Including commentary from:

S&P Global Platts lithium prices up more than 200%, nickel costs rise nearly 35%, and cobalt climbed nearly 90% since August 2020

Battery costs comprise a significant portion of the cost of an EV (Platts estimates battery costs typically constitute 25% to 30% of EV costs, but could go as high as 50% of overall costs of a new EV). If battery costs continue to accelerate rapidly, they could pump the brakes on EV sales in price-sensitive markets such as the U.S. and Western Europe.

Global automakers want to avoid a repeat of the recent computer-chip outage that left their sales lots nearly empty and hurt revenue. They seek diversity of supply and cost management, so will continue to employ multiple options for battery technology. No manufacturer wants to be beholden to a single material, process, or source of supply.

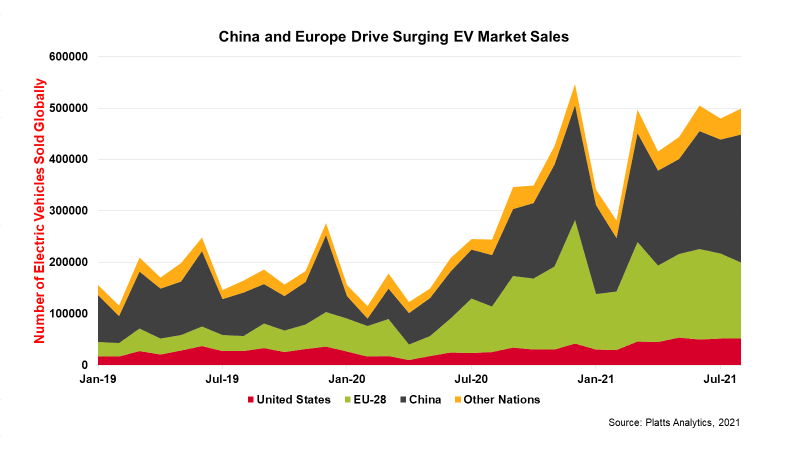

Driven mainly by Chinese and Western European buyers, global sales of plug-in EVs have more than tripled in just 12 months (from 146,000 units in July 2020, to 480,000 units in July 2021)—great news for automakers rapidly transitioning to EV fleets, but skyrocketing battery metals costs could threaten to pump the brakes on EV market demand, according to a new report from S&P Global Platts.

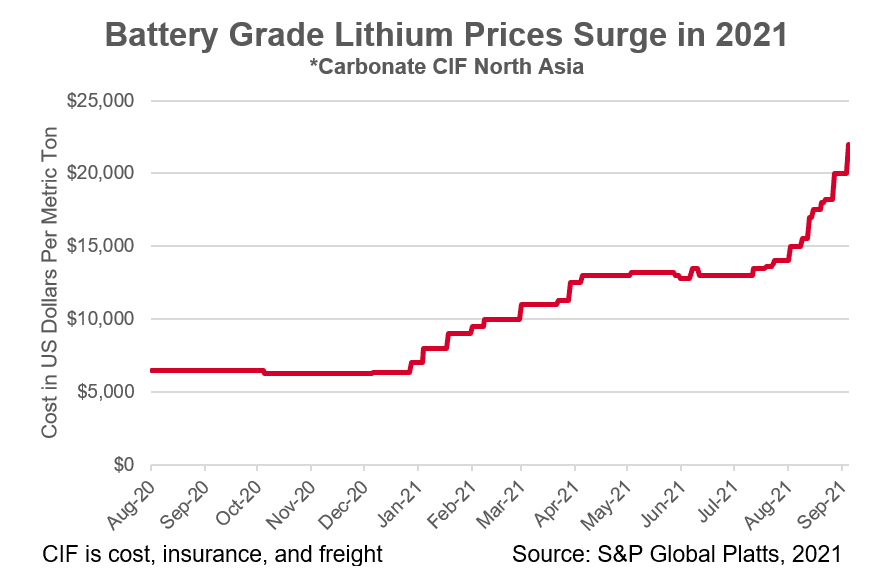

Due to this significant increase in electric vehicle sales, battery metals have surged in the past year, with lithium carbonate prices hitting an all-time high of $20,000/mt in September—an increase of more than 200% since August 2020. Prices for nickel increased nearly 35% during the past year, and cobalt prices have climbed nearly 90%. Chinese nickel sulfate has increased 39% since Platts started delivering price assessments for this metal in October 2020, and Chinese cobalt prices have risen close to 50% during the past year.

The increase in battery metal raw material prices has meant that cathode battery prices and price of battery storage have also climbed. The $/KWh raw material cost for nickel, manganese, and cobalt (NMC) 8:1:1 cathode battery alone has risen nearly 80% during the past year. Meanwhile, prices for an NCA battery, which has a higher percentage of cobalt, have increased about 80% during the past year, Platts said. While metals prices are up, estimated battery costs have risen more modestly—about 5%-7% in the past year, according to the S&P Global Platts Analytics report. This may not seem like much at the outset, but McCafferty said EV sales are sensitive to cost increases in some regions, more than others, and automakers and lithium suppliers are carefully watching their supply chains to ensure the balance doesn’t tip the scales too far and put the brakes on EV sales. “In the U.S. market, for example, a 5% increase in battery storage costs translates to about a 10% reduction in plug-in EV sales in 2022, which equates to roughly 54,000 vehicles,” McCafferty said. “In China, there is less sensitivity to cost due to regulatory mandates. With regards to Western Europe, you have a mix of market influencers, but consumers are certainly motivated by price. Significant price increases could cause some consumers to hit the brakes on purchasing a new EV.” In the short-term, S&P Global Platts Analytics Platts said, lithium chemical producers are happy to see both higher lithium demand and higher prices, but looking ahead, they are also reluctant to lose future market share due to persistent inventory constraints.

The dramatic increase in lithium demand during the past year means lithium now comprises a larger percentage of battery cathode costs. According to S&P Global Platts, lithium now constitutes 40% of NMC 8:1:1 cathode-battery costs-up from about 25% a year ago. For example, in LFP (lithium-iron-phosphate cathode batteries), lithium represents more than 95% of the overall cathode costs, as both phosphate and iron are more plentiful and thus cheaper alternatives to cobalt and nickel metals. The LFP chemistry has traditionally been used in stationary storage applications where the energy-to-weight ratio isn’t a concern. However, according to S&P Global Platts, auto manufacturers are increasingly looking to LFP batteries instead of NCM and NCA chemistries as a battery option. Both China’s Wuling, which manufacturers the Huongguang Mini—the most popular EV in China; as well as Tesla, are now both using LFP batteries in the Chinese manufacturing of their vehicles. With that in mind, during the past year, LFP has taken the lead in the key Chinese battery market, S&P Global Platts Analytics said. In July, 9.3 GWh of LFP batteries were produced, compared with 2.7 GWh in July 2020—an increase of more than 300% production in one year. NMC battery cathode costs have also climbed, growing from 3.2GWh in July 2020, to 8 GWh in July 2021—a production increase of more than 250%, year-over-year. “Supply constraints for computer chips impacted global automotive supply chains in recent months, leaving many dealers with sparse inventory and near-empty sales lots. Due to the escalating costs of critical battery metals and increasing competition for those metals, auto manufacturers are looking to diversify their battery chemistries to avoid a similar shortage,” McCafferty said. They have several critical reasons for doing so—not only to achieve greater energy supply ratios through advancing battery technology, but also to manage the risks associated with material cost and supply,” McCafferty said. “No auto manufacturer wants to be beholden to any one material, process, or source of supply, so diversification offers greater protection to their business continuity and revenue.”