Feb 11, 2022

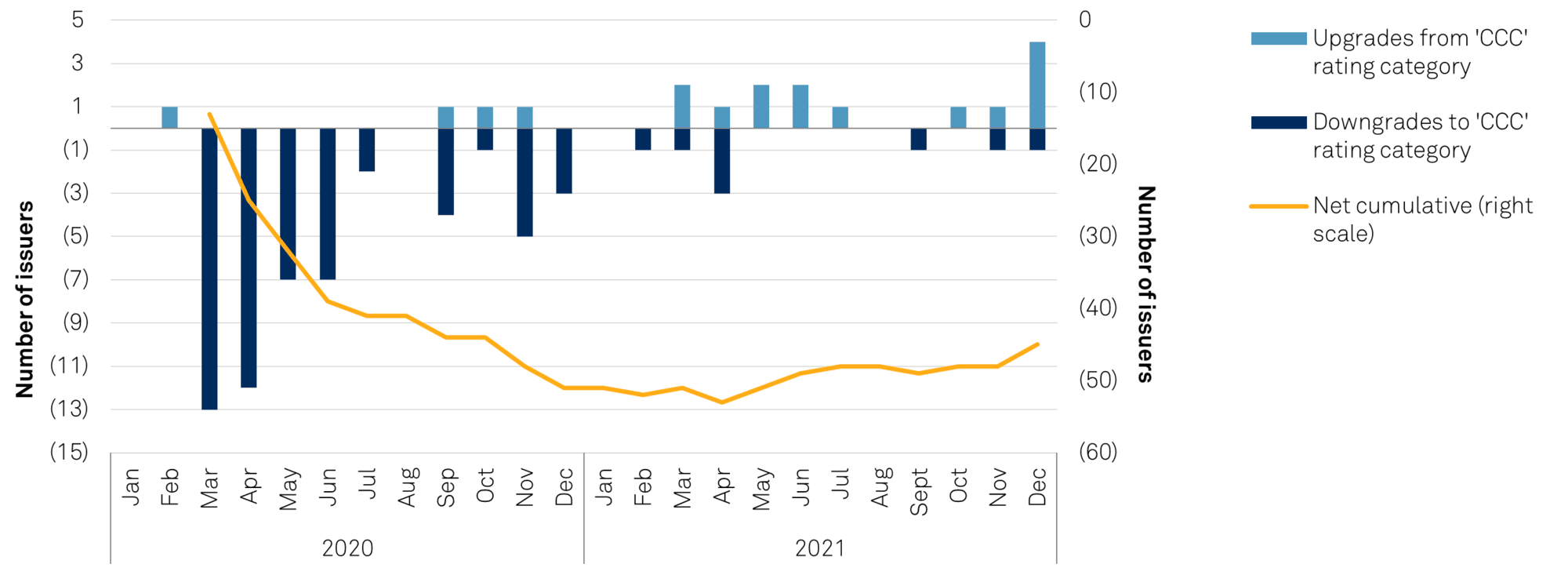

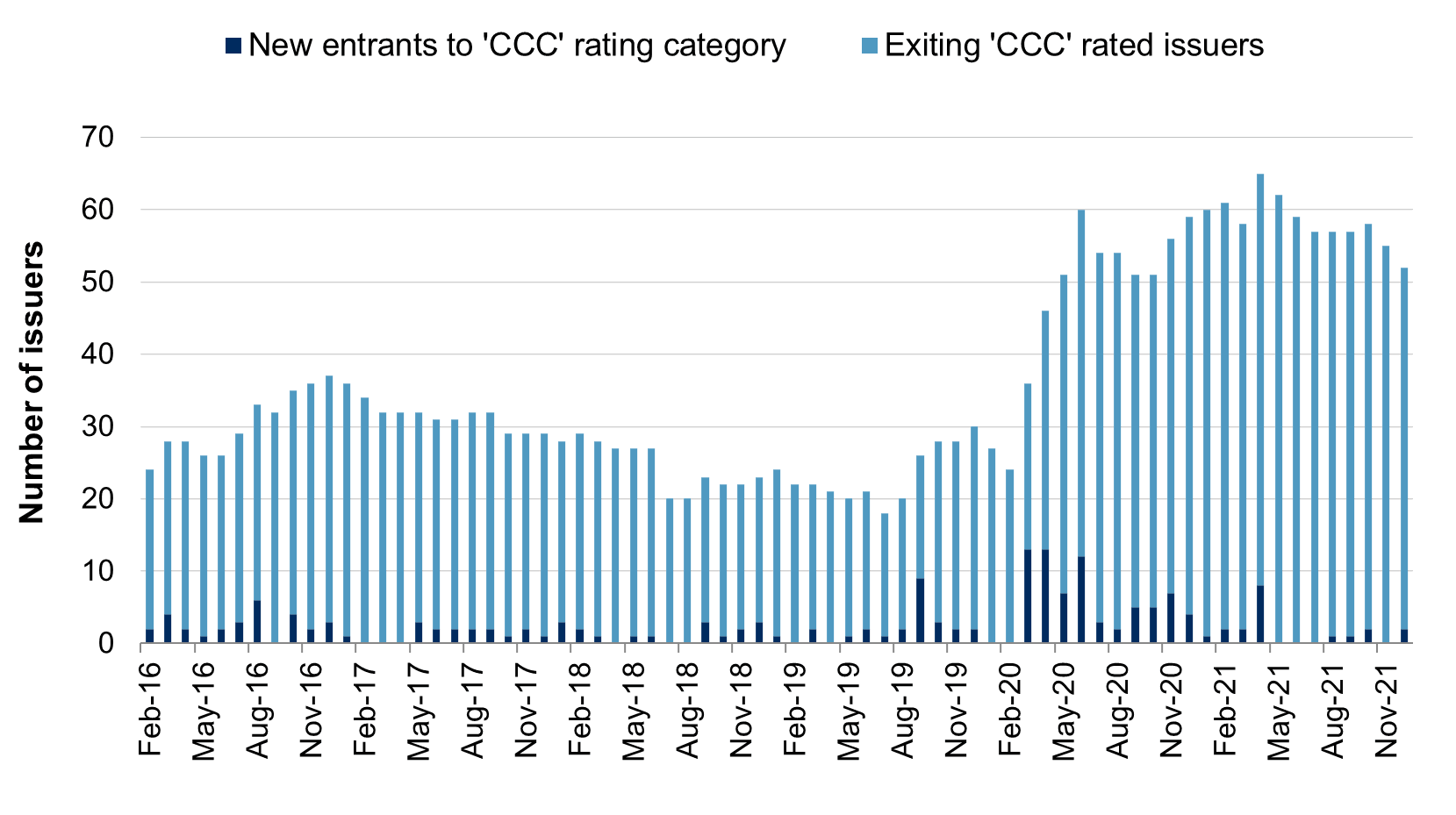

The tally of European companies publicly rated in the 'CCC' category fell to 52 as of Dec.31, 2021, from an all-time high of 65 as of April 30.

Leisure led upgrades amid a pickup in consumer demand.

The European speculative-grade default rate dropped in December to its lowest since 2016.

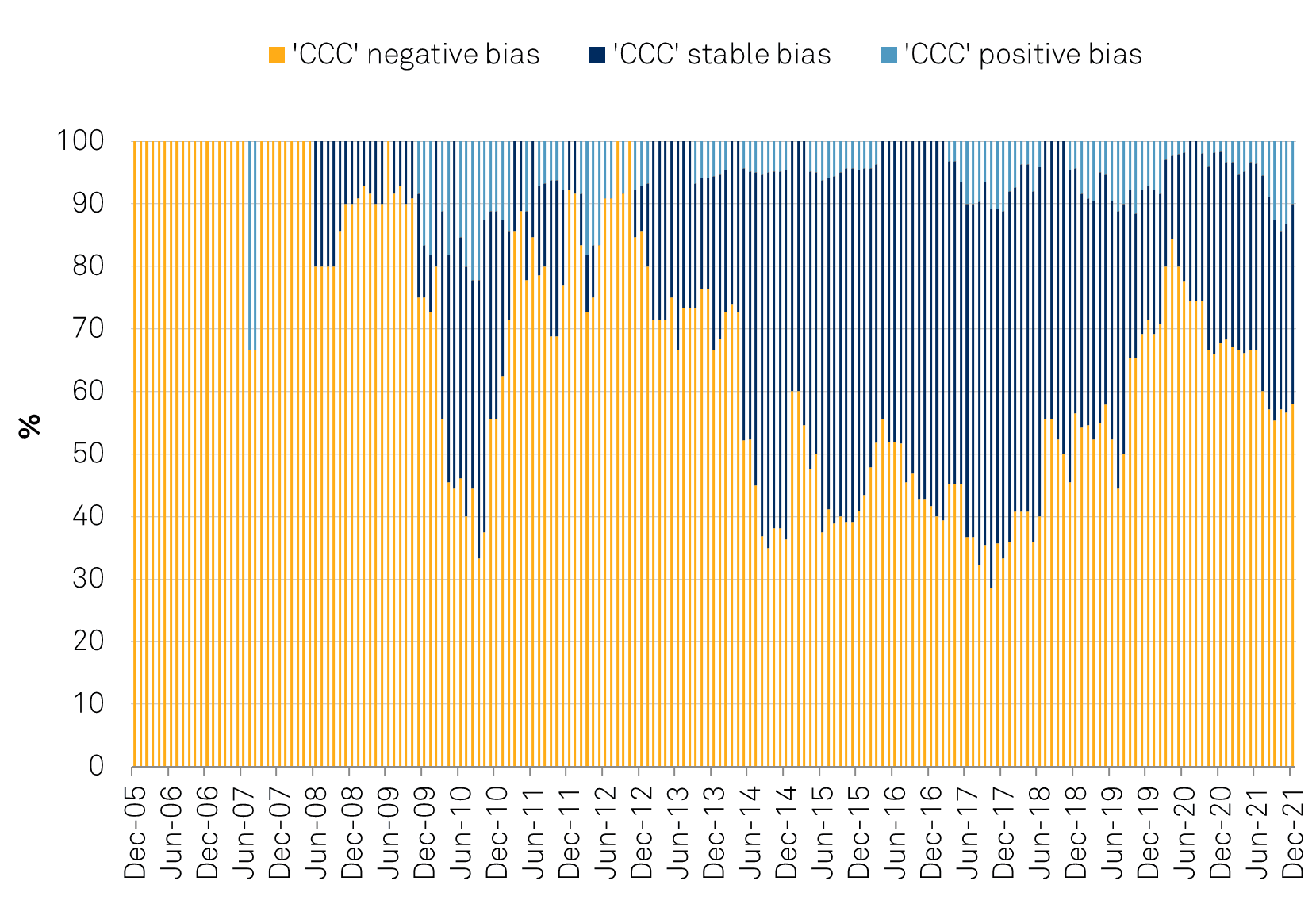

Despite higher upgrades, the negative bias for 'CCC' rated issuers remains elevated at 58% and therefore points to further downgrades.

This report does not constitute a rating action.

Nicole Serino New York +1-212-438-1396

Patrick Drury Byrne Dublin 353-1568-0605

Marta Stojanova London + 44 20 7176 0476

Shripati Pranshu CRISIL Global Analytical Center an S&P affiliate Mumbai

(Editor's Note: Our "Risky Credits" series focuses on corporate issuers rated in the 'CCC' category. Because the majority of defaults are from these companies, those with negative outlooks or ratings on CreditWatch negative are even more important to monitor in this uncertain economic recovery.)

This fall primarily stemmed from six upgrades out of the 'CCC' rating category, compared with only two downgrades into the 'CCC' rating category (see chart 1). With this decrease, the amount of debt rated in the 'CCC' category decreased to US$87 billion from US$101 billion in the same period, remaining higher than the 12-month average of US$80 billion.

Despite the rise in upgrades, the number of ‘CCC’ category rated European companies remains close to double the pre-pandemic total, and 58% of these issuers carry either negative outlooks or negative CreditWatch implications, pointing to further downgrades ahead.

Chart 1 | European Upgrades From 'CCC' Peaked In December; Still A Long Way To Go To Offset Downgrade Deluge Of 2020

Data as of. Dec. 32, 2021. Source: S&P Global Ratings.

Chart 2 | European ‘CCC' Category Rated Issuers Fell In The Fourth Quarter

Many issuers in hotels, gaming, and leisure took big hits from social distancing restrictions across Europe to curb the spread of COVID-19. However, pent-up consumer demand, vaccine campaigns, and issuers' ability to bolster liquidity have helped address highly leveraged capital structures.

Risks remain as omicron and other variants may restrict demand at least through the first quarter (see “Industry Top Trends 2022: Hotels, Gaming, And Leisure,” Jan. 25, 2022).

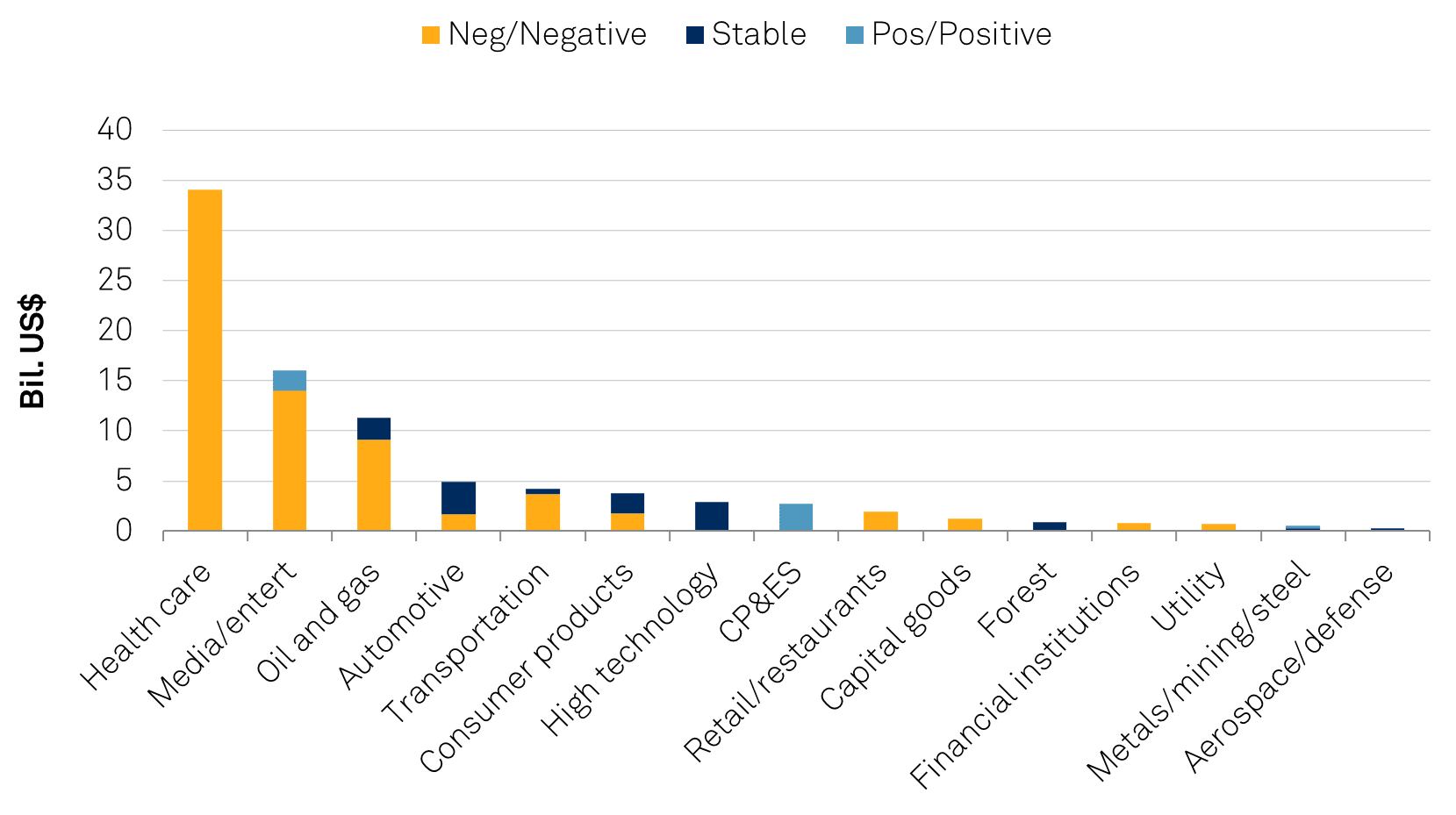

Media/entert--Media and entertainment. CP&ES--Chemicals, packaging, and environmental services. Forest--Forest products and building materials. Data as of Dec. 31, 2021. Source: S&P Global Ratings Research.

with US$34 billion (see chart 3), all of which comes from Endo International PLC and BVI Holdings Mayfair Ltd., which are both at risk for further downgrades. Pandemic uncertainty, labor and supply-chain difficulties, investor scrutiny of pricing and access, and the return of mergers and acquisitions within the industry suggest negative rating actions may outpace positive ones in 2022 (see “Industry Top Trends 2022: Health Care,” Jan. 25, 2022).

Chart 3 | Health Care Leads In European 'CCC' Debt

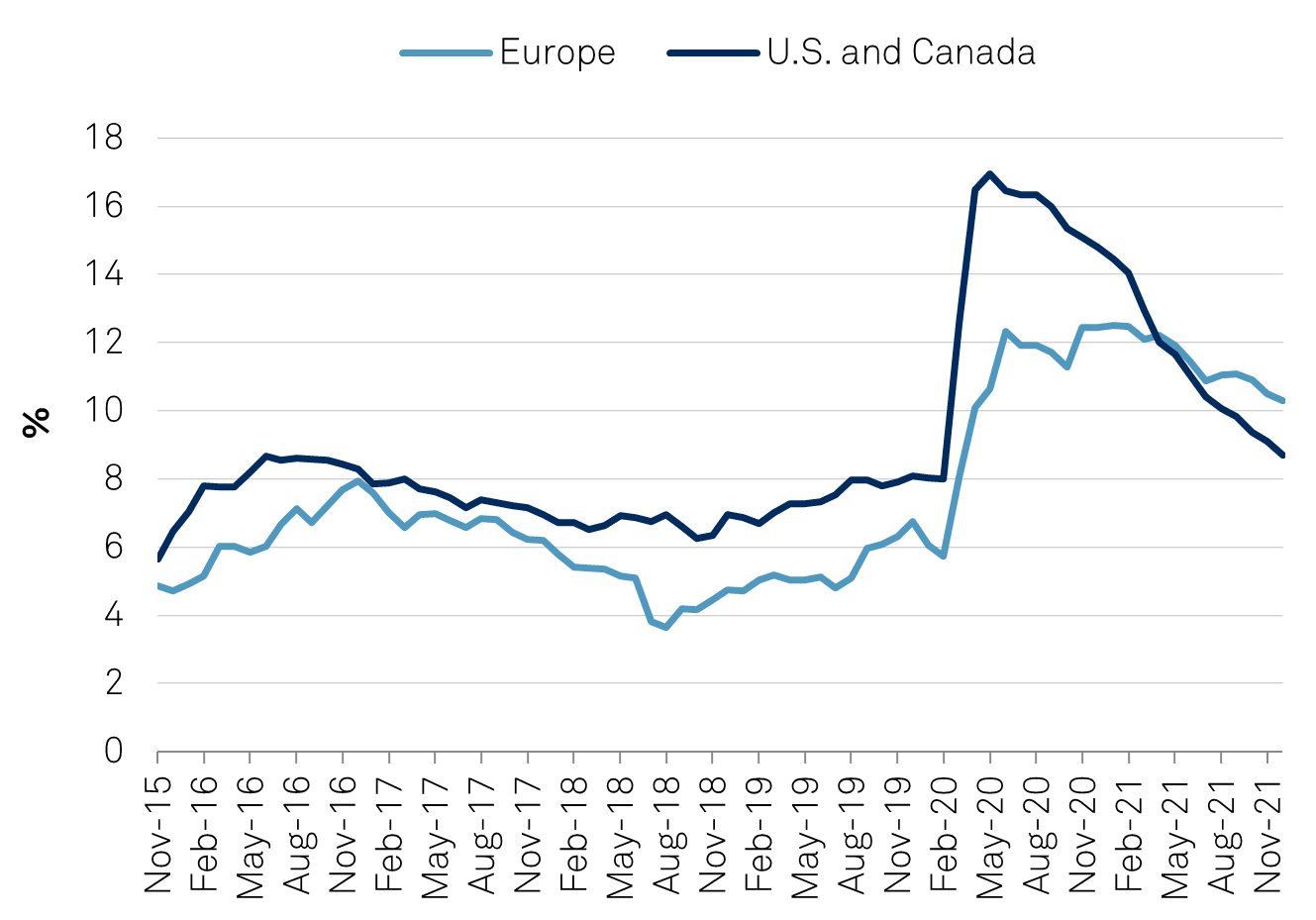

While the percentage of 'CCC' category rated issuers in Europe fell in the fourth quarter, issuers with high debt burdens and an inability to generate free operating cash flow are still struggling to improve credit quality. Uncertainty surrounding COVID-19 and resulting travel restrictions continues to cast a shadow over the recovery trajectory, despite ample evidence of pent-up demand, accommodative debt capital markets, and a higher pace of vaccination. The percentage of 'CCC' rated issuers in the U.S. and Canada has fallen to 8.7% of total rated issuers, from its peak of 17% in May 2020, while Europe has seen a negligible improvement to 10.3% from 12.5% (see chart 4).

Table 1 | Top 10 Corporate Issuers In European 'CCC' Debt Outstanding

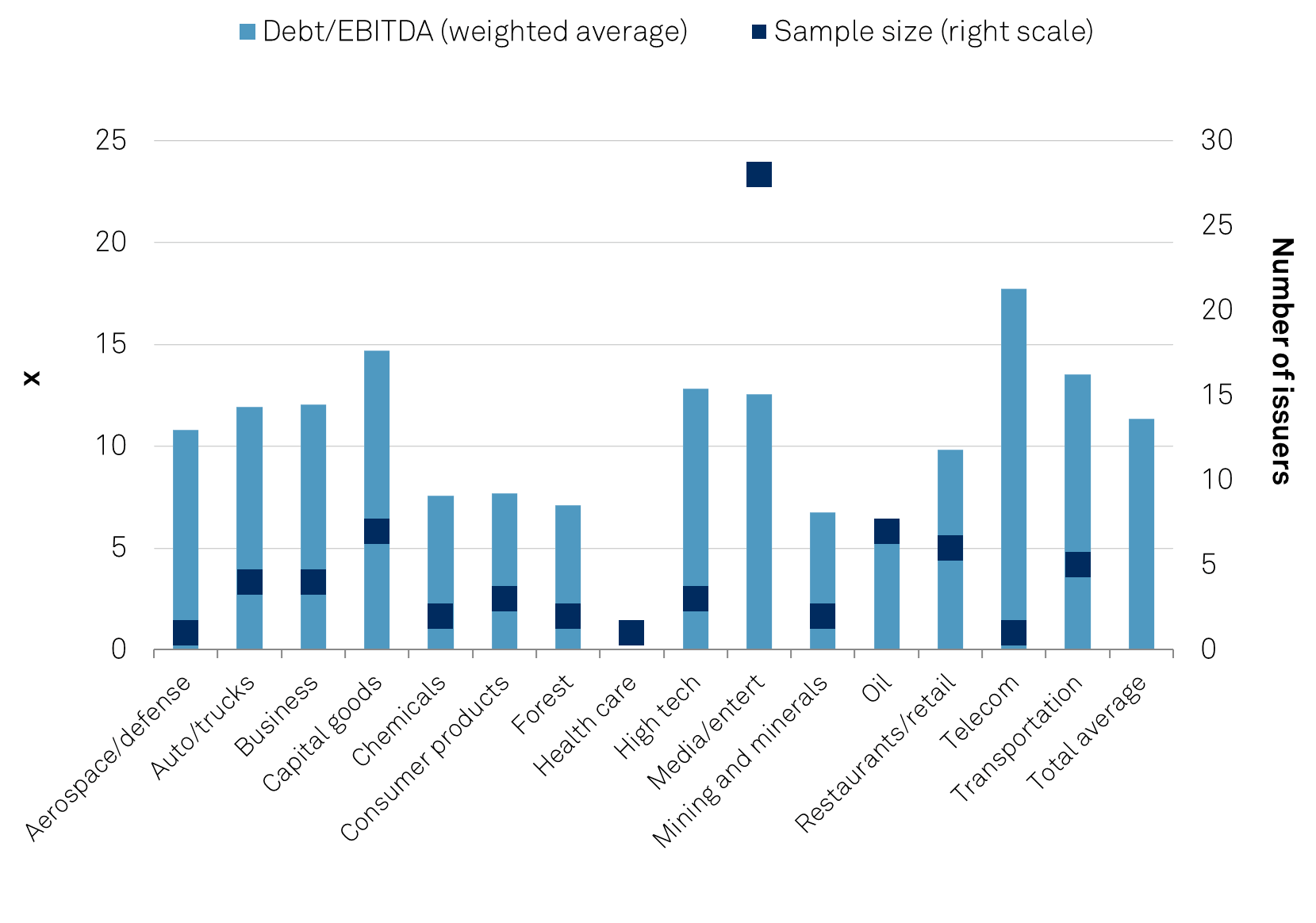

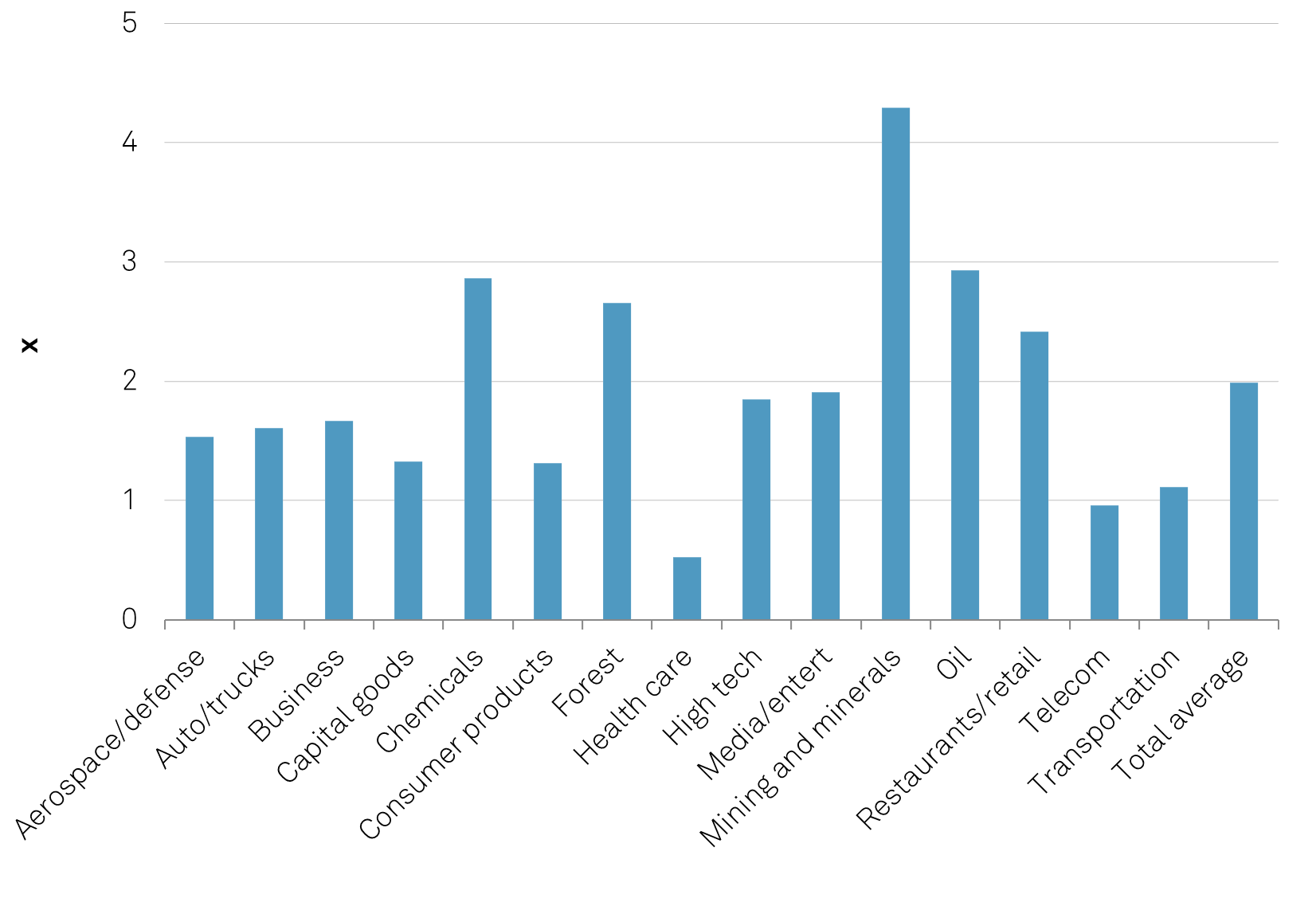

indicating that the sources of funding available to them within the next 12 months depend highly on stable operating performance and continued access to capital markets. Only a small number of companies are at risk of covenant breaches in 2022, all pending the outcome of bookings during the summer season. Average weighted debt-to-EBITDA leverage for the 'CCC' rating category is 11.6x with 2x interest coverage (see charts 5-6), indicating unsustainable leverage levels over the next two years, barring unforeseeable favorable developments on the operating side.

Chart 4 | Europe Lags U.S. And Canada As Percentage Of 'CCC' Companies Remains At Peak Levels

Data as of Dec. 31, 2021. Sources: S&P Global Ratings and S&P Global Market Intelligence's CreditPro.

Chart 5 | Average Debt-To-EBITDA Ratios For 'CCC' Rating Category In Europe

Forest--Forest products/building materials/packaging. Media/entert--Media, entertainment, and leisure. Data as of Dec. 31, 2021. Source: S&P Global Ratings.

Chart 6 | Average Interest Coverage Ratios For 'CCC' Rating Category In Europe

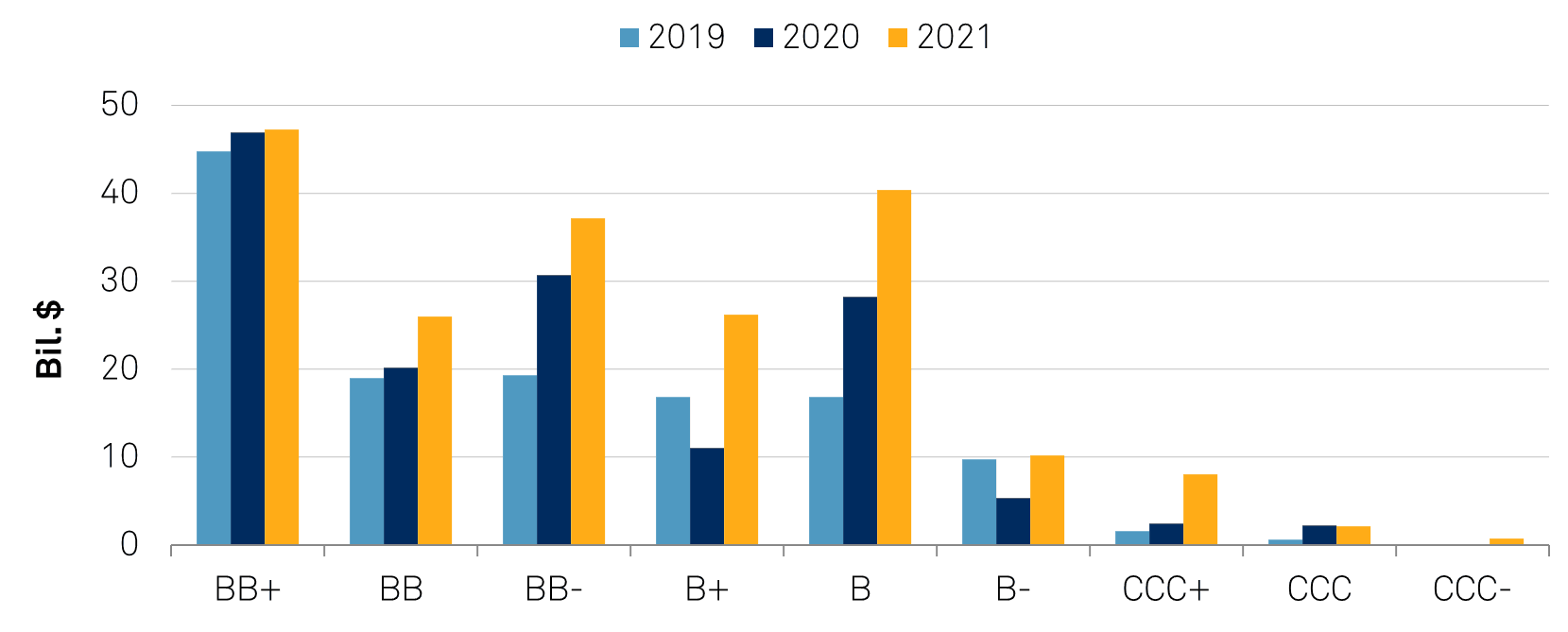

which was more than 125% higher than the 2020 total. Meanwhile, 'BB' rated issuance through 2021 stood 13% higher than in 2020. Speculative-grade ('BB+' or lower) issuance from the European region in 2021 was nearly 35% higher than 2020 levels, at $198 billion (see chart 7).

Chart 7 | 2021 European Speculative-Grade Issuance Rises Higher Than 2020

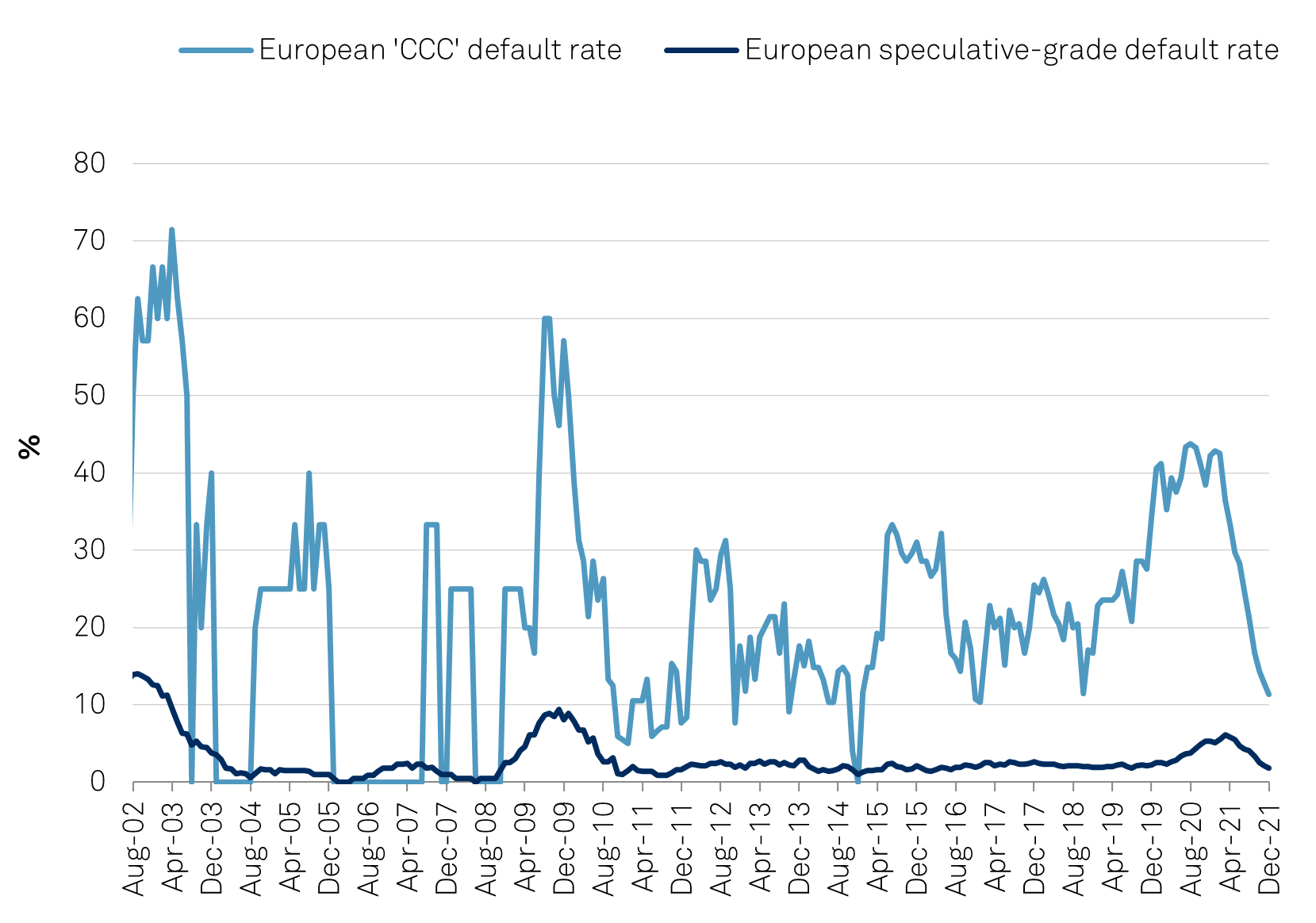

With this decline, the 12-month trailing default rate in the Europe region dropped to 1.8% as of December 2021 (the lowest regional default rate since 2016) from 6.1% in March 2021 (see chart 8).

We expect defaults to continue to slow in the short term before picking back up, boosting the speculative-grade default rate to 2.5% as of September 2022

(see "The European Speculative-Grade Corporate Default Rate Could Reach 2.5% By September 2022," Nov. 18, 2021).

Chart 8 | European 'CCC' Rating Category Default Rate Is Typically 7x Overall Speculative-Grade Default Rate

Trailing-12-month default rates for Dec. 31, 2020-Dec. 31,2021. Data as of Dec. 31, 2021. Sources: S&P Global Ratings and S&P Global Market Intelligence's CreditPro.

Chart 9 | European 'CCC' Category Negative Bias Increased To 58% In December, While Positive Bias Shrank To 10%

Data as of Dec. 31, 2021. Source: S&P Global Ratings.

Global Corporate Defaults Drop Nearly 70% In 2021, Jan. 10, 2022

The European Speculative-Grade Corporate Default Rate Could Reach 2.5% By September 2022, Nov. 18, 2021

European Leveraged Finance And Recovery Second-Quarter 2021 Update: Late Cycle Behavior Or A Brave New World?, July 19, 2021

CLO Pulse Q1 2021: Sector Averages Of Reinvesting European CLO Assets, July 8, 2021