Oct. 19, 2021

This report does not constitute a rating action.

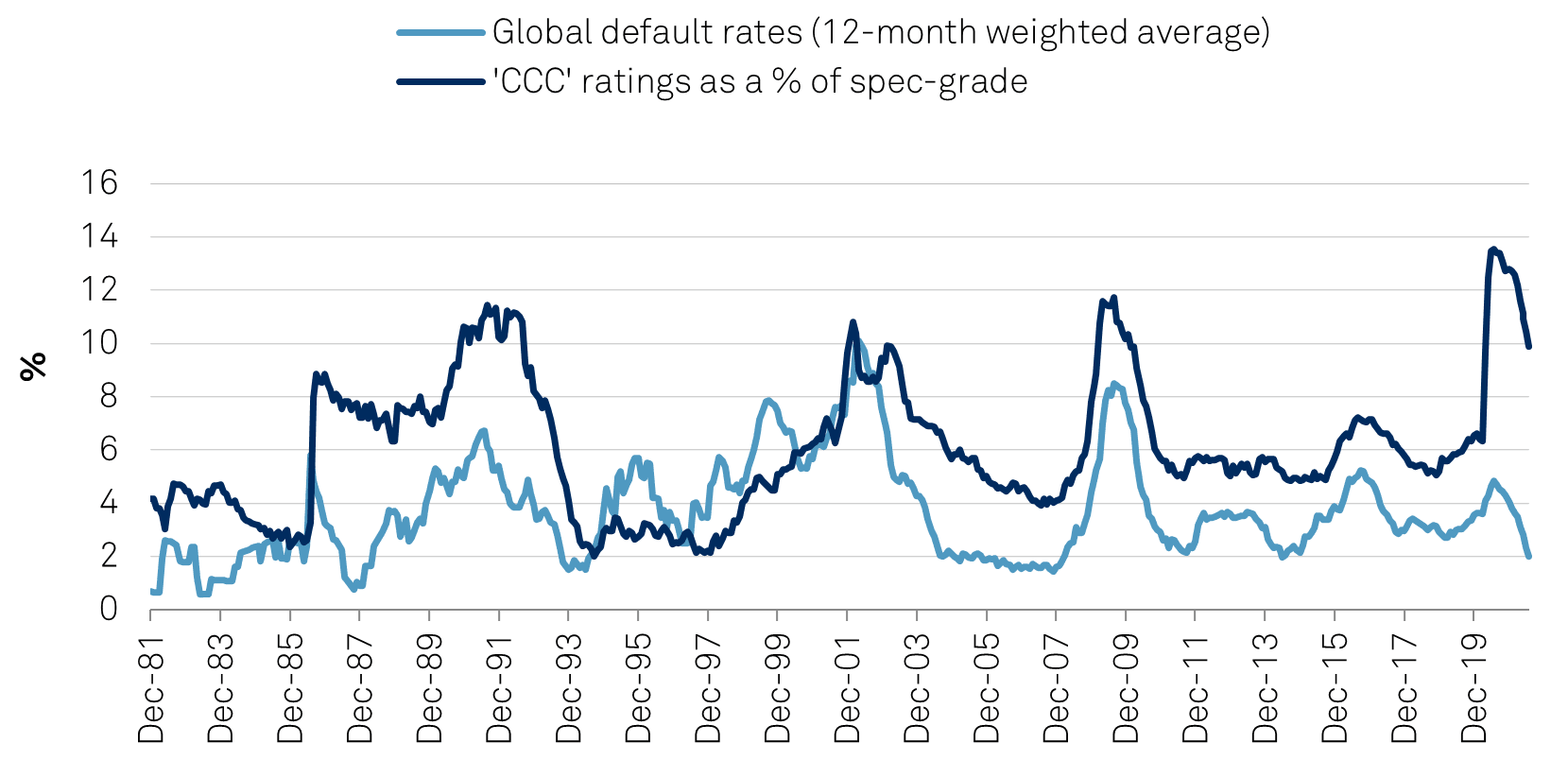

Only 16% of 'CCC' rated issuers defaulted over the last 12 months compared with a historical average of 35%.

The severe impact of the pandemic caused downgrades of companies with relatively stronger businesses compared with those downgraded pre-pandemic, which means their recovery prospects may be greater as restrictions are lifted.

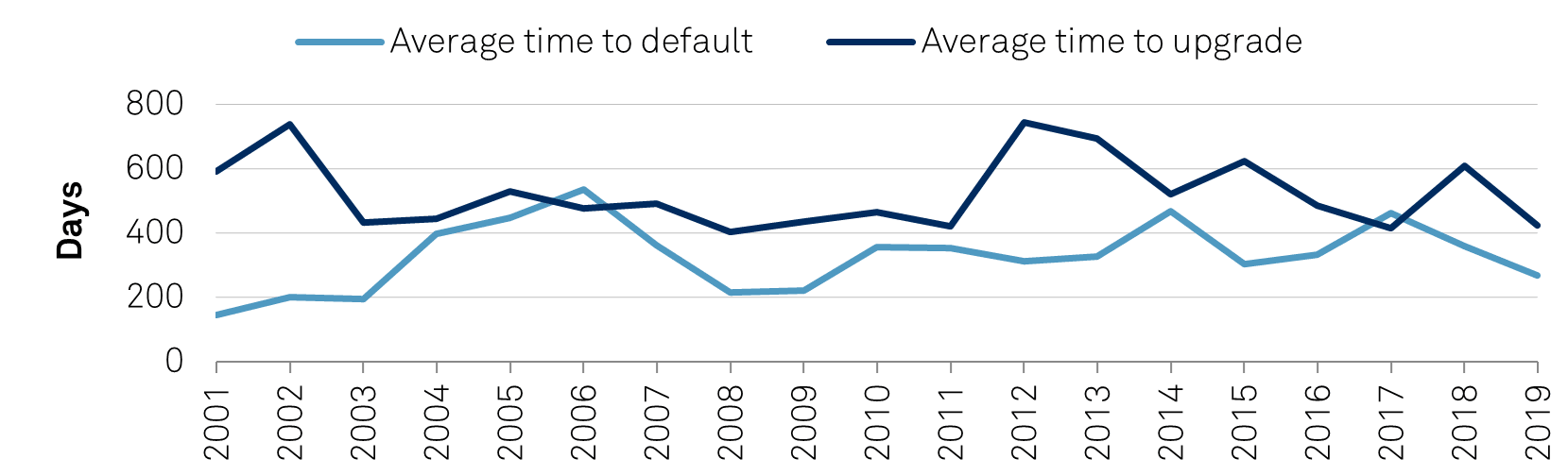

Upgrades out of the 'CCC' category historically take longer in the years following a major crisis as sustainability of credit metrics improvement needs to be proven.

However, default rates could pick up in 2022 if growth and deleveraging prospects stall and key lifelines such as unprecedented policy support and accommodating debt capital markets--essential for the weakest companies--disappear.

Nicole Serino New York +1-212-438-1396

Gregoire Rycx Paris +33-1-4075-2573

Marta Stojanova London +44-20-7176-0476

The initial credit shock of the COVID-19 pandemic on the most vulnerable issuers was severe and fast, as the proportion of issuers rated 'CCC' and below ballooned to record highs.

Most of the issuers downgraded at the beginning of the pandemic were seriously affected by health measures and social distancing protocols as both governments and societies responded to the global crisis. Despite the number of 'CCC' issuers spiking to record levels, speculative-grade default rates have not, peaking at half their levels seen in the 2008 financial crisis and then dropping rapidly.

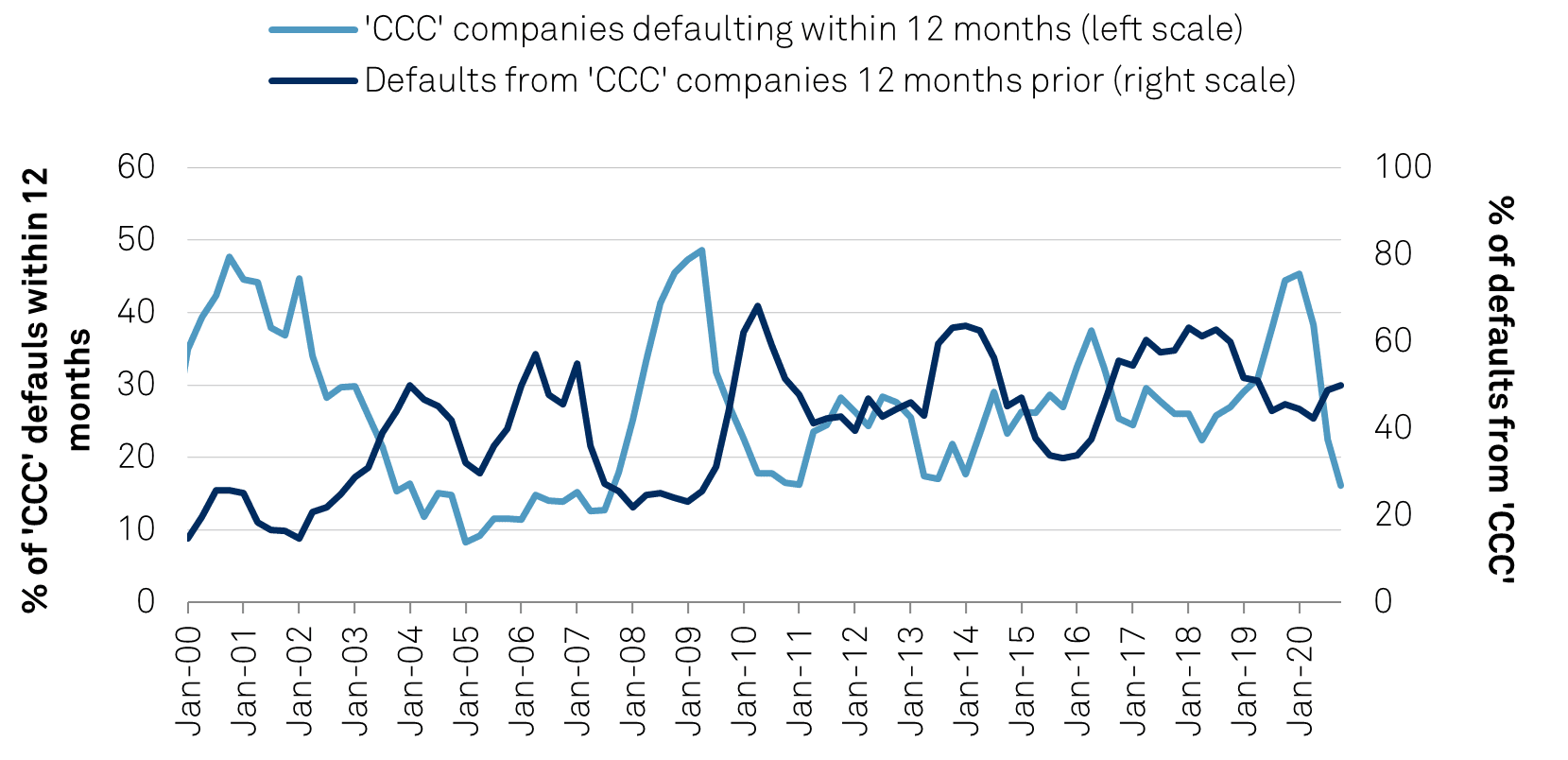

Typically, more than a quarter of companies rated 'CCC' default within 12 months, spending on average 10 months in the rating category before defaulting. However, only 16% of companies rated 'CCC' as of July 2020 defaulted in the subsequent 12 months. This divergence between the percentage of 'CCC' ratings and default rates that occurred in the middle of 2020 is likely due to the abundance of government and central bank support, capital markets' fast rebound, and largely supportive owners--all providing a lifeline to corporate issuers.

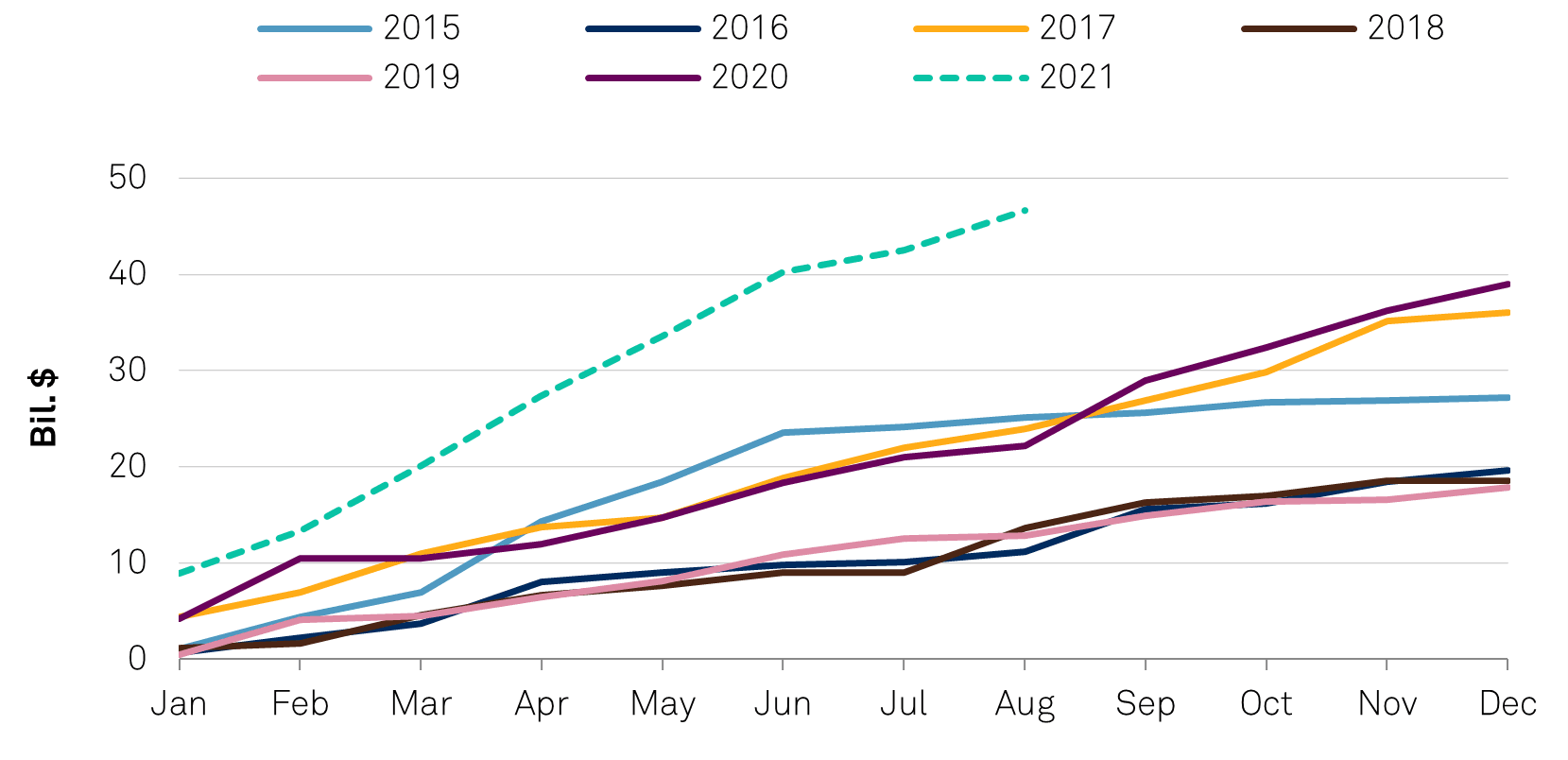

The low interest rate environment and appetite for yield has fueled speculative-grade issuance, which reached $508 billion in August as issuers at even the lowest rating categories have been able to borrow cheaply (see chart 3).

Strong by historical standards, upgrades have largely outpaced downgrades in the 'CCC' space, and absent any external shocks to the market, we can expect to see the upward trend continue in the near term, temporarily weakening the relationship between the share of 'CCC' companies and the corporate default rate.

Chart 1 | Unprecedented Divergence Between Default Rates And 'CCC' Levels

Data as of Aug. 31, 2021. Default rate calculations are based on a 12-month weighted average. Source: S&P Global Market intelligence CreditPro and S&P Global Research.

Chart 2 | Only 16% Of The Companies Rated ‘CCC’ Have Defaulted Over The Past 12 Months

Data as of Sept 30, 2021. Source: S&P Global Ratings.

Chart 3 | 2021 S&P Global Ratings-Rated 'CCC' Issuance Has Shattered Its Previous Year-End Totals

Note: Data includes financial and nonfinancial corporates and excludes sovereign. Data as of Aug. 31, 2021.Sources: S&P Global Ratings, Refinitiv.

A large share of the downgrades to the 'CCC' category stemmed from our view of unsustainable balance sheets and deteriorated financial metrics.

While it is in many cases too early to tell the long-term implications for some sectors of the economy, our assessments of the business risk profile (BRP) for these companies have largely remained unchanged globally so far, which could suggest a relatively rapid normalization of activity as restrictions fade away.

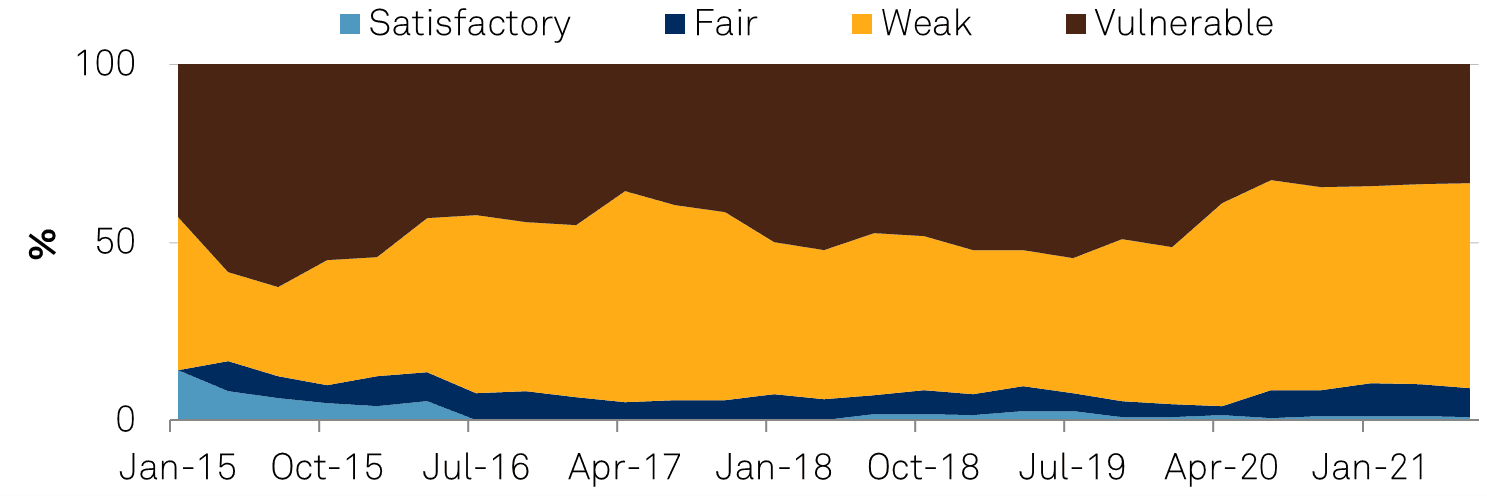

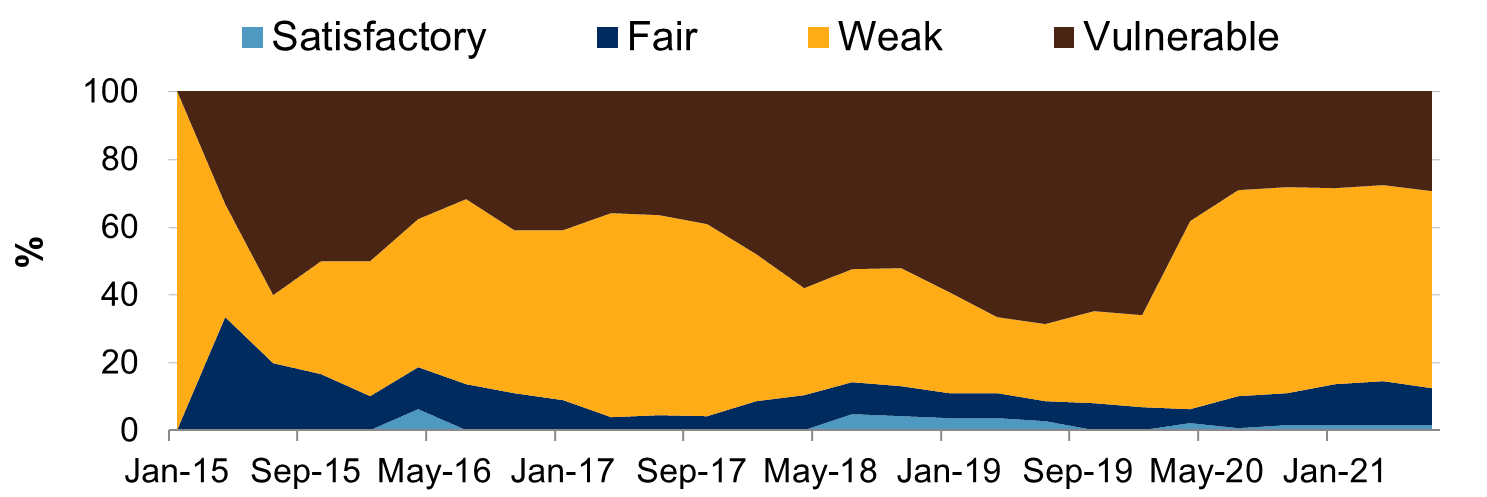

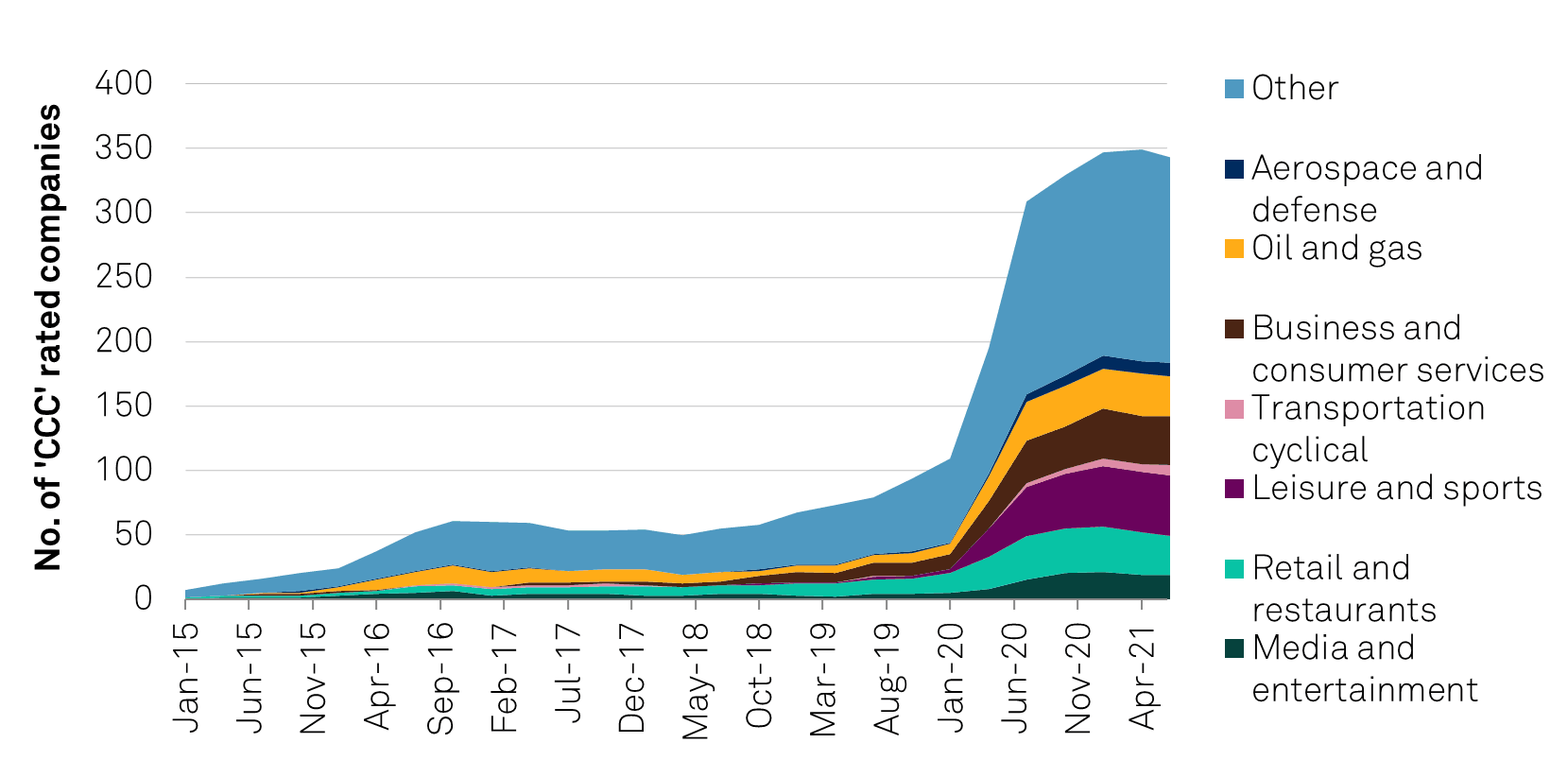

Before the pandemic, more than half of the companies within the 'CCC' category had a vulnerable BRP. Such companies are very small with a weak market position and intense competition, and they operate in secularly declining industries, such as print-based advertisers, certain brick-and-mortar retailers, etc. This number fell to 30% as of the end of the second quarter of 2021, as relatively stronger companies entered the category due to the material impact of the pandemic on their operations. This phenomenon is even more visible in the hardest-hit industries (leisure, transportation, retail, aerospace, oil and gas, and consumer services), which represent over 55% of the total number of 'CCC' rated companies and for which the share of these with a vulnerable BRP has halved since the pandemic.

Chart 4a | Global Nonfinancial 'CCC' Rated Companies

Data as of July 31, 2021. Source: MicroStrategy.

Chart 4b | 'CCC' Rated Companies From Disrupted Sectors

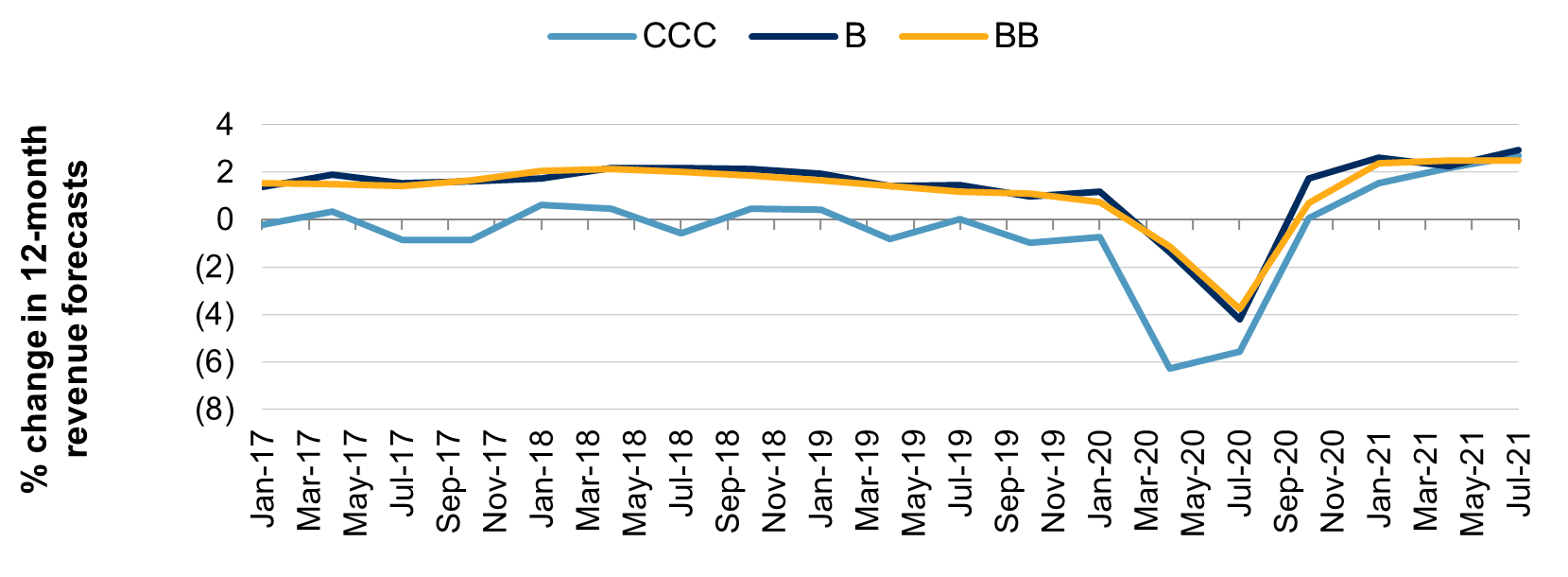

Because the 'CCC' rated companies now on average have stronger BRPs, this translates into unusually strong growth (see chart 7) and deleveraging (see chart 8 and 9) prospects, which should eventually support a positive transition out of the category.

Although it is uncommon for 'CCC' rated companies to have strong deleveraging prospects, it reflects the uncertainty around our base case when it relies upon favorable business, financial, and economic conditions (end of travel restrictions, normalization of consumption habits).

Chart 5 | Disrupted Sectors Make Up Over Half Of The 'CCC' Category

Data as of Sept 30, 2021. Source: MicroStrategy.

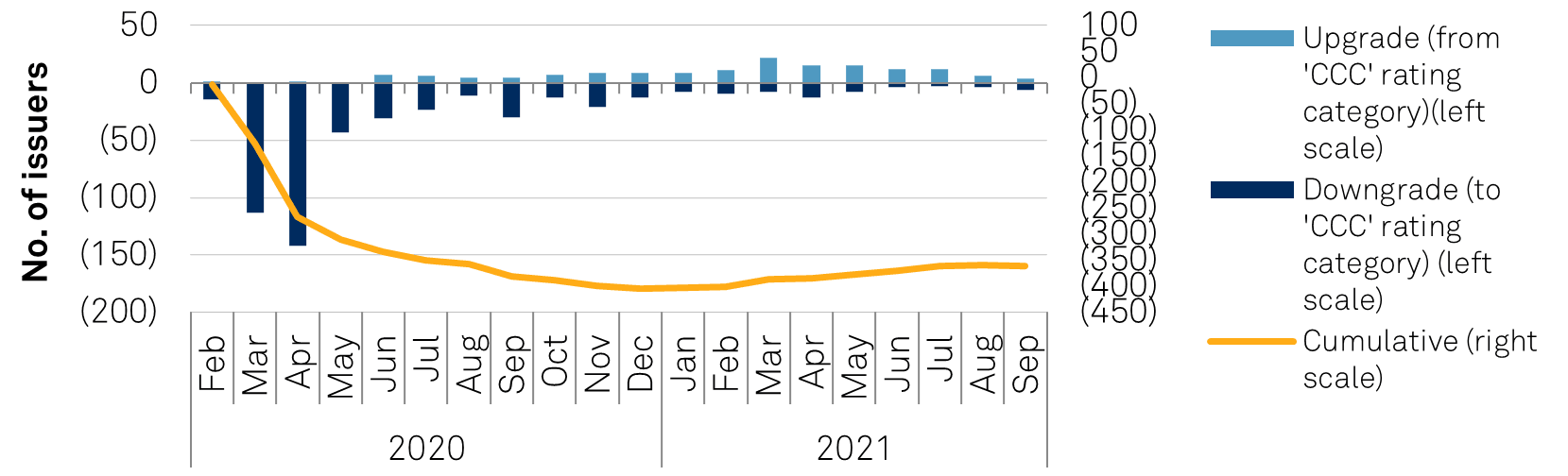

Even so, the signs of stabilization--and, in time, recovery--from the 2020 downgrade wave are noticeable. Several companies were upgraded out of the 'CCC' category only a short time after being downgraded due to the pandemic. We distinguished three profiles of companies that have rapidly emerged out of ‘CCC’:

As the first two profiles of companies mentioned above are opportunity-driven and were allowed by the supportive financing conditions, we can expect the number of upgrades to gradually decline in the coming months as business performance becomes the main driver of rating actions. However, as shown in chart 10, it is customary for upgrades out of the 'CCC' category to take longer in the years following a major crisis (such as in 2001-2002 and 2010-2013) as uncertainties take time to dissipate, credit metrics improve, and the improvement is seen as sustainable.

Chart 6 | Upgrades Out Of ‘CCC’ Gained Momentum Since The Beginning Of 2021

Note: Cumulative net changes are the absolute sum of net ratings change since Feb. 2, 2020. Data as of Sept 30, 2021. Source: S&P Global Ratings.

Chart 7 | Average Change In Rolling-12-Month Revenue Forecasts* Per Rating Category

*Revenue forecasts for the next 12 months. In the middle of a company’s fiscal year, its 12-month revenue forecast is the average of the revenue forecasts for n and n+1. Data as of July 31, 2021. Source: MicroStrategy.

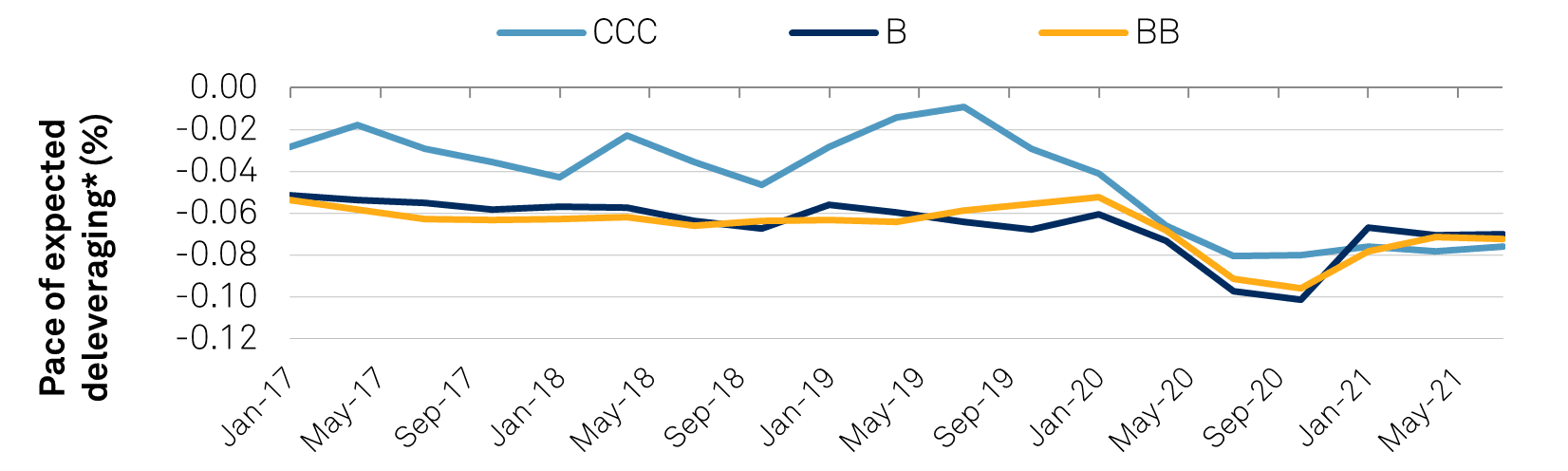

Chart 8 | 'CCC' Ratings Show Fastest Deleveraging Prospects…

*Pace of expected deleveraging as a percentage of first projected year leverage. Note: N+1 (or first projected year) corresponds to the ongoing fiscal year (for instance FY2021 if fiscal year ends in December). Data as of July 31, 2021. Source: MicroStrategy.

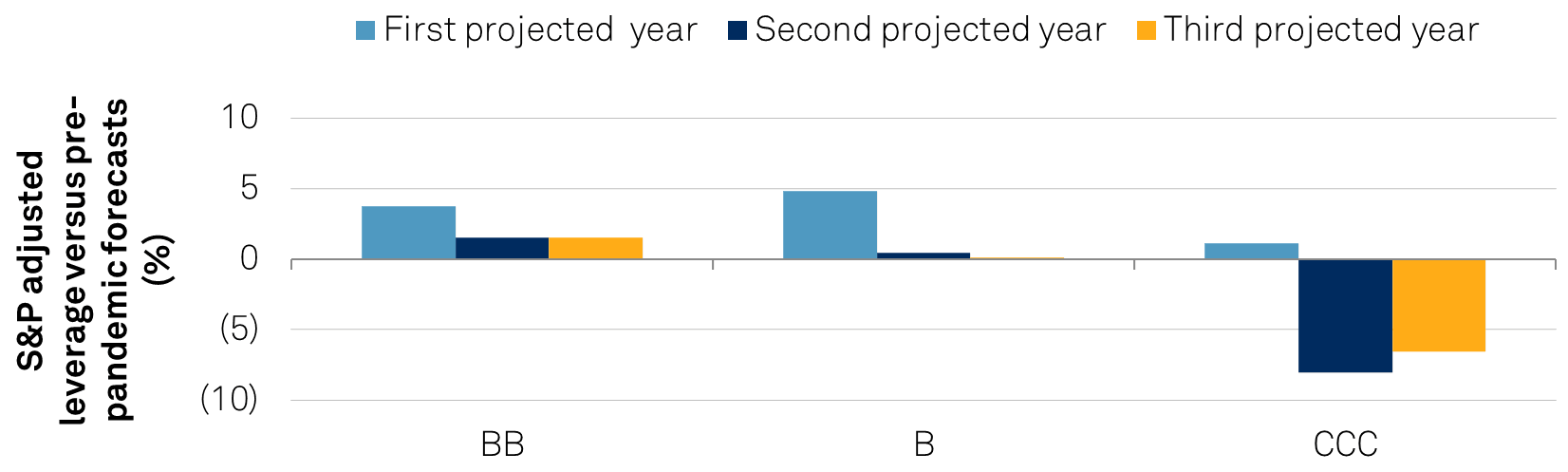

Chart 9 | …And Lower Expected Leverage Than Pre-COVID-19

Note: N+1 (or first projected year) corresponds to the ongoing fiscal year (for instance FY2021 if fiscal year ends in December). Data as of July 31, 2021. Source: MicroStrategy.

Chart 10 | The Rapid Recovery Has Led To Several Swift Upgrades Out Of 'CCC'

Data as of July 31, 2021. Source: S&P Global Ratings.

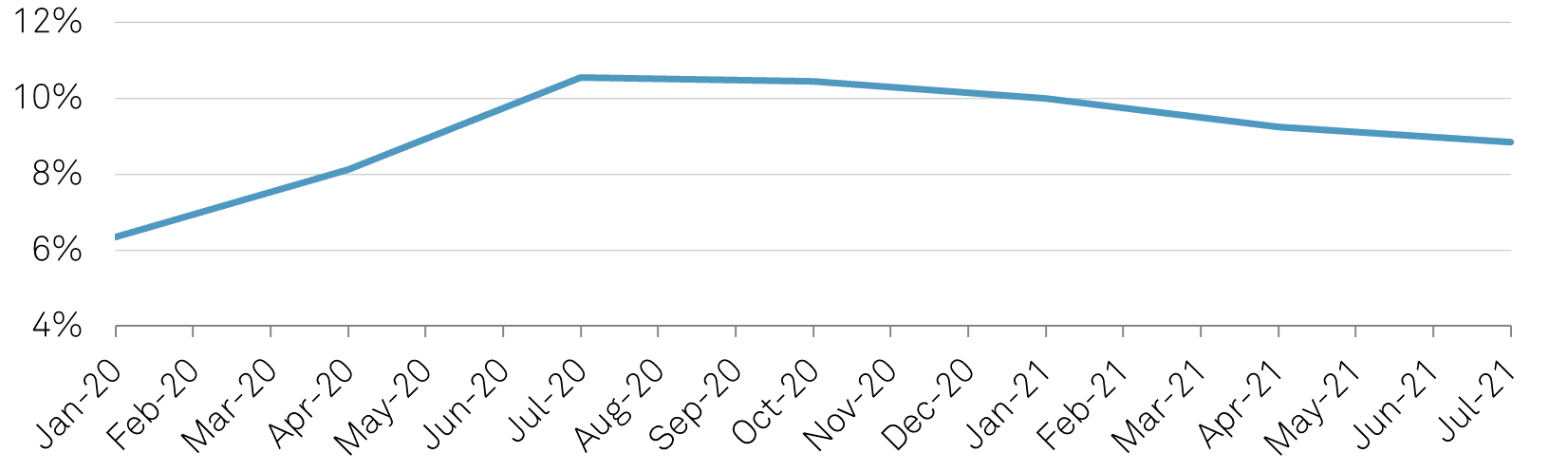

Chart 11 | Liquidity Pressures Have Increased With The Pandemic, Despite Improvement Since Mid-2020

Note: Line represents less-than-adequate liquidity. Data as of July 31, 2021. Source: MicroStrategy.

Within the leveraged finance sector, a crucial observation remains: leverage levels remain elevated for companies rated in the 'B' and 'CCC' categories, though the divergence between sectors and issuers arising from the pandemic persists. Financial market buoyancy and investor appetite for yield have supported issuers that benefited during the pandemic by pursuing debt-funded M&A or distributing dividends to their owners.

By doing so, they passed on any uncertainty regarding their growth and profitability path firmly back in the hands of the lenders.

Consequently, the convergence of the two figures could occur either if default rates caught up with the still-high share of 'CCC' ratings, or the other way around. The most likely scenario is somewhere in the middle. We expect that the combination of strong recovery prospects for 'CCC' rated companies and less supportive governments and financing conditions would lead the strongest companies to be upgraded and the weakest to default. While we don’t expect it in the coming months, default rates could pick up temporarily as issuers are upgraded out of the 'CCC' category, until reaching a new equilibrium and reverting to the original behavior of moving hand in hand.