use will reduce CO2 emissions by 7.5% by 2050

S&P Global Platts Analytics on the obstacles that must be overcome across the hydrogen value chain to increase the speed of production and adoption

A new Future Energy Outlooks report from S&P Global Platts Analytics finds that the deployment of hydrogen in 10 European countries will help reduce their collective CO2 emissions by 7.5% by 2050, as well as reduce the use of traditional fossil fuels in those countries by more than 500,000 barrels-of-oil-equivalent per day (Boe/d). At the same time, their collective energy use from renewables will increase by more than 450 TWh, the Platts Analytics report said.

Europe leads the world in low-carbon hydrogen project development accounting for approximately 50% of the total announced low-carbon projects in the Platts database.

The Platts analysis takes a conservative view regarding hydrogen market penetration as compared to the EU’s hydrogen roadmap as well as individual member states’ implementation plans.

“The potential CO2 emissions reduction of 7.5% by using hydrogen was a surprising result because we took a rather conservative approach and the adoption rates are still very low compared to country targets.”

S&P Global Platts Analytics Manager of Future Energy Signposts and lead author of Platts E- 10 Hydrogen Report

"While 7.5% is not a sizable percentage–considering Europe has committed to net zero–it is still significant in terms of our expectations this early on. The initial results exceeded our early expectations, but there are still a number of hurdles to hydrogen penetration in the European market and beyond.”

Hydrogen can be a critical component of the global energy transition away from fossil fuels, such as oil and gas. Hydrogen is particularly critical as a potential transportation fuel and for decarbonizing certain industrial sectors that will be difficult to decarbonize through other means such as steel, aluminum, chemicals, refining, and cement.

Some of those hurdles, Robba said, include the cost of producing hydrogen, which is still exceedingly high compared to other energy sources, building hydrogen infrastructure, and market acceptance. “There are a number of significant obstacles that must be overcome across the hydrogen value chain to increase speed of production and adoption,” Robba said. “Cost of production is still quite high, and there are significant challenges to be overcome to transport hydrogen. It will also be a significant cost and logistical undertaking for steel manufacturers to transition to hydrogen in their manufacturing processes. It can and needs to be done to decarbonize, but it will take time, money, policy support, and incentives to make it happen more quickly.”

Part of the challenge for emerging lower-carbon fuel sources like hydrogen is the need to create cost parity to other energy sources, not just on a simple cost-to-cost comparison per unit of energy, but to factor in the lower-carbon value that the cleaner fuel offers the market and the climate, Robba said. “The use of low-carbon hydrogen is currently more expensive than traditional fossil-fuel energy sources, but it offers a lower-emission pathway for certain sectors, so it is important to account for those emission reductions in assessing the total value of that product.”

In terms of hydrogen, market participants are ready to move beyond color descriptors for hydrogen types as those are not terribly specific or helpful, Robba said. “The more effective approach to aid the market is to measure value of a resource on a consistent, transparent basis through carbon-intensity calculation and measurement, which is where hydrogen is going in terms of market assessment.”

From our perspective, we are looking at hydrogen as a next generation fuel– a decarbonization fuel. Rather than focusing on a color, we find it more useful to think of hydrogen as a means of decarbonization. If you split hydrogen into 50 different markets, that makes it difficult to create a strong, vibrant market. Hydrogen traded simply as hydrogen creates one large market. The key here is achieving decarbonization, so establishing a standard in understanding the carbon intensity of hydrogen will help decarbonization.

“Our new Platts Carbon Neutral Hydrogen assessments will, first and foremost, reflect the value of the hydrogen molecule, irrespective of production pathway or color,” said Alan Hayes, head of Energy Transition Pricing at S&P Global Platts. As the energy transition gains momentum, market participants, governments, industry, and investors need a trusted and independently assessed price that reflects the value of hydrogen as a commodity to make informed trading and investment decisions and manage risk. Extensive feedback from market participants has illustrated that for a nascent global hydrogen market to grow, its price should be determined by a methodology that focuses on hydrogen as a commodity, not one that is based on its production pathway.

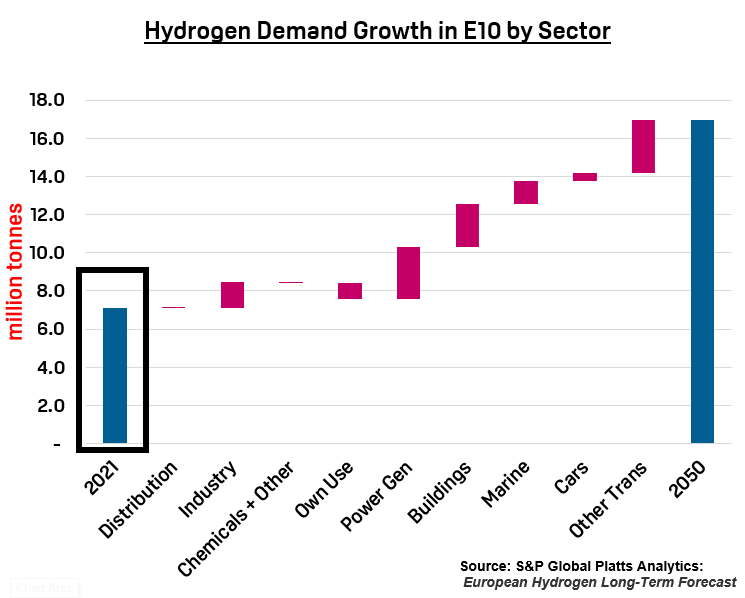

It is important to note, Platts Analytics said, that natural gas demand will increase by an average of around 464,000 MMBtu/d (less than 1% of total natural gas demand in the E10) during the first decade of the forecast compared to the reference case. This is due to the increased demand for fossil-fuel production of hydrogen (blue) with carbon capture, utilization, and storage (CCUS), but declines as hydrogen production shifts toward hydrogen produced with renewable generation (green), and displaces direct, natural gas demand in several sectors.

Only two countries, the United Kingdom, and the Netherlands have provided a dual-track pathway, which allows for hydrogen produced from natural gas with CCUS and renewable energy generated hydrogen.

“This two-step production pathway is a critical step toward jump-starting decarbonization of key industrial sectors that are particularly challenging to decarbonize,” Robba said. “Enabling hydrogen production with fossil fuels and CCUS allows incumbent sectors with existing hydrogen demand and infrastructure to decarbonize quickly and allows renewably powered hydrogen to be scaled to meet future demand.”

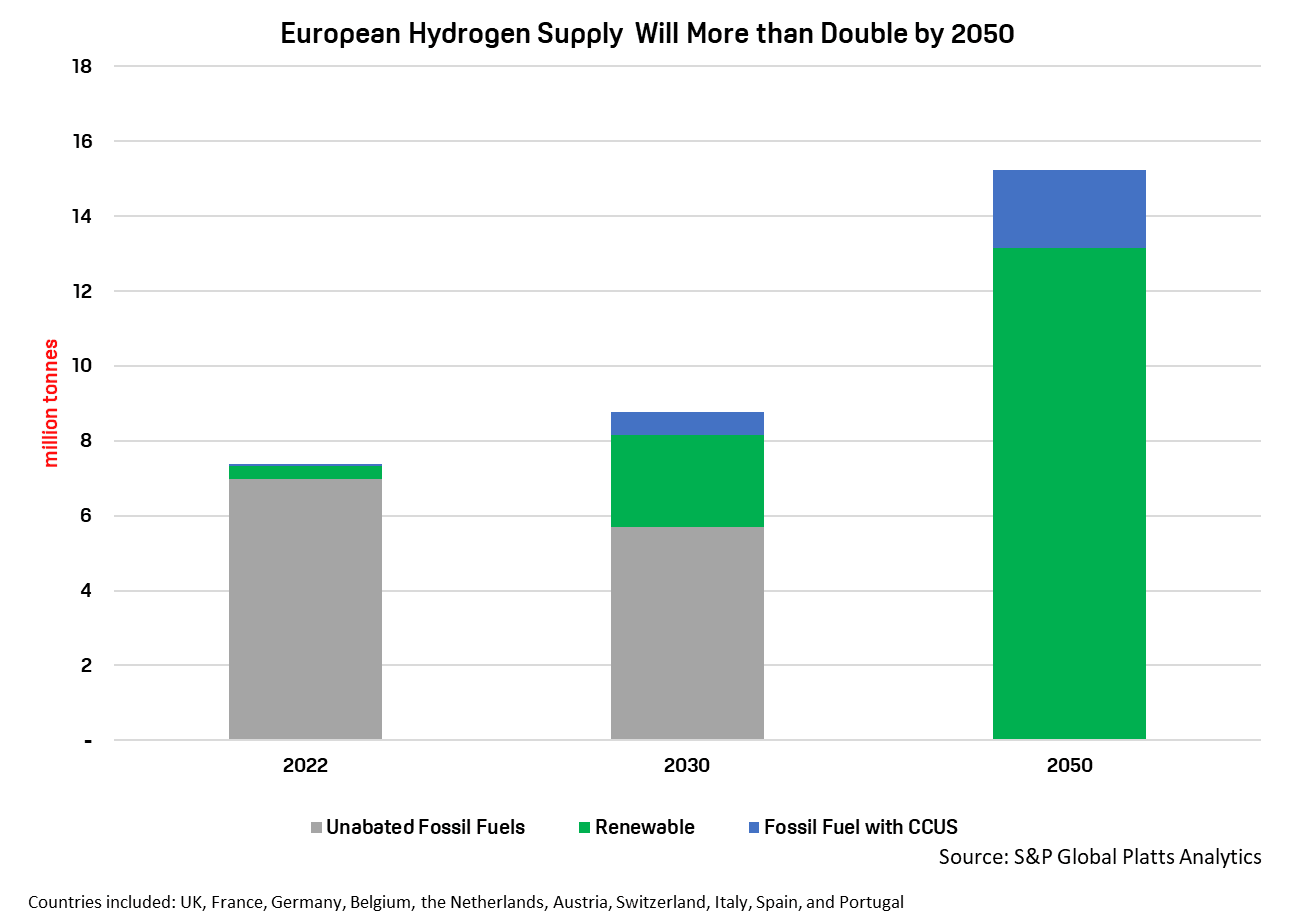

The other eight countries will rely primarily on traditional “grey” hydrogen production to meet demand in the first half of the forecast until green sources can be scaled to meet demand when it will likely play a larger role than other sources. The 10 European countries have 7 million tonnes of existing hydrogen demand in oil refining and in the production of ammonia for fertilizer. This production primarily comes from steam-methane reforming. Future hydrogen growth will come from the transportation and power generation sectors, the S&P Global Platts Analytics report said.

Hydrogen is the first element listed on the periodic table of elements, and as such, it is the most abundant element on the planet. Hydrogen can be produced from many sources, but it is primarily processed from natural gas production and used for oil refining and chemical production.

There are multiple production pathways to generate hydrogen, but there are three primary categories most referenced, each with various levels of emissions—grey, blue, and green, which are described below.

However, these color-based categories are quickly becoming passe. The next evolution for accurately and consistently assessing and monetizing the lower-carbon hydrogen supply will be the carbon-intensity calculation of the product, rather than its production process. Calculating CI of hydrogen production through standardized processes will enable a level playing field for global hydrogen supply, and it can be valued accordingly, say, industry participants.

Grey hydrogen is produced by the traditional process of steam reforming, but this method is not climate-friendly, as waste CO2 is released into the atmosphere.

Blue hydrogen is created using natural gas, but requires a carbon capture, utilization, and storage process (CCUS) to sequester and prevent most of the emissions from getting into the atmosphere. Blue hydrogen is expected to grow into a massive market in conjunction with CCUS investments, but some consider blue hydrogen a transition fuel until green supply becomes plentiful.

Green hydrogen is created using renewably generated electricity, such as wind or solar, to separate water molecules into hydrogen and oxygen. As such, this means green hydrogen is theoretically, completely free of emissions. The green hydrogen market, however, is exceedingly small. Less than 0.1% of global hydrogen production today comes from water electrolysis.

According to the Platts Analytics report, overall hydrogen demand will grow by 2.5 times current demand by 2050 in the 10 European countries assessed, driven by growth in transportation, power generation, and gas blending. The Platts Analytics forecast assumes production will come from both renewable electricity and fossil-fuel production with CCUS. Platts Analytics says both blue and green hydrogen markets are expected to grow considerably, but for green hydrogen to prosper in Europe and elsewhere, a massive scale-up of renewable electricity generation and infrastructure must occur. In short, vast amounts of green electricity are required to produce green hydrogen, and the blue hydrogen market is also large scale, requiring mega-tons-per-year of production in Europe alone to meet current and expected demand growth for hydrogen.

In addition, the EU has strongly emphasized that producers of hydrogen production must build dedicated renewable electricity capacity to meet the need for hydrogen production and that use of electricity for hydrogen production should not replace electricity that would have otherwise helped decarbonize the power system itself. This concept of ‘additionality’ means build your hydrogen infrastructure but also build your own power infrastructure to support it. Do not expect the existing power grid to support it, Robba said.

“Given the EU’s strict stance on additionality, Platts Analytics expects many of the region’s early projects to follow the dedicated renewables and electrolyzer business model, which has limited to no access to grid power,” Robba said. Part of the challenge for this renewable and electrolyzer model is that the electrolyzer process is highly inefficient, losing approximately 30 percent of production. As a result, the amount of renewable electricity required to produce hydrogen is enormous, the report said.

Oil majors and industrial gas companies are already producing hydrogen in Europe and elsewhere with existing infrastructure, the Platts Analytics report said, but many of these same companies have made or are making significant investment commitments to build additional hydrogen capacity.

The emerging clean hydrogen eco-system is fairly complex, so it will take numerous partnerships to bring most projects to life. We expect to see a flurry of announcements involving strategic partnerships necessary to build out the needed hydrogen infrastructure to meet climate objectives, both in Europe and elsewhere.

Part of the ecosystem important to leveraging and transporting hydrogen is the production and use of ammonia. Ammonia, made with clean hydrogen, can be an important part of the overall uptake of hydrogen due to its energy density, existing infrastructure, and non-carbon emitting nature when combusted.

Because ammonia is a much bigger molecule, and much easier to transport than hydrogen, ammonia production is a key enabler for hydrogen. By pairing hydrogen with ammonia, the hydrogen molecule can be transported more easily. Ammonia can also be used as a fuel for power generation and in marine transportation.

In a related effort, Platts launched a full suite of ammonia price assessments in October 2021 to complement its first-to-market hydrogen prices. The hydrogen prices provide a snapshot of the cost of production at key hubs and by using different production pathways including steam-methane reforming and electrolysis.

Download PDF