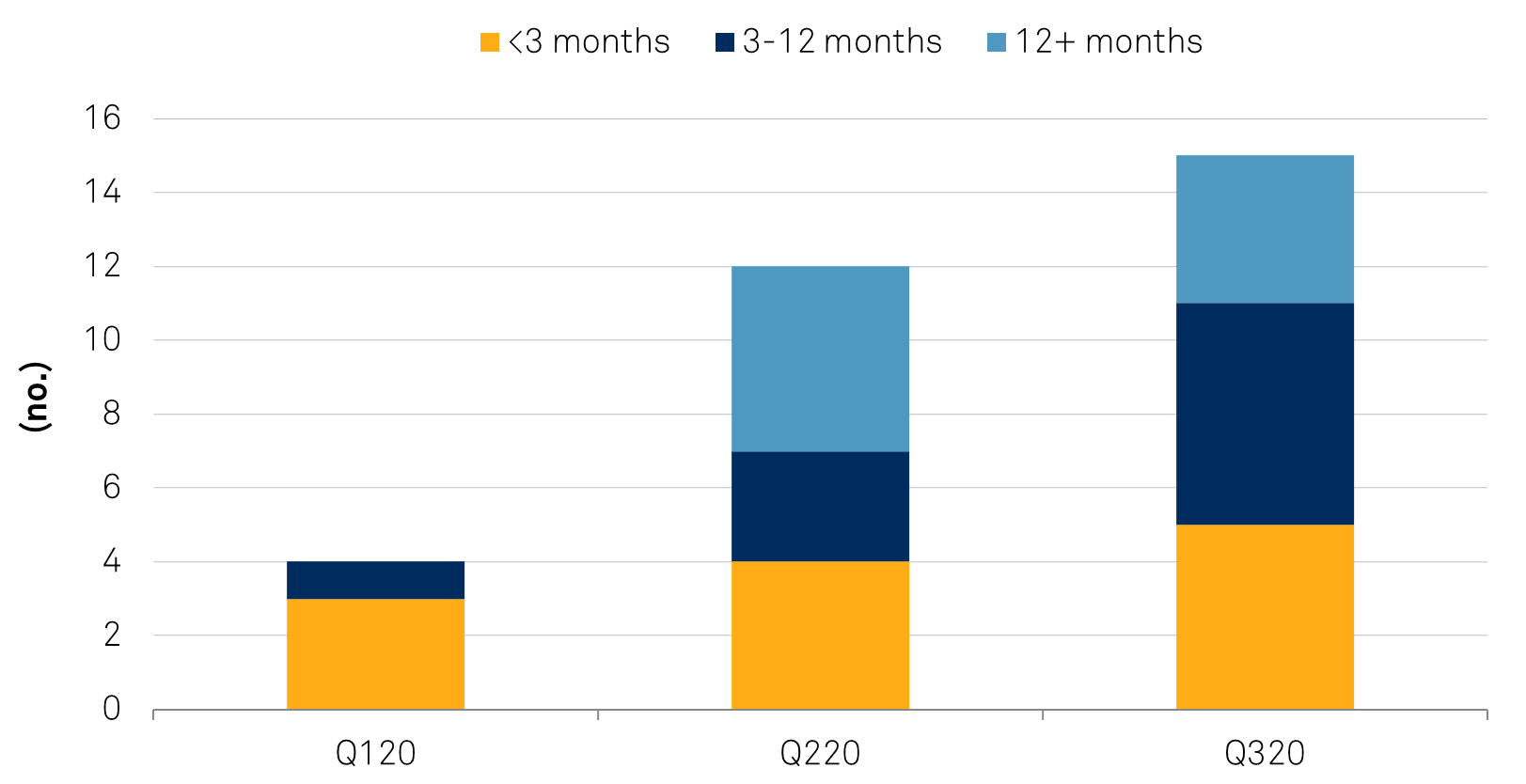

Chart 1 | Liquidity Wasn't The Key Default Trigger In 2020 Months of cash available when European companies defaulted

Source: S&P Global Ratings.

In the nine months to September 2020, approximately one-third of the corporate defaults we saw occurred in companies that we calculated had more than a year's worth of liquidity, based on our evaluation of their monthly cash burn rate at or approaching default. We recognize that most issuers default for reasons other than running out of cash. A strategic restructuring with sufficient liquidity is often viewed by the owner as the best course of action.

Given the uncertain economic outlook and the effect of the pandemic on balance sheets and end markets, we expect many companies will decide to fix their balance sheets by restructuring, some of which we will view as defaults.

Our forecast is for an 8% default rate in the year to September 2021, compared with the current run rate of 4.3% to September 2020

(see "Default, Transition, and Recovery: The European Speculative-Grade Corporate Default Rate Could Reach 8% By September 2021," published on Nov. 25, 2020)

Although the data points we have gathered so far are insufficient to confirm a rising trend, they certainly suggest that many owners are not waiting until the last minute, when cash is severely constrained. The owners are clearly proactively restructuring. Given the lack of financial covenants in most of the defaulted transactions, it is reasonable to conclude that the owners often precipitated these early defaults.

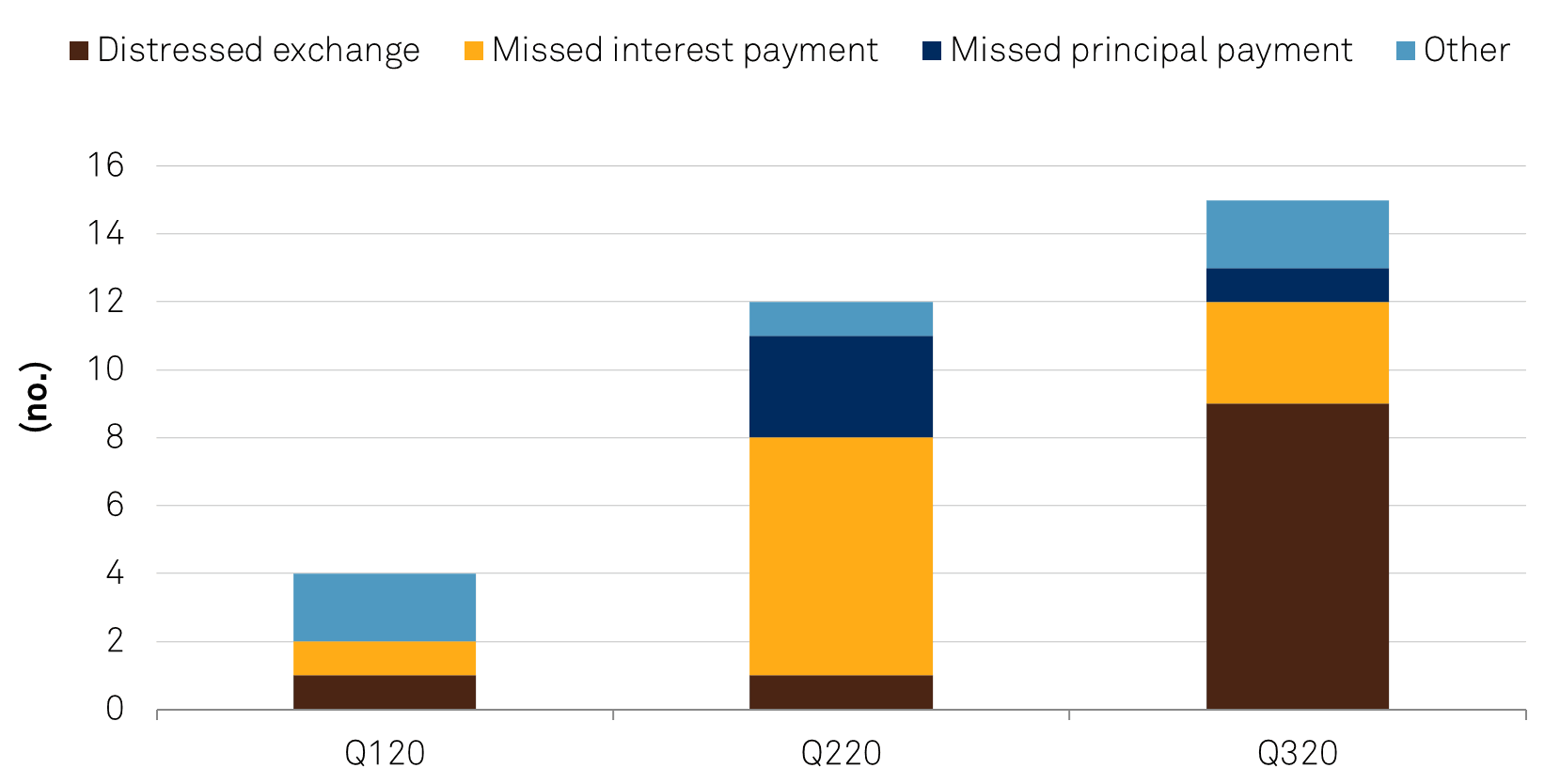

Of the 31 defaults we examined, 15 were due to a missed interest or principal payment, 11 were distressed exchanges, and all but one had been rated in the 'CCC' or 'CC' category before the default. Only two were deemed a bankruptcy--a private rating and Garret Motion Inc. In both cases, individual considerations affected the bankruptcy.

The high proportion of restructurings relative to insolvencies is in line with our recent empirical studies (see "European Corporate Recoveries Over 2003-2019: The Calm Before The COVID-19 Storm," published on Aug. 5, 2020).

Chart 2 | From Interest Payments To Distressed Exchange Defaults at European corporates

We saw a high volume of missed interest payments in the second quarter; but by contrast, in the third quarter, there were a high volume of distressed exchanges. Is this significant? Possibly.

In the first and second quarters of 2020, the focus for many companies was on short-term liquidity. Although market conditions were favorable, allowing many companies to raise new debt and extend existing maturities, many companies were clearly unable to do so, hence the missed interest payments.

By early June, most companies had dealt with the immediate liquidity threat. The focus then moved to capital structure. Specifically, the market wanted to know if companies had a capital structure appropriate for a postpandemic world. A significant proportion of the defaults in the third quarter were restructurings where we consider the company had a considerable short-term liquidity buffer.

It is a little early to claim that this is definite evidence of more proactive owner behavior, given the small data set, but we consider it a possibility. We will continue to gather and publish this data quarterly.

S&P Global Ratings reviewed all 31 defaults that occurred at rated corporates in the first three quarters of 2020. For each default, we estimated how many months the company could have continued to operate before it was unable to keep funding its losses--that is, how long before it would have run out of cash.

To calculate this figure, we took its available cash, plus any facilities that we considered it could realistically have accessed, then compared the result with the company's then-current monthly cash burn rate. This is not an exact science, so we banded the results into less than three months, three to six months, six to 12 months, and more than 12 months. We then assessed how this distribution compares each quarter.

We publish explicit criteria explaining how we approach the issue of default (see "S&P Global Ratings Definitions," published Dec. 7, 2020). Some of the options available to buttress a company's capital structure are defined as a default under our criteria, but not all. To help stakeholders understand the difference, we contrast two recent situations, only one of which we view as a default.

This example should provide some clarity, but, for the avoidance of doubt, is neither criteria nor guidance.

For a debt restructuring (or similar) to be considered a default, it needs to be viewed as distressed, rather than opportunistic, and specifically, the investor needs to receive less value than had been promised in the original contract.

The issuer credit rating is key to determining the difference between distressed and opportunistic restructurings, under our criteria. Our rating committee can also consider other elements, such as debt trading prices or how far in advance of maturity the restructuring occurs, but the issuer credit rating is the starting point. Specifically:

If the issuer credit rating is 'B-' or lower, the debt restructuring would ordinarily be viewed as distressed.

From this starting point, we consider a debt restructuring (such as an exchange, a repurchase, or a term amendment) distressed if in our view:

Conversely, we view a debt restructuring as opportunistic, rather than distressed, if we believe the issuer would be able to avoid insolvency or bankruptcy in the near to medium term, even if the debt restructuring did not take place. For example, a strong credit entity may offer to exchange or repurchase its bonds below par where changes in market interest rates or other factors have caused its bonds to trade at a discount. Such an offer is opportunistic.

To determine if the investor received less value than originally promised, we apply a number of tests. We consider that investors have received less value than promised in the original securities if one or more of the following happens without adequate offsetting compensation:

These tests appear quite simple, but are not, as the criteria does not explicitly advise what constitutes "adequate offsetting compensation." Even a small discrepancy between the restructured debt and the original promise may cause a restructuring to be deemed distressed. However, if the value of the restructured debt is so close to the original promise that it is hard to discern any shortfall, we would not characterize it as a default.

A rating committee will generally determine if a restructuring has failed any of these tests and therefore that the investor received less than the original promise. The committee evaluates both the magnitude of the shortfall and the amount of offsetting compensation.

To see how this works in practice, let's look at two recent examples: Promotora De Informaciones S.A. (Prisa) and Flint HoldCo S.a.r.l (Flint).

Although some senior lenders viewed the proposed Prisa restructuring as favorable to their interests, we regarded the Prisa proposal as a default.

Prisa had revenue in 2019 of about €1.1 billion (excluding Media Capital) and sells educational materials and resources such as textbooks through its subsidiary, Santillana. The group also has radio and press operations.

The company had been rated 'CCC+' since June 2020, as we considered the current capital structure unsustainable. Given this, it should not be a surprise that the proposed maturity extension was deemed to be distressed, rather than opportunistic.

We took the view that the amount of cash pay interest (0.5%, but only from 2023), together with the PIK interest, was not adequate compensation for the extension and the introduction of a €110 million basket for super senior ranking debt. The €400 million debt repayment was not considered part of the compensation for the extension because the company was already contractually obliged to repay this amount as part of the original promise.

As a result of these two elements, S&P Global Ratings advised that an 'SD' rating would be assigned if the proposed transaction went ahead. On Jan. 6, 2021, we downgraded Prisa to 'SD' (see "Research Update: Education And Media Group Prisa Downgraded To 'SD' Following Term Loan Modification Transaction"). We upgraded Prisa to 'CCC+' the following day (see "Education And Media Group Prisa Upgraded To 'CCC+' From 'SD' Following Transaction Completion; Outlook Negative").

We did not consider Flint to have defaulted. The company is a leading supplier of packaging applications, printing consumables, and equipment to the global packaging and printing industry.

Its product portfolio includes flexible packaging and paper and board inks, printing inks for print media, printing blankets, sleeves, pressroom chemicals, as well as digital solutions including web-fed digital color presses.

The company had been rated 'CCC+' since September 2019, as we viewed the current capital structure as unsustainable. In our view, the amount of cash pay interest (see table) was adequate compensation for the two-year term extension. In contrast to Prisa, there was no super senior debt introduced.

The table below details the key relevant differences to these restructurings.

Table 1 | Default Or Not?