Dec. 07, 2021

This report does not constitute a rating action.

The increase in credit risk for syndicated loans is notable and pervasive--encompassing higher default, recovery, and event risks.

Companies that rely on syndicated loans tend to have higher total and first-lien leverage than other speculative-grade issuers, which correlates to lower issuer credit ratings and first-lien recovery expectations.

Recovery expectations for first-lien debt have declined but remain meaningfully better than those for other debt classes.

Looser loan documents expose lenders to higher event risk because they provide firms with ample capacity to take actions that may increase credit risk.

Steve H Wilkinson, CFA New York + 1-212-438-5093

Ramki Muthukrishnan New York + 1-212-438-1384

If beauty is in the eye of the beholder, so is ugliness.

Much has been written about the decline in credit and document quality in the syndicated loan market--including by S&P Global Ratings’ corporate ratings group. The reality is more than just handwringing:

Even so, there continues to be a wide variety of opinions on the fallout for loan investors. Some warn that a doomsday scenario is inevitable, and others suggest the increased flexibility provided to leveraged borrowers by receptive credit markets and the optionality embedded in increasingly complex and flexible loan documents is ultimately beneficial to loan investors. The latter argument says these factors provide firms with avenues to take actions to survive and reduce losses (by frequency and, possibly, magnitude) if they are not forced into a sudden default and the longer and more expensive restructuring process this generally entails.

Our goal in this report is to help investors in broadly syndicated loans better understand the extent of higher credit risk, where these risks reside, and how they might come back to haunt investors.

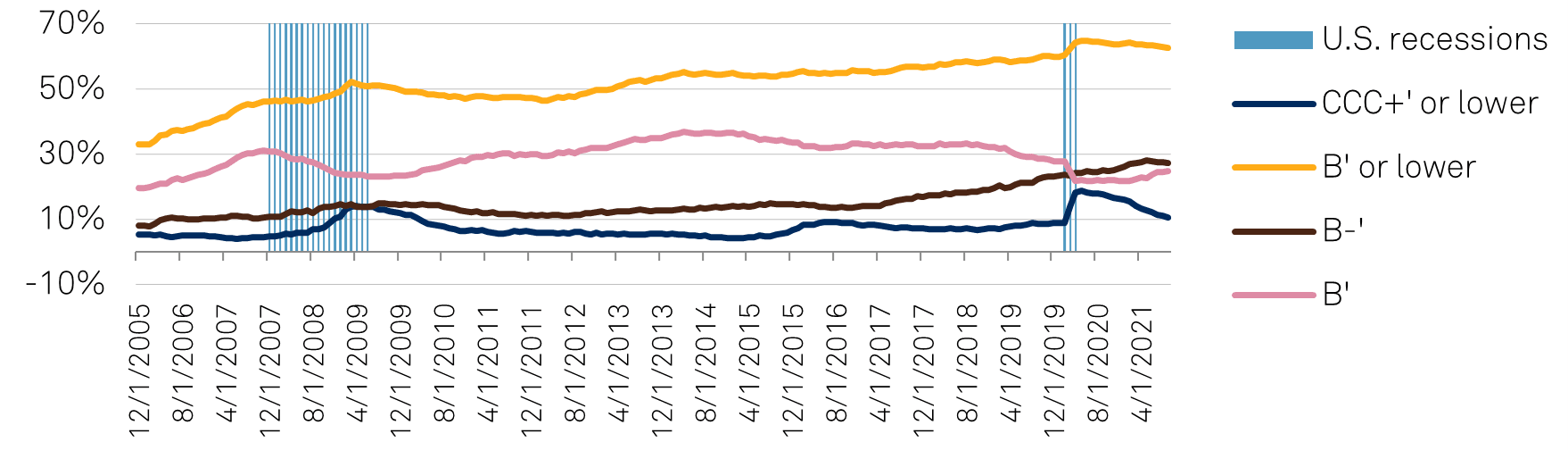

Over the past decade and a half, issuers with investment-grade ratings have declined from 42% at year-end 2005 to 32% at the end of September 2021. The median ICR has declined two notches to ‘B+’ from ‘BB’. Within the speculative-grade segment, the mix of ratings has declined even more dramatically. The concentration of companies rated ‘B’ or lower as a percent of all speculative-grade issuers has increased from about one-third at year-end 2005 to more than 60% since late 2019, with some retrenchment after periods of economic distress (Chart 1).

Chart 1 | North American Non-Financial Corporate Speculative-Grade Issuers Trend

Source: S&P Global Ratings. Data for U.S. and Canadian non-financial corporate entities, excluding entities rated 'D' or 'SD'.

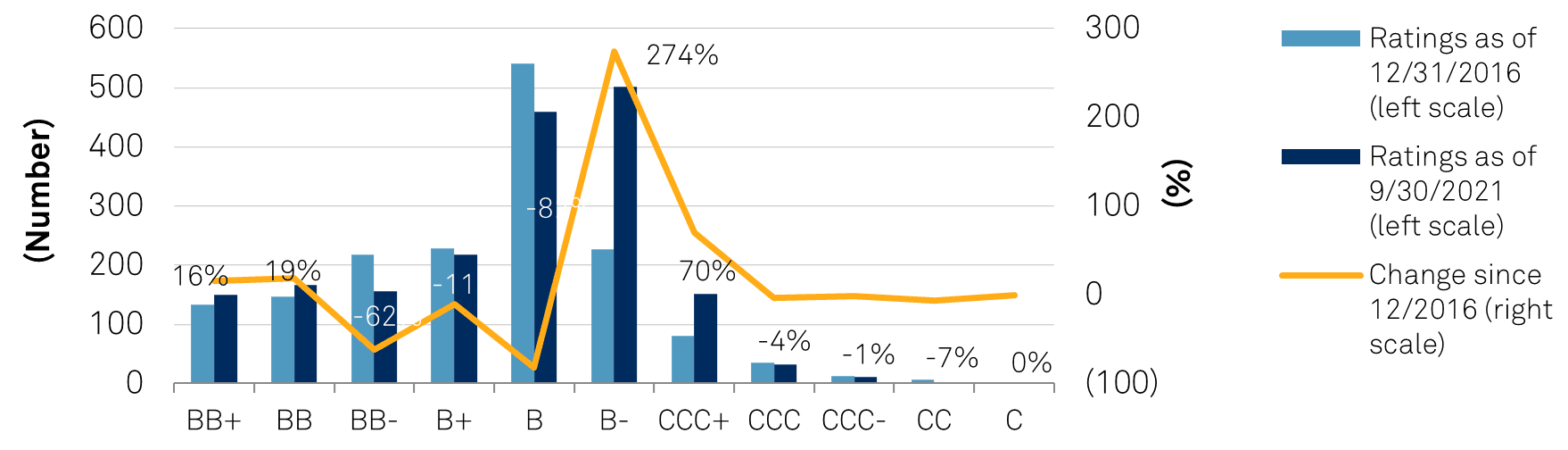

The increase in issuers rated ‘B-’ has been particularly strong, more than double since the end of 2016, while higher-rated speculative-grade issuers have decreased or remained relatively flat (Chart 2).

Chart 2 | North American Non-Financial Corporate Speculative-Grade Issuers Count

Source: S&P Global Ratings. Data for U.S. and Canadian nonfinancial corporate entities.

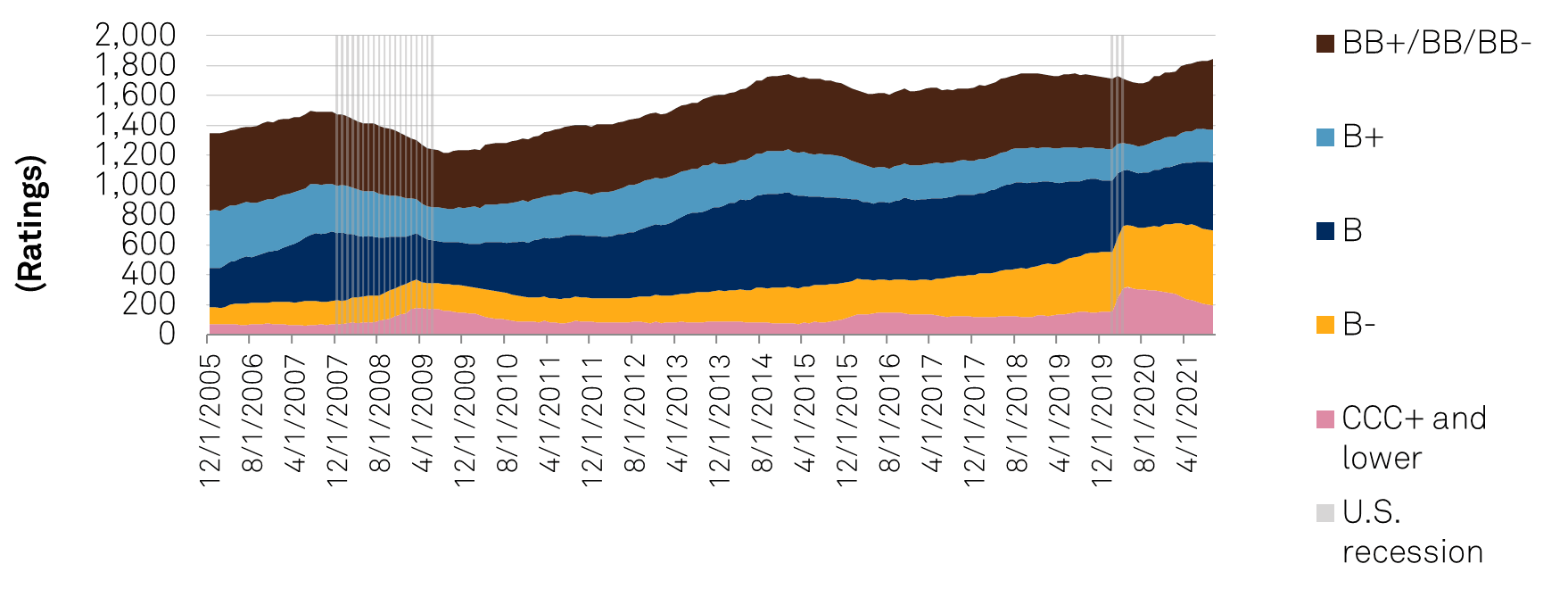

A key factor underlying these trends is a significant increase in the size of the speculative-grade universe, with the growth concentrated at lower ratings due to:

The number of North American speculative-grade non-financial corporate entities has increased 37% since year-end 2005 and 50% since July 2009 (following a contraction in rated entities due to the Great Recession).

The expansion was concentrated in companies rated ‘B’ from year-end 2005 through late 2007 and from the end of the U.S. recession in mid-2009 through late 2015. Investor thirst for yield spurred growth in the ‘B-’ category in early 2017, with the proportion of issuers rated ‘B-’ nearly doubling to 27% from 14% in 2016-2017 (Charts 2 and 3).

Chart 3 | Expanded Speculative-Grade Universe At The Bottom Rungs

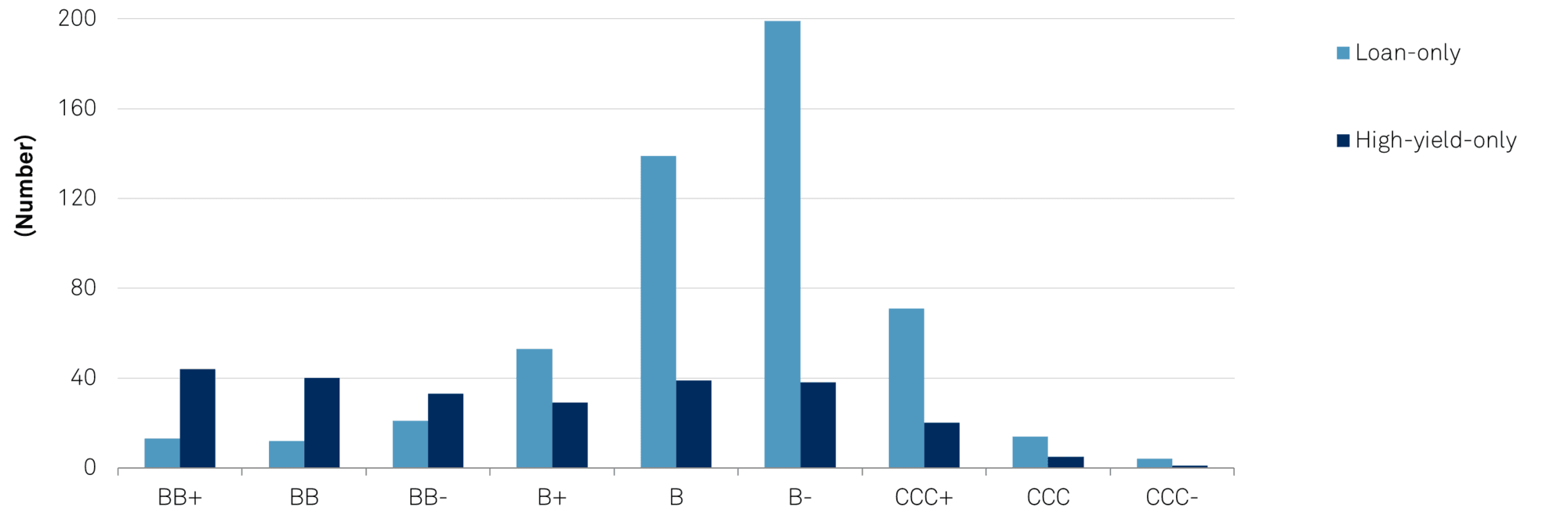

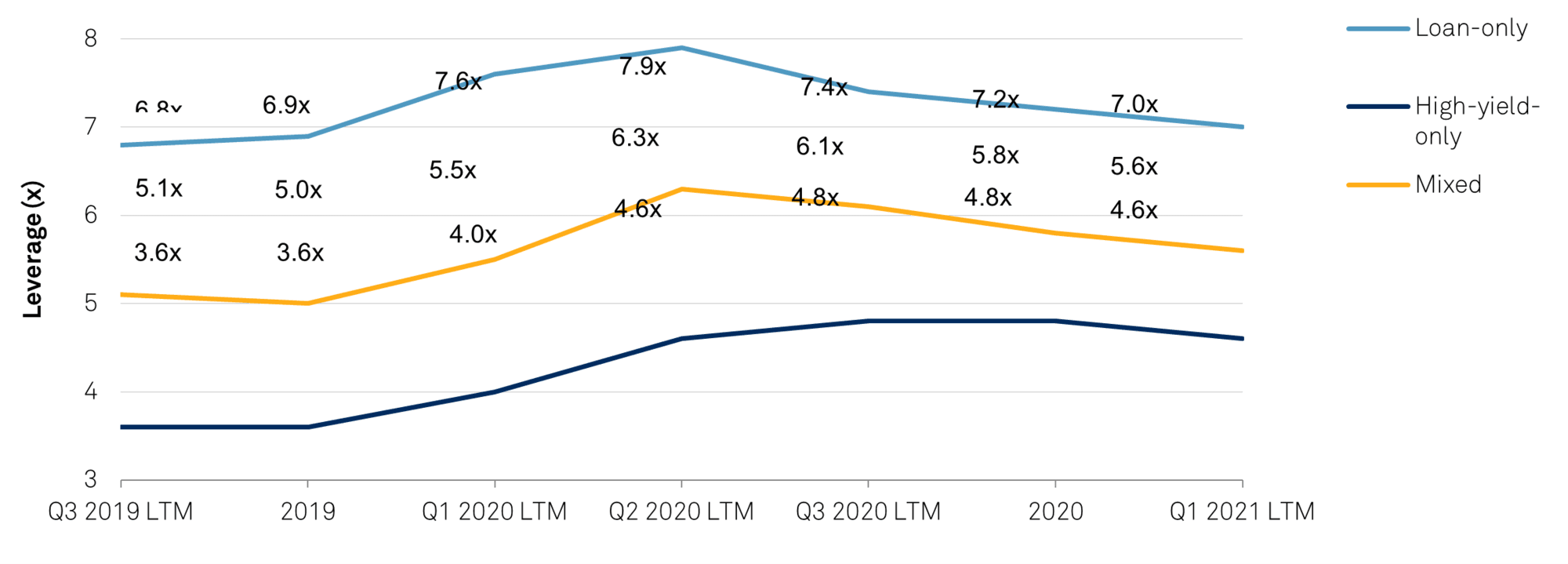

The mix of ICRs is even lower for loan investors, since companies that rely on loan financing tend to be smaller and more highly leveraged

(Charts 4 and 5; see “Leveraged Finance: U.S. Leveraged Finance Q2 2021 Update: Credit Metric Recovery Shows Sector, Rating, And Capital Structure Mix Disparities”, published July 20, 2021).

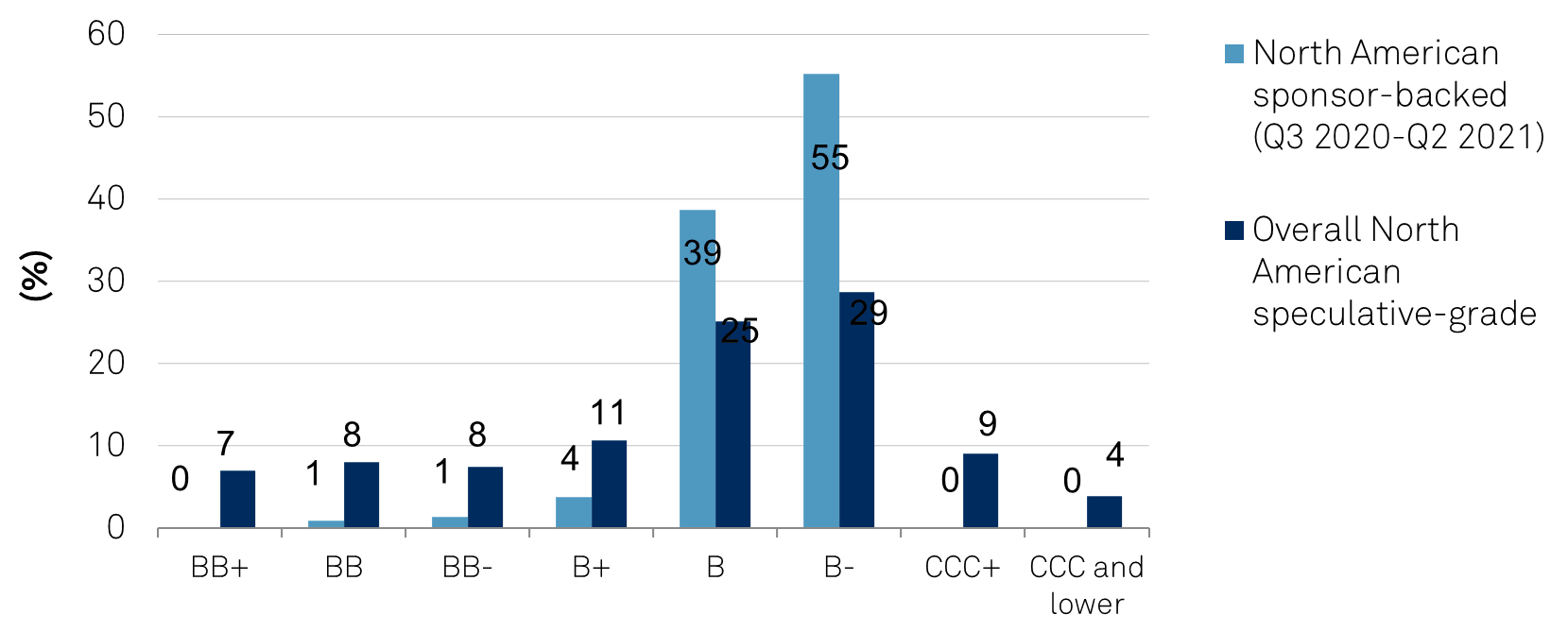

Many newly rated entities with low ICRs that rely heavily on loan financing are previously unrated firms that underwent LBOs by private equity firms. Higher financial risk is likely to persist given the more aggressive financial strategies these firms usually pursue (including debt-financed M&A and dividend recaps). While financial sponsors often emphasize how their involvement with acquired firms should improve access to capital, professional management, and expert guidance, the increase in financial risk is undeniable with the difference in leverage between sponsor-backed companies and speculative-grade borrowers at almost 1.7 turns on average and a median of 1.4 turns, according to data collected from 237 M&A transactions launched between July 2020 and June 2021. Further, many sponsor-owned companies are smaller with weaker business risk profiles, which also corresponds to lower ICRs (Chart 6).

Chart 4 | Issuer Credit Ratings: Loan-Only Versus High-Yield-Only Issuers

Ratings as of June 22, 2021. Source: S&P Global Ratings. A loan-only issuer in our sample (totaling 526 companies) has a rated debt structure that consists exclusively of loans, while a high-yield-only issuer (249 issuers) has a rated debt structure solely composed of high-yield bonds, according to debt rated by S&P Global Ratings. It is possible that a high-yield-only issuer has an asset- or reserve-based lending facility, cash flow revolver, or unrated term loan that we have not rated. Our larger data set also includes issuers with mixed debt structures (315 issuers), though we have not highlighted the statistics for this group because they largely sit between those of the other two groups. Differences in the size of the cohort of companies in these charts vs. the other charts in this article reflect: (i) the data for these charts only includes issuers that had publicly available financial statements for each period covered in Chart 5 at the time these charts were published; (ii) some elimination where ratings on multiple entities are based on the consolidated financial statements of a parent; and (iii) the exclusion of certain sectors from the data set in the Q2 2021 quarter Leveraged Finance article (Utilities, Regulated Transmission, Power Producers, and Infrastructure).

Chart 5 | Median Gross Leverage Transition: Loan-Only Versus High-Yield-Only Issuers

LTM--Lagging 12 months. Source: S&P Global Ratings. Ratings as of June 22, 2021. Source: S&P GlobalRatings. A loan-only issuer in our sample (totaling 526 companies) has a rated debt structure that consists exclusively of loans, while a high-yield-only issuer (249 issuers) has a rated debt structure solely composed of high-yield bonds, according to debt rated by S&P Global Ratings. It is possible that a high-yield-only issuer has an asset- or reserve-based lending facility, cash flow revolver, or unrated term loan that we have not rated. Our larger data set also includes issuers with mixed debt structures (315 issuers), though we have not highlighted the statistics for this group because they largely sit between those of the other two groups. Differences in the size of the cohort of companies in these charts vs. the other charts in this article reflect: (i) the data for these charts only includes issuers that had publicly available financial statements for each period covered in Chart 5 at the time these charts were published; (ii) some elimination where ratings on multiple entities are based on the consolidated financial statements of a parent; and (iii) the exclusion of certain sectors from the data set in the Q2 2021 quarter Leveraged Finance article (Utilities, Regulated Transmission, Power Producers, and Infrastructure).

Chart 6 | Ratings Distribution Of Sponsor-Backed M&A Versus Overall Speculative-Grade

Source: S&P Global Ratings. M&A--Mergers and acquisitions.

Notwithstanding benign expectations for default over the next year (reflecting improving economic conditions, abundant liquidity, and deferred maturities, among other factors) the potential increase in default risk over time, inferred by the distribution of ICRs, is striking in default statistics by ICR over the past 39 years (Table 1), which show a dramatic increase in average, median, and peak default rates for companies with ICRs at the low end of the ratings scale. For example, ‘B’ issuers default at nearly 3x the rate of ‘B+’ issuers and ‘B-‘ firms at more than 1.5x the rate of ‘B’ firms. Obviously, the jump in historical default rates is even more severe for companies in the ‘CCC’ category, but this more reflects issuers we downgraded due to underperformance and liquidity problems than it is of market tolerance for financing risk.

Table 1 | One-Year U.S. Corporate Default Rates By Issuer Rating (1981-2020)

Ultimately, the factors pushing up default risk are also pulling down expectations for recovery-given-default (as we and others have highlighted for years).

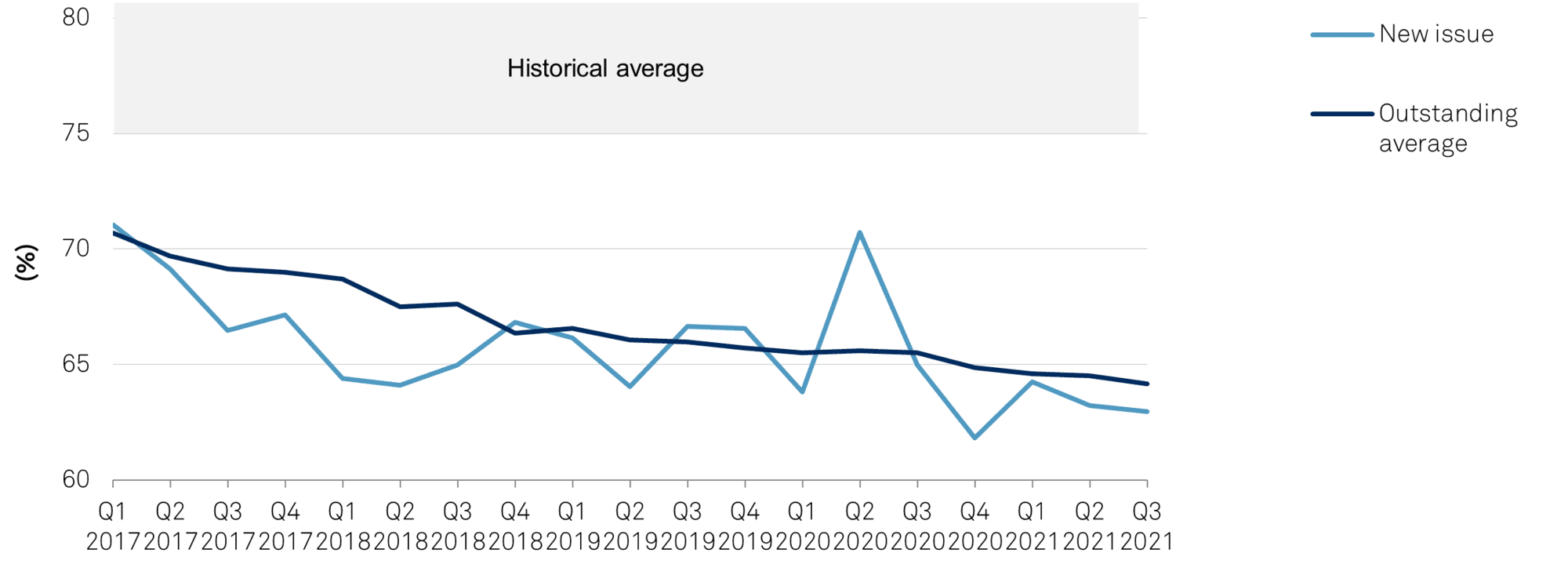

To start, higher leverage is generally inversely correlated with recovery rates after a default, as more debt seeks recovery from the same businesses/assets. However, the impact on first-lien loans has been exacerbated by the increase in total leverage that also fueled a preference for first-lien debt as companies (and sponsors) seek to lower the overall cost of capital. This is especially true for smaller, highly leveraged companies that are often too small to access the high-yield bond market. Financial sponsors also tend to prefer loans over bonds since they are more easily refinanced or repriced and the collateralized loan obligation (CLO) market provides a ready demand. As such, there has been an increase in first-lien-heavy and first-lien-only debt structures that contributed to lower recovery expectations for first-lien debt. Recovery prospects (as approximated by the rounded estimates underlying our recovery ratings) are now consistently, and meaningfully, below historical average actual recovery rates. These are generally cited in the 75%-80% range for first-lien debt on an ultimate (or post-restructuring) basis (Chart 7).

Chart 7 | Average Recovery Estimates For Speculative-Grade Debt

Source: S&P Global Ratings. Data with rounded estimates for all outstanding first-lien debt (loan plus notes/bonds) for U.S. and Canadian non-financial corporate entities.

To a lesser extent, the dominance of covenant-lite term loan structures in the syndicated loan market also contributes to lower actual and expected recovery rates (see Related Research).

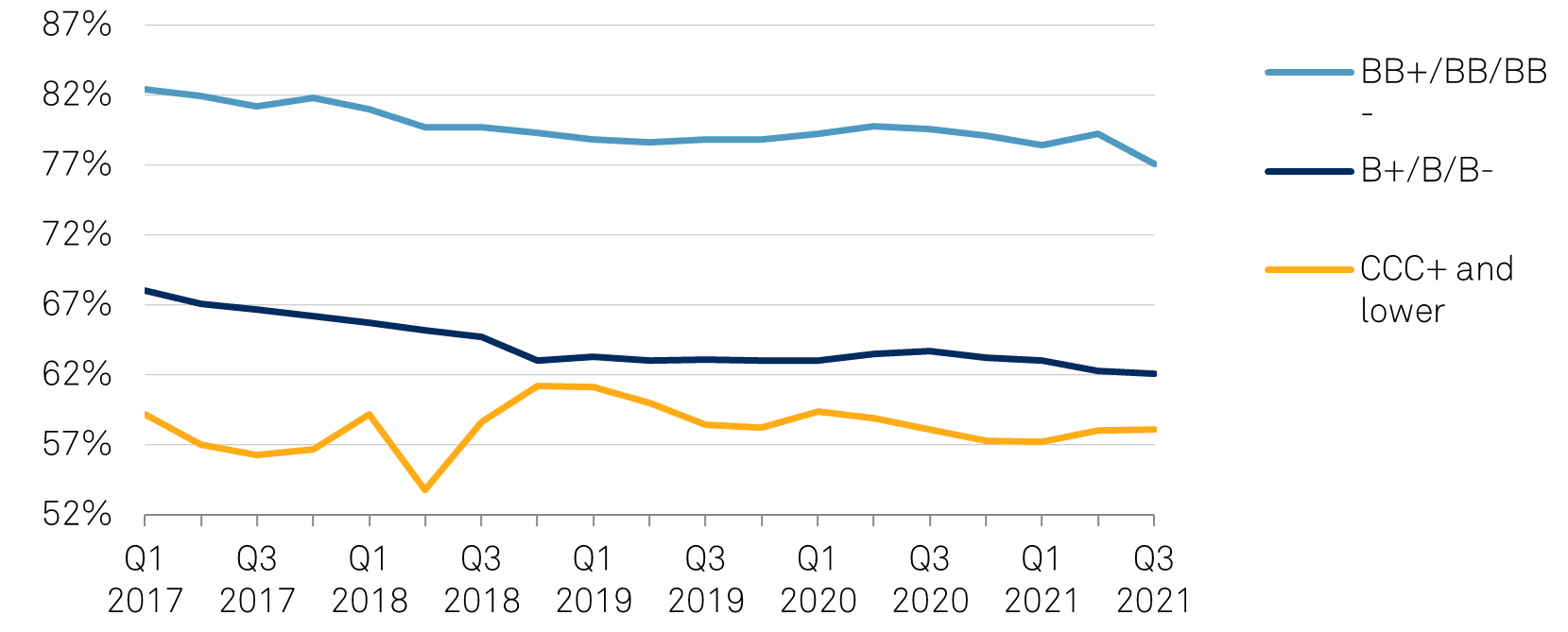

Recovery prospects for first-lien debt by ICR category since the first quarter of 2017 provide more insight (Chart 8). The data show that average first-lien recovery expectations are significantly better for higher-rated speculative-grade companies, particularly in the ‘BB’ category. Total leverage is typically lower, and issuers are more likely to have a layer of unsecured debt that provides a cushion against losses to first-lien creditors.

Chart 8 | Average First-Lien Recovery Estimates By Rating

Even so, there has been a gradual decline in recovery expectations for first-lien debt issued by ‘B’ category (B+/B/B-) and ‘BB’ category (BB+/BB/BB-) credits, with average respective recovery expectations declining 5.9% and 5.4% over this period.

Recovery expectations for companies rated ‘CCC+’ and lower declined less significantly, about 1.1% over this period, and exhibited much more variability (up and down). The size and composition of this group shifts over time. Many of these distressed companies default, and they either restructure or we withdraw our ratings.

From an attribution standpoint, about 80% of the decline in overall average recovery expectations is due to declines within each ICR category, as capital structures have become more leveraged and first-lien-heavy. Attribution was calculated by holding the mix of issuers constant with the first quarter of 2017 but updating recovery rates by ICR category based on the averages in the third quarter of 2021. The remaining 20% of the deterioration reflects the increased concentration of companies with lower ICRs due to the expansion in the rated universe (holding average recovery rates by ICR constant at first-quarter 2017 levels but reflecting the worsening mix of borrowers rated ‘B+’ and lower, expanding to nearly 83% of all speculative-grade companies from about 76%).

Event risk--including the possibility a company will materially increase debt (and leverage) or reshuffle debt priorities beyond what was expected at origination--is another recovery wild card that loan investors need to consider. While our recovery ratings are grounded in our forward-looking default-scenario analysis, recovery prospects can change as circumstances evolve. Our recovery analysis considers sufficient stress to trigger a default, that revolving debt facilities will be substantially drawn prior to default, and that bankruptcy/restructuring expenses will absorb 5% of a defaulted firm’s enterprise value. In addition, we cap recovery ratings on unsecured debt and any debt when we expect the restructuring to be completed in countries with insolvency laws that we view as unreliable or not creditor friendly.

We typically base our recovery analysis on a company’s current debt structure because changes tend to be unpredictable and unquantifiable. Further, the size and relative priority of any new borrowings and the use of such proceeds (M&A, refinancing, dividends, etc.) can significantly affect all aspects of our analysis. This includes the path and likelihood of default; claim amounts; valuation given default; and relative priorities. As such, we typically capture these events in our ratings as part of our surveillance process.

Still, it is important to recognize that loan terms and conditions have meaningfully weakened over the past half-dozen years or so, even for companies at the low end of the speculative-grade scale (see Related Research). As we understand it, weaker loan terms more reflect the limited negotiating power of individual loan buyers that need to put money to work than investor acceptance of various provisions per se. Still, the result is the same.

Increasingly loose and malleable loan terms can provide companies with ample capacity to take actions that increase risk, even for first-lien creditors that sit at (or near) the top of the debt stack. Weak loan terms include significant capacity to increase debt, transfer assets, or pay dividends by virtue of numerous “free and clear” baskets and loose incurrence tests, amplified by expansive EBITDA definitions in loan documents that generally define the capacity to take such actions. Moreover, potential restrictions historically provided by financial maintenance covenants have significantly deteriorated now that covenant-lite term loan structures (with no financial maintenance covenants) dominate the institutional loan market. While some may point to the financial maintenance, covenants that still (nearly always) exist on cash flow revolvers as offering protection, these are springing and only tested if a pre-set borrowing threshold is met (often 25%-40% of the revolving commitment).

Typically changes in debt structure do not dramatically impair recovery prospects for first-lien creditors. Still, the dramatic reduction in first-lien recovery prospects from certain extraordinary (but not explicitly prohibited) restructuring actions taken by certain distressed firms in recent years has been alarming for some investors. The most controversial and aggressive tactics are collateral transfers and priming loan exchanges.

Table 2 | Recovery Impairment From Aggressive Restructuring Actions

Source: S&P Global Ratings.

The reduction in expected par recovery rates for seven collateral transfer transactions completed from July 2017 through September 2020 (Table 2) was significant at about 25% on an average and median basis (reductions of about 40% versus pretransfer expectations on an average and a median basis). For seven priming loan exchanges completed from June 2018 and January 2021, the average recovery rate decline in par was 36% and median was 50%, with percentage reductions of 71% on average and a 91% median. While these cases were dramatic and high profile, these restructuring tactics have been rare and, more to the point, are impossible to predict and quantify. Further, we do not believe rating to a worst-case scenario is reasonable or value-added to investors. As a result, we do not prospectively capture these risks in our recovery analysis, although we will continue to monitor these events to see if there is a useful way to indicate these risks or proactively factor them into our ratings.

Irrespective of the lack of warning lights from market indicators and actual defaults, we view the increase in credit risk in the broadly syndicated loan market as real and pervasive with higher risk evident from default, recovery, and event risk perspectives.

These changes reflect higher tolerance of financial risk, by companies and debt markets, which has contributed to higher leverage and reduced recovery expectations for first-lien debt.

If one seeks a bright spot, it may be that the meaningful expansion of the rated universe improves the transparency and the monitoring of credit risk.

We think investors should remain mindful of the following points:

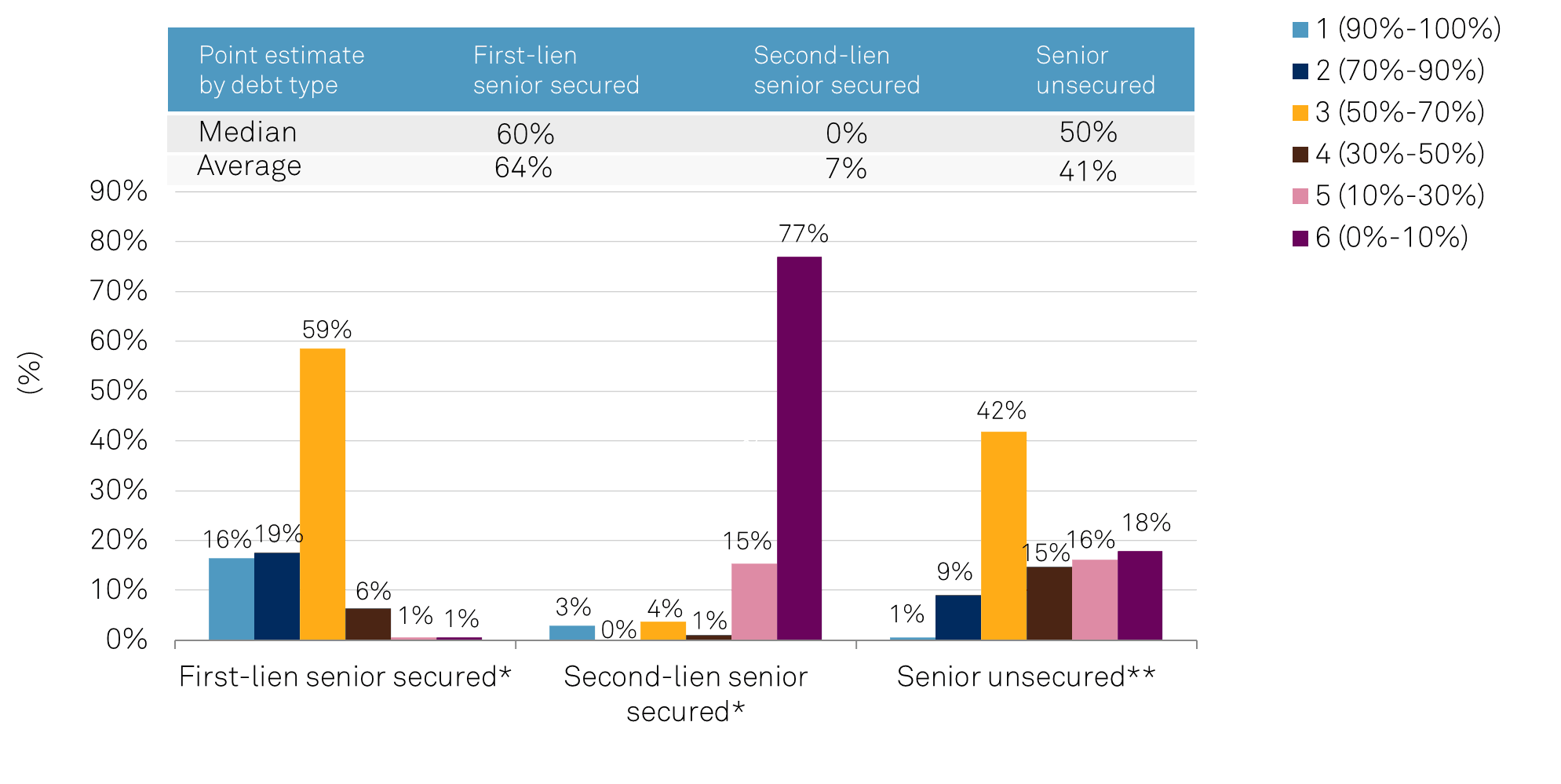

Chart 9 | Recovery Rating Distribution First- and second-lien senior secured vs. senior unsecured

Source: S&P Global Ratings. *Includes notes and loans as Oct. 21, 2021. **Includes notes, medium-term notes, bonds, and debenture as of Oct. 21, 2021.

In our view, potential for these risks to come back to haunt loan investors remains material, as there is no guarantee the next economic downturn will be accompanied by the same extraordinary fiscal and monetary stimulus provided by the U.S. federal government or that the rebound will be as fast. Further, inflation has resurfaced and may lead to higher interest rates, which would squeeze coverage ratios and cash flows and undermine a key justification for the market’s acceptance of higher leverage.