By Stergios Zacharakis, Mary Hogan, Esther Ng, Callum Sinclair, Shivangi Acharya, Luke Milner

Global methanol markets will head into the second half of 2021 under pressure from increasing production capacity, mainly in the US and Iran and despite continued firm demand from China's methanol-to-olefin plants.

Meanwhile, Europe will enter the third quarter with its supply-demand balance tipping from tight to balanced.

Fundamentals in the Asian methanol market will likely be mixed in the second half of the year. Downstream demand in China is expected to remain healthy from strong export growth, underpinned by a thriving US economy, but a resurgence of COVID-19 cases in Asia could dampen export demand.

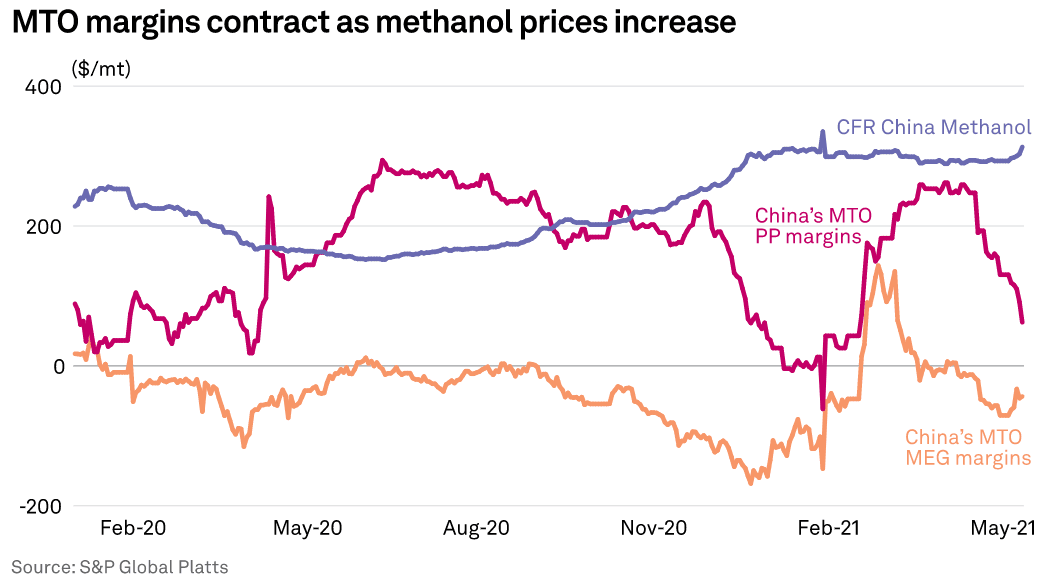

Limited availability of non-sanctioned methanol cargoes may support imported Chinese methanol prices and could impact methanol-to-olefin plants margins.

CFR Far East Asia polypropylene prices have fallen steadily since March, while CFR China methanol prices have remained relatively steady, S&P Global Platts data showed.

Sabalan Petrochemical Company's startup of a 1.65 million mt/year methanol plant in Iran in June could, however, mitigate bullishness in CFR China methanol prices in H2 2021.

In the Indian methanol market, prospects of downstream demand remain shrouded in uncertainty as the country deals with an unprecedented surge in coronavirus infections, leading to a slew of localized lockdowns in many regions.

The subsequent demand destruction was expected to spill over into Q3, while any recovery, albeit staggered, remains contingent on containment of the virus.

Successful US-Iran talks could pave the way for eased sanctions on trade of petrochemicals from Iran, which could effectively improve availability of supplies for India.

The European methanol market has battled with uneven supply in H1, amid planned Q2 maintenance activities which, in combination with supply disruptions from Trinidad and Venezuela, created a bullish price environment.

However, despite expectations of tight supply, the market remained balanced until mid-Q2.

Returning capacities in Europe alongside increased import volumes weighed on prices with excess supply expected to exert further pressure on spot prices towards Q3 unless delays occur.

Despite supply issues dominating market sentiment, demand has held firm and market sources expect that to continue into Q3. Support is mostly to come from the chemical sector in the form of formaldehyde consumption during the coronavirus pandemic.

Expenditure on household improvements has increased notably since restrictions were first enforced over a year ago as traditional spending habits were swiftly altered. As international travel remains uncertain, firm demand for household improvements is expected to continue throughout the summer.

The US methanol market is expected to see supply length in the second half of the year, with mixed market expectations for how that additional capacity could be absorbed.

Market sources expected the anticipated startup of the 2 million mt/y YCI Methanol One facility in late Q2 or early Q3 to help lengthen spot supply to some degree in the US market. Although the amount promptly available could depend on how much, if any, is contracted out for export and how much might remain domestically if prices climb because of higher derivative product demand.

Simultaneously, domestic supply will depend on the reliability of facilities in east Texas and in Trinidad, according to market sources. Several operational issues were reported in the first half of the year, both because of the deep freeze in the US Gulf Coast in late February as well as other infrastructure and gas supply related issues.

Domestic demand for methanol was expected to rise in H2, driven by US COVID-19 vaccinations boosting economic activity. The return to full rates of most intermediates production along the US Gulf, such as acetic acid and vinyl acetate monomer, following widespread facility damage from the deep freeze, is expected to add demand for feedstock methanol.

Higher anticipated construction sector activity is also to add demand from the formaldehyde derivatives segment. Demand for gasoline blendstock MTBE will remain a wild card, however, and dependent upon the rate of economic recovery in Mexico and Latin America in the wake of the pandemic.