May 12, 2021

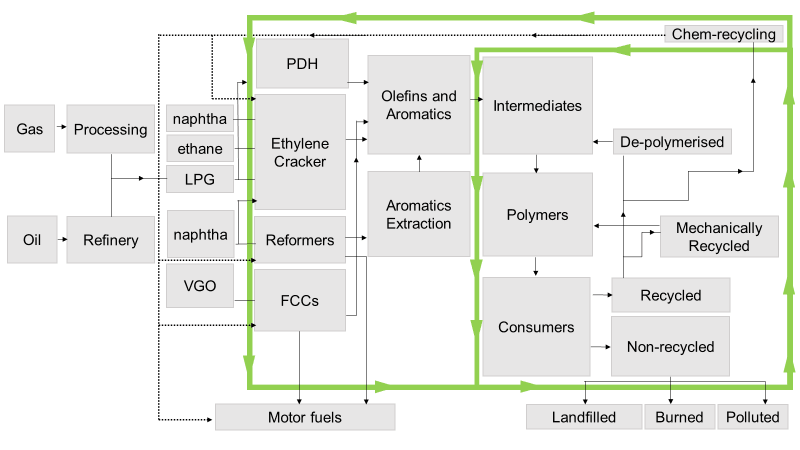

Non-energy demand for oil, particularly chemical feedstock demand, has been one of the fastest-growing portions of oil demand over the past decade. This trend is set to continue over the coming decades as fuel demand languishes on increasing decarbonization goals. Meanwhile, topline demand for polymers (HDPE, LLDPE, PP, PET) will continue to grow in the coming years with higher use in durable (automotive and construction) and non-durable applications (fibers and packaging). However, there are headwinds for continued increases in demand for feedstock naphtha, LPG, and ethane into petrochemical markets. Leakage of plastics into the environment (especially single-use plastics) has led to policy initiatives to reduce consumption or, in most instances, increase the amount of recycled content in packaging. An increase in reusing recycled content can happen in several ways and include mechanical, chemical and depolymerization recycling of plastics. In this special report, we look at the current state of chemical recycling, a proven technology with a small production base that is quickly growing in popularity due to its scalability and fungible outputs of LPG, naphtha and diesel-range products.

As mentioned, there are three main routes to recycling plastics - mechanical, chemical and depolymerization. Currently, the market is dominated by mechanical recycling. In mechanical recycling, recycled content is collected at the curbside, transported to a sorting facility, cleaned, and then ground into flakes. Depending on the quality of the flake, an extruder can make food-grade or non-food grade pellets. These pellets can then be mixed with virgin plastics for either food-grade (beverage bottles or plastic trays) or non-food-grade applications (motor oil containers, fiber for cushion filing).

Technically, mechanical recycling is simple. However, there are challenges to scaling this form of recycling. One, there must be a high level of collection in place to have a product stream to convert to recycled pellets. In 2018, 32.5% of post-consumer plastic waste was collected to be recycled in Europe, according to the European Union. In the U.S. the number is even lower at around 15%. There are EU mandates now in place to increase those levels by 2025 and 2030 (see policy section). Another challenge in mechanical recycling is in the output stream. To reuse mechanically recycled plastic in virgin food-grade applications there must be a high level of purity, a factor that adds costs to the process.

Depolymerization is another recycling technology that allows for waste feed streams to be converted into their pure monomers. The most common application of this technology has been to the PET chain where the feed is converted to PTA and MEG. The PTA and MEG can then be reused to make polymers. Unlike pyrolysis, depolymerization of PET needs a feedstock that has a specific chemical composition. Depolymerization usually occurs using a solvent but companies are exploring other options. French-based company Carbios has developed an enzyme to break down PET into monomers. The company is building an industrial plant in France which is due online at the end of 2021.

Chemical recycling is a broad-based term but in general, it is the process of thermally breaking down plastics into chemical feedstocks which can then re-enter the chemical production process. This area of the recycling market is garnering a lot of interest as it allows mixed feeds to come into the recycling system at the end of life. In addition, chemical recycling produces products that are fungible with traditional hydrocarbons such as naphtha, propane, jet fuel, and diesel. As a result, chemical units can take naphtha from a chemical recycling unit and run it back into the naphtha cracker the same way it would use naphtha distilled from crude oil.

Proven technology The most common method of chemical recycling is pyrolysis, a proven technology that has been around for decades. In pyrolysis, feed waste plastics are heated in the absence of oxygen (with or without catalysts) to break down long-chained molecules into shorter chained molecules. Temperatures in this cracking process range from 300–900°C and depend on the feedstock used (HDPE, LDPE, PP, etc.). The shorter chained “cracked” molecules are distilled into different purity streams that include products such as diesel, jet fuel and naphtha. These purity product streams can then enter back into refinery or chemical operations and be treated the same as “virgin” products derived from crude. A close analogy would be fully fungible renewable diesel being blended with non-renewable diesel.

As mentioned earlier, a challenge with mechanical recycling is sorting and cleaning. Recycled content from homes is usually mixed which means the recycling center must clean and sort the waste into individual streams such as HDPE, PP, PET, etc. In addition, there are very strict contamination limits on food-grade plastics, which results in mechanically recycled content often getting downcycled into alternative end uses such as non-food grade plastic bottles, tarmac filler, or decking. In the case of chemical recycling, the feed product has lower restrictions on what can be fed into the pyrolysis unit. Some plastics, such as PVC, present challenges in pyrolysis due to the presence of HCL but common plastics such as HDPE, LLDPE, and PP can be fed as a mixed stream.

In terms of yields, chemical recycling produces a range of products that range from gases to fuel oils. For the petrochemical market, naphtha is the most important feedstock. Yields of naphtha can vary based on the technology employed and feedstock used but companies have said yields of around 0.6 mt of naphtha feedstocks are possible for every mt of mixed feed.

Commitments and market growth Chemical recycling has traditionally been a niche market with small-scale plants. However, with changing policy and stronger company commitments (see commitments on right) around recycling and reuse, there is strong investment growth into chemical recycling. Many of the world’s largest petrochemical companies have entered into offtake agreements (see Table 1) with chemical recycling companies. For example, in Europe, Plastic Energy has entered into offtake agreements with SABIC and Total. Plastic Energy’s naphtha output, TACOIL, is already being used at petrochemical facilities in the Netherlands and France and they have ambitions to grow their footprint into Asia. The company has signed a non-binding agreement with Petronas to develop projects in Indonesia.

Mura Technology announced in April that its Teeside, England, facility will supply pyrolysis naphtha to Dow’s facilities. The 20,000 mt mixed-feed plastics facility will come online in 2022 and look to expand to 80,000 mt over the coming years, the company has said. In the U.S., several players are also procuring or are in plans to acquire naphtha from pyrolysis of mixed plastic feeds. Shell announced last year that it will extend an agreement with Atlanta-based Nexus fuels to purchase pyrolysis naphtha. CP Chemical also stated that it would be using naphtha from Nexus. Brightmark’s Ashley, Indiana chemical recycling plant, which will be the largest chemical recycling plant in the world at 100,000 mt, is due to come online at the end of 2021. Brightmark has said that all the fuels will go to BP. In addition, Brightmark and SK Global Chemical announced in January they had signed a MOU to develop a 100,000 mt/year plant in South Korea.

Braskem recycled products portfolio to sales of 300,000 mt/year by 2025 and 1 million mt/year by 2030

Source: Various company announcements

Several companies are also utilizing recycled styrene through Agilyx’s technology. This process breaks down polystyrene into feedstock styrene which can then be used again in the production of polystyrene or used for other styrene derivatives such as ABS. Agilyx is supplying American Styrenic’s plants with styrene. Agilyx technology is also being used in Europe by INEOS and Trinseo.

Company

Offtaker

Location

Waste input Capacity (mt)

Start

Output

Plastic Energy

SABIC

Geleen

20,000

2022

Pyrolysis naphtha

TOTAL

Grandpuits

15,000

2023

Seville

5,000

2017

Almeira

2015

Exxon

Notre Dame Gravenchon

25,000

INEOS

Kohln*

30,000

Quantafuel

BASF

Skive

16,000

2019

New Energy

Budapest

8,000

2018

Feunix Ecogy

Dow

Ternuezen

-

Mura

Teeside

Recycling Technologies

Ineos

Wingles

Styrene

Trinseo

Tessenderlo

Nexus

Shell

Norco, Louisiana**

2020

UNK

Various U.S. sites

2021

CP Chem

Various sites

SCG

Map Ta Phut

4,000

SK Global Chemical

Brightnark

South Korea

100,000

Agilyx

Amsty

Oregon

3,650

Illinois

36,500

Toyo Styrene

Japan

*Estimated location based on previous activity at site ** Nexus facility located in Atlanta Source: Various company announcements

Environmental benefit or cost? Chemical recycling is touted by some as the silver bullet solution to addressing environmental concerns associated with waste plastic and to lessen the reliance on oil-derived feedstocks to meet plastics demand. One of the key benefits of chemical recycling is a greater allowance of mixed streams of plastics and the ability to use output pyrolysis naphtha as a fungible product to virgin naphtha derived from crude oil. The nature of the chemical recycling process means there isn’t any “downcycling” which often occurs with mechanical recycling when the product is not of the highest purity. However, chemical recycling does have an environmental footprint that must be weighed against alternatives in determining its net environmental impact relative to alternatives such as virgin sourced plastics.

With chemical recycling, the waste product streams need to be collected, sent to a chemical recycling plant, processed (using high levels of energy in pyrolysis crackers) and then transported back to cracking units which can then crack the pyrolysis naphtha. Various life cycle analyses have been done around the environmental costs of chemical recycling versus different alternatives. Results of those analyses vary greatly and depend on the assumptions made around the alternatives to chemically recycling the plastic. For example, there are generally three main end-of-life routes for plastics: landfilling, incinerating, or recycling (mechanical, depolymerizing, or chemical).

Recently, BASF conducted a study to compare the carbon footprint of chemical recycling versus other end-of-life options for plastics. The study, which was independently reviewed, concluded that chemical recycling emits 2.3 mt less CO2 as compared to an alternative of producing plastics from fossil sources. A key assumption was that a credit of 3.7 mt CO2 was given to chemically recycled plastics as it avoided emissions from incineration. The study also showed that utilizing chemical recycling and mechanical recycling to produce new plastics emits around the same level of emission per mt of plastics produced. The BASF study did not compare the CO2 impact of landfilling waste plastics instead of recycling or incineration. However, Plastic Energy conducted an independent life cycle analysis study of chemical recycling in 2020 and compared landfilling as an end-of-life option for plastics. The study concluded that landfilling had the lowest environmental impact out of the three end-of-life options. The study concluded: “For climate change, landfill shows the lowest impact, followed by chemically recycled LDPE, and incineration. For resource use, fossil chemically recycled LDPE is the most favorable solution, showing environmental credits related to the avoided production of virgin naphtha.” The Plastic Energy study concluded the following in terms of re-using resources: “compared to virgin (fossil) LDPE, chemically recycled LDPE has lower climate change and resources depletion scores.”

In summary, the environmental costs associated with chemical recycling depends on what assumptions are made about the end of life of plastics. If the assumption is that plastics will be burned or leaked into oceans, then chemical and mechanical recycling are better options. However, if landfilling and monitoring the landfill site with strict protocols is the alternative, then this plastic is a form of carbon capture as the carbon molecules in the plastic are highly stable.

Small but poised to grow One clear challenge to chemical recycling, and recycling in general is economies of scale. The largest world-scale chemical recycling plant is currently under construction and will only be able to take in 100,000 mt/year of mixed plastics. By comparison, it is common to see polyethylene or polypropylene facilities with 300,000-500,000 mt/year of capacity. Typically, at least 2-3 of these plants come online every year. This small level of scale in recycling is a function of the market’s logistics. Most waste comes from disparate locations that need to be aggregated and then transported to sorting and then chemical recycling plant. These all add costs along the value chain. By comparison, a world-scale naphtha or ethane cracker will be connected by a pipeline to storage terminals.

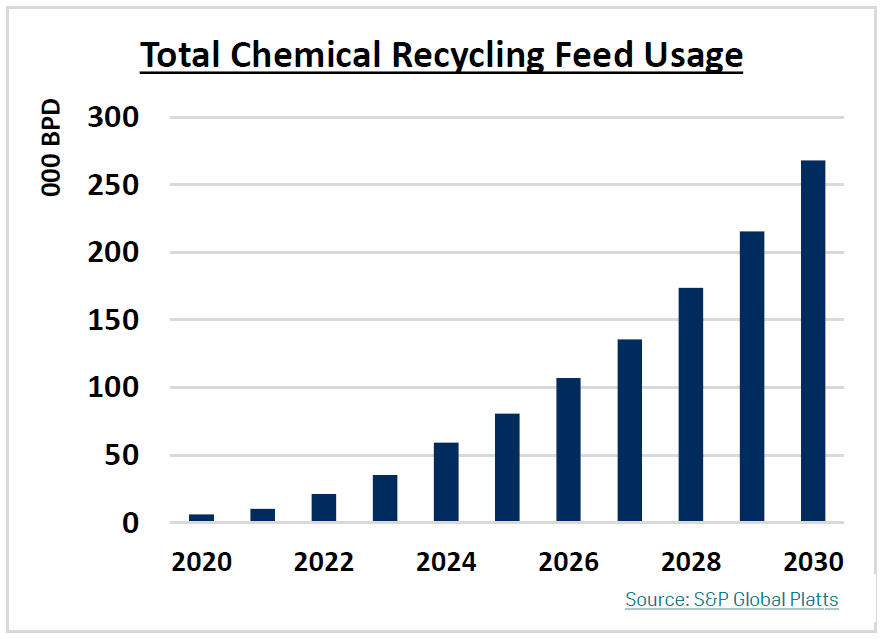

Despite these challenges, the industry is moving in a growth direction regarding circular plastics. Companies such as BASF have come out with goals in terms of recycled feedstock usage. BASF’s target is 250,000 mt by 2025, which equates to roughly 6,000 bpd of naphtha. Other companies have released targets for recycled plastics content production, where a combination of both mechanical and chemical recycling will most likely be used. To put chemical recycling into context, global naphtha usage into ethylene production will be about 250 million mt/year or 6.3 million bpd in 2025. That amount could come from either virgin naphtha, bio naphtha or pyrolysis naphtha through recycled mechanisms. Currently, we estimate that chemical recycling volumes arearound 10,000 bpd. If we assume that just 1% of cracker feeds come from chemical recycled feedstocks by 2025, this would represent 2.5 million mt/year (63,000 bpd )

of naphtha from chemical recycling going into crackers. The virgin feedstock reduction from chemical recycling Source: S&P Global Platts equates to about 50% of a world scale naphtha cracker in 2025. However, as the chart on the right shows, increasing growth in chemical recycling means that chemical recycling will only displace the need for about two world-scale naphtha crackers by 2030.

© 2021 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

The names “S&P Global Platts” and “Platts” and the S&P Global Plattslogo are trademarks of S&P Global Inc. Permission for any commercialuse of the S&P Global Platts logo must be granted in writing by S&PGlobal Inc.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables, and images(“Data”) in this publication only for your personal use or, if you or your company has a license for the Data from S&P Global Platts and you are an authorized user, for your company’s internal business use only. You may not publish, reproduce, extract, distribute, retransmit, resell, create any derivative work from, and/or otherwise provide access to the data or any portion thereof to any person (either within or outside your company, including as part of or via any internal electronic system or intranet), firm or entity, including any subsidiary, parent, or other entity that is affiliated with your company, without S&P Global Platts’ prior written consent or as otherwise authorized under license from S&PGlobal Platts. Any use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to S&P Global Platts.

S&P Global Platts, its affiliates and all of their third-party licensors disclaim any and all warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use as to the Data, or the results obtained by its use or as to the performance thereof. Data in this publication includes independent and verifiable data collected from actual market participants. Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management, or other decision. S&P Global Platts, its affiliates and their third-party licensors do not guarantee the adequacy, accuracy, timeliness and/or completeness of the Data or any component thereof or any communications (whether written, oral, electronic or in other format), and shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive or consequential damages (including but not limited to, loss of profits, trading losses and loss of goodwill).

ICE index data and NYMEX futures data used herein are provided underS&P Global Platts’ commercial licensing agreements with ICE and with NYMEX. You acknowledge that the ICE index data and NYMEX futures data herein are confidential and are proprietary trade secrets and data of ICE and NYMEX or its licensors/suppliers, and you shall use best efforts to prevent the unauthorized publication, disclosure or copying of the ICE index data and/or NYMEX futures data.

Permission is granted for those registered with the Copyright ClearanceCenter (CCC) to copy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222Rosewood Drive, Danvers, MA 01923, phone +1-978-750-8400. Reproduction in any other form, or for any other purpose, is forbidden without the express prior permission of S&P Global Inc. For articles prints contact: The YGS Group, phone +1-717-505-9701 x105 (800-501-9571 from the U.S.).

For all other queries or requests pursuant to this notice, please contactS&P Global Inc. via email at support@platts.com.